Global Parallel Computing Market

Market Size in USD Billion

USD

179.93 Billion

USD

281.42 Billion

2025

2033

USD

179.93 Billion

USD

281.42 Billion

2025

2033

| 2026 - 2033 | |

| USD 179.93 Billion | |

| USD 281.42 Billion | |

| % | |

|

What is the Parallel Computing Market Size and Growth Rate?

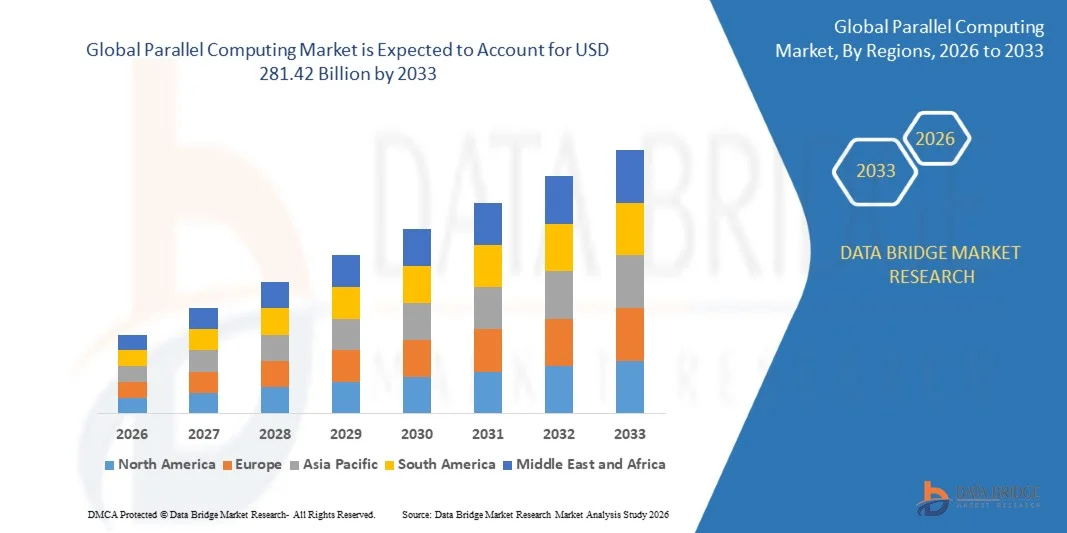

- As per Data Bridge Market Research Analysis, the global parallel computing market size was valued at USD 179.93 billion in 2025 and is expected to reach USD 281.42 billion by 2033, at a CAGR of 5.75% during the forecast period

- The market growth is largely fuelled by the rising demand for high-performance computing in data-intensive applications such as artificial intelligence, machine learning, and big data analytics

- Increasing adoption of cloud computing, GPU acceleration, and multi-core processors across enterprises and research institutions is driving the parallel computing market

Market Size & Forecast

- Global Market Value (2025): USD 179.93 billion in 2025

- Expected Market Value (2033): USD 281.42 billion by 2033

- Forecast CAGR (2026–2033): 5.75%

Parallel Computing Market Analysis

- The parallel computing market is witnessing significant growth due to technological advancements in hardware and software, enabling faster computation and improved efficiency

- Rising focus on real-time data processing, predictive analytics, and complex simulations across various sectors is fostering the adoption of parallel computing systems

- North America dominated the parallel computing market with the largest revenue share of 28.3% in 2025, driven by the early adoption of high-performance computing systems and increasing investments in AI, machine learning, and data analytics across enterprises

- Asia-Pacific region is expected to witness the highest growth rate in the global parallel computing market, driven by rapid digitalization, rising investments in AI and HPC infrastructure, expansion of cloud services, and the emergence of technology hubs in China, Japan, and India

- The hardware segment held the largest market revenue share of 57% in 2025, driven by the increasing demand for high-performance computing systems and specialized processors that can handle complex computations efficiently. Hardware solutions, including GPUs, CPUs, and FPGAs, are widely adopted across enterprises and research institutions to accelerate data processing and enhance overall system performance

Report Scope and Parallel Computing Market Segmentation

|

Attributes |

Parallel Computing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

What is the Key Trend in the Parallel Computing Market?

“Rising Adoption Of High-Performance Computing And Big Data Analytics”

- The growing reliance on high-performance computing (HPC) systems and big data analytics is significantly shaping the parallel computing market, as organizations increasingly require faster processing capabilities for complex computations. Parallel computing architectures are gaining traction due to their ability to perform multiple tasks simultaneously, reducing processing time and improving operational efficiency. This trend strengthens their adoption across IT, finance, healthcare, and scientific research industries, encouraging vendors to innovate with new scalable and energy-efficient solutions

- Increasing emphasis on artificial intelligence (AI), machine learning (ML), and cloud computing has accelerated the demand for parallel computing systems. Enterprises and research institutions are leveraging parallel computing to process large datasets efficiently, enabling faster insights and improved decision-making. The growing integration of parallel computing with AI frameworks is also fostering partnerships between hardware and software providers to enhance performance and functionality

- Cloud-based deployment and virtualization trends are influencing purchasing decisions, with companies seeking flexible, on-demand computing resources. These factors are helping organizations optimize costs, increase scalability, and accelerate time-to-market, while also driving the adoption of hybrid and multi-cloud architectures. Vendors are increasingly promoting parallel computing capabilities to highlight efficiency and performance benefits, appealing to technology-driven consumers

- For instance, in 2024, IBM in the U.S. and Fujitsu in Japan expanded their supercomputing portfolios by integrating advanced parallel computing technologies for AI and scientific simulations. These upgrades were introduced to meet growing demand for faster processing and higher computational accuracy, with deployment across enterprise, research, and cloud platforms. The products were also marketed as energy-efficient and high-performance solutions, enhancing client adoption and loyalty

- While demand for parallel computing is growing, sustained market expansion depends on continuous R&D, energy-efficient designs, and cost-effective deployment. Vendors are also focusing on improving scalability, software-hardware integration, and developing innovative solutions that balance performance, cost, and sustainability for broader adoption

Parallel Computing Market Dynamics

Driver

“Growing Demand For High-Performance Computing And Big Data Analytics”

- Rising enterprise and research requirements for faster data processing and high-performance computation is a major driver for the parallel computing market. Organizations are increasingly replacing traditional computing systems with parallel architectures to enhance processing efficiency and reduce latency. This trend also encourages research into specialized hardware accelerators and optimized parallel algorithms, supporting market diversification

- Expanding applications in AI, machine learning, cloud computing, scientific simulations, and financial modeling are influencing market growth. Parallel computing allows simultaneous task execution, reducing computation time while maintaining accuracy and reliability. The increasing adoption of data-intensive applications globally further reinforces this trend

- Technology vendors are actively promoting parallel computing solutions through software optimization, hardware innovations, and ecosystem partnerships. These efforts are supported by growing enterprise demand for real-time analytics and predictive modeling, and they also encourage collaborations between software developers and hardware manufacturers to improve system performance and energy efficiency

- For instance, in 2023, NVIDIA in the U.S. and Atos in France reported increased deployment of parallel computing frameworks in AI training and high-performance simulations. This expansion followed higher demand for faster processing and computational scalability, driving enterprise adoption and competitive differentiation. Both companies also emphasized energy efficiency and reduced operational costs in marketing campaigns to strengthen client trust and engagement

- Although rising HPC and AI trends support growth, wider adoption depends on cost optimization, energy-efficient designs, and compatibility with existing IT infrastructure. Investment in scalable systems, advanced software development, and integration with cloud platforms will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

“High Implementation Costs And Technical Complexity”

- The relatively high cost of parallel computing hardware and software compared to conventional systems remains a key challenge, limiting adoption among price-sensitive enterprises. Specialized processors, interconnects, and software frameworks contribute to elevated capital expenditures, affecting market penetration in emerging regions. Organizations may delay adoption due to budget constraints and ROI uncertainties

- Technical complexity and limited skilled workforce also affect market growth, as parallel computing requires expertise in programming models, algorithm optimization, and system integration. Limited availability of trained professionals may slow deployment, particularly in developing countries where IT infrastructure is still evolving

- Infrastructure requirements and power consumption challenges further impact adoption, as high-performance parallel systems demand significant energy and cooling resources. Data centers need to optimize physical space, networking, and thermal management, increasing operational costs

- For instance, in 2024, several research institutions in Southeast Asia and Latin America reported slower deployment of parallel computing clusters due to high hardware costs, power constraints, and limited technical expertise, affecting overall system utilization and project timelines

- Overcoming these challenges will require investment in cost-effective hardware, energy-efficient designs, and training programs to build skilled technical resources. Collaboration with cloud service providers, educational institutions, and technology partners can help unlock the long-term growth potential of the global parallel computing market. Furthermore, developing hybrid solutions and user-friendly frameworks will be essential for widespread adoption

Parallel Computing Market Scope

The market is segmented on the basis of component, deployment, vertical, and technology.

- By Component

On the basis of component, the parallel computing market is segmented into software, hardware, and services. The hardware segment held the largest market revenue share of 57% in 2025, driven by the increasing demand for high-performance computing systems and specialized processors that can handle complex computations efficiently. Hardware solutions, including GPUs, CPUs, and FPGAs, are widely adopted across enterprises and research institutions to accelerate data processing and enhance overall system performance.

The software segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising need for optimized parallel computing frameworks, programming models, and APIs that allow efficient workload distribution and task execution. Software solutions facilitate scalability, reduce computation time, and enable seamless integration with cloud platforms, making them highly valuable for AI, big data analytics, and scientific simulations.

- By Deployment

On the basis of deployment, the market is segmented into cloud, on-premises, and hybrid. The cloud segment held the largest share in 2025, owing to its flexibility, scalability, and cost-effectiveness for enterprises seeking high-performance computing capabilities without investing heavily in physical infrastructure. Cloud-based parallel computing allows organizations to access powerful resources on-demand, supporting faster analytics and AI workloads.

The hybrid segment is expected to witness the fastest growth from 2026 to 2033, fueled by the increasing need for organizations to balance on-premises infrastructure with cloud capabilities. Hybrid deployment enables efficient workload management, improved security, and better cost optimization, making it a preferred choice for enterprises with complex computational requirements.

- By Vertical

On the basis of vertical, the market is segmented into BFSI, healthcare & life sciences, government, manufacturing & automotive, IT & telecom, and others. The IT & telecom vertical held the largest market share of 23.2% in 2025, driven by the high adoption of parallel computing for data centers, AI-driven applications, and large-scale network management. Parallel computing enables these sectors to process massive datasets quickly and enhance service delivery.

The healthcare & life sciences vertical is expected to witness the fastest growth from 2026 to 2033, due to the increasing need for parallel computing in genomics, drug discovery, and medical imaging applications. Advanced computational capabilities help accelerate research, reduce analysis time, and support personalized healthcare solutions.

- By Technology

On the basis of technology, the market is segmented into programming models & APIs, accelerator microarchitecture/ISA, interconnect & fabric technologies, orchestration & middleware, libraries & kernels, and others. The accelerator microarchitecture/ISA segment held the largest share in 2025, fueled by growing deployment of GPUs, TPUs, and FPGAs that significantly enhance computation speed and efficiency.

The programming models & APIs segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the need for standardized development tools and efficient workload distribution across parallel computing architectures. These technologies simplify development, improve performance, and enable seamless integration with cloud and on-premises environments, supporting AI, ML, and HPC applications.

Which Region Holds the Largest Share of the Parallel Computing Market?

- North America dominated the parallel computing market with the largest revenue share of 28.3% in 2025, driven by the early adoption of high-performance computing systems and increasing investments in AI, machine learning, and data analytics across enterprises

- The region’s strong IT infrastructure, presence of major technology vendors, and high demand for cloud-based services are fueling growth

- Businesses and research institutions increasingly rely on parallel computing for complex simulations, data processing, and scientific research, establishing North America as a key hub for market expansion

U.S. Parallel Computing Market Insight

The U.S. parallel computing market captured the largest revenue share in 2025 within North America, supported by the country’s leadership in cloud computing, AI adoption, and supercomputing infrastructure. Organizations across BFSI, healthcare, manufacturing, and government sectors are integrating parallel computing to improve computational efficiency, reduce processing times, and accelerate innovation. The presence of leading hardware and software providers, alongside continuous R&D investments, strengthens the U.S. position in the global parallel computing market.

Europe Parallel Computing Market Insight

The Europe parallel computing market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing digitization, rising AI and big data adoption, and government initiatives supporting high-performance computing. The region is focusing on modernizing IT infrastructure across industries, including automotive, healthcare, and manufacturing. European enterprises are increasingly deploying parallel computing systems to enhance data processing capabilities, support research, and optimize industrial operations.

U.K. Parallel Computing Market Insight

The U.K. parallel computing market is projected to grow rapidly from 2026 to 2033, fueled by advancements in AI, machine learning, and cloud computing adoption. Increasing investments in fintech, healthcare analytics, and government research programs are contributing to market expansion. The integration of parallel computing solutions enhances computational speed, accuracy, and efficiency, meeting the growing demand for data-driven decision-making and advanced simulations in both public and private sectors.

Germany Parallel Computing Market Insight

The Germany parallel computing market is expected to witness significant growth from 2026 to 2033, driven by robust R&D initiatives, industrial automation, and demand for high-performance computing in manufacturing and automotive sectors. Germany’s well-developed technology ecosystem and focus on innovation enable enterprises to adopt parallel computing for process optimization, simulation, and predictive analytics. The growing adoption of cloud-based HPC solutions further accelerates market expansion in the country.

Asia-Pacific Parallel Computing Market Insight

The Asia-Pacific parallel computing market is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing investments in AI, cloud infrastructure, and digital transformation across China, Japan, India, and South Korea. The region is experiencing rising demand for high-performance computing in IT services, research institutions, and industrial applications. In addition, the emergence of APAC as a manufacturing and technology hub for computing hardware and software is driving the accessibility and adoption of parallel computing solutions.

Japan Parallel Computing Market Insight

The Japan parallel computing market is projected to grow rapidly from 2026 to 2033 due to the country’s strong focus on AI, robotics, and supercomputing initiatives. Japanese enterprises are increasingly leveraging parallel computing for advanced simulations, scientific research, and data-intensive applications. Investments in HPC infrastructure, cloud-based computing, and R&D projects are expected to boost market expansion, particularly in manufacturing, healthcare, and government research sectors.

China Parallel Computing Market Insight

The China parallel computing market accounted for the largest revenue share in Asia-Pacific in 2025, driven by the country’s expanding IT infrastructure, rapid digitization, and increasing adoption of cloud-based and high-performance computing systems. The growing focus on AI, big data analytics, and industrial automation supports market growth. Strong government initiatives, investment in supercomputing centers, and availability of cost-effective computing hardware are further propelling the market in China.

Which are the Top Companies in Parallel Computing Market?

The Parallel Computing industry is primarily led by well-established companies, including:

- Amazon Web Services, Inc. (U.S.)

- Apple Inc. (U.S.)

- Atos SE (U.K.)

- Dell Inc. (U.S.)

- Fujitsu (U.K.)

- Hewlett Packard Enterprise Development LP (U.S.)

- IBM Corporation (U.S.)

- Intel Corporation (U.S.)

- Microsoft (U.S.)

- NVIDIA Corporation (U.S.)

What are the Recent Developments in Parallel Computing Market?

- In March 2025, Quantum Machines launched the NVIDIA DGX Quantum Early Customer Program, introducing a tightly integrated quantum-classical computing platform. The solution combines Quantum Machines’ OPX1000 modular quantum control system with NVIDIA’s GH200 Grace Hopper Superchips, delivering ultra-low latency of under 4 microseconds between quantum control and AI supercomputers. This innovation enhances computational efficiency for quantum and AI workloads, positioning the company at the forefront of hybrid computing solutions and strengthening its presence in high-performance computing markets

- In November 2024, Eviden, part of the Atos Group, unveiled BXI v3, the third-generation European scale-out networking technology designed for AI and HPC workloads. Developed with the French Atomic Energy Commission (CEA), it integrates SmartNIC technology and application protocol offloading to optimize CPU and GPU utilization, improving application execution speed by up to 35% while reducing total cost of ownership. This development addresses networking bottlenecks, enhancing performance and efficiency for AI and high-performance computing applications

- In November 2023, Fujitsu introduced a novel technology to dynamically optimize CPU and GPU usage in real time, prioritizing processes with higher execution efficiency. Integrated into an upcoming AI-powered workload broker, this innovation helps allocate computational resources based on factors such as computation time, accuracy, and cost. The technology aims to alleviate the global GPU shortage caused by surging demand from generative AI and deep learning, boosting performance and efficiency across AI and HPC workloads while enabling more cost-effective resource management

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.