Global Truck As A Service Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

41.52 Billion

USD

237.37 Billion

2025

2033

USD

41.52 Billion

USD

237.37 Billion

2025

2033

| 2026 –2033 | |

| USD 41.52 Billion | |

| USD 237.37 Billion | |

| % | |

|

Segmentación del mercado global de camiones como servicio, por servicio (suscripción de vehículos y pago por uso, arrendamiento completo y gestión de flotas, capacidad de carga como servicio [FaaS], camiones pesados de flota dedicada [HDT] y otros servicios), tipo de camión (camiones pesados [HDT], camiones medianos [MDT] y camiones ligeros [LDT]), propulsión (motor de combustión interna [ICE], vehículo eléctrico de batería [BEV], híbrido y vehículo eléctrico de pila de combustible [FCEV]), usuario final (logística y transporte, comercio minorista y comercio electrónico, fabricación e industria, construcción y minería, y otros usuarios finales) - Tendencias de la industria y pronóstico hasta 2033

Tamaño del mercado de camiones como servicio

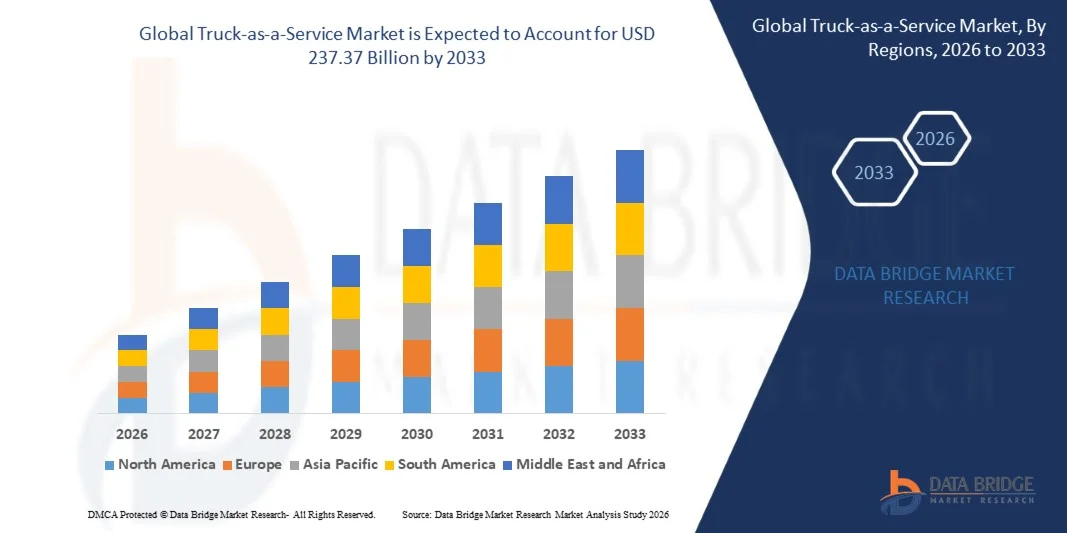

- El tamaño del mercado global de camiones como servicio se valoró en USD 41,52 mil millones en 2025 y se espera que alcance los USD 237,37 mil millones para 2033 , con una CAGR del 24,35% durante el período de pronóstico.

- El crecimiento del mercado está impulsado en gran medida por el cambio creciente hacia modelos logísticos con activos livianos y la creciente necesidad de optimización de costos en las operaciones de carga y transporte, lo que alienta a los operadores de flotas a alejarse de la propiedad tradicional de camiones.

- Además, la creciente demanda de soluciones de transporte flexibles, escalables y basadas en tecnología, combinada con avances en telemática, plataformas de gestión de flotas y modelos de movilidad basados en servicios, está acelerando la adopción de ofertas de camiones como servicio y apoyando la expansión general del mercado.

Análisis del mercado de camiones como servicio

- Truck-as-a-Service, que ofrece acceso combinado a vehículos, mantenimiento, cumplimiento y gestión digital de flotas, se está convirtiendo en una solución esencial para los usuarios logísticos, minoristas e industriales que buscan eficiencia operativa y una reducción del gasto de capital.

- La creciente adopción de modelos de transporte basados en suscripción y pago por uso, junto con la creciente presión para mejorar la utilización de la flota y gestionar la demanda fluctuante de carga, está impulsando significativamente el crecimiento del mercado de camiones como servicio.

- Europa dominó el mercado de camiones como servicio con una participación del 35% en 2025, debido a la fuerte adopción de modelos de transporte con activos livianos, regulaciones estrictas sobre emisiones y el rápido cambio hacia soluciones de movilidad compartida y sustentable.

- Se espera que Asia-Pacífico sea la región de más rápido crecimiento en el mercado de camiones como servicio durante el período de pronóstico debido a la rápida urbanización, la expansión de la actividad de comercio electrónico y la creciente demanda de soluciones logísticas escalables.

- El segmento de suscripción de vehículos y pago por uso dominó el mercado con una cuota de mercado del 32,6 % en 2025, gracias a su alta flexibilidad y rentabilidad para los operadores de flotas que se enfrentan a la fluctuación de la demanda de carga. Este modelo permite a las empresas acceder a camiones sin compromisos de propiedad a largo plazo, lo que reduce la inversión inicial de capital y mejora la gestión del flujo de caja. La sólida adopción entre los proveedores de logística de pequeño y mediano tamaño, junto con la creciente aceptación de los precios basados en el uso, consolidó la posición de liderazgo del segmento.

Alcance del informe y segmentación del mercado de camiones como servicio

|

Atributos |

Perspectivas clave del mercado de camiones como servicio |

|

Segmentos cubiertos |

|

|

Países cubiertos |

América del norte

Europa

Asia-Pacífico

Oriente Medio y África

Sudamerica

|

|

Actores clave del mercado |

|

|

Oportunidades de mercado |

|

|

Conjuntos de información de datos de valor añadido |

Además de los conocimientos del mercado, como el valor de mercado, la tasa de crecimiento, los segmentos del mercado, la cobertura geográfica, los actores del mercado y el escenario del mercado, el informe de mercado elaborado por el equipo de investigación de mercado de Data Bridge incluye un análisis experto en profundidad, análisis de importación/exportación, análisis de precios, análisis de consumo de producción y análisis pestle. |

Tendencias del mercado de camiones como servicio

“Cambio hacia modelos de transporte con pocos activos y basados en suscripciones”

- Una tendencia importante en el mercado de camiones como servicio es la creciente transición hacia modelos de transporte con pocos activos y basados en suscripción, impulsada por operadores de flotas que buscan reducir la inversión de capital y mejorar la flexibilidad financiera. Las empresas se alejan cada vez más de la propiedad total de los camiones y, en su lugar, adoptan el acceso a vehículos basado en servicios, con mantenimiento, seguros y herramientas digitales para la flota.

- Por ejemplo, Volvo Trucks ha ampliado su oferta de Volvo on Demand para ofrecer a las flotas acceso flexible a camiones sin compromisos de propiedad a largo plazo. Estos modelos ayudan a los operadores logísticos a gestionar volúmenes de carga fluctuantes, manteniendo al mismo tiempo unos costes operativos predecibles.

- La demanda de transporte por suscripción está aumentando en la logística regional y de última milla, donde la variabilidad estacional de la demanda requiere soluciones de flota escalables. Esta tendencia favorece una mejor utilización de la flota y reduce los riesgos de inactividad de los activos para los operadores.

- Las plataformas digitales que permiten la disponibilidad de vehículos en tiempo real, el seguimiento del uso y la transparencia de costes están reforzando el atractivo de los modelos de camiones como servicio. Estas tecnologías mejoran la visibilidad operativa y facilitan la toma de decisiones basada en datos.

- Los objetivos de sostenibilidad también influyen en esta tendencia, ya que los modelos basados en servicios simplifican el acceso a camiones eléctricos y de bajas emisiones sin una gran inversión inicial. Esto fomenta una adopción más rápida de flotas más limpias.

- En general, el cambio hacia el transporte de activos livianos está redefiniendo las estructuras de propiedad de las flotas y acelerando la adopción del camión como servicio como estrategia logística central.

Dinámica del mercado de camiones como servicio

Conductor

Creciente demanda de operaciones de flotas rentables y flexibles

- La creciente necesidad de operaciones de flotas rentables y flexibles es un factor clave en el mercado de camiones como servicio. Las empresas de logística y transporte se enfrentan al aumento de los costos de combustible, los gastos de mantenimiento y los requisitos de cumplimiento normativo, lo que hace que los modelos de propiedad tradicionales sean menos atractivos.

- Por ejemplo, los grandes proveedores de logística están adoptando soluciones integrales de arrendamiento y gestión de flotas de empresas como Daimler Truck para estabilizar los costos operativos y mejorar el tiempo de actividad de la flota. Estos servicios reducen la incertidumbre financiera y la carga operativa.

- El crecimiento del comercio electrónico y los modelos de entrega justo a tiempo requieren flotas que puedan escalar rápidamente en respuesta a las fluctuaciones de la demanda. El servicio de camiones permite a las empresas aumentar o reducir su capacidad sin compromisos financieros a largo plazo.

- Los operadores de flotas también priorizan la eficiencia operativa, el mantenimiento predictivo y la optimización de rutas, aspectos cada vez más integrados en los modelos de transporte basados en servicios. Esto mejora la productividad y reduce el tiempo de inactividad.

- La necesidad de gastos mensuales predecibles y una mejor gestión del flujo de caja continúa fortaleciendo la demanda de ofertas de Truck-as-a-Service, posicionando la flexibilidad y el control de costos como los principales impulsores del crecimiento.

Restricción/Desafío

Alta complejidad en la integración de flotas y estandarización de servicios

- El mercado de camiones como servicio se enfrenta a desafíos relacionados con la complejidad de integrar vehículos, telemática, servicios de mantenimiento y plataformas digitales en un modelo operativo unificado. La gestión de múltiples componentes de servicio en diversas flotas dificulta la implementación para proveedores y usuarios.

- Por ejemplo, la integración de sistemas telemáticos de terceros, infraestructura de carga y software de gestión de flotas en flotas mixtas de camiones requiere una coordinación y una alineación técnica significativas. Estos desafíos pueden ralentizar la adopción y aumentar los plazos de implementación.

- Las diferencias en los requisitos regulatorios, las expectativas de servicio y las prácticas operativas entre regiones complican aún más los esfuerzos de estandarización. Los proveedores deben personalizar sus ofertas, lo que aumenta la complejidad operativa.

- Garantizar una calidad de servicio consistente en flotas grandes y geográficamente dispersas sigue siendo un desafío para los proveedores de camiones como servicio. La variabilidad en las redes de mantenimiento y la disponibilidad de la infraestructura pueden afectar la confiabilidad.

- Estos desafíos de integración y estandarización presionan a los proveedores de servicios para que inviertan en plataformas interoperables y marcos de servicios escalables para respaldar el crecimiento sostenido del mercado.

Alcance del mercado de camiones como servicio

El mercado está segmentado según el servicio, el tipo de camión, la propulsión y el usuario final.

- Por servicio

En función del servicio, el mercado de camiones como servicio se segmenta en suscripción de vehículos y pago por uso, leasing integral y gestión de flotas, capacidad de carga como servicio (FaaS), flota dedicada de camiones pesados (HDT) y otros servicios. El segmento de suscripción de vehículos y pago por uso dominó el mercado con la mayor participación, un 32,6%, en 2025, gracias a su alta flexibilidad y rentabilidad para los operadores de flotas que enfrentan una demanda de carga fluctuante. Este modelo permite a las empresas acceder a camiones sin compromisos de propiedad a largo plazo, lo que reduce la inversión inicial y mejora la gestión del flujo de caja. La sólida adopción entre los proveedores de logística de pequeño y mediano tamaño, junto con la creciente aceptación de los precios basados en el uso, consolidó el liderazgo del segmento en el mercado.

Se proyecta que el segmento de leasing y gestión de flotas de servicio completo registrará el mayor crecimiento entre 2026 y 2033, impulsado por la creciente demanda de soluciones integrales para flotas. Las empresas prefieren cada vez más externalizar el mantenimiento, el cumplimiento normativo, la telemática y la gestión del ciclo de vida de los vehículos para mejorar la eficiencia operativa y el tiempo de actividad de la flota. La creciente complejidad de las operaciones de flotas y la necesidad de costes operativos predecibles están acelerando la adopción de modelos de servicio completo entre los grandes usuarios logísticos e industriales.

- Por tipo de camión

Según el tipo de camión, el mercado se clasifica en camiones pesados (HDT), camiones medianos (MDT) y camiones ligeros (LDT). El segmento de camiones pesados representó la mayor participación en los ingresos en 2025, debido a su amplio uso en el transporte de mercancías de larga distancia, la logística interurbana y el transporte industrial. Los HDT son preferidos por su alta capacidad de carga útil y durabilidad, lo que los hace cruciales para las redes logísticas a gran escala. Los modelos de camiones como servicio (CaaS) permiten a los operadores implementar HDT sin una gran inversión inicial, lo que mejora la eficiencia del capital. La fuerte demanda del comercio transfronterizo y el transporte de mercancías impulsado por la infraestructura respaldan el continuo dominio. Los operadores de flotas también se benefician del mantenimiento integrado y la garantía de disponibilidad de los HDT.

Se espera que el segmento de camiones de servicio mediano experimente el mayor crecimiento durante el período de pronóstico, impulsado por la expansión de las redes de distribución urbanas y regionales. Los MDT se utilizan cada vez más para la logística de última milla y media milla debido a su equilibrio entre capacidad de carga útil y maniobrabilidad. El rápido crecimiento de los centros regionales de cumplimiento de comercio electrónico impulsa una mayor adopción de modelos de servicio basados en MDT. Las empresas prefieren las suscripciones a MDT para abordar las restricciones de entrega urbana y optimizar costos. La creciente demanda de flotas de entrega flexibles en ciudades de nivel 2 y 3 acelera aún más el crecimiento.

- Por propulsión

En función de la propulsión, el mercado de camiones como servicio se segmenta en motores de combustión interna (ICE), vehículos eléctricos de batería (BEV), híbridos y vehículos eléctricos de pila de combustible (FCEV). El segmento de ICE dominó el mercado en 2025, gracias a su consolidada infraestructura de abastecimiento y a la amplia familiaridad de la flota. Los camiones ICE siguen siendo la opción preferida para el transporte de mercancías de larga distancia y cargas pesadas donde la infraestructura de carga es limitada. Los menores costes de adquisición y la probada fiabilidad de su rendimiento contribuyen a su continua adopción. Muchos operadores de flotas confían en modelos de servicio basados en ICE para garantizar la continuidad operativa en diversas geografías. La disponibilidad de redes de mantenimiento cualificadas refuerza aún más su dominio.

Se prevé que el segmento de vehículos eléctricos de batería crezca a su ritmo más rápido entre 2026 y 2033, impulsado por el endurecimiento de las regulaciones sobre emisiones y la creciente presión sobre los costes del combustible. Las ofertas de camiones como servicio (VEB) basadas en VEB permiten a las empresas avanzar hacia la sostenibilidad sin una gran inversión de capital. Los incentivos gubernamentales y los objetivos corporativos de descarbonización aceleran la adopción de VEB en la logística urbana y regional. La reducción de los costes de operación y mantenimiento aumenta los beneficios económicos a largo plazo. La expansión de la infraestructura de carga y los avances en la autonomía de las baterías impulsan aún más el rápido crecimiento.

- Por el usuario final

Según el usuario final, el mercado se segmenta en logística y transporte, comercio minorista y comercio electrónico, manufactura e industria, construcción y minería, y otros. El segmento de logística y transporte registró la mayor cuota de mercado en 2025, impulsado por la alta utilización de la flota y la demanda de soluciones de transporte rentables. Las empresas de logística adoptan cada vez más el sistema "Truck-as-a-Service" para mejorar la escalabilidad y reducir los tiempos de inactividad. Los modelos de flota externalizados ayudan a los operadores a gestionar los picos de demanda y la variabilidad de las rutas con mayor eficacia. La integración de herramientas telemáticas y de optimización de rutas mejora aún más la eficiencia operativa. El crecimiento continuo del transporte de mercancías nacional e internacional refuerza el dominio de este segmento.

Se proyecta que el segmento minorista y de comercio electrónico experimente el mayor crecimiento durante el período de pronóstico, impulsado por la rápida expansión de las compras en línea y los modelos de distribución omnicanal. Las empresas de comercio electrónico confían en soluciones flexibles de transporte por carretera para gestionar las operaciones de última milla y logística inversa. El sistema "Camión como Servicio" permite a los minoristas ampliar sus flotas durante periodos promocionales sin compromisos de propiedad a largo plazo. La creciente demanda de plazos de entrega más rápidos acelera su adopción. El auge de los centros logísticos urbanos refuerza aún más las sólidas perspectivas de crecimiento.

Análisis regional del mercado de camiones como servicio

- Europa dominó el mercado de camiones como servicio con la mayor participación en los ingresos del 35 % en 2025, impulsada por la fuerte adopción de modelos de transporte con activos livianos, estrictas regulaciones de emisiones y el rápido cambio hacia soluciones de movilidad compartida y sustentable.

- Los operadores de flotas de toda la región prefieren cada vez más Truck-as-a-Service para reducir el gasto de capital, garantizar el cumplimiento normativo y acelerar la transición hacia camiones eléctricos y de bajas emisiones.

- Este dominio se ve respaldado además por redes logísticas transfronterizas bien desarrolladas, una alta penetración de servicios de arrendamiento de flotas y la adopción de telemática avanzada y gestión de flotas, lo que posiciona a Europa como un mercado maduro e impulsado por la innovación.

Análisis del mercado alemán de camiones como servicio

El mercado alemán de camiones como servicio representó la mayor participación en Europa en 2025, gracias a la sólida base industrial del país y su liderazgo en logística e innovación automotriz. Los operadores de flotas alemanes priorizan la eficiencia operativa, el mantenimiento predictivo y la sostenibilidad, lo que impulsa la demanda de soluciones integrales de leasing y gestión de flotas. La presencia de importantes centros logísticos y un fuerte enfoque en la reducción de las emisiones de carbono impulsan aún más la expansión del mercado.

Análisis del mercado de camiones como servicio en el Reino Unido

Se proyecta que el mercado británico de camiones como servicio (CAGR) crezca a una tasa de crecimiento anual compuesta (TCAC) constante durante el período de pronóstico, impulsado por la creciente demanda de soluciones de transporte flexibles y la creciente adopción de modelos de transporte por carretera de pago por uso y suscripción. El crecimiento del comercio electrónico y las redes de reparto urbano incentiva a las empresas a evitar la propiedad de flotas a largo plazo. La presión regulatoria para reducir las emisiones y la congestión también impulsa la adopción de camiones basados en servicios.

Perspectiva del mercado de camiones como servicio en América del Norte

El mercado norteamericano de camiones como servicio (Truck-as-a-Service) posee una cuota de mercado sustancial, impulsada por los altos volúmenes de carga, la demanda de transporte de larga distancia y la adopción generalizada de modelos de externalización de flotas. Los proveedores de logística de la región aprovechan el transporte por carretera basado en servicios para gestionar los costes operativos y optimizar la utilización de la flota. Una sólida infraestructura digital y el análisis avanzado de flotas impulsan aún más el crecimiento del mercado.

Análisis del mercado de camiones como servicio en Asia-Pacífico

Se prevé que el mercado de camiones como servicio (CAGR) de Asia-Pacífico experimente la tasa de crecimiento anual compuesta (TCAC) más rápida entre 2026 y 2033, impulsado por la rápida urbanización, la expansión del comercio electrónico y la creciente demanda de soluciones logísticas escalables. Las empresas de las economías emergentes están adoptando el transporte por carretera basado en servicios para evitar los elevados costos iniciales de los vehículos. Las inversiones gubernamentales en infraestructura logística y movilidad inteligente aceleran el crecimiento regional.

Análisis del mercado de camiones como servicio en China

China dominó el mercado de camiones como servicio en Asia-Pacífico en 2025, gracias a su extensa red logística, su amplia base de fabricación y la rápida adopción de plataformas digitales de transporte. El impulso hacia una logística inteligente y soluciones de transporte rentables impulsa una fuerte demanda de modelos de camiones como servicio. El creciente énfasis en la reducción de emisiones y la modernización de la flota contribuye aún más a la expansión del mercado.

Cuota de mercado de camiones como servicio

La industria de camiones como servicio está liderada principalmente por empresas bien establecidas, entre las que se incluyen:

- Daimler Truck AG (Alemania)

- AB Volvo (Suecia)

- TRATON SE (Alemania)

- Tata Motors Limited (India)

- Einride AB (Suecia)

- BYD Company Limited (China)

- Volta Trucks (Suecia)

- Xos, Inc. (EE. UU.)

- Nikola Corporation (EE. UU.)

- Hyliion Holdings Corp. (EE. UU.)

- Convoy Inc. (EE. UU.)

- Trimble Transportation (EE. UU.)

- Omnitracs LLC (EE. UU.)

- OCTO Telematics Ltd. (Italia)

- Microlise Limited (India)

- Masternaut Limited (Reino Unido)

- Transfix (EE. UU.)

- Fleet Advantage LLC (EE. UU.)

Últimos avances en el mercado global de camiones como servicio

- En septiembre de 2024, Volvo Trucks fortaleció el mercado de camiones como servicio con la entrega de 70 camiones eléctricos Volvo VNR bajo la iniciativa SWITCH-ON, lo que permitió a múltiples flotas del sur de California adoptar camiones de cero emisiones para operaciones regionales de transporte de mercancías y acarreo. Con el respaldo de la EPA y la financiación de South Coast AQMD, el programa reduce las barreras financieras y operativas para la electrificación. La integración de Volvo on Demand acelera aún más la adopción en el mercado al permitir que las flotas accedan a camiones eléctricos a través de un modelo basado en servicios con una inversión inicial mínima, lo que refuerza la transición hacia soluciones de transporte de mercancías sostenibles y con pocos activos.

- En noviembre de 2023, Hydrogen Vehicle Systems Limited (HVS) se asoció con Zeti, junto con Gravis Capital, para introducir un modelo de Transporte como Servicio (TSA) para camiones de pila de combustible de hidrógeno, expandiendo la movilidad basada en servicios al segmento del hidrógeno. Esta colaboración impulsa una comercialización más amplia de camiones de hidrógeno al integrar vehículos, financiación y servicios operativos en una única oferta. La iniciativa refuerza la confianza del mercado en las soluciones de Truck as a Service impulsadas por hidrógeno al abordar los desafíos de coste, financiación y adopción que enfrentan los operadores de flotas.

- En agosto de 2023, la colaboración de Webfleet con VEV, proveedor de soluciones de flotas eléctricas, contribuyó significativamente al ecosistema de camiones como servicio al respaldar la transición integral a flotas eléctricas. Esta colaboración permite a las flotas gestionar el abastecimiento de vehículos, la infraestructura de carga, la electrificación de las instalaciones y las operaciones continuas mediante información telemática basada en datos. Este desarrollo mejora la eficiencia operativa y la optimización energética, reforzando la propuesta de valor de los modelos de camiones basados en servicios y acelerando la adopción de flotas comerciales de vehículos eléctricos.

- En junio de 2022, WattEV anunció planes para operar 12 000 camiones eléctricos bajo su modelo de "Camión como Servicio" para 2030, lo que demuestra una gran confianza en el transporte de mercancías electrificado basado en servicios. Con el respaldo de una red de carga de gigavatios, la iniciativa aborda las deficiencias críticas de infraestructura que limitan la adopción de camiones eléctricos. El lanzamiento de la Parada de Camiones Eléctricos de Bakersfield, que incluye generación solar, almacenamiento de baterías y carga de megavatios, refuerza la escalabilidad y la viabilidad a largo plazo de las plataformas de "Camión como Servicio" eléctrico.

- En marzo de 2022, la startup estadounidense WattEV encargó 50 camiones Volvo VNR Electric para su modelo "Camión como Servicio", lo que marca un avance hacia los servicios comerciales de transporte de mercancías electrificado. Junto con el despliegue de vehículos, el desarrollo de estaciones de carga de alta capacidad en California mejora la preparación operativa para el transporte de mercancías eléctricas. Esta iniciativa impulsó el impulso inicial del mercado al demostrar cómo la integración de vehículos e infraestructura de carga puede facilitar operaciones prácticas de transporte de mercancías eléctricas basadas en servicios.

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.