North America Plastic Compounding Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

58.94 Billion

USD

85.13 Billion

2024

2032

USD

58.94 Billion

USD

85.13 Billion

2024

2032

| 2025 –2032 | |

| USD 58.94 Billion | |

| USD 85.13 Billion | |

| % | |

|

Segmentación del mercado de compuestos plásticos en Norteamérica por tipo de polímero (termoplásticos, termoestables, plásticos de ingeniería, bioplásticos, etc.), tipo de relleno (rellenos minerales, refuerzos, aditivos, etc.), proceso de fabricación (extrusión, compactación/prensado, amasadora/mezcla Banbury, compuestos por moldeo por inyección, etc.), propiedades (resistencia, durabilidad, flexibilidad, resistencia al impacto, rigidez, etc.), aplicación (aeroespacial y defensa, embalaje, electricidad y electrónica, energía, construcción, automoción, dispositivos médicos, mobiliario, etc.): tendencias y pronóstico del sector hasta 2032.

Tamaño del mercado de compuestos plásticos de América del Norte

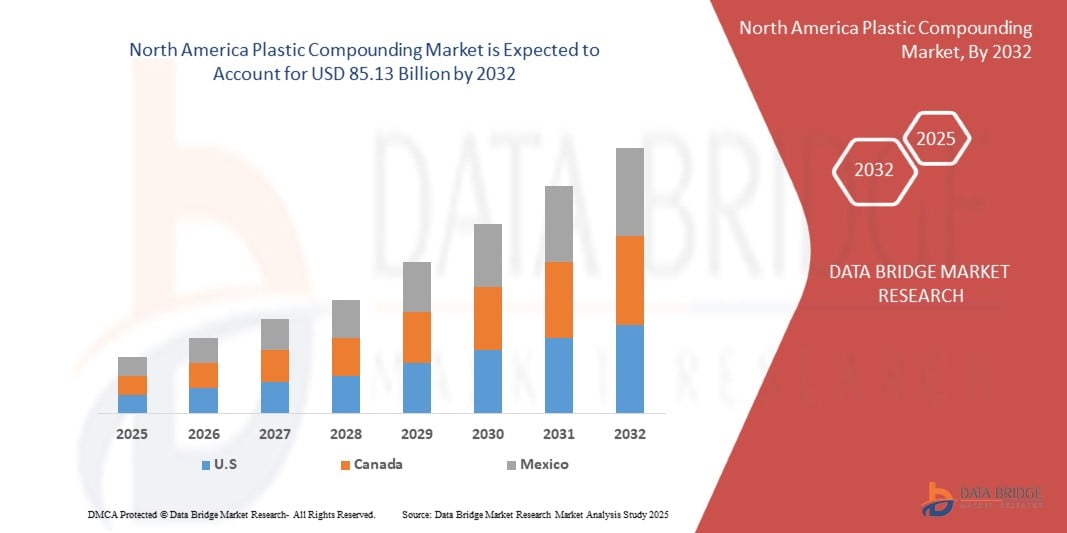

- El tamaño del mercado de compuestos plásticos de América del Norte se valoró en USD 58,94 en 2024 y se espera que alcance los USD 85,13 mil millones para 2032 , con una CAGR de 4,75% durante el período de pronóstico mediante el cambio hacia compuestos plásticos reciclables y biodegradables debido a las regulaciones ambientales, los avances en las tecnologías de compuestos que mejoran el rendimiento y la rentabilidad de los productos y las políticas e iniciativas gubernamentales de apoyo que promueven el uso de plásticos en diversas industrias.

- Además, se espera que el mercado aumente el uso de bioplásticos y alternativas de compuestos sostenibles, el aumento en la adopción de vehículos eléctricos que requieren polímeros avanzados y la creciente demanda de soluciones plásticas reciclables y circulares.

Análisis del mercado de compuestos plásticos en América del Norte

- El aumento global en el cambio hacia compuestos plásticos reciclables y biodegradables debido a las regulaciones ambientales, los avances en las tecnologías de compuestos que mejoran el rendimiento del producto y la rentabilidad.

- Los factores clave incluyen el aumento global en el cambio hacia compuestos plásticos reciclables y biodegradables debido a las regulaciones ambientales, los avances en tecnologías de compuestos que mejoran el rendimiento y la rentabilidad de los productos, la creciente demanda de los sectores de transmisión de energía y el aumento de las inversiones en la modernización de la red y la infraestructura transfronteriza.

- Estados Unidos domina el mercado de compuestos plásticos de América del Norte, con la mayor participación en los ingresos del 64,03 % en 2024, una creciente demanda de propiedades de materiales mejoradas, rentabilidad y una creciente adopción en diversas aplicaciones industriales.

- Se proyecta que EE. UU. será el país de más rápido crecimiento en el mercado durante el período de pronóstico, impulsado por la creciente demanda de materiales livianos y duraderos en todas las industrias y un enfoque creciente en compuestos plásticos reciclables y sostenibles.

- Se espera que el segmento de termoplásticos domine el mercado de compuestos plásticos de América del Norte con una participación del 61,36 % en 2025, impulsado por la creciente demanda de mejores propiedades de los materiales, rentabilidad y un uso industrial más amplio.

Alcance del informe y segmentación del mercado de compuestos plásticos en América del Norte

|

Atributos |

Perspectivas clave del mercado de compuestos plásticos en América del Norte |

|

Segmentos cubiertos |

|

|

Países cubiertos |

América del norte

|

|

Actores clave del mercado |

|

|

Oportunidades de mercado |

|

|

Conjuntos de información de datos de valor añadido |

Además de los conocimientos sobre escenarios de mercado como valor de mercado, tasa de crecimiento, segmentación, cobertura geográfica y actores principales, los informes de mercado seleccionados por Data Bridge Market Research también incluyen análisis de importación y exportación, descripción general de la capacidad de producción, análisis del consumo de producción, análisis de tendencias de precios, escenario de cambio climático, análisis de la cadena de suministro, análisis de la cadena de valor, descripción general de materias primas/consumibles, criterios de selección de proveedores, análisis PESTLE, análisis de Porter y marco regulatorio. |

Tendencias del mercado de compuestos plásticos en América del Norte

Creciente demanda de plásticos de alto rendimiento

- La demanda de compuestos plásticos de alto rendimiento está creciendo rápidamente, impulsada por la creciente urbanización, la actividad industrial y el creciente uso de vehículos eléctricos e infraestructuras inteligentes. Los compuestos plásticos avanzados abordan estos desafíos ofreciendo mayor durabilidad, eficiencia energética y un rendimiento superior del producto.

- A medida que los países se centran en reducir las emisiones de carbono y mejorar la estabilidad de la red eléctrica, se observa una tendencia creciente hacia la modernización de la infraestructura eléctrica mediante el uso de compuestos plásticos innovadores. Esta transición es crucial para satisfacer la creciente demanda de electricidad, a la vez que se promueven sistemas de transmisión más limpios y eficientes.

- Los principales actores de la industria, como Covestro, LyondellBasell y BASF, están aumentando significativamente sus esfuerzos de I+D para desarrollar compuestos plásticos de próxima generación que sean más sostenibles, flexibles y de alto rendimiento, impulsando aún más la innovación y el crecimiento del mercado.

- Los avances en la tecnología de compuestos plásticos, caracterizados por una mejor estabilidad térmica, aislamiento eléctrico y resistencia mecánica, impulsan el crecimiento del mercado. Los principales fabricantes desarrollan activamente compuestos especializados para apoyar la integración de energías renovables a gran escala y mejorar la infraestructura energética interregional, impulsando la expansión del mercado global de compuestos plásticos en Norteamérica.

Dinámica del mercado de compuestos plásticos en América del Norte

Conductor

Cambio hacia compuestos plásticos reciclables y biodegradables debido a las regulaciones ambientales

- La creciente demanda mundial de materiales sostenibles, impulsada por estrictas regulaciones ambientales, la creciente concienciación de los consumidores y los objetivos de sostenibilidad de las empresas, está ejerciendo una enorme presión sobre los métodos tradicionales de producción de plástico. Para afrontar este desafío, muchos fabricantes están acelerando las inversiones en compuestos plásticos reciclables y biodegradables para reducir el impacto ambiental y apoyar iniciativas de economía circular. Estos avances están creando soluciones de materiales más ecológicas, eficientes y preparadas para el futuro, de forma similar a cómo las tecnologías de eficiencia energética optimizan el uso de recursos.

- Por ejemplo, en 2024, varias importantes empresas químicas anunciaron proyectos a gran escala centrados en ampliar la capacidad de fabricación de compuestos de plásticos biodegradables, con el objetivo de satisfacer la creciente demanda de los sectores del embalaje, la automoción y los bienes de consumo. Estas iniciativas se centran en reducir los residuos plásticos, mejorar la reciclabilidad y cumplir con los marcos regulatorios globales, como el Plan de Acción para la Economía Circular de la UE.

- Estas inversiones no solo están transformando las formulaciones de materiales, sino que también permiten una mayor adopción de plásticos sostenibles en todas las industrias. Empresas líderes como BASF, Covestro y LyondellBasell están invirtiendo fuertemente en I+D para desarrollar compuestos plásticos de origen biológico y reciclables de nueva generación, garantizando un mejor rendimiento y cumplimiento ambiental.

- Además, el compromiso continuo de gobiernos, empresas privadas y organismos reguladores desempeña un papel fundamental en la promoción de plásticos reciclables y biodegradables como componente esencial de las iniciativas globales de sostenibilidad. Estas iniciativas están consolidando los compuestos plásticos ecológicos como un factor clave de la economía circular y un importante motor de crecimiento en el mercado global de compuestos plásticos de Norteamérica.

Restricción/Desafío

Volatilidad en los precios de las materias primas, especialmente las derivadas del petróleo, como el polipropileno y el polietileno

- La volatilidad de los precios de las materias primas, en particular las derivadas del petróleo, como el polipropileno y el polietileno, sigue siendo un obstáculo importante para el mercado norteamericano de compuestos plásticos. La fluctuación de los precios afecta los costos de producción y la rentabilidad, lo que genera incertidumbre tanto para fabricantes como para usuarios finales.

- Además, la dependencia de los mercados de petróleo crudo expone a la industria de compuestos a tensiones geopolíticas, interrupciones en la cadena de suministro y políticas comerciales cambiantes, que pueden conducir a picos repentinos de precios o escasez.

- Por ejemplo, a principios de 2025, las fluctuaciones del precio mundial del petróleo crudo provocaron que los precios del polipropileno variaran más de un 20% en cuestión de meses, lo que afectó directamente los costos de insumos de los fabricantes de compuestos plásticos y obligó a realizar ajustes en las estrategias de precios.

- Además, las materias primas alternativas, como las materias primas de origen biológico, si bien son prometedoras, actualmente están limitadas por los mayores costos y los desafíos de escalabilidad, lo que impide mitigar por completo la volatilidad de los precios del petróleo.

- Esta inestabilidad de precios plantea desafíos para la planificación y la inversión a largo plazo en el sector de compuestos plásticos, especialmente para los pequeños fabricantes y las regiones con menor resiliencia financiera. A pesar de los esfuerzos por diversificar las fuentes de materias primas y mejorar la flexibilidad de la cadena de suministro, la volatilidad de los precios de las materias primas sigue siendo un obstáculo clave para un crecimiento estable.

Alcance del mercado de compuestos plásticos en América del Norte

El mercado está segmentado según el tipo de polímero, tipo de relleno, proceso de fabricación, usabilidad, propiedades y aplicación.

- Tipo de polímero

Según el tipo de polímero, el mercado se segmenta en termoplásticos, plásticos termoestables, plásticos de ingeniería, bioplásticos y otros. En 2025, se prevé que el segmento de termoplásticos domine el mercado con una cuota de mercado del 61,36 %, con una tasa de crecimiento anual compuesta (TCAC) del 4,24 % entre 2025 y 2032, impulsada por la creciente demanda de materiales ligeros y duraderos en todas las industrias y un mayor enfoque en compuestos plásticos reciclables y sostenibles.

- Tipo de relleno

Según el tipo de relleno, el mercado se segmenta en rellenos minerales, refuerzos, aditivos y otros. En 2025, se prevé que el segmento de rellenos minerales domine el mercado con una cuota de mercado del 47,86 %, con una tasa de crecimiento anual compuesta (TCAC) del 5,56 % entre 2025 y 2032, impulsada por la creciente demanda de mejores propiedades de los materiales, la rentabilidad y su creciente adopción en diversas aplicaciones industriales.

- Proceso de fabricación

Según el proceso de fabricación, el mercado se segmenta en extrusión, compactación/prensado, amasadora/mezcla Banbury, compuestos basados en moldeo por inyección, entre otros. En 2025, se prevé que el segmento de extrusión domine el mercado con una cuota de mercado del 44,05 %, con una tasa de crecimiento anual compuesta (TCAC) del 5,12 % entre 2025 y 2032, impulsada por su adopción generalizada para un compuesto eficiente y continuo, y la creciente demanda de compuestos plásticos de alta calidad en diversas industrias.

- Propiedades

Según sus propiedades, el mercado se segmenta en resistencia, durabilidad, flexibilidad, resistencia al impacto, rigidez, entre otras. En 2025, se prevé que el segmento de resistencia domine el mercado con una cuota de mercado del 27,98 %, con una tasa de crecimiento anual compuesta (TCAC) del 5,42 % entre 2025 y 2032, impulsada por la creciente demanda de compuestos plásticos duraderos y de alto rendimiento en las industrias automotriz, de construcción y de bienes de consumo.

- Solicitud

Según su aplicación, el mercado se segmenta en aeroespacial y defensa, embalaje, electricidad y electrónica, energía y electricidad, construcción, automoción, dispositivos médicos, mobiliario, entre otros. En 2025, se prevé que el segmento automotriz domine el mercado con una cuota de mercado del 26,65 %, con una tasa de crecimiento anual compuesta (TCAC) del 3,38 % entre 2025 y 2032, impulsada por la creciente demanda de compuestos plásticos ligeros, duraderos y reciclables para mejorar la eficiencia del combustible y cumplir con las estrictas normativas ambientales.

Análisis regional del mercado de compuestos plásticos de América del Norte

- Se espera que el mercado de compuestos plásticos de América del Norte alcance los USD 85,13 mil millones para 2032, desde USD 58,94 mil millones en 2024, creciendo a una CAGR del 4,75% en el período de pronóstico de 2025 a 2032.

- América del Norte destina una parte significativa de su PIB a la manufactura y el desarrollo industrial, lo que garantiza una sólida financiación para materiales avanzados y tecnologías innovadoras de compuestos plásticos. En contraste, los mercados emergentes están incrementando sus inversiones en compuestos plásticos, impulsados por la creciente industrialización, la urbanización y la creciente demanda de materiales sostenibles y de alto rendimiento. La disponibilidad de financiación, tanto del sector público como del privado, desempeña un papel crucial en la expansión de la capacidad de producción y la adopción de compuestos plásticos avanzados a nivel mundial.

- En Estados Unidos, las tecnologías avanzadas de compuestos plásticos se adoptan e integran ampliamente en diversas aplicaciones industriales, impulsando sectores como el automotriz, el aeroespacial y el electrónico. Por el contrario, los mercados emergentes con infraestructura de fabricación en desarrollo están experimentando un rápido crecimiento en la demanda de compuestos plásticos especializados, impulsado por la expansión de las bases industriales y el aumento de las necesidades en los sectores de la salud, la automoción y el envasado. A medida que estos sistemas sanitarios e industriales se centralizan o privatizan, a menudo se produce un aumento de la inversión en tecnologías de vanguardia para compuestos plásticos, lo que promueve el crecimiento del mercado y la accesibilidad.

Perspectiva del mercado de compuestos plásticos de Canadá y América del Norte

Se espera que Canadá registre una CAGR del 4,44 % entre 2025 y 2032 en la región de América del Norte, impulsada por la creciente demanda de mejores propiedades de los materiales, mayor rentabilidad y una mayor adopción en diversas aplicaciones industriales.

Perspectiva del mercado de compuestos plásticos de América del Norte en México

Se espera que México registre una CAGR de 3.91% entre 2025 y 2032, impulsada por la creciente demanda de materiales ligeros y duraderos en todas las industrias y un enfoque cada vez mayor en compuestos plásticos reciclables y sostenibles.

Cuota de mercado de compuestos plásticos en América del Norte

El mercado de compuestos plásticos de América del Norte está liderado principalmente por empresas bien establecidas, entre las que se incluyen:

- LyondellBasell Industries Holdings BV (EE. UU.)

- BASF (Alemania)

- LG Chem (Corea del Sur)

- Dow (EE.UU.)

- SABIC (Arabia Saudita)

- Covestro AG (Alemania)

- Teknor Apex (EE. UU.)

- LANXESS (Alemania)

- Corporación Celanese (EE. UU.)

- Borealis GmbH (Austria)

- Asahi Kasei Corp. (Japón)

- Mitsubishi Chemical Group Corporation (Japón)

- DuPont (EE. UU.)

- Corporación Avient (EE. UU.)

- INEOS (Reino Unido)

- Ciencia Kingfa. Y tecnología. Co., Ltd (China)

- Washington Penn (EE. UU.)

- Compañía RTP (EE. UU.)

- Syensqo (Bélgica)

- Envalior (Alemania)

- Arkema (Francia)

- Trinseo (Estados Unidos)

- Daicel Corporation (Japón)

- KANEKA CORPORATION (Japón)

- TORAY INDUSTRIES, INC. (Japón)

- Mitsui Chemicals, Inc. (Japón)

- Ensinger (Alemania)

- CLARIANT (Suiza)

Últimos avances en el mercado de compuestos plásticos de América del Norte

- En junio de 2025, Envalior, en colaboración con SENTImotion y Frencken Group, anunció una innovación de producto que consiste en un nuevo concepto de caja de engranajes para brazos robóticos, fabricado con plástico de ingeniería Stanyl PA46. Este desarrollo permite cajas de engranajes un 50 % más ligeras y rentables que las alternativas metálicas, lo que facilita la producción a gran escala de robots ligeros y energéticamente eficientes. Esta innovación beneficia significativamente a Envalior, ya que amplía su presencia en los sectores de la robótica y la movilidad, abriendo nuevas oportunidades de crecimiento en la automatización industrial y de consumo.

- En mayo de 2024, Envalior anunció su participación en la conferencia SKZ "Plásticos en aplicaciones de ingeniería eléctrica y eléctrica", donde presentó innovaciones de producto, como compuestos sostenibles de poliamida 6 y un nuevo PBT ignífugo sin halógenos (p. ej., Pocan BFN4221Z). Este desarrollo se centra en ampliar la cartera de plásticos de ingeniería de Envalior con una mayor proporción de materias primas sostenibles, lo que permite a los clientes reducir su huella de carbono y su dependencia de insumos fósiles. Los materiales destacados ofrecen un rendimiento mecánico mejorado y una mayor resistencia al fuego, lo que posiciona a Envalior para satisfacer mejor la creciente demanda en sectores como la electromovilidad, el 5G y los sistemas autónomos, a la vez que refuerza su liderazgo en termoplásticos sostenibles.

- En julio de 2025, Arkema lanzó Zenimid, una nueva marca para su gama de poliimidas de ultraalto rendimiento, lo que marca un desarrollo estratégico de producto. Esta innovación enriquece la cartera de materiales especiales de Arkema, satisfaciendo sectores de alta demanda como el aeroespacial, la electrónica y la automoción. Con una excepcional resistencia térmica, mecánica y química, Zenimid impulsa el crecimiento de la empresa en aplicaciones avanzadas. Este lanzamiento refuerza la posición de Arkema en el mercado de polímeros de alto rendimiento.

- En junio de 2025, Trinseo presentó LIGOS A9615, un nuevo adhesivo acrílico diseñado para el segmento de etiquetas de uso general (GPL), lanzado el 9 de junio de 2025, dirigido a etiquetas de película en el mercado del sudeste asiático. Este desarrollo representa un lanzamiento estratégico que refuerza la fortaleza de Trinseo en innovación adhesiva. Entre sus principales ventajas se incluyen una excelente resistencia al envejecimiento, una removibilidad limpia con capacidad de reposicionamiento y resistencia a los plastificantes, lo que permite una adhesión fiable incluso en superficies curvas de PVC, comunes en bienes de consumo y aplicaciones de embalaje.

- En febrero de 2025, Trinseo anunció el lanzamiento del primer producto de resina de poliestireno (rPS) transparente y reciclado por disolución en Europa, específicamente aprobado para el contacto directo con alimentos y que cumple oficialmente con el Reglamento (UE) 2022/1616. Este hito regulatorio se produjo tras extensas pruebas, incluyendo una "Prueba de Desafío" realizada con el Instituto Fraunhofer para validar la eficacia de la descontaminación y el cumplimiento de la seguridad alimentaria de la resina final. Producida en las instalaciones de Trinseo en Schkopau y con aproximadamente un 30% de contenido reciclado, la nueva resina rPS ofrece una reducción de la huella de carbono de aproximadamente el 18% en comparación con el poliestireno virgen. Para Trinseo, este desarrollo representa un avance estratégico en sostenibilidad, que permite a la empresa satisfacer la creciente demanda de soluciones de materiales circulares y respaldar los objetivos de contenido reciclado de sus clientes.

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Tabla de contenido

1 INTRODUCCIÓN

1.1 OBJETIVOS DEL ESTUDIO

1.2 DEFINICIÓN DE MERCADO

1.3 INFORMACIÓN GENERAL

1.4 LIMITACIONES

1.5 MERCADOS CUBIERTOS

2 SEGMENTACIÓN DEL MERCADO

2.1 MERCADOS CUBIERTOS

2.2 ÁMBITO GEOGRÁFICO

2,3 AÑOS CONSIDERADOS PARA EL ESTUDIO

2.4 MONEDA Y PRECIOS

2.5 MODELO DE VALIDACIÓN DE DATOS TRÍPODE DBMR

2.6 MODELADO MULTIVARIADO

2.7 ENTREVISTAS PRINCIPALES CON LÍDERES DE OPINIÓN CLAVE

2.8 CUADRÍCULA DE POSICIÓN DE MERCADO DBMR

2.9 CUADRÍCULA DE COBERTURA DE APLICACIONES DEL MERCADO

2.1 FUENTES SECUNDARIAS

2.11 SUPUESTOS

3 RESUMEN EJECUTIVO

4 INFORMACIÓN PREMIUM

4.1 ANÁLISIS DE LAS CINCO FUERZAS DE PORTER

4.1.1 AMENAZA DE NUEVOS ENTRANTES

4.1.2 PODER DE NEGOCIACIÓN DE LOS PROVEEDORES

4.1.3 PODER DE NEGOCIACIÓN DE LOS COMPRADORES

4.1.4 AMENAZA DE SUSTITUTOS

4.1.5 COMPETENCIA INTERNA

4.2 SEGUIMIENTO DE INNOVACIÓN Y ANÁLISIS ESTRATÉGICO

4.2.1 ANÁLISIS DE GRANDES ACUERDOS Y ALIANZAS ESTRATÉGICAS

4.2.1.1 EMPRESAS CONJUNTAS

4.2.1.2 FUSIONES Y ADQUISICIONES

4.2.1.3 LICENCIAS Y ASOCIACIONES

4.2.1.4 COLABORACIONES TECNOLÓGICAS

4.2.1.5 DESINVERSIONES ESTRATÉGICAS

4.2.2 NÚMERO DE PRODUCTOS EN DESARROLLO

4.2.3 ETAPA DE DESARROLLO

4.2.4 CRONOGRAMAS E HITOS

4.2.5 ESTRATEGIAS Y METODOLOGÍAS DE INNOVACIÓN

4.2.6 EVALUACIÓN Y MITIGACIÓN DE RIESGOS

4.2.7 PERSPECTIVAS FUTURAS

4.3 ANÁLISIS DE LA CADENA DE VALOR

4.4 ESCENARIO DE IMPORTACIÓN Y EXPORTACIÓN

4.5 CAPACIDAD DE PRODUCCIÓN PARA LOS MEJORES FABRICANTES

4.6 PERSPECTIVA DE LA MARCA

4.7 COMPORTAMIENTO DE COMPRA DEL CONSUMIDOR

4.8 BASE DE DATOS DE LAS FABRICANTES DE MEZCLAS Y LOS EQUIPOS QUE UTILIZAN

4.9 ANÁLISIS DE PATENTES

4.9.1 CALIDAD Y RESISTENCIA DE LA PATENTE

4.9.2 FAMILIAS DE PATENTES

4.9.3 LICENCIAS Y COLABORACIONES

4.9.4 PANORAMA DE PATENTES DE LA REGIÓN

4.9.5 ESTRATEGIA Y GESTIÓN DE LA PROPIEDAD INTELECTUAL

4.1 COBERTURA DE MATERIA PRIMA

4.11 ANÁLISIS DE LA CADENA DE SUMINISTRO DEL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE

4.11.1 DESCRIPCIÓN GENERAL

4.11.2 ESCENARIOS DE COSTOS LOGÍSTICOS

4.11.3 IMPORTANCIA DE LOS PROVEEDORES DE SERVICIOS LOGÍSTICOS (PSL)

4.12 AVANCES TECNOLÓGICOS EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE

4.12.1 IA Y OPTIMIZACIÓN DE PROCESOS DIGITALES

4.12.2 TECNOLOGÍAS AVANZADAS DE EXTRUSIÓN Y MANEJO DE MATERIALES

4.12.3 COMPUESTOS POLIMÉRICOS FUNCIONALIZADOS Y DE BASE BIOLÓGICA

4.12.4 SOLUCIONES DE COMPUESTOS INTELIGENTES Y CON EFICACIA

4.12.5 AUTOMATIZACIÓN E INDUSTRIA 4.0 EN OPERACIONES DE COMPUESTO

4.12.6 INNOVACIONES EN SOSTENIBILIDAD Y ECONOMÍA CIRCULAR

4.12.7 PLATAFORMAS DE FORMULACIÓN Y PARTICIPACIÓN DEL CLIENTE DIGITAL

4.13 CRITERIOS DE SELECCIÓN DE PROVEEDORES

4.14 CUADRANTE DE EVALUACIÓN DE LA EMPRESA

4.15 ANÁLISIS DE PRECIOS

5. EL PAPEL DE LOS ARANCELES EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE

5.1 PANORAMA ARANCELARIO: ARANCELES SOBRE POLÍMEROS, ADITIVOS Y MAQUINARIA

5.2 IMPACTO DE LOS ARANCELES EN LAS ESTRUCTURAS DE COSTOS Y LA DINÁMICA DE LA CADENA DE SUMINISTRO

5.3 INFLUENCIA DE LOS ACUERDOS COMERCIALES Y LAS POLÍTICAS REGULADORAS

5.4 TENDENCIAS DEL MERCADO QUE AMPLIFICAN LOS IMPACTOS ARANCELARIOS

5.5 IMPLICACIONES COMPETITIVAS PARA LOS PARTICIPANTES DE LA INDUSTRIA

5.6 RETOS Y OPORTUNIDADES DERIVADOS DE LOS ARANCELES

5.7 EMPRESAS CLAVE Y RESUMEN DE LA ESTRATEGIA TARIFARIA

6 COBERTURA REGLAMENTARIA: MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE

7 DESCRIPCIÓN GENERAL DEL MERCADO

7.1 CONTROLADORES

7.1.1 CAMBIO HACIA COMPUESTOS PLÁSTICOS RECICLABLES Y BIODEGRADABLES DEBIDO A LAS REGULACIONES AMBIENTALES

7.1.2 AVANCES EN TECNOLOGÍAS DE COMPUESTOS QUE MEJORAN EL RENDIMIENTO DEL PRODUCTO Y LA RENTABLE EFICIENCIA

7.1.3 DESARROLLO DE PLÁSTICOS NANOCOMPUESTOS QUE OFRECEN PROPIEDADES MECÁNICAS Y DE BARRERA SUPERIORES

7.1.4 AUMENTO DEL USO DE PLÁSTICOS COMPUESTOS EN DISPOSITIVOS MÉDICOS DEBIDO A LA BIOCOPATIBILIDAD Y LA COMPATIBILIDAD DE ESTERILIZACIÓN

7.2 RESTRICCIONES

7.2.1 VOLATILIDAD EN LOS PRECIOS DE LAS MATERIAS PRIMAS, ESPECIALMENTE LAS MATERIAS PRIMAS A BASE DE PETRÓLEO, COMO EL POLIPROPILENO Y EL POLIETILENO

7.2.2 PROCESOS DE RECICLAJE COMPLEJOS Y FALTA DE INFRAESTRUCTURA ADECUADA PARA LA GESTIÓN DE RESIDUOS COMPUESTOS DE PLÁSTICO

7.3 OPORTUNIDADES

7.3.1 USO CRECIENTE DE BIOPLÁSTICOS Y ALTERNATIVAS DE COMPUESTOS SOSTENIBLES

7.3.2 AUMENTO EN LA ADOPCIÓN DE VEHÍCULOS ELÉCTRICOS QUE REQUIEREN POLÍMEROS AVANZADOS

7.3.3 AUMENTO DE LA DEMANDA DE SOLUCIONES DE PLÁSTICO RECICLABLES Y CIRCULARES

7.4 DESAFÍOS

7.4.1 LIMITACIONES DE RENDIMIENTO DE LAS ALTERNATIVAS SOSTENIBLES

7.4.2 FRAGMENTACIÓN REGLAMENTARIA Y DE NORMAS ENTRE REGIONES

8 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO DE POLÍMERO

8.1 DESCRIPCIÓN GENERAL

8.2 TERMOPLÁSTICOS

8.2.1 TERMOPLÁSTICOS, POR TIPO

8.2.2 POLIETILENO (PE), POR TIPO

8.3 PLÁSTICOS DE INGENIERÍA

8.3.1 PLÁSTICOS DE INGENIERÍA, POR TIPO

8.4 PLÁSTICOS TERMOESTABLECIDOS

8.4.1 PLÁSTICOS TERMOESTABLECIDOS, POR TIPO

8.5 BIOPLÁSTICOS

8.5.1 BIOPLÁSTICOS, POR TIPO

8.6 OTROS

9 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO DE RELLENO

9.1 INFORMACIÓN GENERAL

9.2 RELLENOS MINERALES

9.2.1 RELLENOS MINERALES, POR TIPO

9.3 REFUERZOS

9.3.1 REFUERZOS, POR TIPO

9.4 ADITIVOS

9.4.1 ADITIVOS, POR TIPO

9.5 OTROS

10 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR PROCESO DE FABRICACIÓN

10.1 INFORMACIÓN GENERAL

10.2 EXTRUSIÓN

10.2.1 EXTRUSIÓN, POR TIPO

10.2.2 EXTRUSIÓN, POR SISTEMA DE PELETIZACIÓN

10.3 COMPUESTOS BASADOS EN MOLDEO POR INYECCIÓN

10.3.1 COMPUESTO BASADO EN MOLDEO POR INYECCIÓN, MEDIANTE SISTEMA DE PELETIZACIÓN

10.4 COMPACTACIÓN/PRESIONADO

10.4.1 COMPACTACIÓN/PRESIONADO, MEDIANTE SISTEMA DE PELETIZACIÓN

10.5 AMASADORA/MEZCLA BANBURY

10.5.1 MEZCLA AMASADORA/BANBURY, MEDIANTE SISTEMA DE PELETIZACIÓN

10.6 OTROS

11 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR PROPIEDADES

11.1 INFORMACIÓN GENERAL

11.2 RESISTENCIA

11.3 DURABILIDAD

11.4 FLEXIBILIDAD

11.5 RESISTENCIA AL IMPACTO

11.6 RIGIDEZ

11.7 OTROS

12 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR APLICACIÓN

12.1 INFORMACIÓN GENERAL

12.2 AUTOMOTRIZ

12.2.1 AUTOMOTRIZ, POR CATEGORÍA

12.2.1.1 COMPONENTES INTERIORES, POR TIPO

12.2.1.2 PARTES EXTERIORES DE LA CARROCERÍA, POR TIPO

12.2.1.3 APLICACIONES BAJO EL CAPÓ, POR TIPO

12.3 EMBALAJE

12.3.1 EMBALAJE, POR CATEGORÍA

12.3.1.1 ENVASES DE ALIMENTOS Y BEBIDAS, POR TIPO

12.3.1.2 ENVASES INDUSTRIALES, POR TIPO

12.3.1.3 EMBALAJE DE BIENES DE CONSUMO, POR TIPO

12.4 EDIFICACIÓN Y CONSTRUCCIÓN

12.4.1 EDIFICACIÓN Y CONSTRUCCIÓN, POR CATEGORÍA

12.5 ELECTRICIDAD Y ELECTRÓNICA

12.5.1 ELECTRICIDAD Y ELECTRÓNICA, POR CATEGORÍA

12.6 DISPOSITIVOS MÉDICOS

12.6.1 DISPOSITIVOS MÉDICOS, POR CATEGORÍA

12.7 MUEBLES

12.7.1 MUEBLES, POR CATEGORÍA

12.8 ENERGÍA Y POTENCIA

12.8.1 ENERGÍA Y POTENCIA, POR CATEGORÍA

12.9 AEROESPACIAL Y DEFENSA

12.9.1 AEROESPACIAL Y DEFENSA, POR CATEGORÍA

12.1 OTROS

13 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE POR PAÍSES

13.1 AMÉRICA DEL NORTE

13.1.1 EE. UU.

13.1.2 CANADÁ

13.1.3 MÉXICO

14 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE: PANORAMA DE LA EMPRESA

14.1 ANÁLISIS DE ACCIONES DE LA EMPRESA: AMÉRICA DEL NORTE

15 ANÁLISIS FODA

16 PERFILES DE EMPRESAS

16.1 SABIC

16.1.1 INSTANTÁNEA DE LA EMPRESA

16.1.2 ANÁLISIS DE INGRESOS

16.1.3 ANÁLISIS DE LAS ACCIONES DE LA EMPRESA

16.1.4 PORTAFOLIO DE PRODUCTOS

16.1.5 DESARROLLO RECIENTE

16.2 LYONDELLBASELL INDUSTRIES HOLDINGS BV

16.2.1 INSTANTÁNEA DE LA EMPRESA

16.2.2 ANÁLISIS DE INGRESOS

16.2.3 ANÁLISIS DE LAS ACCIONES DE LA EMPRESA

16.2.4 PORTAFOLIO DE PRODUCTOS

16.2.5 DESARROLLOS/NOTICIAS RECIENTES

16.3 DOW

16.3.1 INSTANTÁNEA DE LA EMPRESA

16.3.2 ANÁLISIS DE INGRESOS

16.3.3 ANÁLISIS DE LAS ACCIONES DE LA EMPRESA

16.3.4 PORTAFOLIO DE PRODUCTOS

16.3.5 DESARROLLO RECIENTE

16.4 DUPONT

16.4.1 INSTANTÁNEA DE LA EMPRESA

16.4.2 ANÁLISIS DE INGRESOS

16.4.3 ANÁLISIS DE LAS ACCIONES DE LA EMPRESA

16.4.4 PORTAFOLIO DE PRODUCTOS

16.4.5 DESARROLLO RECIENTE

16.5 ARKEMA

16.5.1 INSTANTÁNEA DE LA EMPRESA

16.5.2 ANÁLISIS DE INGRESOS

16.5.3 ANÁLISIS DE LAS ACCIONES DE LA EMPRESA

16.5.4 PORTAFOLIO DE PRODUCTOS

16.5.5 DESARROLLOS RECIENTES

16.6 ASAHI KASEI CORP.

16.6.1 INSTANTÁNEA DE LA EMPRESA

16.6.2 ANÁLISIS DE INGRESOS

16.6.3 PORTAFOLIO DE PRODUCTOS

16.6.4 DESARROLLO RECIENTE

16.7 CORPORACIÓN AVIENT

16.7.1 INSTANTÁNEA DE LA EMPRESA

16.7.2 ANÁLISIS DE INGRESOS

16.7.3 PORTAFOLIO DE PRODUCTOS

16.7.4 DESARROLLO RECIENTE

16.8 BOREALIS GMBH

16.8.1 INSTANTÁNEA DE LA EMPRESA

16.8.2 PORTAFOLIO DE PRODUCTOS

16.8.3 DESARROLLO RECIENTE

16.9 BASF

16.9.1 INSTANTÁNEA DE LA EMPRESA

16.9.2 ANÁLISIS DE INGRESOS

16.9.3 PORTAFOLIO DE PRODUCTOS

16.9.4 DESARROLLO RECIENTE

16.1 CORPORACIÓN CLEANESE

16.10.1 INSTANTÁNEA DE LA EMPRESA

16.10.2 ANÁLISIS DE INGRESOS

16.10.3 PORTAFOLIO DE PRODUCTOS

16.10.4 DESARROLLO RECIENTE

16.11 CHIMEI

16.11.1 INSTANTÁNEA DE LA EMPRESA

16.11.2 ANÁLISIS DE INGRESOS

16.11.3 PORTAFOLIO DE PRODUCTOS

16.11.4 DESARROLLO RECIENTE

16.12 CLARIANTE

16.12.1 INSTANTÁNEA DE LA EMPRESA

16.12.2 ANÁLISIS DE INGRESOS

16.12.3 PORTAFOLIO DE PRODUCTOS

16.12.4 DESARROLLO RECIENTE

16.13 COVESTRO AG

16.13.1 INSTANTÁNEA DE LA EMPRESA

16.13.2 ANÁLISIS DE INGRESOS

16.13.3 PORTAFOLIO DE PRODUCTOS

16.13.4 DESARROLLO RECIENTE

16.14 CORPORACIÓN DAICEL

16.14.1 INSTANTÁNEA DE LA EMPRESA

16.14.2 ANÁLISIS DE INGRESOS

16.14.3 PORTAFOLIO DE PRODUCTOS

16.14.4 DESARROLLOS RECIENTES

16.15 ENSINGER GMBH

16.15.1 INSTANTÁNEA DE LA EMPRESA

16.15.2 PORTAFOLIO DE PRODUCTOS

16.15.3 DESARROLLO RECIENTE

16.16 ENVALIOR

16.16.1 INSTANTÁNEA DE LA EMPRESA

16.16.2 PORTAFOLIO DE PRODUCTOS

16.16.3 DESARROLLOS RECIENTES

16.17 INEOS

16.17.1 INSTANTÁNEA DE LA EMPRESA

16.17.2 PORTAFOLIO DE PRODUCTOS

16.17.3 DESARROLLO RECIENTE

16.18 CORPORACIÓN KANEKA

16.18.1 INSTANTÁNEA DE LA EMPRESA

16.18.2 ANÁLISIS DE INGRESOS

16.18.3 PORTAFOLIO DE PRODUCTOS

16.18.4 DESARROLLO RECIENTE

16.19 KINGFA CIENCIA Y TECNOLOGÍA. CO., LTD.

16.19.1 INSTANTÁNEA DE LA EMPRESA

16.19.2 ANÁLISIS DE INGRESOS

16.19.3 PORTAFOLIO DE PRODUCTOS

16.19.4 DESARROLLO RECIENTE

16.2 LANXESS

16.20.1 INSTANTÁNEA DE LA EMPRESA

16.20.2 ANÁLISIS DE INGRESOS

16.20.3 CARTERA DE NEGOCIOS

16.20.4 DESARROLLO RECIENTE

16.21 LG QUÍMICO

16.21.1 INSTANTÁNEA DE LA EMPRESA

16.21.2 ANÁLISIS DE INGRESOS

16.21.3 PORTAFOLIO DE PRODUCTOS

16.21.4 DESARROLLO RECIENTE

16.22 CORPORACIÓN DEL GRUPO QUÍMICO MITSUBISHI.

16.22.1 INSTANTÁNEA DE LA EMPRESA

16.22.2 ANÁLISIS DE INGRESOS

16.22.3 PORTAFOLIO DE PRODUCTOS

16.22.4 DESARROLLO RECIENTE

16.23 PRODUCTOS QUÍMICOS MITSUI, INC.

16.23.1 INSTANTÁNEA DE LA EMPRESA

16.23.2 ANÁLISIS DE INGRESOS

16.23.3 PORTAFOLIO DE PRODUCTOS

16.23.4 DESARROLLO RECIENTE

16.24 RTP COMPAÑÍA

16.24.1 INSTANTÁNEA DE LA EMPRESA

16.24.2 PORTAFOLIO DE PRODUCTOS

16.24.3 DESARROLLO RECIENTE

16.25 SCG

16.25.1 INSTANTÁNEA DE LA EMPRESA

16.25.2 ANÁLISIS DE INGRESOS

16.25.3 PORTAFOLIO DE PRODUCTOS

16.25.4 DESARROLLO RECIENTE

16.26 SYENSQO

16.26.1 INSTANTÁNEA DE LA EMPRESA

16.26.2 ANÁLISIS DE INGRESOS

16.26.3 PORTAFOLIO DE PRODUCTOS

16.26.4 DESARROLLOS RECIENTES

16.27 TEKNOR APEX

16.27.1 INSTANTÁNEA DE LA EMPRESA

16.27.2 PORTAFOLIO DE PRODUCTOS

16.27.3 DESARROLLO RECIENTE

16.28 INDUSTRIAS TORAY, INC.

16.28.1 INSTANTÁNEA DE LA EMPRESA

16.28.2 ANÁLISIS DE INGRESOS

16.28.3 PORTAFOLIO DE PRODUCTOS

16.28.4 DESARROLLO RECIENTE

16.29 TRINSEO

16.29.1 INSTANTÁNEA DE LA EMPRESA

16.29.2 ANÁLISIS DE INGRESOS

16.29.3 CARTERA DE SOLUCIONES

16.29.4 DESARROLLOS RECIENTES

16.3 WASHINGTON PENN

16.30.1 INSTANTÁNEA DE LA EMPRESA

16.30.2 PORTAFOLIO DE PRODUCTOS

16.30.3 DESARROLLO RECIENTE

17 CUESTIONARIO

18 INFORMES RELACIONADOS

Lista de Tablas

TABLA 1 ETAPAS DE LA CADENA DE VALOR

TABLA 2 PERSPECTIVA DE LA MARCA: MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE

TABLA 3 COMPORTAMIENTO DE COMPRA DEL CONSUMIDOR

TABLA 4 ACTORES DE AMÉRICA DEL NORTE EN LA FABRICACIÓN DE COMPUESTOS PLÁSTICOS

TABLA 5 NÚMERO DE PATENTES POR AÑO

CUADRO 6 NÚMERO DE PATENTES POR REGIÓN/PAÍS

TABLA 7 PRINCIPALES SOLICITANTES DE PATENTES

CUADRO 8 EXPOSICIÓN ARANCELARIA Y RESPUESTA ESTRATÉGICA POR TIPO DE EMPRESA

CUADRO 9 EXPOSICIÓN ARANCELARIA Y RESPUESTA ESTRATÉGICA DE LOS ACTORES CLAVE

TABLA 10 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO DE POLÍMERO, 2018-2032 (MILES DE USD)

TABLA 11 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO DE POLÍMERO, 2018-2032 (KILOTONELADAS)

TABLA 12 MERCADO DE TERMOPLÁSTICOS EN COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 13 MERCADO DE TERMOPLÁSTICOS EN COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 14 MERCADO DE TERMOPLÁSTICOS EN COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 15 MERCADO DE POLIETILENO (PE) EN COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 16 PLÁSTICOS DE INGENIERÍA EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 17 PLÁSTICOS DE INGENIERÍA EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 18 PLÁSTICOS DE INGENIERÍA EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 19 PLÁSTICOS TERMOESTABLECIDOS EN EL MERCADO DE COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 20 PLÁSTICOS TERMOESTABLECIDOS EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 21 PLÁSTICOS TERMOESTABLECIDOS EN EL MERCADO DE COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 22 MERCADO DE BIOPLÁSTICOS EN COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 23 MERCADO DE BIOPLÁSTICOS EN COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 24 MERCADO DE BIOPLÁSTICOS EN COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 25 OTROS MERCADOS DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 26 OTROS EN AMÉRICA DEL NORTE EN EL MERCADO DE COMPUESTOS PLÁSTICOS, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 27 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO DE FILTRO, 2018-2032 (MILES DE USD)

TABLA 28 RELLENOS MINERALES EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 29 RELLENOS MINERALES EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 30 MERCADO DE REFUERZOS DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 31 MERCADO DE REFUERZOS DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 32 ADITIVOS EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 33 ADITIVOS EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 34 OTROS MERCADOS DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 35 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR PROCESO DE FABRICACIÓN, 2018-2032 (MILES DE USD)

TABLA 36 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR PROCESO DE FABRICACIÓN, 2018-2032 (KILOTONELADAS)

TABLA 37 MERCADO DE EXTRUSIÓN DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 38 MERCADO DE EXTRUSIÓN DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 39 MERCADO DE EXTRUSIÓN DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 40 MERCADO DE EXTRUSIÓN DE COMPUESTOS DE PLÁSTICO EN AMÉRICA DEL NORTE, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 41 MERCADO DE COMPUESTOS DE PLÁSTICO BASADOS EN MOLDEO POR INYECCIÓN EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 42 MERCADO DE COMPUESTOS DE PLÁSTICO BASADOS EN MOLDEO POR INYECCIÓN EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 43 MERCADO DE COMPUESTOS DE PLÁSTICO BASADOS EN MOLDEO POR INYECCIÓN EN AMÉRICA DEL NORTE, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 44 MERCADO DE COMPACTACIÓN/PRESIONADO DE PLÁSTICOS EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 45 COMPACTACIÓN/PRESIONADO EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 46 COMPACTACIÓN/PRESIONADO EN EL MERCADO DE COMPUESTOS DE PLÁSTICO EN AMÉRICA DEL NORTE, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 47 MERCADO DE AMASADORAS/MEZCLAS BANBURY EN COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 48 MERCADO DE AMASADORAS/MEZCLAS BANBURY EN AMÉRICA DEL NORTE PARA COMPUESTOS DE PLÁSTICO, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 49 MERCADO DE MEZCLA DE AMASADORAS/BANBURY EN COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 50 OTROS MERCADOS DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 51 OTROS MERCADOS DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 52 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR PROPIEDADES, 2018-2032 (MILES DE USD)

TABLA 53 RESISTENCIA DE AMÉRICA DEL NORTE EN EL MERCADO DE COMPUESTOS PLÁSTICOS, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 54 DURABILIDAD EN EL MERCADO DE COMPUESTOS DE PLÁSTICO EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 55 FLEXIBILIDAD EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 56 RESISTENCIA AL IMPACTO EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 57 RIGIDEZ EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 58 OTROS MERCADOS DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 59 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR APLICACIÓN, 2018-2032 (MILES DE USD)

TABLA 60 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR APLICACIÓN, 2018-2032 (KILOTONELADAS)

TABLA 61 MERCADO DE COMPUESTOS PLÁSTICOS AUTOMOTRICES EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 62 MERCADO DE COMPUESTOS PLÁSTICOS AUTOMOTRICES EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 63 MERCADO DE COMPUESTOS PLÁSTICOS AUTOMOTRICES EN AMÉRICA DEL NORTE, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 64 COMPONENTES INTERIORES DE AMÉRICA DEL NORTE EN EL MERCADO DE COMPUESTOS PLÁSTICOS, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 65 PARTES EXTERIORES DE CARROCERÍA EN EL MERCADO DE COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 66 APLICACIONES INTERNAS EN AMÉRICA DEL NORTE EN EL MERCADO DE COMPUESTOS PLÁSTICOS, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 67 MERCADO DE ENVASES DE PLÁSTICO EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 68 MERCADO DE ENVASES DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 69 MERCADO DE ENVASES DE PLÁSTICO EN AMÉRICA DEL NORTE, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 70 MERCADO DE ENVASES DE ALIMENTOS Y BEBIDAS EN COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 71 MERCADO DE ENVASES INDUSTRIALES DE AMÉRICA DEL NORTE EN COMPUESTOS DE PLÁSTICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 72 MERCADO DE ENVASES DE BIENES DE CONSUMO EN COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 73 MERCADO DE CONSTRUCCIÓN Y EDIFICACIÓN DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 74 MERCADO DE CONSTRUCCIÓN Y EDIFICACIÓN DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 75 MERCADO DE CONSTRUCCIÓN Y EDIFICACIÓN DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 76 MERCADO DE PRODUCTOS ELÉCTRICOS Y ELECTRÓNICOS EN COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 77 MERCADO DE PRODUCTOS ELÉCTRICOS Y ELECTRÓNICOS EN COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 78 MERCADO DE PRODUCTOS ELÉCTRICOS Y ELECTRÓNICOS EN COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 79 MERCADO DE DISPOSITIVOS MÉDICOS EN COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 80 MERCADO DE DISPOSITIVOS MÉDICOS EN COMPUESTOS DE PLÁSTICO EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 81 MERCADO DE DISPOSITIVOS MÉDICOS EN COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 82 MERCADO DE MUEBLES DE AMÉRICA DEL NORTE EN COMPUESTOS DE PLÁSTICO, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 83 MERCADO DE MUEBLES DE AMÉRICA DEL NORTE EN COMPUESTOS DE PLÁSTICO, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 84 MERCADO DE MUEBLES DE AMÉRICA DEL NORTE EN COMPUESTOS DE PLÁSTICO, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 85 MERCADO DE ENERGÍA Y PODER EN COMPUESTOS DE PLÁSTICO EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 86 MERCADO DE ENERGÍA Y PODER EN COMPUESTOS DE PLÁSTICO EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 87 MERCADO DE ENERGÍA Y ELECTRICIDAD EN COMPUESTOS DE PLÁSTICO EN AMÉRICA DEL NORTE, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 88 MERCADO DE COMPUESTOS PLÁSTICOS DE LA INDUSTRIA AEROESPACIAL Y DE DEFENSA DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 89 MERCADO DE COMPUESTOS PLÁSTICOS DE LA INDUSTRIA AEROESPACIAL Y DE DEFENSA DE AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 90 MERCADO DE COMPUESTOS PLÁSTICOS DE LA INDUSTRIA AEROESPACIAL Y DE DEFENSA DE AMÉRICA DEL NORTE, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 91 OTROS MERCADOS DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (MILES DE USD)

TABLA 92 OTROS MERCADOS DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR REGIÓN, 2018-2032 (KILOTONELADAS)

TABLA 93 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR PAÍS, 2018-2032 (MILES DE USD)

TABLA 94 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR PAÍS, 2018-2032 (KILOTONELADAS)

TABLA 95 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO DE POLÍMERO, 2018-2032 (MILES DE USD)

TABLA 96 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO DE POLÍMERO, 2018-2032 (KILOTONELADAS)

TABLA 97 MERCADO DE TERMOPLÁSTICOS EN COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 98 MERCADO DE POLIETILENO (PE) EN COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 99 PLÁSTICOS DE INGENIERÍA EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 100 PLÁSTICOS TERMOESTABLECIDOS EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 101 MERCADO DE BIOPLÁSTICOS EN COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 102 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO DE RELLENO, 2018-2032 (MILES DE USD)

TABLA 103 RELLENOS MINERALES EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 104 MERCADO DE REFUERZOS DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 105 ADITIVOS EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 106 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR PROCESO DE FABRICACIÓN, 2018-2032 (MILES DE USD)

TABLA 107 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR PROCESO DE FABRICACIÓN, 2018-2032 (KILOTONELADAS)

TABLA 108 MERCADO DE EXTRUSIÓN DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 109 MERCADO DE EXTRUSIÓN DE COMPUESTOS DE PLÁSTICO EN AMÉRICA DEL NORTE, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 110 MERCADO DE COMPUESTOS DE PLÁSTICO BASADOS EN MOLDEO POR INYECCIÓN EN AMÉRICA DEL NORTE, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 111 COMPACTACIÓN/PRESIONADO EN EL MERCADO DE COMPUESTOS DE PLÁSTICO EN AMÉRICA DEL NORTE, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 112 MERCADO DE AMASADORAS/MEZCLAS BANBURY EN AMÉRICA DEL NORTE PARA COMPUESTOS DE PLÁSTICO, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 113 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR PROPIEDADES, 2018-2032 (MILES DE USD)

TABLA 114 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR APLICACIÓN, 2018-2032 (MILES DE USD)

TABLA 115 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR APLICACIÓN, 2018-2032 (KILOTONELADAS)

TABLA 116 MERCADO DE COMPUESTOS PLÁSTICOS AUTOMOTRICES EN AMÉRICA DEL NORTE, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 117 COMPONENTES INTERIORES DE AMÉRICA DEL NORTE EN EL MERCADO DE COMPUESTOS PLÁSTICOS, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 118 PARTES EXTERIORES DE CARROCERÍA EN EL MERCADO DE COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 119 APLICACIONES INTERNAS EN AMÉRICA DEL NORTE EN EL MERCADO DE COMPUESTOS PLÁSTICOS, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 120 MERCADO DE ENVASES DE PLÁSTICO EN AMÉRICA DEL NORTE, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 121 MERCADO DE ENVASES DE ALIMENTOS Y BEBIDAS EN COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 122 MERCADO DE ENVASES INDUSTRIALES DE AMÉRICA DEL NORTE EN COMPUESTOS DE PLÁSTICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 123 MERCADO DE ENVASES DE BIENES DE CONSUMO EN COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 124 MERCADO DE CONSTRUCCIÓN Y EDIFICACIÓN DE COMPUESTOS PLÁSTICOS EN AMÉRICA DEL NORTE, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 125 MERCADO DE PRODUCTOS ELÉCTRICOS Y ELECTRÓNICOS EN COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 126 MERCADO DE DISPOSITIVOS MÉDICOS EN COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 127 MERCADO DE MUEBLES DE AMÉRICA DEL NORTE EN COMPUESTOS DE PLÁSTICO, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 128 MERCADO DE ENERGÍA Y ELECTRICIDAD EN COMPUESTOS DE PLÁSTICO EN AMÉRICA DEL NORTE, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 129 MERCADO DE COMPUESTOS PLÁSTICOS DE LA INDUSTRIA AEROESPACIAL Y DE DEFENSA DE AMÉRICA DEL NORTE, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 130 MERCADO DE COMPUESTOS PLÁSTICOS DE EE. UU., POR TIPO DE POLÍMERO, 2018-2032 (MILES DE USD)

TABLA 131 MERCADO DE COMPUESTOS PLÁSTICOS DE EE. UU., POR TIPO DE POLÍMERO, 2018-2032 (KILOTONELADAS)

TABLA 132 MERCADO DE TERMOPLÁSTICOS EN COMPUESTOS PLÁSTICOS DE EE. UU., POR TIPO, 2018-2032 (MILES DE USD)

TABLA 133 MERCADO DE POLIETILENO (PE) EN COMPUESTOS PLÁSTICOS DE EE. UU., POR TIPO, 2018-2032 (MILES DE USD)

TABLA 134 PLÁSTICOS DE INGENIERÍA EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE EE. UU., POR TIPO, 2018-2032 (MILES DE USD)

TABLA 135 PLÁSTICOS TERMOESTABLECIDOS DE EE. UU. EN EL MERCADO DE COMPUESTOS DE PLÁSTICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 136 BIOPLÁSTICOS EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE EE. UU., POR TIPO, 2018-2032 (MILES DE USD)

TABLA 137 MERCADO DE COMPUESTOS PLÁSTICOS DE EE. UU., POR TIPO DE RELLENO, 2018-2032 (MILES DE USD)

TABLA 138 RELLENOS MINERALES EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE EE. UU., POR TIPO, 2018-2032 (MILES DE USD)

TABLA 139 MERCADO DE REFUERZOS EN COMPUESTOS PLÁSTICOS DE EE. UU., POR TIPO, 2018-2032 (MILES DE USD)

TABLA 140 ADITIVOS EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE EE. UU., POR TIPO, 2018-2032 (MILES DE USD)

TABLA 141 MERCADO DE COMPUESTOS DE PLÁSTICO DE EE. UU., POR PROCESO DE FABRICACIÓN, 2018-2032 (MILES DE USD)

TABLA 142 MERCADO DE COMPUESTOS DE PLÁSTICO DE EE. UU., POR PROCESO DE FABRICACIÓN, 2018-2032 (KILOTONELADAS)

TABLA 143 MERCADO DE EXTRUSIÓN EN COMPUESTOS DE PLÁSTICO EN EE. UU., POR TIPO, 2018-2032 (MILES DE USD)

TABLA 144 MERCADO DE EXTRUSIÓN DE PLÁSTICOS EN ESTADOS UNIDOS, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 145 MERCADO DE COMPUESTOS DE PLÁSTICO BASADOS EN MOLDEO POR INYECCIÓN EN EE. UU., POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 146 MERCADO DE COMPACTACIÓN/PRESIONADO DE PLÁSTICOS EN EE. UU., POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 147 MERCADO DE MEZCLA DE AMASADORAS/BANBURY EN COMPUESTOS DE PLÁSTICO EN EE. UU., POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 148 MERCADO DE COMPUESTOS PLÁSTICOS DE EE. UU., POR PROPIEDADES, 2018-2032 (MILES DE USD)

TABLA 149 MERCADO DE COMPUESTOS PLÁSTICOS DE EE. UU., POR APLICACIÓN, 2018-2032 (MILES DE USD)

TABLA 150 MERCADO DE COMPUESTOS PLÁSTICOS DE EE. UU., POR APLICACIÓN, 2018-2032 (KILOTONELADAS)

TABLA 151 MERCADO DE COMPUESTOS DE PLÁSTICO EN AUTOMÓVILES DE EE. UU., POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 152 COMPONENTES INTERIORES DE EE. UU. EN EL MERCADO DE COMPUESTOS PLÁSTICOS, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 153 PARTES DE CARROCERÍA EXTERIOR EN EL MERCADO DE COMPUESTOS DE PLÁSTICO DE EE. UU., POR TIPO, 2018-2032 (MILES DE USD)

TABLA 154 APLICACIONES INTERNAS EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE EE. UU., POR TIPO, 2018-2032 (MILES DE USD)

TABLA 155 MERCADO DE ENVASES DE PLÁSTICO EN ESTADOS UNIDOS, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 156 MERCADO DE ENVASES DE ALIMENTOS Y BEBIDAS EN COMPUESTOS DE PLÁSTICO DE EE. UU., POR TIPO, 2018-2032 (MILES DE USD)

TABLA 157 MERCADO DE ENVASES INDUSTRIALES DE ESTADOS UNIDOS EN COMPUESTOS DE PLÁSTICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 158 MERCADO DE ENVASES DE BIENES DE CONSUMO EN ESTADOS UNIDOS, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 159 MERCADO DE CONSTRUCCIÓN Y EDIFICACIÓN DE COMPUESTOS DE PLÁSTICO EN EE. UU., POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 160 MERCADO DE PRODUCTOS ELÉCTRICOS Y ELECTRÓNICOS EN COMPUESTOS DE PLÁSTICO DE EE. UU., POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 161 MERCADO DE DISPOSITIVOS MÉDICOS DE ESTADOS UNIDOS EN EL MERCADO DE COMPUESTOS DE PLÁSTICO, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 162 MERCADO DE MUEBLES EN COMPUESTOS DE PLÁSTICO DE EE. UU., POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 163 MERCADO DE ENERGÍA Y PODER EN COMPUESTOS DE PLÁSTICO EN EE. UU., POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 164 MERCADO DE COMPUESTOS PLÁSTICOS DE LA INDUSTRIA AEROESPACIAL Y DE DEFENSA DE EE. UU., POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 165 MERCADO DE COMPUESTOS PLÁSTICOS DE CANADÁ, POR TIPO DE POLÍMERO, 2018-2032 (MILES DE USD)

TABLA 166 MERCADO DE COMPUESTOS PLÁSTICOS DE CANADÁ, POR TIPO DE POLÍMERO, 2018-2032 (KILOTONELADAS)

TABLA 167 MERCADO DE TERMOPLÁSTICOS EN COMPUESTOS PLÁSTICOS DE CANADÁ, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 168 MERCADO DE POLIETILENO (PE) EN COMPUESTOS PLÁSTICOS DE CANADÁ, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 169 MERCADO DE PLÁSTICOS DE INGENIERÍA EN CANADÁ, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 170 PLÁSTICOS TERMOENDURECIBLES EN EL MERCADO DE COMPUESTOS DE PLÁSTICO DE CANADÁ, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 171 MERCADO DE BIOPLÁSTICOS EN COMPUESTOS PLÁSTICOS DE CANADÁ, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 172 MERCADO DE COMPUESTOS PLÁSTICOS DE CANADÁ, POR TIPO DE RELLENO, 2018-2032 (MILES DE USD)

TABLA 173 RELLENOS MINERALES EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE CANADÁ, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 174 MERCADO DE REFUERZOS DE COMPUESTOS PLÁSTICOS DE CANADÁ, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 175 ADITIVOS EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE CANADÁ, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 176 MERCADO DE COMPUESTOS DE PLÁSTICO DE CANADÁ, POR PROCESO DE FABRICACIÓN, 2018-2032 (MILES DE USD)

TABLA 177 MERCADO DE COMPUESTOS DE PLÁSTICO DE CANADÁ, POR PROCESO DE FABRICACIÓN, 2018-2032 (KILOTONELADAS)

TABLA 178 MERCADO DE EXTRUSIÓN DE COMPUESTOS DE PLÁSTICO EN CANADÁ, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 179 MERCADO DE EXTRUSIÓN DE PLÁSTICOS EN CANADÁ, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 180 MERCADO DE COMPUESTOS DE PLÁSTICO BASADOS EN MOLDEO POR INYECCIÓN EN CANADÁ, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 181 COMPACTACIÓN/PRESIONADO EN EL MERCADO DE COMPUESTOS DE PLÁSTICO DE CANADÁ, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 182 MERCADO DE MEZCLA DE AMASADORAS/BANBURY EN LA FABRICACIÓN DE COMPUESTOS DE PLÁSTICO DE CANADÁ, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 183 MERCADO DE COMPUESTOS PLÁSTICOS DE CANADÁ, POR PROPIEDADES, 2018-2032 (MILES DE USD)

TABLA 184 MERCADO DE COMPUESTOS PLÁSTICOS DE CANADÁ, POR APLICACIÓN, 2018-2032 (MILES DE USD)

TABLA 185 MERCADO DE COMPUESTOS PLÁSTICOS DE CANADÁ, POR APLICACIÓN, 2018-2032 (KILOTONELADAS)

TABLA 186 MERCADO DE COMPUESTOS DE PLÁSTICO EN AUTOMÓVILES DE CANADÁ, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 187 COMPONENTES INTERIORES DE CANADÁ EN EL MERCADO DE COMPUESTOS PLÁSTICOS, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 188 PIEZAS DE CARROCERÍA EXTERIOR EN EL MERCADO DE COMPUESTOS DE PLÁSTICO DE CANADÁ, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 189 APLICACIONES INTERNAS EN CANADÁ EN EL MERCADO DE COMPUESTOS PLÁSTICOS, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 190 MERCADO DE ENVASES DE PLÁSTICO EN CANADÁ, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 191 MERCADO DE ENVASES DE ALIMENTOS Y BEBIDAS EN CANADÁ, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 192 MERCADO DE ENVASES INDUSTRIALES DE CANADÁ EN COMPUESTOS DE PLÁSTICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 193 MERCADO DE ENVASES DE BIENES DE CONSUMO EN CANADÁ, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 194 MERCADO DE CONSTRUCCIÓN Y EDIFICACIÓN DE PLÁSTICOS EN CANADÁ, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 195 MERCADO DE PRODUCTOS ELÉCTRICOS Y ELECTRÓNICOS EN COMPUESTOS DE PLÁSTICO DE CANADÁ, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 196 MERCADO DE DISPOSITIVOS MÉDICOS DE CANADÁ EN COMPUESTOS DE PLÁSTICO, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 197 MERCADO DE MUEBLES DE CANADÁ EN COMPUESTOS DE PLÁSTICO, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 198 MERCADO DE ENERGÍA Y ELECTRICIDAD EN COMPUESTOS DE PLÁSTICO EN CANADÁ, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 199 MERCADO DE COMPUESTOS PLÁSTICOS DE LA INDUSTRIA AEROESPACIAL Y DE DEFENSA DE CANADÁ, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 200 MERCADO DE COMPUESTOS PLÁSTICOS DE MÉXICO, POR TIPO DE POLÍMERO, 2018-2032 (MILES DE USD)

TABLA 201 MERCADO DE COMPUESTOS PLÁSTICOS DE MÉXICO, POR TIPO DE POLÍMERO, 2018-2032 (KILOTONELADAS)

TABLA 202 MERCADO DE TERMOPLÁSTICOS EN COMPUESTOS PLÁSTICOS DE MÉXICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 203 MERCADO DE POLIETILENO (PE) EN COMPUESTOS PLÁSTICOS DE MÉXICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 204 PLÁSTICOS DE INGENIERÍA EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE MÉXICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 205 PLÁSTICOS TERMOESTABLECIDOS EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE MÉXICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 206 BIOPLÁSTICOS EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE MÉXICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 207 MERCADO DE COMPUESTOS PLÁSTICOS DE MÉXICO, POR TIPO DE RELLENO, 2018-2032 (MILES DE USD)

TABLA 208 RELLENOS MINERALES EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE MÉXICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 209 MERCADO DE REFUERZOS DE COMPUESTOS PLÁSTICOS EN MÉXICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 210 ADITIVOS EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE MÉXICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 211 MERCADO DE COMPUESTOS PLÁSTICOS EN MÉXICO, POR PROCESO DE FABRICACIÓN, 2018-2032 (MILES DE USD)

TABLA 212 MERCADO DE COMPUESTOS PLÁSTICOS EN MÉXICO, POR PROCESO DE FABRICACIÓN, 2018-2032 (KILOTONELADAS)

TABLA 213 MERCADO DE EXTRUSIÓN EN COMPUESTOS PLÁSTICOS EN MÉXICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 214 MERCADO DE EXTRUSIÓN EN COMPUESTOS PLÁSTICOS EN MÉXICO, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 215 MERCADO DE COMPUESTOS DE PLÁSTICO BASADOS EN MOLDEO POR INYECCIÓN EN MÉXICO, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 216 COMPACTACIÓN/PRESIONADO EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE MÉXICO, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 217 MERCADO DE MÉXICO DE AMASADORAS/MEZCLAS BANBURY EN LA FABRICACIÓN DE COMPUESTOS DE PLÁSTICO, POR SISTEMA DE PELETIZACIÓN, 2018-2032 (MILES DE USD)

TABLA 218 MERCADO DE COMPUESTOS PLÁSTICOS DE MÉXICO, POR PROPIEDADES, 2018-2032 (MILES DE USD)

TABLA 219 MERCADO DE COMPUESTOS PLÁSTICOS DE MÉXICO, POR APLICACIÓN, 2018-2032 (MILES DE USD)

TABLA 220 MERCADO DE COMPUESTOS PLÁSTICOS DE MÉXICO, POR APLICACIÓN, 2018-2032 (KILOTONELADAS)

TABLA 221 MERCADO AUTOMOTRIZ DE COMPUESTOS PLÁSTICOS EN MÉXICO, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 222 COMPONENTES INTERIORES DE MÉXICO EN EL MERCADO DE COMPUESTOS PLÁSTICOS, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 223 PARTES EXTERIORES DE CARROCERÍA EN EL MERCADO DE COMPUESTOS PLÁSTICOS DE MÉXICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 224 APLICACIONES INTERNAS EN MÉXICO EN EL MERCADO DE COMPUESTOS PLÁSTICOS, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 225 MERCADO DE ENVASES DE PLÁSTICO EN MÉXICO, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 226 MERCADO DE ENVASES DE ALIMENTOS Y BEBIDAS EN MÉXICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 227 MERCADO DE EMPAQUES INDUSTRIALES EN COMPUESTOS PLÁSTICOS DE MÉXICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 228 MERCADO DE ENVASES DE BIENES DE CONSUMO EN MÉXICO, POR TIPO, 2018-2032 (MILES DE USD)

TABLA 229 MERCADO DE CONSTRUCCIÓN Y EDIFICACIÓN DE COMPUESTOS PLÁSTICOS EN MÉXICO, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 230 MERCADO DE PRODUCTOS ELÉCTRICOS Y ELECTRÓNICOS EN COMPUESTOS PLÁSTICOS DE MÉXICO, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 231 MERCADO DE DISPOSITIVOS MÉDICOS EN COMPUESTOS PLÁSTICOS DE MÉXICO, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 232 MERCADO DE MUEBLES EN MÉXICO EN COMPUESTOS DE PLÁSTICO, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 233 MERCADO DE ENERGÍA Y ELECTRICIDAD EN MÉXICO, POR CATEGORÍA, 2018-2032 (MILES DE USD)

TABLA 234 MERCADO DE COMPUESTOS PLÁSTICOS DE LA INDUSTRIA AEROESPACIAL Y DE DEFENSA DE MÉXICO, POR CATEGORÍA, 2018-2032 (MILES DE USD)

Lista de figuras

FIGURA 1 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE

FIGURA 2 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE: TRIANGULACIÓN DE DATOS

FIGURA 3 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE: ANÁLISIS DROC

FIGURA 4 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE: ANÁLISIS DEL MERCADO DE AMÉRICA DEL NORTE VS. REGIONAL

FIGURA 5 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE: ANÁLISIS DE INVESTIGACIÓN DE EMPRESAS

FIGURA 6 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE: MODELADO MULTIVARIADO

FIGURA 7 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE: DATOS DEMOGRÁFICOS DE LAS ENTREVISTAS

FIGURA 8 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE: CUADRÍCULA DE POSICIÓN DE MERCADO DE DBMR

FIGURA 9 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE: CUADRÍCULA DE COBERTURA DE APLICACIÓN DEL MERCADO

FIGURA 10 RESUMEN EJECUTIVO

FIGURA 11 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE: SEGMENTACIÓN

FIGURA 12 CINCO SEGMENTOS COMPRENDEN EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO DE POLÍMERO

FIGURA 13 DECISIONES ESTRATÉGICAS

FIGURA 14 SE ESPERA QUE EL CAMBIO HACIA COMPUESTOS PLÁSTICOS RECICLABLES Y BIODEGRADABLES DEBIDO A LA REGULACIÓN AMBIENTAL IMPULSE EL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE DURANTE EL PERÍODO PRONOSTICADO DE 2025 A 2032

FIGURA 15 SE ESPERA QUE EL SEGMENTO DE TERMOPLÁSTICOS REPRESENTE LA MAYOR PARTICIPACIÓN DEL MERCADO DE COMPUESTOS DE PLÁSTICO DE AMÉRICA DEL NORTE EN 2025 Y 2032

FIGURA 16 ANÁLISIS DE LAS CINCO FUERZAS DE PORTER

FIGURA 17 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE: ANÁLISIS DE LA CADENA DE VALOR

FIGURA 18 ESCENARIO DE IMPORTACIÓN Y EXPORTACIÓN (MILES DE USD)

FIGURA 19 CAPACIDAD DE PRODUCCIÓN DE LOS MEJORES FABRICANTES

FIGURA 20 CÓDIGO IPC V/S NÚMERO DE PATENTES

FIGURA 21 NÚMERO DE PATENTES POR AÑO

FIGURA 22 NÚMERO DE PATENTES POR REGIÓN/PAÍS

FIGURA 23 PRINCIPALES SOLICITANTES DE PATENTES

FIGURA 24 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, 2024-2032, PRECIO DE VENTA PROMEDIO (USD/KG)

FIGURA 25 IMPULSORES, RESTRICCIONES, OPORTUNIDADES Y DESAFÍOS DEL MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE

FIGURA 26 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE: POR TIPO DE POLÍMERO, 2024

FIGURA 27 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR TIPO DE FILTRO, 2024

FIGURA 28 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR PROCESO DE FABRICACIÓN, 2024

FIGURA 29 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR PROPIEDADES, 2024

FIGURA 30 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE, POR APLICACIÓN, 2024

FIGURA 31 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE: INSTANTÁNEA (2024)

FIGURA 32 MERCADO DE COMPUESTOS PLÁSTICOS DE AMÉRICA DEL NORTE: PARTICIPACIÓN DE LA EMPRESA 2024 (%)

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.