Global Aromatase Inhibitor Drug Class Market

Taille du marché en milliards USD

TCAC :

%

USD

4.73 Billion

USD

7.14 Billion

2025

2033

USD

4.73 Billion

USD

7.14 Billion

2025

2033

| 2026 –2033 | |

| USD 4.73 Billion | |

| USD 7.14 Billion | |

| % | |

|

Global Aromatase Inhibiteur de la classe des médicaments Segmentation du marché, par médicament (Anastrozole, Létrozole, Exémestane, Formestane, Fadrozole, etc.), Type (Inhibiteurs d'aromatase non stéroïdiens et inhibiteurs d'aromatase stéroïdienne), Application (traitement contre le cancer du sein, traitement de la fertilité, etc.), Utilisateur final (Hôpitals, cliniques spécialisées, soins à domicile, etc.) - Tendances de l'industrie et prévisions à 2033

Classe de médicament Inhibiteur de l'aromatase Taille du marché

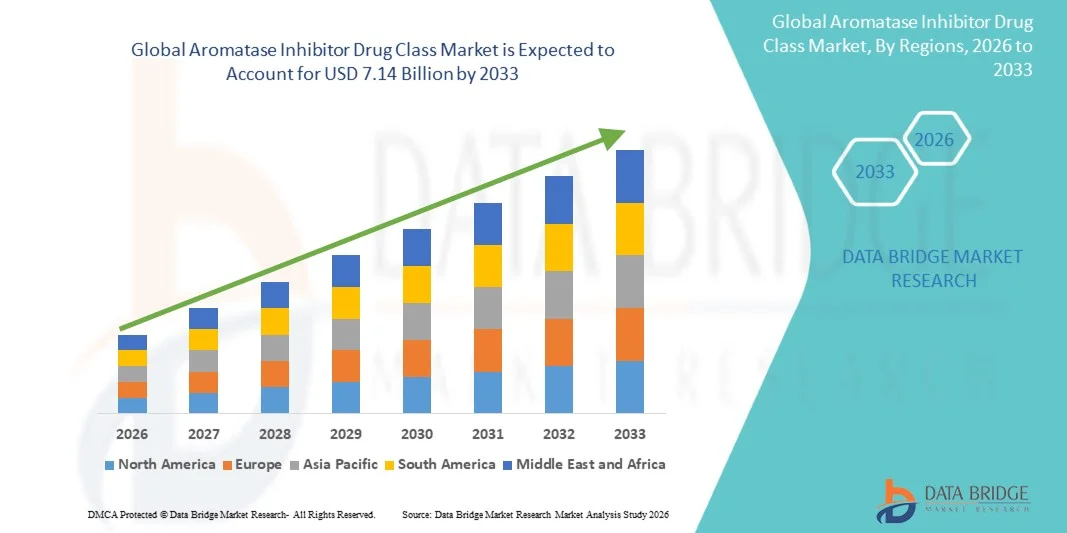

- La taille du marché de l'inhibiteur mondial de l'aromatase a été évaluée à4,73 milliards de dollars en 2025et devrait atteindre7,14 milliards de dollars en 2033, à unTCAC de 5,30%pendant la période de prévision

- La croissance du marché est en grande partie due à l'augmentation de la prévalencecancer du sein positif aux récepteurs hormonaux, l'adoption croissante dethérapies hormonales, et l'utilisation croissante d'inhibiteurs de l'aromatase comme options de traitement de première intention et d'adjuvant, en particulier chez les femmes ménopausées

- De plus, l'augmentation des données cliniques appuyant l'amélioration des résultats en matière de survie, une plus grande disponibilité de formulations génériques rentables et une sensibilisation accrue aux traitements anticancéreux à base endocrine renforcent la demande d'inhibiteurs de l'aromatase, ce qui stimule significativement la croissance globale du marché.

Inhibiteur de l'aromatase

- Les inhibiteurs de l'aromatase, qui suppriment la production d'oestrogènes en inhibant l'enzyme aromatase, sont des composants essentiels de la thérapie hormonale pour les cancers positifs pour les récepteurs d'oestrogènes, en particulier le cancer du sein, et sont largement utilisés dans les milieux hospitaliers, cliniques et ambulatoires.

- La demande croissante de médicaments inhibiteurs de l'aromatase est principalement attribuable à l'augmentation de l'incidence mondiale du cancer du sein, à la préférence croissante pour des traitements endocriniens ciblés par rapport à la chimiothérapie et à l'utilisation croissante de ces agents dans les protocoles de traitement précoce et métastatique

- L'Amérique du Nord a dominé le marché de la classe des médicaments inhibiteurs de l'aromatase avec la plus grande part de revenus de 38,6% en 2025, soutenue par une infrastructure d'oncologie avancée, des taux d'adoption élevés de traitements, des cadres de remboursement favorables et une forte présence de fabricants pharmaceutiques de marque et génériques, les États-Unis représentant la majorité de la demande régionale.

- On s'attend à ce que l'Asie-Pacifique soit la région qui connaît la croissance la plus rapide du marché des inhibiteurs de l'aromatase pendant la période de prévision en raison de la sensibilisation accrue au cancer, de l'amélioration de l'accès aux soins oncologiques, de l'augmentation des dépenses de soins de santé et de la disponibilité accrue d'inhibiteurs génériques de l'aromatase dans des pays comme la Chine et l'Inde.

- Le segment des inhibiteurs de l'aromatase non stéroïdienne a dominé le marché avec une part de 61,4 % en 2025, en raison de leur utilisation clinique généralisée, de leur fort profil d'efficacité et de leur rôle de première ligne dans le traitement du cancer du sein positif aux récepteurs hormonaux

Portée du rapport et segmentation du marché des inhibiteurs de l'aromatase

| Attributs | Classe de médicaments inhibiteurs de l'aromatase Principales perspectives du marché |

| Segments couverts |

|

| Pays couverts | Amérique du Nord

Europe

Asie-Pacifique

Moyen-Orient et Afrique

Amérique du Sud

|

| Principaux acteurs du marché |

|

| Possibilités de marché |

|

| Infos sur la valeur ajoutée | En plus des renseignements sur les scénarios du marché comme la valeur du marché, le taux de croissance, la segmentation, la couverture géographique et les principaux intervenants, les rapports de marché établis par Data Bridge Market Research comprennent également une analyse approfondie des experts, l'épidémiologie des patients, l'analyse des pipelines, l'analyse des prix et le cadre réglementaire. |

Classe de médicaments Inhibiteurs de l'aromatase Tendances du marché

L'utilisation accrue d'inhibiteurs d'aromatase dans les thérapies personnalisées et combinées

- L'adoption croissante d'approches thérapeutiques personnalisées et de régimes combinés, en particulier dans la prise en charge du cancer du sein par les récepteurs hormonaux positifs, pour améliorer l'efficacité et les résultats des patients constitue une tendance importante et accélérée sur le marché mondial des inhibiteurs de l'aromatase.

- Par exemple, les inhibiteurs de l'aromatase tels que le létrozole et l'anastrozole sont de plus en plus prescrits en association avecInhibiteurs de CDK4/6dans le cancer du sein avancé et métastatique, améliorant significativement la survie sans progression par rapport à la monothérapie

- Les progrès dans les tests de biomarqueurs et le profil génomique permettent aux cliniciens de mieux identifier les patients qui sont les plus susceptibles de bénéficier de thérapies à base d'inhibiteurs de l'aromatase, en soutenant des décisions de traitement plus ciblées et optimisées

- L'évolution croissante vers des durées prolongées de traitement adjuvant, où les inhibiteurs de l'aromatase sont utilisés au-delà de cinq ans chez certains patients, influe davantage sur les modèles de prescription et la demande à long terme de ces médicaments.

- L'intégration d'inhibiteurs de l'aromatase dans l'évolution des lignes directrices cliniques et de la pratique de l'oncologie dans le monde réel renforce leur rôle de thérapies fondamentales dans les cancers hormonaux.

- Les essais cliniques en cours évaluant les inhibiteurs de l'aromatase à des stades antérieurs de la maladie et les milieux préventifs élargissent leur portée thérapeutique et leur potentiel commercial à long terme

- L'augmentation de la production de données probantes dans le monde réel favorise l'acceptation plus large des régimes à base d'inhibiteurs de l'aromatase chez les oncologues, ce qui renforce la confiance dans l'innocuité et l'efficacité à long terme.

- Cette tendance vers des stratégies de traitement plus adaptées, fondées sur des données probantes et axées sur la combinaison consiste à remodeler les normes thérapeutiques, ce qui incite les entreprises pharmaceutiques à investir dans la gestion du cycle de vie et les essais cliniques en association.

Dynamique du marché des inhibiteurs de l'aromatase

Chauffeur

Le fardeau croissant du cancer du sein et la préférence pour la thérapie endocrinienne

- L'augmentation de l'incidence mondiale du cancer du sein positif aux récepteurs hormonaux, en particulier chez les femmes ménopausées, est l'un des principaux moteurs de la demande de thérapies inhibiteurs de l'aromatase

- Par exemple, en mars 2025, plusieurs sociétés d'oncologie ont réaffirmé les inhibiteurs de l'aromatase en tant que traitement adjuvant de première ligne dans les recommandations cliniques actualisées pour le cancer du sein au stade précoce

- Comparativement à la chimiothérapie, les inhibiteurs de l'aromatase offrent un mécanisme d'action ciblé avec une tolérance améliorée, ce qui conduit le médecin et le patient à préférer les approches de traitement basées sur l'endocrine

- L'élargissement de l'accès au diagnostic du cancer, aux programmes de dépistage et aux soins oncologiques dans les économies émergentes accroît le bassin de patients admissibles au traitement des inhibiteurs de l'aromatase

- Les initiatives gouvernementales de sensibilisation au cancer et les programmes de dépistage permettent un diagnostic plus précoce, augmentant ainsi les taux d'initiation à la thérapie des inhibiteurs de l'aromatase

- La connaissance croissante du médecin des protocoles de traitement des inhibiteurs de l'aromatase et des données sur les résultats à long terme renforce la confiance prescrite dans diverses populations de patients.

- La disponibilité généralisée d'inhibiteurs génériques de l'aromatase a amélioré l'accessibilité et l'adhésion, favorisant ainsi une croissance soutenue du marché dans les régions développées et en développement.

Restriction/Défi

Effets secondaires à long terme et préoccupations liées au traitement

- L'utilisation à long terme d'inhibiteurs de l'aromatase est associée à des effets indésirables tels que la perte de densité osseuse, la douleur articulaire et les risques cardiovasculaires, qui peuvent limiter l'adhésion et la persistance du patient au traitement.

- Par exemple, des études cliniques dans le monde réel ont rapporté l'arrêt du traitement chez certains patients en raison de symptômes musculosquelettiques associés à l'utilisation prolongée d'un inhibiteur de l'aromatase

- La gestion de ces effets secondaires au moyen de thérapies de soutien, de stratégies de surveillance et d'éducation des patients ajoute au fardeau global du traitement et aux coûts des soins de santé

- Bien que l'on étudie de nouvelles stratégies de dosage et des interventions de soutien, les préoccupations concernant la qualité de vie demeurent un obstacle à la prolongation du traitement.

- Il sera essentiel de relever les défis liés à l'adhésion en améliorant la gestion des patients, les stratégies d'atténuation des risques et les thérapies endocriniennes de la prochaine génération pour soutenir l'expansion à long terme du marché.

- Une sensibilisation limitée des patients à la prise en charge des effets indésirables associés aux inhibiteurs de l'aromatase peut conduire à un arrêt prématuré et à des résultats sous-optimaux du traitement.

- La variabilité de la couverture des remboursements et de l'accès aux services de soins de soutien dans les régions complique encore l'adhésion à long terme à la thérapie des inhibiteurs de l'aromatase.

Catégorie de médicament Inhibiteur de l'aromatase Portée du marché

Le marché est segmenté en fonction du médicament, du type, de l'application et de l'utilisateur final.

- Par drogue

Sur la base du médicament, le marché mondial des inhibiteurs de l'aromatase est segmenté en anastrozole, létrozole, exémestane, formestane, fadrozole et autres. Le segment du létrozole domine le marché avec la plus grande part de revenus en 2025, en raison de son utilisation généralisée comme traitement de première ligne dans le cancer du sein positif aux récepteurs hormonaux et de son profil d'efficacité clinique solide. Le létrozole est largement prescrit en milieu adjuvant et métastatique, appuyé par de solides lignes directrices cliniques et des données sur les résultats à long terme. Sa large acceptation parmi les oncologues, sa disponibilité dans les formes génériques et de marque, et son utilisation croissante hors étiquette dans les traitements de fertilité renforcent encore sa domination. En outre, le letrozole bénéficie d'une couverture de remboursement favorable sur les principaux marchés, soutenant une forte adhésion au traitement et une demande soutenue.

Le segment de l'exémestane devrait connaître la croissance la plus rapide au cours de la période de prévision, en raison de l'utilisation croissante chez les patients qui développent une résistance ou une intolérance aux inhibiteurs de l'aromatase non stéroïdienne. En tant qu'inhibiteur des stéroïdes avec un mécanisme d'action distinct, l'exémestane est de plus en plus utilisé dans les traitements endocriniens séquentiels et prolongés. L'adoption croissante de combinaisons thérapeutiques et la préférence clinique croissante pour des stratégies de changement dans la gestion à long terme du cancer du sein alimentent sa croissance. L'élargissement des données cliniques à l'appui de son rôle dans l'amélioration de la survie sans maladie accélère encore l'adoption du marché.

- Par type

Selon le type, le marché est segmenté en inhibiteurs de l'aromatase non stéroïdienne et en inhibiteurs de l'aromatase stéroïdienne. Le segment des inhibiteurs de l'aromatase non stéroïdienne a dominé le marché en 2025 avec une part de marché de 61,4 %, en raison de l'utilisation intensive d'anastrozole et de létrozole comme thérapies standard de soins. Ces médicaments sont largement recommandés dans les lignes directrices internationales de traitement en raison de leur efficacité prouvée, des profils d'innocuité favorables et de la facilité d'administration orale. Leur forte présence dans les protocoles de traitement du cancer du sein au stade précoce et métastatique contribue de façon significative à la domination du marché. De plus, la grande disponibilité des versions génériques a amélioré l'accessibilité et l'accessibilité, favorisant l'adoption à grande échelle dans les régions développées et émergentes.

Le segment des inhibiteurs de l'aromatase stéroïdienne devrait croître le plus rapidement au cours de la période de prévision, en raison de leur utilisation croissante chez les patients nécessitant des traitements endocriniens alternatifs ou séquentiels. Les inhibiteurs stéroïdiens tels que l'exémestane gagnent en traction grâce à leur mécanisme de liaison irréversible, qui peut offrir des avantages en cas de progression de la maladie. La sensibilisation accrue des cliniciens au séquençage personnalisé et à la gestion de la résistance favorise la croissance du segment. Les essais cliniques en cours et les stratégies de traitement adjuvant élargi renforcent encore la demande d'inhibiteurs stéroïdiens.

- Par demande

Sur la base de l'application, le marché est segmenté en traitement du cancer du sein, traitement de la fertilité, et d'autres applications. Le segment du traitement du cancer du sein a dominé le marché avec la plus grande part des revenus en 2025, en raison de la forte prévalence du cancer du sein positif aux récepteurs hormonaux dans le monde. Les inhibiteurs de l'aromatase sont un traitement fondamental pour les femmes ménopausées, utilisés dans les milieux adjuvant, néoadjuvant et métastatique. Une forte approbation clinique, une longue durée de traitement et une augmentation des taux de survie ont entraîné une demande soutenue et récurrente. En outre, l'intégration d'inhibiteurs de l'aromatase dans des régimes combinés avec des thérapies ciblées soutient davantage la domination du marché.

Le segment du traitement de la fertilité devrait connaître la croissance la plus rapide au cours de la période prévue, en raison de l'utilisation croissante du létrozole pour l'induction de l'ovulation et de la prise en charge du syndrome ovaire polykystique (SOP). L'augmentation des taux d'infertilité, le retard des grossesses et l'acceptation croissante des traitements pharmacologiques de fertilité alimentent la demande. Le létrozole est de plus en plus préféré aux thérapies traditionnelles en raison de l'amélioration des résultats de la grossesse et des profils de risque plus faibles. L'expansion des cliniques de fertilité et la sensibilisation aux applications hors étiquette dans les marchés émergents accélèrent la croissance de ce segment.

- Par Utilisateur final

Sur la base de l'utilisateur final, le marché est segmenté en hôpitaux, cliniques spécialisées, soins à domicile et autres. Le segment des hôpitaux a dominé le marché en 2025, appuyé par la prestation centralisée de soins oncologiques, l'accès à des installations de diagnostic spécialisées et des approches de traitement multidisciplinaires. Les hôpitaux servent de centres primaires pour le diagnostic du cancer, l'initiation du traitement et la gestion des stades avancés de la maladie. Des volumes plus élevés de patients, des protocoles de traitement structurés et de solides cadres de remboursement contribuent à la part de revenus du segment. De plus, les hôpitaux jouent un rôle clé dans l'administration de combinaisons thérapeutiques et dans la surveillance des résultats à long terme du traitement.

On prévoit que le segment des soins à domicile connaîtra la croissance la plus rapide au cours de la période de prévision, en raison de la nature orale des thérapies des inhibiteurs de l'aromatase et de la transition vers la prise en charge externe et à domicile du cancer. L'amélioration de l'éducation des patients, la surveillance numérique de la santé et l'importance croissante accordée à la qualité de vie appuient cette tendance. Les établissements de soins à domicile permettent d'adhérer à la thérapie à long terme avec des coûts de soins de santé réduits et des visites à l'hôpital. La croissance de la population âgée et la préférence croissante pour des modèles de soins pratiques et axés sur le patient accélèrent encore la croissance de ce segment

Inhibiteur de l'aromatase Classe de drogue Marché Analyse régionale

- L'Amérique du Nord a dominé le marché de la classe des médicaments inhibiteurs de l'aromatase avec la plus grande part de revenus de 38,6% en 2025, soutenue par une infrastructure d'oncologie avancée, des taux d'adoption élevés de traitements, des cadres de remboursement favorables et une forte présence de fabricants pharmaceutiques de marque et génériques, les États-Unis représentant la majorité de la demande régionale.

- Les patients et les fournisseurs de soins de santé de la région préfèrent fortement les inhibiteurs de l'aromatase en raison de leur efficacité clinique avérée, de la disponibilité d'options à la fois de marque et génériques, et d'une forte inclusion dans les lignes directrices de traitement standard pour la prise en charge du cancer du sein

- Cette adoption généralisée est soutenue par des politiques de remboursement favorables, un accès rapide à des diagnostics de cancer avancés et une grande sensibilisation aux thérapies endocriniennes, établissant les inhibiteurs de l'aromatase comme un traitement de base dans les hôpitaux et les hôpitaux ambulatoires.

Inhibiteur américain de l'aromatase

Le marché américain de la classe des médicaments inhibiteurs de l'aromatase a remporté la plus grande part de revenus en Amérique du Nord en 2025, en raison de l'incidence élevée du cancer du sein positif aux récepteurs hormonaux et de l'adoption précoce de thérapies endocriniennes de pointe. Aux États-Unis, les médecins privilégient de plus en plus les inhibiteurs de l'aromatase en raison de leur forte efficacité clinique, de leurs bienfaits à long terme pour la survie et de leur inclusion comme traitement de première ligne dans les lignes directrices nationales en oncologie. La disponibilité généralisée de médicaments génériques et de marque, conjuguée à des politiques de remboursement favorables, soutient davantage la croissance du marché. De plus, une forte participation aux essais cliniques et l'adoption rapide de régimes combinés avec des thérapies ciblées continuent de favoriser l'expansion du marché.

Europe Inhibiteur de l'aromatase Classe de médicaments Aperçu du marché

Le marché européen des inhibiteurs de l'aromatase devrait s'étendre à un important TCAC au cours de la période de prévision, principalement en raison de l'augmentation de la prévalence du cancer et des systèmes de santé publique bien établis. L'accent mis de plus en plus sur le diagnostic précoce du cancer et les protocoles de traitement normalisés dans les pays européens favorise une demande constante d'inhibiteurs de l'aromatase. Les fournisseurs européens de soins de santé sont favorables à ces thérapies pour leur rapport coût-efficacité et des preuves cliniques solides à long terme. On observe une croissance dans les hôpitaux et les services ambulatoires, appuyée par l'utilisation croissante de génériques et l'élargissement de l'accès aux thérapies endocriniennes.

Inhibiteurs de l'aromatase au Royaume-Uni

Le marché de la classe des médicaments inhibiteurs de l'aromatase au Royaume-Uni devrait croître à un TCAC remarquable au cours de la période de prévision, grâce à l'adoption d'un traitement du cancer du sein dirigé par des lignes directrices au sein du Service national de santé. La sensibilisation accrue au cancer du sein positif aux récepteurs hormonaux et l'augmentation des initiatives de dépistage contribuent à un diagnostic plus précoce et à des taux de traitement plus élevés. La préférence pour des inhibiteurs de l'aromatase générique rentables soutient davantage la demande soutenue. En outre, les activités de recherche en cours et les études de résultats dans le monde réel au Royaume-Uni continuent de renforcer la confiance des médecins à l'égard de la thérapie endocrinienne à long terme.

Allemagne Inhibiteur de l'aromatase Classe de médicaments Aperçu du marché

Le marché allemand des inhibiteurs de l'aromatase devrait s'étendre à un TCAC considérable, alimenté par une infrastructure d'oncologie avancée et une forte importance accordée au traitement fondé sur des données probantes. Les cliniciens allemands adoptent largement des inhibiteurs de l'aromatase en raison de leur efficacité avérée et de leur profil de sécurité favorable. Le pays dispose d'une solide base de fabrication pharmaceutique et d'un solide environnement de remboursement pour améliorer l'accès aux thérapies de marque et génériques. L'accent mis de plus en plus sur la médecine personnalisée et les stratégies séquentielles de traitement endocrinien stimule la croissance du marché en Allemagne.

Inhibiteurs de l'aromatase en Asie-Pacifique

Le marché des inhibiteurs de l'aromatase en Asie et dans le Pacifique est sur le point de croître le plus rapidement possible durant la période de prévision, en raison de l'augmentation de l'incidence du cancer, de l'amélioration de l'accès aux soins de santé et de la sensibilisation croissante aux thérapies hormonales. L'urbanisation rapide, l'expansion des infrastructures oncologiques et l'augmentation des investissements publics dans les soins de santé dans des pays comme la Chine, le Japon et l'Inde stimulent l'adoption de traitements. La disponibilité croissante de génériques peu coûteux améliore considérablement l'accès des patients. De plus, une participation accrue aux essais cliniques mondiaux favorise une plus large acceptation des thérapies des inhibiteurs de l'aromatase dans toute la région.

Japon Inhibiteur de l'aromatase Classe de drogue Aperçu du marché

Le marché japonais des inhibiteurs de l'aromatase prend de l'ampleur en raison du vieillissement de la population et de la forte prévalence du cancer du sein chez les femmes ménopausées. Le système de santé japonais met fortement l'accent sur le diagnostic précoce et la prise en charge à long terme des maladies, en soutenant l'utilisation soutenue des thérapies endocriniennes. Les inhibiteurs de l'aromatase sont largement prescrits en raison de leur profil bénéfice-risque favorable. De plus, une forte adhésion des médecins aux lignes directrices cliniques et l'adoption croissante de combinaisons thérapeutiques contribuent à la croissance régulière du marché.

Inde Inhibiteur de l'aromatase Classe de médicaments Aperçu du marché

En 2025, le marché indien des inhibiteurs de l'aromatase a représenté une part importante des revenus en Asie-Pacifique, en raison de l'augmentation du fardeau du cancer, de l'augmentation des capacités diagnostiques et de la sensibilisation accrue aux soins de santé. La forte industrie pharmaceutique générique de l'Inde assure une grande disponibilité d'inhibiteurs d'aromatase abordables, améliorant l'accès au traitement dans les zones urbaines et semi-urbaines. Les programmes gouvernementaux de lutte contre le cancer et la pénétration croissante des centres d'oncologie privés appuient davantage l'expansion du marché. De plus, l'acceptation croissante du traitement endocrinien à long terme contribue à une croissance soutenue du marché indien.

Part de marché de l'inhibiteur de l'aromatase

L'industrie de la classe des médicaments inhibiteurs de l'aromatase est principalement dirigée par des entreprises bien établies, notamment :

- Pfizer Inc. (États-Unis)

- AstraZeneca (Royaume-Uni)

- Novartis AG (Suisse)

- Sanofi (France)

- Bayer AG (Allemagne)

- Teva Pharmaceutical Industries Ltd. (Israël)

- Sandoz International GmbH (Suisse)

- Apotex Inc. (Canada)

- Sun Pharmaceutical Industries Ltd. (Inde)

- Dr. Reddy-S Laboratories Ltd. (Inde)

- Cipla Limited (Inde)

- Hétero Drugs Limited (Inde)

- Zydus Lifesciences Limited (Inde)

- Lupin Limited (Inde)

- Amneal Pharmaceuticals, Inc. (États-Unis)

- Hikma Pharmaceuticals PLC (Royaume-Uni)

- ANI Pharmaceuticals, Inc. (États-Unis)

- Fresenius Kabi AG (Allemagne)

- Mayne Pharma Group Limited (Australie)

Quelles sont les évolutions récentes du marché mondial des inhibiteurs de l'aromatase?

- En août 2025, des recherches publiées ont montré qu'une nouvelle classe de composés appelés inhibiteurs de cysteinylamide polyisoprénylés (IAPC) a démontré une activité puissante contre les cellules cancéreuses du sein résistantes aux inhibiteurs de l'aromatase, ce qui montre que de nouvelles stratégies pour surmonter la résistance dans le traitement de l'IA

- En juillet 2025, un essai de phase 2 a été lancé pour évaluer le léflutrozole, un inhibiteur de l'aromatase de première classe, pour le traitement de l'infertilité masculine due à une faible testostérone, indiquant une expansion potentielle des applications thérapeutiques de l'IA au-delà de l'oncologie.

- En janvier 2025, une étude clinique a révélé que la combinaison de la capécitabine métronomique et d'un inhibiteur de l'aromatase augmentait significativement la survie sans progression et la survie globale chez les patients atteints de cancer du sein HR+ par rapport à l'inhibiteur de l'aromatase seul, suggérant que les stratégies d'association pourraient améliorer les résultats thérapeutiques.

- En décembre 2024, la Commission européenne a approuvé l'utilisation du ribociclib plus un inhibiteur de l'aromatase comme traitement adjuvant pour le cancer du sein précoce négatif de HR+/HER2, en alignant la politique réglementaire européenne sur les indications des États-Unis et en élargissant l'accès à l'ensemble des États membres de l'UE.

- En septembre 2024, la Food and Drug Administration (FDA) des États-Unis a approuvé le ribociclib (Kisqali) en association avec un inhibiteur de l'aromatase pour le traitement adjuvant des adultes atteints d'un cancer du sein précoce positif aux hormones (HR+)/HER2-négatif à haut risque de récidive, étendant le rôle des inhibiteurs de l'aromatase au-delà de l'utilisation métastatique à des stades antérieurs, sur la base des données de l'essai de phase III de NATALEE

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.