Global High Drug To Antibody Ratio Adc Therapies Market

Taille du marché en milliards USD

TCAC :

%

USD

2.12 Billion

USD

7.96 Billion

2025

2033

USD

2.12 Billion

USD

7.96 Billion

2025

2033

| 2026 –2033 | |

| USD 2.12 Billion | |

| USD 7.96 Billion | |

| % | |

|

Global High Drug-to-Antibody Ratio ADC Therapies Market Segmentation, Par type de charge utile (inhibiteurs de la topoisomérase, inhibiteurs de microtubules, agents digérants de l'ADN, etc.), Indication (cancer du sein, malignités hématologiques, cancer du poumon, cancer colorectal, etc.), Étape de développement : essais précliniques, cliniques et produits commercialisés) - Tendances de l'industrie et prévisions jusqu'en 2033

Haut rapport drogue-anticorps ADC Thérapies Taille du marché

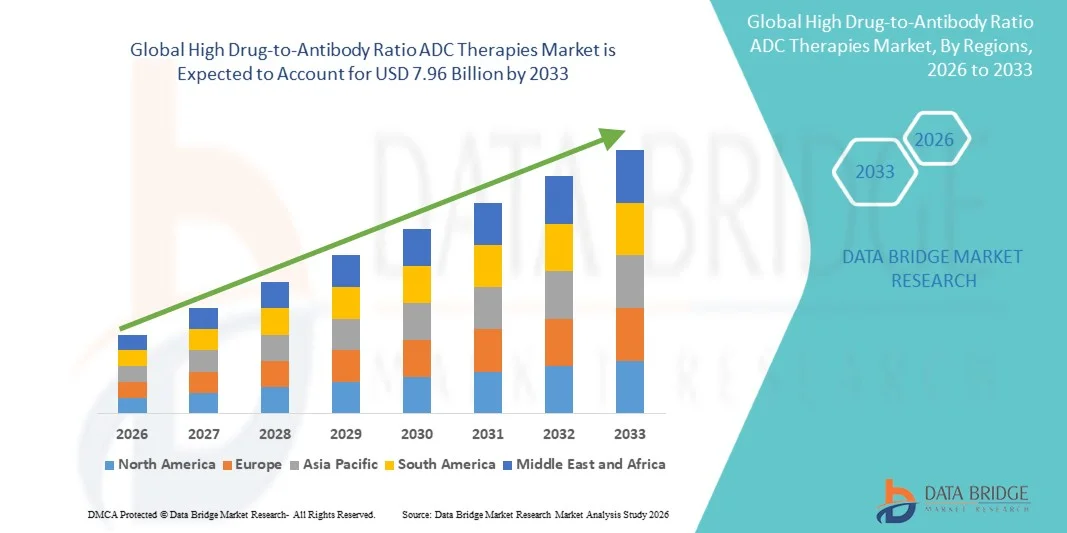

- La taille du marché mondial des thérapies ADC a été évaluée à2,12 milliards de dollars en 2025et devrait atteindre7,96 milliards de dollars en 2033, à unTCAC de 18,00 %pendant la période de prévision

- La croissance du marché est en grande partie alimentée par l'adoption de plus en plus de médicaments antidrogues en oncologie, en raison de leur efficacité thérapeutique accrue, de leur capacité à fournir des charges utiles cytotoxiques plus élevées directement aux cellules tumorales, et des progrès dans les technologies de liaison qui améliorent la stabilité et réduisent la toxicité non ciblée

- De plus, l'augmentation de la demande de thérapies contre le cancer ciblées, l'incidence croissante de tumeurs hématologiques et solides et l'augmentation des investissements dans la recherche et le développement clinique de l'ADC accélèrent l'adoption de thérapies ADC à forte intensité de DAR, ce qui stimule considérablement la croissance générale du marché.

Haut rapport drogue-anticorps ADC Analyse du marché des thérapies

- Les thérapies ADC à ratio médicament-anticorps élevé (DAR), conçues pour fournir des charges utiles plus élevées de médicaments cytotoxiques directement aux cellules tumorales, sont de plus en plus vitales en oncologie en raison de leur efficacité accrue, de la réduction de la toxicité systémique et de la capacité de traiter les tumeurs hématologiques et solides, conduisant à l'adoption en milieu clinique et hospitalier

- La demande croissante de thérapies DAR ADC est principalement alimentée par l'augmentation de la prévalence du cancer, l'accent mis de plus en plus sur les thérapies ciblées et les innovations continues dans les technologies de liaison et de conjugaison ADC, qui améliorent les résultats du traitement et la conformité des patients

- L'Amérique du Nord a dominé le marché des thérapies ADC à fort rapport drogue-anticorps avec la plus grande part de revenus d'environ 39,5 % en 2025, appuyée par une infrastructure d'oncologie avancée, des investissements en R-D élevés, des cadres réglementaires solides et la présence de grands développeurs ADC et de startups en biotechnologie aux États-Unis.

- L'Asie-Pacifique devrait être la région qui connaîtra la croissance la plus rapide pendant la période de prévision, en raison de l'augmentation de l'incidence du cancer, de l'amélioration de l'infrastructure des soins de santé, de l'expansion des essais cliniques et de l'adoption croissante de thérapies ciblées dans des pays comme la Chine, le Japon et l'Inde.

- Le segment des produits commercialisés dominait le marché avec une part des revenus de 44,3 % en 2025, en raison de la présence d'ADC approuvés par la FDA et de leur adoption clinique généralisée.

Portée du rapport et rapport élevé entre les médicaments et les anticorps Thérapies ADC Segmentation du marché

| Attributs | Haut rapport drogue-anticorps ADC Thérapies Principales perspectives du marché |

| Segments couverts |

|

| Pays couverts | Amérique du Nord

Europe

Asie-Pacifique

Moyen-Orient et Afrique

Amérique du Sud

|

| Principaux acteurs du marché |

|

| Possibilités de marché |

|

| Infos sur la valeur ajoutée | En plus des renseignements sur les scénarios de marché comme la valeur marchande, le taux de croissance, la segmentation, la couverture géographique et les principaux intervenants, les rapports de marché établis par Data Bridge Market Research comprennent également une analyse approfondie des experts, l'épidémiologie des patients, l'analyse des pipelines, l'analyse des prix et le cadre réglementaire. |

Haut rapport drogue-anticorps ADC Thérapies Tendances du marché

(en milliers de dollars)Expansion grâce à des technologies novatrices de charge utile et à des progrès cliniques(en milliers de dollars)

- Une tendance significative et accélérée du marché mondial des thérapies ADC à haut rapport médicaments-anticorps (DAR) est la mise au point de nouvelles technologies de liaison et de charge utile qui permettent d'augmenter les ratios médicaments-anticorps tout en maintenant la stabilité et la prestation ciblée. Cette approche améliore l'efficacité thérapeutique et élargit la gamme des cancers traitables, en particulier dans les tumeurs malignes hématologiques et les tumeurs solides

- Par exemple, en 2024, Seagen a présenté une nouvelle génération de candidats à l'ADC à haute DAR ciblant le cancer du sein HER2-positif, montrant des résultats précliniques prometteurs avec une charge utile cytotoxique améliorée et minimisant la toxicité hors cible. De même, l'amélioration du trastuzumab deruxtecan par Daiichi Sankyo's a démontré une augmentation de la DAR tout en préservant la spécificité des anticorps, ce qui a permis d'augmenter la puissance dans les essais cliniques. Ces progrès améliorent les résultats cliniques et la tolérance des patients, favorisant une adoption plus large dans les centres d'oncologie

- De plus, les progrès dans les techniques de conjugaison spécifiques au site et la chimie de la bioconjugaison permettent aux fabricants d'optimiser la DAR sans compromettre la stabilité des anticorps, de réduire les risques d'immunogénicité et d'améliorer les profils pharmacocinétiques.

- La tendance à l'augmentation des CAD DAR s'appuie également sur le nombre croissant d'essais cliniques portant sur des combinaisons avec des immunothérapies, des inhibiteurs des points de contrôle et des chimiothérapies standard, reflétant l'importance croissante des CAD dans les stratégies globales de gestion du cancer

- L'intégration de technologies de fabrication améliorées, telles que les plates-formes automatisées de conjugaison et les méthodes de purification améliorées, accélère le développement d'ADC à haute DAR évolutives, permettant une transition rapide des essais précliniques aux applications cliniques

- Ces innovations façonnent collectivement les attentes en matière de thérapies ADC plus efficaces, ciblées et adaptées aux patients, ce qui stimule l'investissement et l'intérêt pour la recherche en matière de développement ADC à haut risque

Haut rapport drogue-anticorps ADC Dynamique du marché des thérapies

Chauffeur

La demande croissante de thérapies contre le cancer ciblées et d'amélioration des résultats cliniques

- L'augmentation de l'incidence mondiale du cancer, associée à la demande croissante de médicaments de précision, est un facteur important pour l'adoption de thérapies ADC à haute DAR

- Par exemple, la FDA a accéléré l'approbation du deruxtécan fam-trastuzumab en 2022 pour le cancer du sein métastatique HER2-positif a mis en évidence les avantages cliniques des CAD à haut DAR, y compris une meilleure survie sans progression et une réduction de la toxicité systémique. De même, les essais cliniques en cours de Gemtuzumab ozogamicine dans la leucémie myéloïde aiguë démontrent une efficacité accrue chez les patients n'ayant pas répondu à la chimiothérapie conventionnelle.

- Sensibiliser davantage les oncologues aux avantages des CAD dans les cellules tumorales ciblées de façon sélective tout en minimisant les effets néfastes alimente davantage la croissance du marché

- En outre, l'augmentation du financement des secteurs privé et public pour la recherche et le développement d'ADC, parallèlement aux collaborations entre les entreprises biopharmaceutiques et les établissements universitaires, accélère l'innovation dans les technologies à charge utile élevée DAR

- La prévalence croissante des cancers difficiles à traiter et le besoin de traitements personnalisés continuent de stimuler l'investissement dans les plateformes de DCA, en mettant l'accent sur l'optimisation des fenêtres thérapeutiques et des résultats pour les patients

Restriction/Défi

(en milliers de dollars)Coûts de développement élevés, obstacles réglementaires et préoccupations en matière de sécurité(en milliers de dollars)

- Le coût relativement élevé du développement de thérapies ADC à haute DAR, y compris la chimie de conjugaison complexe, un contrôle rigoureux de la qualité et des essais cliniques coûteux, constitue un obstacle important à l'expansion du marché.

- Par exemple, les ADC de conjugaison propres à un site de fabrication nécessitent des installations spécialisées et du personnel hautement qualifié, ce qui accroît les investissements initiaux pour les petites et moyennes entreprises de biotechnologie. Cela peut retarder l'entrée sur le marché des candidats innovants

- Les défis réglementaires, y compris les exigences strictes des organismes comme la FDA et l'EMA en matière de sécurité, de stabilité et d'efficacité, peuvent ralentir les délais d'approbation et augmenter les coûts de développement

- Les préoccupations concernant la toxicité et l'immunogénicité potentielles non ciblées des CAA à haut DAR peuvent limiter l'adoption généralisée jusqu'à ce que les données cliniques sur l'innocuité à long terme soient disponibles.

- Il sera essentiel de relever ces défis grâce à des procédés de fabrication optimisés, à une solide validation préclinique et à des collaborations stratégiques avec des experts en réglementation pour soutenir la croissance sur le marché de l'ADC à haute DAR

Haut rapport drogue-anticorps ADC Thérapies Portée du marché

Le marché est segmenté selon le type de charge utile, l'indication et l'étape de développement.

• Par type de charge utile

Sur la base du type de charge utile, le marché des thérapies ADC à fort rapport drogue-anticorps est segmenté en inhibiteurs de la topoisomérase, inhibiteurs de la microtubule, agents de dégradation de l'ADN et autres. Le segment des inhibiteurs de la topoisomérase a dominé la plus grande part du marché de 41,5 % en 2025, en raison de leur efficacité avérée dans le traitement ciblé du cancer et de la réduction de la toxicité non ciblée. Ces inhibiteurs sont largement adoptés dans le cancer du sein et les tumeurs hématologiques en raison de leur capacité à induire des dommages à l'ADN sélectivement dans les cellules tumorales qui se divisent rapidement. Les entreprises pharmaceutiques préfèrent les charges utiles basées sur la topoisomérase pour leur pharmacocinétique prévisible et leurs profils de sécurité établis. La compatibilité de ces charges utiles avec des rapports médicament-anticorps élevés permet d'obtenir des résultats thérapeutiques puissants tout en minimisant les effets secondaires systémiques. L'augmentation du succès clinique et des approbations réglementaires des ADC de Topoisomerase renforce encore la domination du marché. L'adoption est particulièrement élevée en Amérique du Nord et en Europe, où les pipelines d'oncologie sont matures et où il existe une infrastructure biologique avancée.

Le segment des agents digérants de l'ADN devrait être témoin du TCAC le plus rapide de 22,1 % entre 2026 et 2033, alimenté par des essais cliniques en cours ciblant des cancers difficiles à traiter tels que les tumeurs pulmonaires et colorectales. Les ADC qui portent atteinte à l'ADN offrent un indice thérapeutique élevé et peuvent être adaptés aux combinaisons thérapeutiques, ce qui augmente leur attractivité clinique. La croissance s'accélère en élargissant la recherche sur les nouvelles technologies de liaison et d'anticorps qui améliorent l'efficacité de la livraison de la charge utile. Les marchés émergents adoptent de plus en plus l'ADN Damaging ADC en raison de leur potentiel en oncologie de précision et en médecine personnalisée.

• Par indication

Sur la base de l'indication, le marché est segmenté en cancer du sein, malignités hématologiques, cancer du poumon, cancer colorectal, et autres. Les thérapies contre le cancer du sein représentaient la plus grande part des revenus en 2025, soit 38,7 %, en raison des taux d'incidence élevés à l'échelle mondiale et de l'adoption de CAD dans les traitements du cancer du sein HER2 positifs et triplement négatifs. Les protocoles cliniques établis, ainsi que les politiques de remboursement favorables sur les principaux marchés, contribuent à la domination. Les intervenants pharmaceutiques de premier plan continuent de se concentrer sur le cancer du sein en raison de résultats d'essais cliniques solides, d'une sensibilisation accrue des patients et de l'adoption dans les systèmes de santé tant privés que publics.

Le segment des malignités hématologiques devrait enregistrer le TCAC le plus rapide de 21,5 % entre 2026 et 2033, en raison de la prévalence croissante des leucémies, des lymphomes et du myélome multiple. Les ADC ciblant les cancers hématologiques bénéficient d'un taux de réponse plus élevé et d'une toxicité systémique réduite, ce qui favorise l'accélération des pipelines de développement. Les études cliniques continuent d'étendre les indications aux populations de patients rechutés et réfractaires. Les produits biologiques émergents et l'intégration de nouvelles charges utiles comme les agents d'analyse de l'ADN et les inhibiteurs de la topoisomérase accélèrent davantage la croissance dans ce segment.

• Par étape de développement

Sur la base du stade de développement, le marché est segmenté en essais précliniques, cliniques et produits commercialisés. Le segment des produits commercialisés a dominé le marché avec une part des revenus de 44,3 % en 2025, en raison de la présence d'ADC approuvés par la FDA et de leur adoption clinique généralisée. Ces produits fournissent des données validées sur l'innocuité et l'efficacité, ce qui en fait des choix privilégiés pour les oncologues et les établissements de santé. Les produits commerciaux établis bénéficient également de la reconnaissance de la marque, de la couverture d'assurance et de solides réseaux de distribution.

Le segment des essais cliniques devrait connaître le TCAC le plus rapide de 23,4 %, de 2026 à 2033, alors que les compagnies pharmaceutiques étendront de façon dynamique les pipelines de CDA en ciblant les besoins en oncologie non satisfaits. L'innovation dans la technologie des liens, l'augmentation des ratios médicaments-anticorps et les nouvelles charges utiles alimentent le développement clinique rapide. L'essor du financement mondial de la recherche en oncologie, les incitatifs réglementaires pour les thérapies révolutionnaires et les collaborations entre les start-up en biotechnologie et les grands médicaments stimulent la croissance. Les marchés émergents participent également de plus en plus aux essais cliniques, élargissant l'accès des patients et accélérant l'adoption mondiale des CAA de prochaine génération.

Haut rapport drogue-anticorps ADC Analyse régionale du marché des thérapies

- L'Amérique du Nord a dominé le marché des thérapies ADC à fort rapport médicaments-anticorps avec la plus grande part de revenus d'environ 39,5 % en 2025, appuyée par une infrastructure d'oncologie avancée, un investissement élevé en R-D, de solides cadres réglementaires et la présence de grands développeurs ADC et de startups en biotechnologie aux États-Unis.

- De plus, les partenariats stratégiques entre les entreprises pharmaceutiques et les centres universitaires de lutte contre le cancer stimulent le développement et la commercialisation de nouvelles thérapies ADC

- L'adoption généralisée est également soutenue par des dépenses de santé élevées, la disponibilité de centres d'oncologie spécialisés et des politiques de remboursement favorables, établissant l'Amérique du Nord comme le premier marché pour les thérapies ADC à haut DAR

États-Unis Haut rapport drogue-anticorps ADC Thérapies Aperçu du marché

Le marché américain des thérapies ADC à fort rapport médicaments-anticorps a enregistré la plus grande part de revenus en Amérique du Nord en 2025, alimentée par de vastes activités d'essais cliniques, une collaboration solide entre les instituts de recherche biopharmaceutiques et universitaires et une forte sensibilisation des patients aux thérapies ciblées. Par exemple, l'approbation par la FDA de la fam-trastuzumab deruxtecan pour le cancer du sein HER2-positif et les essais en cours de Geptuzumab ozogamicine pour la leucémie myéloïde aiguë mettent en évidence l'adoption rapide par la région d'ADC innovants. Le fort pipeline de R-D et l'infrastructure d'oncologie établie continuent de propulser le marché américain.

Rapport entre les drogues et les anticorps ADC Thérapies Aperçu du marché

Le marché européen des thérapies ADC à fort rapport médicaments-anticorps devrait s'étendre à un TCAC important au cours de la période de prévision, en raison de l'augmentation de la prévalence du cancer, de l'augmentation du soutien gouvernemental à la recherche en oncologie et de normes réglementaires rigoureuses pour les produits biologiques. Par exemple, en 2023, Roche et AstraZeneca ont lancé des programmes cliniques de haute DAR ADC dans plusieurs centres d'oncologie européens, visant à répondre aux besoins thérapeutiques non satisfaits dans les cancers du sein et du poumon. L'accent mis sur la médecine de précision et l'adoption croissante de thérapies ciblées devrait stimuler davantage la croissance du marché.

U.K. Rapport élevé entre les médicaments et les anticorps Thérapies ADC Aperçu du marché

On s'attend à ce que le marché des thérapies ADC au Royaume-Uni soit en croissance à un TCAC remarquable au cours de la période de prévision, en raison de l'expansion de l'infrastructure de traitement du cancer, de l'augmentation de la participation aux essais cliniques et de l'augmentation des dépenses en soins de santé pour les produits biologiques novateurs. Par exemple, la collaboration entre les hôpitaux basés au Royaume-Uni et les développeurs mondiaux d'ADC soutient les essais de nouveaux candidats à l'ADC à haute DAR ciblant les tumeurs hématologiques, améliorant l'accessibilité et accélérant l'adoption.

Allemagne Haut rapport drogue-anticorps ADC Thérapies Aperçu du marché

Au cours de la période de prévision, le marché allemand des thérapies ADC devrait se développer à un taux élevé de TCAC, alimenté par le pays et axé sur l'innovation en biotechnologie, les établissements de soins de santé de pointe et les incitations réglementaires à la recherche clinique. Par exemple, BioNTech et d'autres entreprises de biotechnologie allemandes investissent dans des plateformes de développement ADC pour améliorer la livraison de charge utile ciblée, reflétant une tendance croissante vers l'oncologie de précision.

Asie-Pacifique Haut rapport drogue-anticorps ADC Thérapies Aperçu du marché

Le marché des thérapies ADC à fort rapport médicaments-anticorps en Asie et dans le Pacifique est sur le point de croître au rythme le plus rapide au cours de la période de prévision, en raison de l'augmentation de l'incidence du cancer, de l'amélioration de l'infrastructure des soins de santé, de l'expansion des essais cliniques et de l'adoption croissante de thérapies ciblées dans des pays comme la Chine, le Japon et l'Inde. Par exemple, en Chine, l'approbation réglementaire de plusieurs candidats à l'ADC et l'expansion des centres d'oncologie dans les villes de niveau 1 facilitent l'accès des patients. En Inde, les collaborations entre les entreprises de biotechnologie nationales et les développeurs mondiaux d'ADC permettent la production locale et les études cliniques. De même, l'investissement du Japon dans la recherche en oncologie de haute technologie et l'adoption de thérapies novatrices pour les cancers du sein, du poumon et de l'hématologie stimulent la croissance du marché dans toute la région.

Japon Haut rapport drogue-anticorps ADC Thérapies Aperçu du marché

Le marché japonais des thérapies ADC à fort rapport médicaments-anticorps prend de l'ampleur en raison de l'infrastructure de soins de santé avancée, de l'adoption précoce de thérapies oncologiques novatrices et de la sensibilisation accrue au cancer. Par exemple, la participation du Japon aux essais cliniques ADC à haut niveau DAR à l'échelle mondiale et la disponibilité de subventions de recherche subventionnées par le gouvernement accélèrent la mise au point et l'adoption de nouvelles thérapies ADC.

Chine Haut rapport drogue-anticorps ADC Thérapies Aperçu du marché

En 2025, le marché chinois des thérapies ADC a représenté la plus grande part des revenus du marché en Asie-Pacifique, attribuable à l'augmentation de la prévalence du cancer, à l'expansion des réseaux hospitaliers et à l'augmentation de la population de la classe moyenne à la recherche de thérapies anticancéreuses de pointe. Par exemple, les développeurs d'ADC basés à Shanghai ont lancé plusieurs candidats d'ADC à haut DAR dans des essais cliniques de phase II et III, démontrant ainsi l'adoption rapide par la région de traitements d'oncologie de pointe. Les initiatives gouvernementales appuyant la fabrication de produits biologiques et la recherche clinique propulsent le marché.

Haut rapport drogue-anticorps ADC Part de marché des thérapies

L'industrie des thérapies ADC à haut rapport drogue-anticorps est principalement dirigée par des entreprises bien établies, notamment :

- Pfizer Inc. (États-Unis)

- Roche Holding AG (Suisse)

- AbbVie Inc. (États-Unis)

- Amgen Inc. (États-Unis)

- Astellas Pharma Inc. (Japon)

- Daiichi Sankyo Company, Limited (Japon)

- Mersana Therapeutics, Inc. (États-Unis)

- Synaffix BV (Pays-Bas)

- Genmab A/S (Danemark)

- Innovent Biologics, Inc. (Chine)

- Wuxi Biologics (Chine)

- IGM Biosciences, Inc. (États-Unis)

- RemeGen Co., Ltd. (Chine)

Les derniers développements du marché mondial des thérapies ADC à haut rapport drogue-anticorps

- En janvier 2025, la Food and Drug Administration des États-Unis a approuvé Datopotamab Deruxtecan‐dlnk (Datroway), un conjugué d'anticorps dirigés par Trop‐2 développé par Daiichi Sankyo et AstraZeneca pour les adultes atteints d'un cancer du sein non résécable ou métastatique, HER2‐négatif, offrant une nouvelle option de traitement ADC ciblé pour les patients ayant reçu un traitement préalable endocrinien et une chimiothérapie

- En avril 2025, Datopotabab Deruxtecan (Datroway) a reçu une autorisation de mise sur le marché dans l'Union européenne, ce qui élargit encore l'accès à ce traitement ADC pour les patients atteints d'un cancer du sein non résécable ou métastatique, HER2-négatif

- En juin 2025, la FDA des États-Unis a approuvé Datroway pour le traitement du cancer du poumon non à petites cellules de l'EGFR, marquant la première approbation de ce traitement ADC dans une indication du cancer du poumon et élargissant son impact clinique au-delà du cancer du sein

- En juin 2025, la Food and Drug Administration des États-Unis a approuvé Datroway pour le cancer du poumon non à petites cellules avancé, offrant une option ciblée pour les patients atteints de tumeurs mutées EGFR résistantes à d'autres thérapies et soulignant l'utilité clinique croissante des CAD dans plusieurs types de cancer

- En octobre 2025, AstraZeneca et Daiichi Sankyo ont signalé que Datroway avait amélioré de façon significative la survie globale des patients atteints d'un cancer du sein triplement négatif au cours d'un essai clinique à la fin de l'étude, en soulignant le bénéfice thérapeutique potentiel et la progression clinique des thérapies ADC à haut potentiel.

- En novembre 2025, les biopharmaceutiques du premier jour ont accepté d'acquérir le portefeuille d'oncologie de Mersana Therapeutics pour un montant maximal de 285 millions de dollars, ce qui a amené Mersanas à diriger l'actif d'ADC Emi‐Le (cible B7‐H4) dans le portefeuille d'oncologie du premier jour et a révélé une forte confiance des investisseurs dans le potentiel des thérapies avancées d'ADC

- En mai 2025, Radiance Biopharma a conclu une entente de licence exclusive pour un ADC ciblé ROR-1, élargissant les collaborations de développement dans l'espace ADC et soutenant l'innovation dans les conjuguants de nouvelle génération

- En juin 2025, SunRock Biopharma et Escugen ont annoncé un partenariat en vue de développer SRB123, un ADC de première classe ciblé par le CCR9 destiné à traiter de multiples tumeurs solides, démontrant une collaboration et une diversification croissantes dans les pipelines de développement des ADC

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.