Global Systemic Lupus Erythematosus Treatment Market

Taille du marché en milliards USD

TCAC :

%

USD

949.20 Million

USD

1,699.18 Million

2025

2033

USD

949.20 Million

USD

1,699.18 Million

2025

2033

| 2026 –2033 | |

| USD 949.20 Million | |

| USD 1,699.18 Million | |

| % | |

|

Segmentation du marché mondial du lupus érythémateux systémique par type de traitement (antipaludéens, anti-inflammatoires non stéroïdiens, cytotoxiques et immunosuppresseurs, traitements de fond antirhumatismaux, anticorps monoclonaux, anticoagulants, produits biologiques et autres), diagnostic (analyses sanguines, analyse d'urine et radiographie pulmonaire), forme pharmaceutique (comprimés, gélules, injections et autres), voie d'administration (orale, intraveineuse et sous-cutanée), symptômes (douleurs thoraciques, fatigue, adénopathies, fièvre, malaise général, anxiété, chute de cheveux, perte de poids, aphtes, photosensibilité, éruptions cutanées et autres), utilisateurs finaux (cliniques, hôpitaux et autres), circuit de distribution (pharmacies hospitalières, pharmacies de détail et pharmacies en ligne) - Tendances et prévisions du secteur 2033

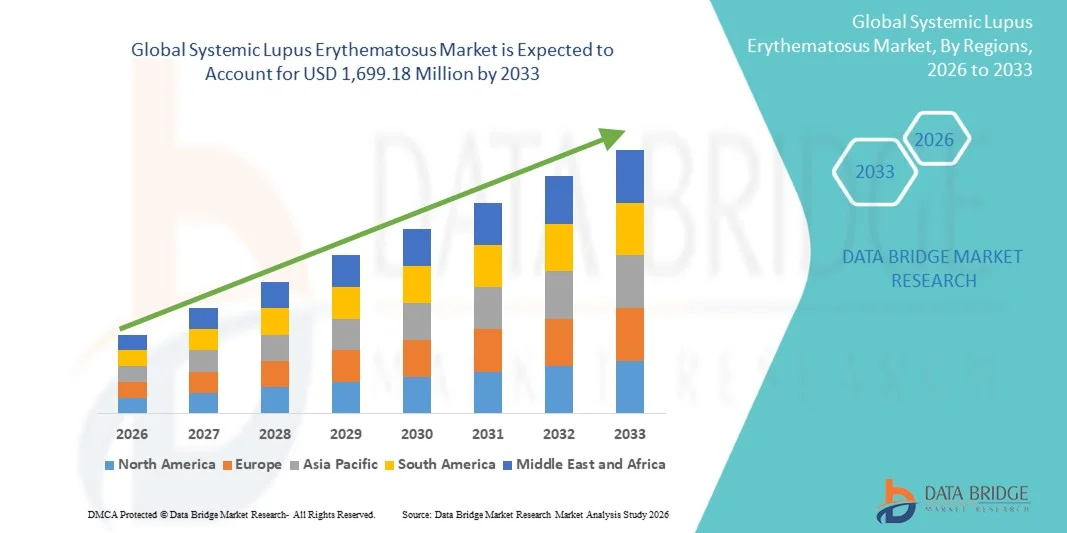

Taille du marché du lupus érythémateux systémique

- Le marché mondial du lupus érythémateux systémique était évalué à 949,20 millions de dollars américains en 2025 et devrait atteindre 1 699,18 millions de dollars américains d’ici 2033 , avec un TCAC de 7,55 % au cours de la période de prévision.

- La croissance du marché est largement alimentée par une sensibilisation accrue, un diagnostic précoce et les progrès des thérapies ciblées et des produits biologiques, ce qui permet une meilleure prise en charge de la maladie et de meilleurs résultats pour les patients.

- De plus, la prévalence croissante des maladies auto-immunes, associée à une demande accrue des patients pour des traitements efficaces et personnalisés, positionne les nouvelles thérapies comme le choix privilégié en pratique clinique. Ces facteurs convergents accélèrent l'adoption des traitements du lupus érythémateux systémique, stimulant ainsi significativement la croissance du secteur.

Analyse du marché du lupus érythémateux systémique

- Les traitements du lupus érythémateux systémique, comprenant les biothérapies, les immunosuppresseurs et les corticostéroïdes, sont des composantes de plus en plus essentielles de la prise en charge des maladies auto-immunes, tant en milieu clinique qu'hospitalier, en raison de leur capacité à contrôler l'inflammation, à prévenir les lésions organiques et à améliorer la qualité de vie des patients.

- La demande croissante de traitements contre le lupus érythémateux systémique est principalement alimentée par la prévalence accrue de la maladie, une sensibilisation grandissante des patients et des professionnels de santé, et une préférence accrue pour des options thérapeutiques ciblées et personnalisées offrant une meilleure efficacité et moins d'effets secondaires.

- L'Amérique du Nord a dominé le marché du lupus érythémateux systémique avec la plus grande part de revenus (39,8 %) en 2025, caractérisée par une infrastructure de soins de santé avancée, des dépenses de santé élevées, une adoption précoce des produits biologiques et une forte présence d'acteurs pharmaceutiques clés. Les États-Unis ont connu une croissance substantielle de l'utilisation des traitements, en particulier dans les cas nouvellement diagnostiqués et réfractaires, grâce aux innovations des entreprises pharmaceutiques établies et des jeunes entreprises de biotechnologie axées sur les anticorps monoclonaux et les immunothérapies ciblées.

- La région Asie-Pacifique devrait connaître la croissance la plus rapide sur le marché du lupus érythémateux systémique au cours de la période de prévision, en raison d'une sensibilisation accrue à la maladie, d'un accès élargi aux soins de santé et de l'augmentation des revenus disponibles permettant un meilleur accès aux traitements.

- Le segment des produits biologiques a dominé le marché du lupus érythémateux systémique avec une part de marché de 41,8 % en 2025, grâce à leur grande efficacité, leur spécificité et leur utilisation croissante en première ou deuxième intention dans les cas modérés à sévères.

Portée du rapport et segmentation du marché du lupus érythémateux systémique

|

Attributs |

Principaux enseignements du marché du lupus érythémateux systémique |

|

Segments couverts |

|

|

Pays couverts |

Amérique du Nord

Europe

Asie-Pacifique

Moyen-Orient et Afrique

Amérique du Sud

|

|

Acteurs clés du marché |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Systemic Lupus Erythematosus Market Trends

“Advancements Through Biologics and Targeted Therapies”

- A significant and accelerating trend in the global systemic lupus erythematosus market is the growing adoption of biologics and targeted therapies, which are improving disease management and reducing flares compared to conventional treatments

- For instance, belimumab and anifrolumab are increasingly prescribed to moderate-to-severe SLE patients, offering improved efficacy and safety profiles over traditional immunosuppressants

- Targeted therapies enable personalized treatment approaches by modulating specific immune pathways, reducing systemic side effects, and improving patient adherence. For instance, some emerging monoclonal antibodies focus on B-cell modulation to minimize organ damage and disease progression

- The integration of novel therapies with patient monitoring systems allows clinicians to track disease activity, medication response, and flare prediction, enhancing clinical decision-making and patient outcomes

- This trend towards more effective, tailored, and patient-centric therapies is fundamentally reshaping treatment expectations in SLE management. Consequently, pharmaceutical companies are developing next-generation biologics and combination therapies with improved safety, efficacy, and administration convenience

- The demand for innovative systemic lupus erythematosus therapies is growing rapidly across both developed and emerging markets, as patients and healthcare providers increasingly prioritize efficacy, safety, and personalized care

- Collaboration between pharmaceutical companies and research institutions is fostering the development of novel biomarkers and companion diagnostics, supporting more precise and individualized therapy selection

Systemic Lupus Erythematosus Market Dynamics

Driver

“Increasing Prevalence and Awareness of Autoimmune Disorders”

- The rising prevalence of systemic lupus erythematosus worldwide, coupled with growing awareness among healthcare providers and patients, is a significant driver for the heightened demand for advanced therapies

- For instance, in March 2025, GlaxoSmithKline announced initiatives to expand belimumab access programs targeting newly diagnosed and high-risk SLE patients in North America and Europe. Such strategies by key companies are expected to drive systemic lupus erythematosus market growth in the forecast period

- As more patients receive early diagnosis and timely treatment, therapies that reduce flares, prevent organ damage, and improve quality of life are increasingly preferred, boosting adoption

- Furthermore, rising investments in research and development of novel therapies, along with patient education programs, are making systemic lupus erythematosus treatment more effective and accessible

- The availability of patient support programs, reimbursement coverage, and telemedicine consultations further facilitates the adoption of advanced therapies, contributing to sustained market growth

- Increasing collaborations between pharmaceutical companies, healthcare providers, and patient advocacy groups are enhancing awareness campaigns and improving early diagnosis rates

- Expansion of healthcare infrastructure in emerging regions is enabling better access to systemic lupus erythematosus therapies, driving adoption in previously underserved markets

Restraint/Challenge

“High Treatment Costs and Regulatory Hurdles”

- Concerns surrounding the high cost of biologics and targeted therapies pose a significant challenge to broader market penetration, particularly in price-sensitive and emerging regions. As these therapies often require long-term administration, affordability remains a barrier for many patients

- For instance, high out-of-pocket expenses for monoclonal antibody treatments have limited access in regions with low healthcare coverage, making some patients rely on conventional immunosuppressants instead

- Regulatory hurdles and long approval timelines for novel therapies also slow market expansion, as companies must demonstrate rigorous safety and efficacy to secure global approvals. For instance, regulatory authorities in Asia-Pacific often require extensive local clinical data before approving biologics

- While biosimilars are gradually becoming available and reducing costs, the perception of higher prices for innovative therapies can still hinder adoption, especially among newly diagnosed or mild cases

- Overcoming these challenges through patient assistance programs, biosimilar adoption, and streamlined regulatory processes will be vital for sustained growth in the systemic lupus erythematosus market

- Limited awareness and education among patients in certain regions regarding advanced therapies can delay treatment initiation, reducing overall market uptake

- Variability in reimbursement policies and healthcare coverage across regions may restrict access to high-cost therapies, posing a continuous challenge to market expansion

Systemic Lupus Erythematosus Market Scope

The market is segmented on the basis of treatment type, diagnosis, dosage form, route of administration, symptoms, end-users, and distribution channel.

- By Treatment Type

On the basis of treatment type, the systemic lupus erythematosus market is segmented into antimalarial drugs, NSAIDs, cytotoxic and immunosuppressive drugs, DMARDs, monoclonal antibodies, anticoagulants, biologics, and others. The biologics segment dominated the market with the largest revenue share of 41.8% in 2025, driven by their high efficacy in controlling moderate-to-severe SLE symptoms and preventing organ damage. Biologics such as belimumab and anifrolumab are increasingly preferred for targeted immune modulation with reduced systemic toxicity. Strong adoption in developed regions and high patient awareness further support market dominance. Insurance coverage and reimbursement policies facilitate accessibility, reinforcing market share. The integration of biologics with digital patient monitoring systems also improves adherence and long-term outcomes. Ongoing clinical trials and new approvals for biologics continue to expand their patient base globally.

The monoclonal antibodies segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing R&D activities and clinical acceptance. These therapies target specific immune pathways, offering improved efficacy for refractory or severe SLE cases. Personalized medicine and favorable reimbursement strategies are accelerating adoption. Monoclonal antibodies also reduce side effects compared to conventional immunosuppressants, improving patient adherence. The growth is fueled by rising patient awareness and expanding access in emerging markets. Biopharmaceutical companies are actively developing next-generation antibodies with better safety and administration convenience.

- By Diagnosis

On the basis of diagnosis, the market is segmented into blood tests, urinalysis, and chest X-ray. The blood tests segment dominated the market with the largest revenue share in 2025, as these tests are essential for detecting autoantibodies and monitoring disease activity. Blood tests such as ANA, anti-dsDNA, and complement levels guide therapy selection and early flare detection. Blood testing is minimally invasive, cost-effective, and widely adopted in hospitals and specialized clinics. Advanced multiplex testing enhances diagnostic accuracy and improves treatment planning. High adoption is observed in North America and Europe due to established healthcare infrastructure. Continuous innovations in biomarker testing further reinforce dominance.

The urinalysis segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising prevalence of lupus nephritis. Early detection of kidney involvement is critical to prevent permanent damage and adjust immunosuppressive therapy. Technological advancements such as automated urinalysis and point-of-care devices are accelerating adoption. Growing awareness of renal complications among patients and clinicians supports market growth. Urinalysis is increasingly integrated into routine monitoring protocols, especially in emerging regions.

- By Dosage Form

On the basis of dosage form, the market is segmented into tablet, capsule, injection, and others. The injection segment dominated the market in 2025, primarily due to the growing use of biologics and monoclonal antibodies requiring parenteral administration. Injectable therapies provide precise dosing, improved bioavailability, and rapid therapeutic effect, especially in severe or refractory SLE. Hospitals and specialty clinics ensure safe administration and monitoring of infusion reactions. Patient-friendly devices such as auto-injectors enhance adherence and convenience. Strong physician preference for injectable therapies in hospital settings reinforces market leadership. The segment also benefits from new formulations that reduce injection frequency.

The tablet segment is expected to witness the fastest growth rate from 2026 to 2033, driven by continued demand for oral antimalarial, NSAID, and DMARD therapies. Oral forms offer convenience, ease of self-administration, and long-term adherence for mild-to-moderate SLE. Tablets are cost-effective and widely accessible, especially in outpatient and clinic settings. Growth is supported by increasing awareness and patient preference for non-invasive therapies. Pharmaceutical companies continue to innovate combination oral formulations for better efficacy. Expansion in emerging markets also supports faster growth for oral dosage forms.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, intravenous (IV), and subcutaneous. The intravenous segment dominated the market with the largest revenue share in 2025 due to the administration of biologics and monoclonal antibodies in controlled hospital settings. IV therapy ensures precise dosing, predictable pharmacokinetics, and close monitoring of adverse effects. It is particularly preferred for severe or organ-threatening SLE cases. Hospitals and specialized clinics provide the necessary infrastructure for safe IV administration. IV therapy also supports integration with treatment protocols and monitoring systems. The high adoption in North America and Europe further reinforces dominance.

The subcutaneous segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the availability of self-administered biologics and monoclonal antibodies. Subcutaneous therapy allows home administration, reducing hospital visits and improving convenience. This route enhances patient adherence and satisfaction. Growing awareness about at-home care and telemedicine support contributes to rapid adoption. Pharmaceutical companies are developing auto-injectors and prefilled pens for safer subcutaneous delivery. Expansion in emerging markets with limited hospital access also supports subcutaneous growth.

- By Symptoms

On the basis of symptoms, the market is segmented into chest pain, fatigue, swollen lymph nodes, fever, general discomfort, uneasiness, hair loss, weight loss, mouth sores, sensitivity to sunlight, skin rash, and others. The fatigue segment dominated the market in 2025, as fatigue is one of the most common and persistent symptoms affecting quality of life. Fatigue drives patient demand for effective therapies to manage inflammation and autoimmune activity. Clinicians prioritize treatments that reduce fatigue along with other SLE manifestations. Awareness programs and patient support initiatives emphasize fatigue management. High adoption is observed in developed regions with better access to advanced therapies. Fatigue-focused treatment strategies continue to grow with new therapy launches.

The skin rash segment is expected to witness the fastest growth rate from 2026 to 2033 due to the increasing prevalence of cutaneous lupus manifestations. Early treatment of skin symptoms is critical to prevent disease progression and improve patient confidence. Topical and systemic therapies targeting skin involvement are gaining rapid adoption. Rising awareness among patients and dermatologists accelerates demand. Technological innovations in dermatology diagnostics enhance early identification and treatment of cutaneous lupus. Emerging markets with increasing SLE awareness also contribute to faster growth.

- By End-Users

On the basis of end-users, the market is segmented into clinics, hospitals, and others. The hospital segment dominated the market with the largest revenue share in 2025 due to the administration of complex therapies such as biologics, monoclonal antibodies, and IV treatments. Hospitals offer comprehensive facilities, patient monitoring, and management of severe SLE cases. High adoption is observed in tertiary care centers and specialized autoimmune clinics. Hospitals also provide controlled storage, dosing, and administration for expensive therapies. The segment benefits from strong infrastructure and trained staff. Integration with digital patient monitoring systems further supports dominance.

The clinics segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing outpatient diagnosis, early intervention, and availability of oral and subcutaneous therapies. Clinics are expanding their capacity for comprehensive SLE care, particularly in urban and semi-urban regions. Convenient access, lower costs, and reduced hospital dependence accelerate clinic adoption. Telemedicine and remote patient monitoring further enhance clinic-based therapy. Patient education programs and community outreach strengthen growth in clinic settings. Emerging regions with limited hospital access see faster uptake in clinics.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with the largest revenue share in 2025, as high-cost biologics and monoclonal antibodies are typically dispensed directly under clinical supervision. Hospitals ensure proper storage, dosing accuracy, and patient monitoring, which is critical for advanced therapies. Strong integration with treatment protocols supports hospital pharmacy dominance. Adoption is highest in developed regions with established healthcare infrastructure. Hospitals provide patient counseling and adherence support for complex treatments. Partnerships between pharma companies and hospital pharmacies further reinforce market share.

The online pharmacy segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing digitalization, e-commerce penetration, and patient preference for home delivery of oral and subcutaneous therapies. Online platforms enhance accessibility in remote and underserved regions. Convenience, subscription models, and teleconsultation support contribute to rapid adoption. Growing awareness of online pharmacy reliability and safety is accelerating uptake. Integration with digital health records and home monitoring devices boosts patient adherence. Emerging markets with high internet penetration are key contributors to online pharmacy growth.

Systemic Lupus Erythematosus Market Regional Analysis

- North America dominated the systemic lupus erythematosus market with the largest revenue share of 39.8% in 2025, characterized by advanced healthcare infrastructure, high healthcare expenditure, early adoption of biologics, and a strong presence of key pharmaceutical players

- Patients and healthcare providers in the region highly value the efficacy, safety, and personalized treatment options offered by modern SLE therapies, along with the availability of comprehensive monitoring and support programs

- This widespread adoption is further supported by well-established healthcare infrastructure, high healthcare expenditure, strong insurance coverage, and significant investment in research and development, establishing North America as the leading market for systemic lupus erythematosus treatment

U.S. Systemic Lupus Erythematosus Market Insight

The U.S. systemic lupus erythematosus market captured the largest revenue share in 2025 within North America, fueled by early diagnosis, high awareness, and widespread adoption of advanced therapies such as biologics and monoclonal antibodies. Patients and healthcare providers increasingly prioritize effective, targeted, and personalized treatment options to manage moderate-to-severe SLE and prevent organ damage. The growing availability of patient support programs, insurance coverage, and specialized autoimmune clinics further propels market growth. Moreover, the integration of digital health tools, telemedicine, and remote disease monitoring is enhancing treatment adherence and improving outcomes. Continuous R&D investment by key pharmaceutical companies is expanding therapy options and driving market expansion.

Europe Systemic Lupus Erythematosus Market Insight

The Europe systemic lupus erythematosus market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing awareness of autoimmune diseases and rising adoption of advanced therapies. Stringent healthcare standards and reimbursement policies support the uptake of biologics and monoclonal antibodies. The increase in urbanization, coupled with the rising prevalence of SLE, is fostering market growth. European patients also value improved quality of life through early intervention and effective disease management. The market is witnessing significant growth across hospitals and specialty clinics, with therapies being integrated into both established and new healthcare programs. Expansion in telemedicine and digital monitoring is further enhancing accessibility and adherence.

U.K. Systemic Lupus Erythematosus Market Insight

The U.K. systemic lupus erythematosus market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing disease awareness and demand for advanced treatment options. Rising concerns about long-term organ damage and chronic symptoms are encouraging patients and clinicians to adopt biologics and monoclonal antibodies. In addition, the U.K.’s strong healthcare infrastructure, widespread insurance coverage, and access to specialist clinics support market expansion. Digital patient monitoring, telehealth consultations, and home-based therapy options are contributing to convenience and adherence. Robust pharmaceutical R&D and clinical trial activity in the region are also driving therapy innovation.

Germany Systemic Lupus Erythematosus Market Insight

The Germany systemic lupus erythematosus market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of autoimmune diseases and the growing adoption of advanced therapies. Germany’s well-developed healthcare infrastructure, emphasis on clinical research, and patient-centric care promote the adoption of biologics and monoclonal antibodies. Hospitals and specialty clinics provide comprehensive monitoring for severe and refractory cases. The integration of digital tools for disease management is gaining traction. Growing patient awareness of early diagnosis and treatment benefits is boosting market penetration. Sustainability and precision medicine initiatives are further strengthening therapy adoption in the country.

Asia-Pacific Systemic Lupus Erythematosus Market Insight

The Asia-Pacific systemic lupus erythematosus market is poised to grow at the fastest CAGR during the forecast period, driven by rising disease awareness, expanding healthcare infrastructure, and increasing adoption of biologics and monoclonal antibodies. Countries such as China, Japan, and India are witnessing growth in specialized autoimmune clinics and hospital-based treatment programs. Government initiatives promoting digital health and patient monitoring support therapy uptake. The growing middle class and rising disposable incomes are improving access to advanced therapies. Increasing R&D collaborations and clinical trials in the region are accelerating the introduction of new therapies. Telemedicine and e-health platforms further enhance patient adherence and accessibility.

Japan Systemic Lupus Erythematosus Market Insight

The Japan systemic lupus erythematosus market is gaining momentum due to high disease awareness, advanced healthcare infrastructure, and patient preference for effective and convenient treatment options. Adoption of biologics and monoclonal antibodies is increasing, particularly in hospital and outpatient settings. The integration of telemedicine and remote patient monitoring supports adherence and long-term disease management. An aging population is driving demand for easy-to-use and safe therapies. Strong clinical research activity and government support for autoimmune disease management further accelerate growth. The emphasis on early diagnosis and targeted therapy adoption is shaping the market landscape.

India Systemic Lupus Erythematosus Market Insight

The India systemic lupus erythematosus market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to increasing awareness of autoimmune disorders, rapid urbanization, and improving healthcare access. Rising middle-class population and disposable incomes are enabling better access to advanced therapies such as biologics and monoclonal antibodies. Hospitals and specialty clinics are expanding SLE care services. The push towards digital health platforms and telemedicine facilitates patient monitoring and therapy adherence. Availability of affordable treatment options and domestic pharmaceutical development support market growth. Increasing initiatives for early diagnosis and disease management programs are further driving adoption across the country.

Systemic Lupus Erythematosus Market Share

The Systemic Lupus Erythematosus industry is primarily led by well-established companies, including:

- GSK plc (U.K.)

- AstraZeneca (U.K.)

- Pfizer Inc. (U.S.)

- F. Hoffmann‑La Roche Ltd (Switzerland)

- Bristol‑Myers Squibb Company (U.S.)

- Eli Lilly and Company (U.S.)

- Novartis AG (Switzerland)

- Merck & Co., Inc. (U.S.)

- Sanofi (France)

- AbbVie Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- UCB S.A. (Belgium)

- Amgen Inc. (U.S.)

- Biogen Inc. (U.S.)

- ImmuPharma PLC (U.K.)

- Horizon Therapeutics plc (Ireland)

- Anthera Pharmaceuticals, Inc. (U.S.)

- Xencor, Inc. (U.S.)

- RemeGen Co., Ltd. (China)

- I‑Mab Biopharma (China)

What are the Recent Developments in Global Systemic Lupus Erythematosus Market?

- In December 2025, researchers reported that telitacicept demonstrated promising results in a Phase 3 clinical trial for systemic lupus erythematosus, showing statistically significant reductions in disease activity compared with placebo and offering hope for a new biologic treatment that targets both BLyS and APRIL immune pathways a strategy that could expand effective therapy choices for SLE patients

- In October 2025, the U.S. Food and Drug Administration (FDA) approved Genentech’s Gazyva® (obinutuzumab) for the treatment of active lupus nephritis in adult patients, marking the first anti‑CD20 monoclonal antibody approved for this serious SLE complication and expanding treatment options for patients at risk of kidney damage

- In October 2025, results from a Phase 3 telitacicept study for systemic lupus erythematosus were published in The New England Journal of Medicine, showing statistically significant improvement in disease activity versus placebo and validating its dual BAFF/APRIL inhibitory mechanism as a promising SLE treatment strategy

- In March 2025, the FDA accepted Roche’s supplemental Biologics License Application (sBLA) for Gazyva/Gazyvaro® (obinutuzumab) for lupus nephritis, based on positive Phase III REGENCY results demonstrating improved renal outcomes, with regulatory decisions

- In April 2023, a Phase 1/2 clinical trial of CAR‑T cell therapy for people with moderate to severe or treatment‑resistant SLE was launched in China, representing a novel cell‑based immunotherapy approach aimed at refractory lupus patients

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.