Global White Oak Alternatives Market

Taille du marché en milliards USD

TCAC :

%

USD

363.62 Million

USD

850.14 Million

2025

2033

USD

363.62 Million

USD

850.14 Million

2025

2033

| 2026 –2033 | |

| USD 363.62 Million | |

| USD 850.14 Million | |

| % | |

|

Global White Oak Alternatives Market Segmentation, By Type (Oak Staves, Oak Chips, Oak Cubes, Oak Spiral, and Oak Powder), End User (Wine, Whiskey, Beer, and Other Alcoholic Beverages) - Industry Trends and Forecast to 2033

White Oak Alternatives Market Size

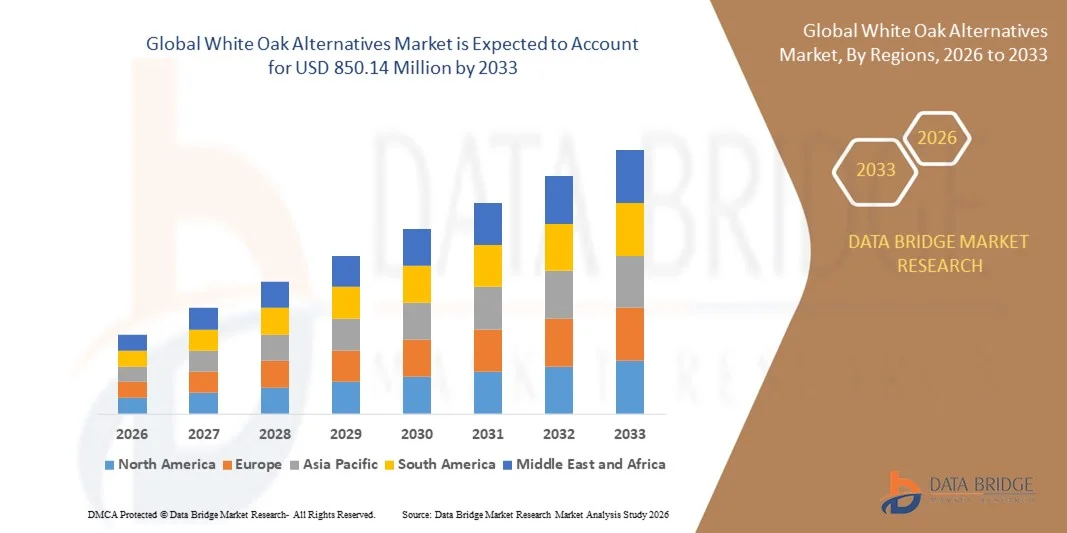

- The global white oak alternatives market size was valued at USD 363.62 million in 2025 and is expected to reach USD 850.14 million by 2033, at a CAGR of 11.2% during the forecast period

- The market growth is largely fueled by the increasing demand for premium wines, whiskeys, and craft beers, encouraging producers to adopt white oak alternatives such as chips, staves, cubes, spirals, and powder to achieve desired flavor profiles efficiently and cost-effectively

- Furthermore, rising consumer preference for unique, high-quality alcoholic beverages and the need for faster aging processes is driving wineries and distilleries to incorporate oak alternatives into production. These converging factors are accelerating the adoption of white oak products, thereby significantly boosting the industry's growth

White Oak Alternatives Market Analysis

- White oak alternatives, including chips, staves, cubes, spirals, and powder, are increasingly vital for beverage aging processes, allowing producers to impart oak-derived flavors, aromas, and tannins without relying solely on traditional barrels

- The escalating demand for white oak alternatives is primarily fueled by the growth of craft beverage industries, rising consumer focus on premium and consistent taste profiles, and the need for cost-efficient, flexible aging solutions in both commercial and small-scale production settings

- North America dominated the white oak alternatives market with a share of over 40% in 2025, due to the growing demand for premium wines, whiskeys, and craft beers, as well as increased adoption of cost-effective aging solutions such as oak chips and staves

- Asia-Pacific is expected to be the fastest growing region in the white oak alternatives market during the forecast period due to increasing urbanization, rising disposable incomes, and growing interest in premium alcoholic beverages in countries such as China, Japan, and India

- Oak chips segment dominated the market with a market share of 41.5% in 2025, due to their cost-effectiveness, ease of use, and versatility across different alcoholic beverages. Producers often prefer oak chips for their ability to deliver consistent flavor profiles and accelerated maturation compared to traditional barrels

Report Scope and White Oak Alternatives Market Segmentation

|

Attributes |

White Oak Alternatives Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

White Oak Alternatives Market Trends

Rising Adoption of Oak Alternatives in Craft and Premium Beverages

- A significant trend in the white oak alternatives market is the growing adoption of oak staves, chips, and spirals in craft spirits, wine, and premium beverage production, driven by the need for controlled maturation and distinctive flavor profiles. This trend is encouraging beverage producers to experiment with alternative oak products to achieve consistent results while managing costs

- For instance, Independent Stave Company provides sustainably sourced oak staves and spirals that are widely used by wineries and distilleries to replicate traditional barrel aging effects. These products allow beverage makers to tailor flavor extraction and aromatic profiles with precision

- The rising preference for smaller batch production in craft distilleries and boutique wineries is increasing the utilization of alternative oak solutions that provide flexibility in aging duration and intensity. Producers are leveraging these alternatives to innovate with limited resources and create signature flavor characteristics

- Premium spirit producers are incorporating white oak alternatives to maintain consistency in taste across seasonal batches and large-scale production runs. This approach ensures product uniformity without relying solely on expensive full-sized barrels

- The wine industry is increasingly adopting oak chips and inserts to enhance aging in stainless steel or neutral vessels, enabling faster maturation and richer flavor profiles. This strategy is shaping the market by offering scalable, cost-efficient aging solutions for wineries of varied sizes

- Sustainability considerations are further driving the use of white oak alternatives as producers seek to minimize waste and reduce reliance on newly harvested barrels. These alternatives support environmentally conscious production while maintaining the sensory qualities expected by consumers

White Oak Alternatives Market Dynamics

Driver

Increasing Demand for Cost-Effective and Controlled Aging Solutions

- The growing need for affordable and consistent aging methods in craft spirits and wine production is driving demand for white oak alternatives that replicate barrel aging effects. These alternatives offer precise flavor control, reduced capital investment, and faster maturation times compared with traditional barrel usage

- For instance, Seguin Moreau supplies toasted oak chips and micro-oxygenation staves that enable distilleries and wineries to achieve targeted flavor profiles efficiently. Their products allow producers to manage aging intensity while reducing storage and investment costs

- Small and medium-sized beverage producers are adopting these alternatives to enhance product consistency, reduce aging times, and optimize warehouse space. This is particularly relevant in markets where traditional barrels are scarce or expensive

- The flexibility of using oak alternatives enables beverage makers to experiment with flavor profiles, adjust tannin levels, and replicate vintage characteristics without altering production timelines. This versatility supports innovation and market differentiation

- The increasing demand for premium-quality beverages at competitive prices is further reinforcing this driver. Producers are strategically leveraging oak alternatives to balance cost, quality, and production efficiency

Restraint/Challenge

High Variability in Flavor Extraction Across Different Oak Products

- The white oak alternatives market faces challenges due to differences in flavor extraction rates, toast levels, and wood composition, which can result in inconsistent taste and aroma across batches. This variability makes standardizing product profiles more difficult, especially for larger-scale operations

- For instance, Independent Stave Company notes that differences in grain tightness and toast profiles can produce variations in flavor intensity even within the same oak source. Producers must carefully monitor usage to achieve desired results

- Achieving uniformity requires precise selection, preparation, and monitoring of oak alternatives, increasing labor and quality control requirements. This complexity can limit scalability for some beverage producers

- The reliance on suppliers for consistent quality and product specifications exposes manufacturers to supply-side risks. Variations in wood sourcing or processing methods may impact sensory outcomes and consumer acceptance

- Market growth continues to be constrained by these flavor variability concerns, as producers must balance the cost and flexibility benefits of oak alternatives with the need to maintain consistent and desirable beverage profiles

White Oak Alternatives Market Scope

The market is segmented on the basis of type and end-user.

- By Type

On the basis of type, the white oak alternatives market is segmented into oak staves, oak chips, oak cubes, oak spiral, and oak powder. The oak chips segment dominated the market with the largest revenue share of 41.5% in 2025, driven by their cost-effectiveness, ease of use, and versatility across different alcoholic beverages. Producers often prefer oak chips for their ability to deliver consistent flavor profiles and accelerated maturation compared to traditional barrels. The market also witnesses strong demand for oak chips due to their compatibility with various aging methods, including stainless steel tanks and smaller vessels, and the wide range of flavor intensities they can impart. Oak chips also allow for precise control over toasting levels, enhancing the sensory characteristics of beverages.

The oak staves segment is anticipated to witness the fastest growth rate of 19.8% from 2026 to 2033, fueled by increasing adoption in premium wine and whiskey production. Oak staves provide more surface contact than chips, allowing for a richer extraction of oak compounds while maintaining a natural maturation process. They are preferred by producers aiming to balance cost efficiency with the depth of flavor traditionally associated with barrels. The flexibility to customize stave sizes and toasting levels further supports their growing popularity in the market.

- By End User

On the basis of end user, the white oak alternatives market is segmented into wine, whiskey, beer, and other alcoholic beverages. The wine segment held the largest market revenue share in 2025, driven by the growing adoption of oak alternatives in both red and white wines to impart oak-derived flavors without relying solely on expensive barrels. Winemakers often choose oak alternatives to maintain flavor consistency and reduce aging time while meeting consumer preferences for smoother, aromatic wines. The market for wine applications also benefits from innovations in infusion techniques that allow controlled extraction of tannins and vanilla, caramel, or smoky notes, enhancing the overall sensory profile.

The whiskey segment is expected to witness the fastest CAGR from 2026 to 2033, driven by the rising demand for premium and craft whiskeys. For instance, companies such as Jim Beam and Buffalo Trace are increasingly using oak cubes and staves to accelerate maturation and develop signature flavor profiles. Oak alternatives in whiskey production offer flexibility, allowing distillers to experiment with different levels of toast and contact times to achieve unique taste experiences. The segment growth is also supported by smaller distilleries adopting cost-effective alternatives to traditional barrels without compromising quality.

White Oak Alternatives Market Regional Analysis

- North America dominated the white oak alternatives market with the largest revenue share of over 40% in 2025, driven by the growing demand for premium wines, whiskeys, and craft beers, as well as increased adoption of cost-effective aging solutions such as oak chips and staves

- Producers in the region highly value the ability of white oak alternatives to impart oak-derived flavors and aromas efficiently, while reducing dependency on traditional barrels and enabling more consistent maturation outcomes

- This widespread adoption is further supported by the presence of established wineries and distilleries, advanced production infrastructure, and a preference for innovation in beverage aging, establishing white oak alternatives as a favored solution across both large-scale and craft beverage producers

U.S. White Oak Alternatives Market Insight

The U.S. white oak alternatives market captured the largest revenue share in 2025 within North America, fueled by the rising popularity of craft spirits and boutique wines. Producers are increasingly adopting oak cubes and chips to achieve premium flavor profiles while optimizing production costs. The growing trend of experimentation in flavor development, combined with robust demand for consistent maturation results, further propels the market. Moreover, the integration of white oak alternatives in small-batch production and custom aging processes is significantly contributing to the market's expansion.

Europe White Oak Alternatives Market Insight

The Europe white oak alternatives market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the demand for high-quality wines and spirits, as well as innovative aging solutions. The presence of traditional wine regions, coupled with a growing focus on cost-effective production techniques, is fostering the adoption of oak chips, staves, and cubes. European producers are also drawn to the efficiency and flexibility that white oak alternatives offer, enabling them to meet consumer expectations for consistent taste and aroma. The market is witnessing growth across both commercial wineries and craft distilleries, with alternatives being incorporated into new production lines and renovation projects.

U.K. White Oak Alternatives Market Insight

The U.K. white oak alternatives market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the rising trend of craft beverages and premium alcohol products. In addition, consumer demand for distinctive flavor profiles and high-quality spirits is encouraging beverage producers to adopt oak-based alternatives. The U.K.’s strong presence of craft breweries, distilleries, and wineries, along with the increasing focus on innovation and experimentation, is expected to continue driving market growth.

Germany White Oak Alternatives Market Insight

The Germany white oak alternatives market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s well-established wine and spirits industry and the increasing focus on modern production techniques. Germany’s infrastructure and emphasis on technological innovation in beverage production promote the adoption of oak cubes, staves, and chips. Producers are leveraging alternatives to reduce aging time, achieve consistent flavor extraction, and meet rising consumer expectations for premium quality alcoholic beverages.

Asia-Pacific White Oak Alternatives Market Insight

The Asia-Pacific white oak alternatives market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by increasing urbanization, rising disposable incomes, and growing interest in premium alcoholic beverages in countries such as China, Japan, and India. The region's beverage producers are adopting oak alternatives to accelerate maturation and introduce nuanced flavors efficiently. Furthermore, the expansion of craft breweries, distilleries, and boutique wineries in APAC is boosting the accessibility and utilization of white oak alternatives across diverse beverage categories.

Japan White Oak Alternatives Market Insight

The Japan white oak alternatives market is gaining momentum due to the country’s appreciation for high-quality beverages and the growing popularity of craft whiskeys and wines. Japanese producers are increasingly using oak staves and cubes to deliver distinct flavor profiles while optimizing aging periods. The integration of white oak alternatives into production aligns with the demand for consistency and premium quality. Moreover, Japan’s aging population and high consumer focus on luxury beverages are expected to spur further adoption in both commercial and small-scale operations.

China White Oak Alternatives Market Insight

The China white oak alternatives market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to the country’s expanding middle class, rising consumption of premium wines and spirits, and increasing interest in craft beverages. Chinese producers are adopting oak chips, cubes, and staves to enhance flavor and reduce reliance on traditional barrels. The push towards innovative beverage production and the presence of domestic manufacturers supplying cost-effective oak alternatives are key factors propelling the market in China.

White Oak Alternatives Market Share

The white oak alternatives industry is primarily led by well-established companies, including:

- White Oak (U.S.)

- The Vintner Vault (U.S.)

- Rich Xiberta USA, Inc (U.S.)

- THE BARREL MILL (U.S.)

- Canadell (France)

- Sascha Rudnik (Germany)

- Seguin Moreau Napa Cooperage (France)

- Oak Solutions Group (U.S.)

- Oak Chips Inc (U.S.)

- AGROVIN (Spain)

Latest Developments in Global White Oak Alternatives Market

- In December 2025, Oak Chips Inc. introduced Boozy Boost Sticks, a micro‑oak stave product designed for single‑bottle aging that allows producers and enthusiasts to replicate barrel-aged flavors efficiently. This launch provides smaller wineries and distilleries with a cost-effective method to produce premium-quality wines and spirits without investing in full barrels, significantly increasing accessibility to oak flavor profiles. The introduction of these sticks also promotes experimentation with flavor intensity and maturation techniques, encouraging innovation and expanding the market for small-batch and artisanal beverage producers

- In 2025, Oak Solutions Group expanded its product line with the Next Generation Series of French and American oak chips, featuring advanced toasting and processing techniques to optimize flavor extraction and structure. This enhancement allows producers to achieve more consistent results while tailoring the aromatic and tannin profile to specific beverage types. By improving control over maturation outcomes, the launch strengthens the adoption of oak alternatives in both commercial-scale and boutique production, reinforcing their value as a flexible and efficient solution for aging

- In 2025, Seguin Moreau broadened its oak alternatives portfolio by upgrading its OenoChips, OenoBlock, and OenoStick product lines to offer precise and targeted flavor extraction. This development supports winemakers and distillers in creating complex and distinctive profiles without relying solely on traditional barrels, reducing both production costs and aging time. The expansion reflects a shift toward customizable oak solutions, which is driving market growth by meeting the increasing demand for high-quality, consistent sensory outcomes in alcoholic beverages

- In November 2024, Oak Solutions Group completed the acquisition of Innerstave, integrating its inventory, technology, and product expertise into its portfolio. This strategic move expanded the company’s global market reach and product offerings, providing a broader array of oak alternatives for beverage producers. The acquisition enables producers to access a wider variety of oak formats, toasting levels, and infusion techniques, supporting innovation in flavor development and accelerating adoption of oak alternatives across different beverage segments

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.