North America Pallet Packaging Products Market

Taille du marché en milliards USD

TCAC :

%

USD

4.49 Billion

USD

6.79 Billion

2025

2033

USD

4.49 Billion

USD

6.79 Billion

2025

2033

| 2026 –2033 | |

| USD 4.49 Billion | |

| USD 6.79 Billion | |

| % | |

|

Amérique du Nord Palettes Produits d'emballage Segmentation du marché, type de produit (films à étirer, films à hottes, euro-palettes, boîtes à palettes, calottes et bouchons à palettes, feuilles à glissement et feuilles à niveaux, enrouleurs à étirer, hottes à étirer et filets à palettes), type de machine (entièrement automatiques et semi-automatiques), type de fonction (enveloppage, encrassement, protection et calottement, et autres), application (aliments et boissons, vente au détail et commerce électronique, produits emballés par les consommateurs, produits pharmaceutiques, produits chimiques, agriculture et horticulture, fabrication industrielle, automobile, électronique et appareils et autres), utilisation finale (logistique et fournisseurs de 3PL, usines de fabrication, centres de distribution de détail, opérateurs de chaînes froides et autres), chaîne de distribution (directe et indirecte) - Tendances et prévisions de l'industrie jusqu'en 2033

Amérique du Nord Palettes Emballage Produits Taille du marché

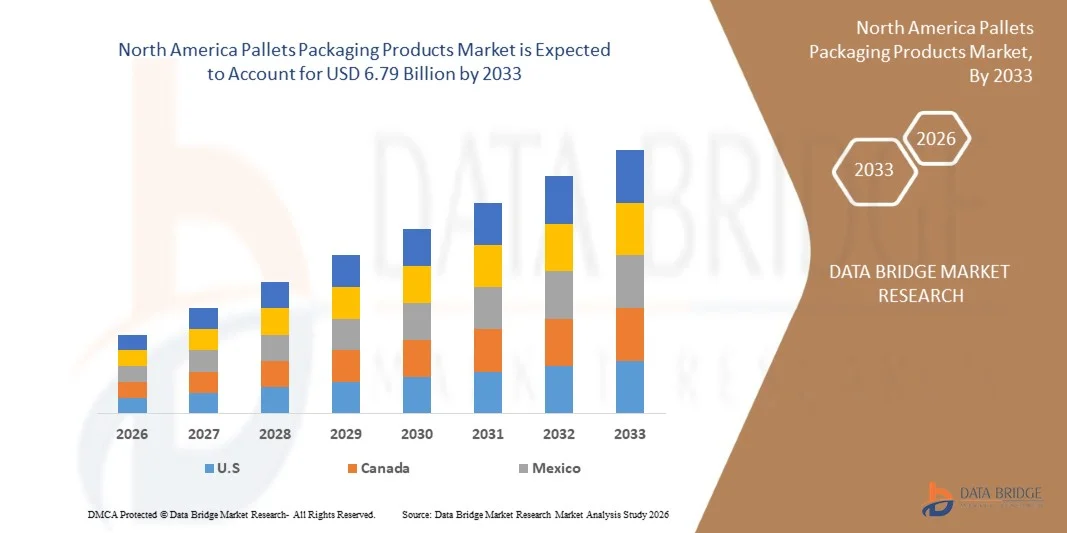

- Le marché nord-américain des produits d'emballage de palettes devrait atteindre6,79 milliards de dollars 2033de4,49 milliards de dollars en 2025, croissance avec unTCAC de 5,4 %pour la période de prévision 2026-2033

- Le marché des produits d'emballage de palettes en Amérique du Nord connaît une croissance soutenue et résiliente, soutenue par une forte production industrielle, l'expansion continue de l'infrastructure d'entreposage et de distribution, et l'adoption généralisée de systèmes de palettes normalisés dans des secteurs clés tels que l'alimentation et les boissons, les produits pharmaceutiques, les produits chimiques, la fabrication, le commerce de détail et les biens de consommation en mouvement rapide. La hausse des échanges transfrontaliers entre les États-Unis, le Canada et le Mexique, ainsi que l'expansion rapide du commerce électronique et du commerce de détail omnicanal, stimulent la demande soutenue de solutions d'emballage de palettes efficaces, durables et à haute charge.

- L'expansion du marché est encore renforcée par des réglementations axées sur la durabilité et des engagements d'ESG d'entreprise, ce qui entraîne une adoption accrue de matériaux de palette recyclables, réutilisables et légers comme le plastique, le composite et le bois d'ingénierie. L'accent mis sur la sécurité des travailleurs, la stabilité de la charge et la réduction des dommages lors de la manipulation automatisée et manuelle des matériaux accélère l'utilisation de palettes à haute performance. De plus, les investissements dans l'automatisation des entrepôts, les systèmes de manutention robotique et les palettes intelligentes avec des capacités de suivi améliorent l'efficacité de la chaîne d'approvisionnement et soutiennent la croissance à long terme du marché des produits d'emballage de palettes partout en Amérique du Nord.

Amérique du Nord Palettes Produits d'emballage Analyse du marché

- L'emballage des palettes devient de plus en plus critique dans toute l'Amérique du Nord en termes de logistique et d'écosystèmes industriels, ce qui permet une manutention sécuritaire, efficace et normalisée des marchandises dans les opérations d'entreposage, de transport et de distribution. Les palettes améliorent la stabilité de la charge, réduisent les dommages causés aux produits et améliorent l'efficacité de la manutention des matériaux dans des secteurs clés comme la fabrication, les aliments et les boissons, les produits pharmaceutiques, les produits chimiques, la construction et le commerce de détail.

- L'expansion de la production industrielle, la croissance rapide du commerce électronique et l'automatisation croissante des entrepôts en Amérique du Nord alimentent une forte demande de solutions d'emballage de palettes. Les industries adoptent de plus en plus des systèmes avancés d'emballage et de stabilisation des palettes pour améliorer l'efficacité de la chaîne d'approvisionnement, réduire le travail manuel et répondre aux exigences croissantes en matière de débit.

- De plus, des normes réglementaires rigoureuses en matière de sécurité des travailleurs, de réduction des déchets d'emballage et de durabilité accélèrent l'adoption de matériaux d'emballage recyclables et légers pour palettes. Les entreprises investissent de plus en plus dans des palettes écologiques et des films stretch recyclables pour se conformer aux directives environnementales de l'UE et aux objectifs de durabilité des entreprises.

- On prévoit que les États-Unis occuperont la première place sur le marché des produits d'emballage des palettes en Amérique du Nord en 2025, représentant 76,41 % de la part de marché régionale. Cette domination est soutenue par la forte base manufacturière du pays, l'infrastructure logistique avancée, l'adoption élevée de l'automatisation dans les entrepôts, et des règlements stricts de sécurité au travail. Les initiatives gouvernementales visant à promouvoir des emballages durables et des chaînes d'approvisionnement efficaces renforcent encore la position de leader de l'Allemagne sur le marché nord-américain.

- Le segment des Stretch Films devrait dominer le marché des produits d'emballage de palettes en Amérique du Nord en 2026, avec une part de marché de 23,04 %, en raison de son rapport coût-efficacité, de sa flexibilité, de son fort confinement des charges et de sa facilité d'application. Les films stretch sont largement utilisés pour sécuriser les marchandises palettisées pendant l'entreposage et le transit, en particulier dans les environnements logistiques et d'entreposage automatisés à volume élevé, ce qui les rend essentiels pour assurer l'intégrité du produit et minimiser les pertes.

Portée du rapport et segmentation du marché des produits d'emballage des palettes en Amérique du Nord

| Attributs | Produits d'emballage des palettes en Amérique du Nord |

| Segments couverts |

|

| Pays couverts | Amérique du Nord

|

| Principaux acteurs du marché |

|

| Possibilités de marché |

|

| Infos sur la valeur ajoutée | En plus des renseignements sur les scénarios du marché tels que la valeur marchande, le taux de croissance, la segmentation, la couverture géographique et les principaux intervenants, les rapports de marché établis par Data Bridge Market Research comprennent aussi l'analyse des exportations d'importations, l'aperçu des capacités de production, l'analyse de la consommation de production, l'analyse des tendances des prix, le scénario du changement climatique, l'analyse de la chaîne d'approvisionnement, l'analyse de la chaîne de valeur, l'aperçu des matières premières et des consommables, les critères de sélection des fournisseurs, l'analyse PESTLE, l'analyse Porter et le cadre réglementaire. |

Amérique du Nord Palettes Produits d'emballage Tendances du marché

L'adoption de produits d'emballage de palettes dans toute la logistique nord-américaine et les opérations industrielles

- L'expansion constante des activités de fabrication, d'entreposage et de logistique dans toute l'Amérique du Nord est un facteur important de l'adoption de solutions d'emballage de palettes. Comme le commerce transfrontalier, le commerce électronique et les réseaux de distribution industrielle continuent de s'étendre, les entreprises comptent de plus en plus sur l'emballage des palettes pour assurer la manutention sécuritaire, efficace et rentable des marchandises dans les chaînes d'approvisionnement complexes et les corridors de transport à grande quantité.

- L'emballage des palettes joue un rôle crucial dans la protection des marchandises et la continuité opérationnelle tout au long des processus d'entreposage et de transport. En permettant des charges unitaires stables, en minimisant les dommages causés aux produits et en améliorant l'efficacité de la manutention, l'emballage des palettes réduit les risques associés à la manutention manuelle tout en soutenant des opérations ininterrompues entre les entrepôts, les centres de distribution, les usines de fabrication et les réseaux d'approvisionnement de détail.

- L'utilisation croissante d'opérations logistiques de pointe, y compris l'entreposage automatisé, les systèmes de stockage à grande baie et les modèles de livraison juste à temps, a accru la demande de solutions d'emballage de palettes à haute performance. Les innovations dans les films stretch, les boîtes à palettes, les couvercles et les systèmes de fixation améliorent la stabilité, la sécurité et l'efficacité de la charge dans des conditions logistiques et de transport exigeantes.

- Les pays d'Amérique du Nord dotés de solides bases industrielles et de centres logistiques, comme les États-Unis, le Canada et le Mexique, sont à l'origine de l'adoption généralisée de solutions d'emballage de palettes. Des règlements stricts en matière de sécurité au travail, des mandats de durabilité et la nécessité d'optimiser l'efficacité du transport encouragent les industries à adopter des systèmes d'emballage de palettes normalisés, durables et recyclables.

- Dans l'ensemble, l'ampleur croissante des opérations de production industrielle, de commerce et de logistique en Amérique du Nord place l'emballage des palettes comme une composante essentielle de la stratégie moderne de la chaîne d'approvisionnement. L'emballage de palettes soutient la sécurité des produits, l'efficacité opérationnelle, la conformité réglementaire et la croissance durable dans toute l'Amérique du Nord.

Amérique du Nord Palettes Produits d'emballage Dynamique du marché

Chauffeur

Croissance des réseaux de logistique, d'entreposage et de distribution organisés

- La croissance des réseaux organisés de logistique, d'entreposage et de distribution stimule la demande mondiale d'emballage de palettes, à mesure que les chaînes d'approvisionnement passent du stockage fragmenté aux entrepôts centralisés, aux grands centres de distribution et aux installations 3PL gérées par des professionnels.

- Les palettes servent d'épine dorsale à ces environnements logistiques modernes, permettant un empilage efficace, un racking, une manutention mécanisée et l'exécution des commandes à haut débit, améliorant ainsi les délais d'exécution et le contrôle des stocks.

- L'expansion des infrastructures d'entreposage et de distribution, entraînée par le commerce électronique et les opérations 3PL, a accru l'utilisation des palettes pour faciliter la consolidation, le mouvement et le stockage des marchandises dans les chaînes d'approvisionnement nationales et internationales.

- Étant donné que les industries comptent de plus en plus sur la manutention normalisée des matériaux dans les centres logistiques centralisés et mécanisés, les palettes demeurent un atout essentiel et fondamental, assurant une demande soutenue et prévisible dans les chaînes d'approvisionnement modernes.

Restriction/Défi

Volatilité en matière première Disponibilité et prix

- La volatilité de la disponibilité et des prix des matières premières constitue une restriction importante affectant le marché des emballages de palettes. La production de palettes est fortement tributaire de matériaux clés comme le bois, les plastiques et les polymères recyclés, dont l'offre et les coûts sont sujets à des fluctuations en raison de facteurs tels que les pénuries saisonnières de bois, les changements dans la production de résine, la dynamique du commerce mondial et les pressions inflationnistes. Cette imprévisibilité augmente non seulement les coûts de fabrication, mais affecte aussi la planification des achats, la stabilité des prix et la continuité de la chaîne d'approvisionnement pour les utilisateurs finaux. Par conséquent, les fabricants et les fournisseurs de services de logistique doivent faire face à des difficultés pour maintenir la qualité, la disponibilité et l'abordabilité des palettes, ce qui fait de la volatilité des matières premières un facteur critique limitant la croissance du marché.

Par exemple,

- Comme l'indiquent les indices d'Emballaging News UK en mai 2025, l'achat de palettes spécifiques en bois est devenu plus difficile pour les fabricants, parallèlement à la hausse des prix du bois, ce qui indique des problèmes de disponibilité des matières premières qui compliquent la planification de la production et la stabilité des coûts.

- Comme l'a souligné Global Wood en juillet 2024, les fabricants de palettes au Royaume-Uni et en Irlande font face à des hausses significatives du coût des matières premières en raison de la disponibilité limitée des billes, de l'augmentation des prix des usines outre-mer et de la baisse des volumes de bois importé, ce qui entraîne une volatilité des coûts des matières premières pour les palettes.

- En conclusion, la volatilité de la disponibilité des matières premières et des prix demeure une contrainte critique pour le marché des emballages de palettes. Les fluctuations des coûts du bois, des plastiques et des polymères recyclés, dues aux pénuries d'approvisionnement, à la dynamique commerciale et aux contraintes de production, ont une incidence directe sur les dépenses de fabrication, la tarification des palettes et la planification des achats. Cette imprévisibilité met les fabricants au défi de maintenir une disponibilité constante des produits, un contrôle des coûts et des normes de qualité. En conséquence, la volatilité des matières premières non seulement limite la croissance du marché, mais oblige aussi les producteurs de palettes et les utilisateurs finals à adopter un approvisionnement stratégique, des matériaux de remplacement et une gestion efficace des stocks pour atténuer les risques et maintenir la continuité de la chaîne d'approvisionnement.

Amérique du Nord Palettes Produits d'emballage Portée du marché

Le marché des produits d'emballage des palettes en Amérique du Nord est segmenté en six segments notables, selon le type de produit, le type de machine, le type de fonction, l'application, l'utilisation finale et le canal de distribution.

- Par type de produit

Sur la base du type de produit, le marché est segmenté en films stretch, films de hotte rétractable, palettes euro, boîtes à palettes, couvercles et capsules de palettes, feuilles de glissement et feuilles de niveau, enveloppes stretch, hottes stretch et filets de palettes. En 2026, on prévoit que le segment des films stretch dominera le marché mondial des produits d'emballage de palettes avec la plus grande part de marché de 23,04 %, en raison de leur stabilité de charge supérieure, de leur étirement élevé, de leur résistance à la perforation et de leur rentabilité dans la sécurisation des marchandises palettisées pendant le stockage et le transport. Les films stretch sont largement utilisés dans les industries des aliments et des boissons, des produits pharmaceutiques, des produits chimiques et des biens de consommation pour prévenir le déplacement des charges, l'infiltration d'humidité et la contamination. De plus, leur compatibilité avec les systèmes d'emballage de palettes manuelles et automatisées, ainsi qu'avec la demande croissante de films recyclables et downgauged, favorise la croissance des segments.

Le segment des films stretch devrait croître à un TCAC de 5,9 %, en raison de la hausse de l'automatisation des entrepôts, de la demande d'emballages légers et recyclables et de l'utilisation généralisée dans les secteurs de la logistique, de l'alimentation et des produits pharmaceutiques en Amérique du Nord.

- Par type de machine

Sur la base du type de machine, le marché est segmenté en systèmes entièrement automatiques et semi-automatiques. En 2026, le segment entièrement automatique devrait dominer le marché mondial des produits d'emballage de palettes avec une part de marché de 64,78 %, en raison de sa capacité à gérer des opérations de palettisation à haut débit avec une qualité d'emballage constante, une réduction de la dépendance à la main-d'oeuvre et une efficacité opérationnelle accrue. Les systèmes d'emballage de palettes entièrement automatiques sont largement utilisés dans les installations de fabrication et de distribution à grande échelle pour réduire au minimum les temps d'arrêt, améliorer la sécurité des travailleurs et assurer un confinement uniforme des charges. L'intégration avec les systèmes de convoyeurs, la robotique, les commandes PLC et la surveillance de l'industrie 4.0 accélère encore l'adoption parmi les utilisateurs finaux à haut volume.

Le segment entièrement automatique devrait enregistrer un TCAC de 5,3%, soutenu par l'automatisation croissante dans les entrepôts, l'optimisation des coûts de main-d'oeuvre, et l'adoption de systèmes d'emballage de palettes compatibles avec l'industrie 4.0 dans toute l'Amérique du Nord.

- Par type de fonction

Sur la base du type de fonction, le marché est segmenté en enveloppe, sangle, protection & rembourrage, capotage, etc. En 2026, le secteur de l'emballage devrait dominer le marché mondial des produits d'emballage de palettes avec une part de marché de 45,41 %, en raison de son rôle crucial dans la stabilisation des charges de palettes, la protection des marchandises contre la poussière, l'humidité et les dommages mécaniques et la sécurité du transport sur de longues distances. Les solutions d'emballage telles que l'emballage stretch et rétractable sont largement utilisées dans la logistique, l'alimentation et les boissons, et la fabrication industrielle en raison de leur polyvalence, facilité d'application et compatibilité avec différentes tailles de palettes. L'accent mis de plus en plus sur l'efficacité de la chaîne d'approvisionnement et la réduction des dommages contribue à l'expansion du segment.

Le segment de l'emballage devrait croître à un TCAC de 5,7 %, en raison de l'importance croissante accordée à la stabilité de la charge, à la réduction des dommages et à l'efficacité du transport de palettes dans les chaînes d'approvisionnement nord-américaines.

- Par demande

Sur la base de l'application, le marché est segmenté en aliments et boissons, commerce de détail et électronique, produits emballés de consommation (PAG), produits pharmaceutiques, produits chimiques, agriculture et horticulture, fabrication industrielle, automobile, électronique et électroménager, etc. En 2026, le segment des aliments et boissons devrait dominer le marché mondial des produits d'emballage de palettes, avec la plus grande part de marché de 20,50 %, en raison du volume élevé de mouvements palettisés des aliments emballés, des boissons et des consommables en vrac nécessitant des solutions d'emballage sûres, hygiéniques et résistantes aux dommages. L'emballage en palettes assure l'intégrité du produit pendant l'entreposage en chaîne froide, l'entreposage et le transport long-courrier. La demande croissante de produits alimentaires emballés et prêts à consommer, ainsi que des règlements rigoureux en matière de salubrité et de manipulation des aliments, continuent de favoriser l'adoption dans ce segment.

Le segment des aliments et des boissons devrait croître à un TCAC de 6,2 %, en raison de l'expansion de la logistique de la chaîne du froid, de la consommation élevée d'aliments emballés et de la stricte réglementation en matière de salubrité des aliments en Amérique du Nord.

- Par utilisation finale

Sur la base de l'utilisation finale, le marché est segmenté en fournisseurs de logistique & 3PL, usines de fabrication, centres de distribution de détail, opérateurs de chaîne du froid, etc. En 2026, le segment des fournisseurs de logistique & 3PL devrait dominer le marché mondial des produits d'emballage de palettes avec la plus grande part de marché de 38,96 %, en raison de la manutention, de la consolidation et de la redistribution des marchandises palettisées dans plusieurs industries. Les fournisseurs de services logistiques comptent beaucoup sur les solutions d'emballage de palettes pour assurer la stabilité de la charge, réduire les dommages de transit et améliorer l'efficacité de l'entrepôt. La croissance rapide du commerce électronique, du commerce transfrontalier et des services d'entreposage tiers accroît encore la demande de produits d'emballage de palettes fiables et évolutives.

Le segment des fournisseurs de services logistiques et 3PL devrait croître à un TCAC de 5,9 %, en raison de la croissance du commerce électronique, de l'expansion des services logistiques de tiers et de l'augmentation du commerce transfrontalier en Amérique du Nord.

- Par canal de distribution

Sur la base du canal de distribution, le marché est classé en canaux directs et indirects. Le canal direct est ensuite segmenté en équipes de vente de l'entreprise, en contrats directs d'OEM et en sites Web appartenant à l'entreprise, tandis que le canal indirect est segmenté en grossistes/distributeurs, en magasins d'approvisionnement industriels et en commerce électronique tiers. En 2026, le segment direct devrait dominer le marché mondial des produits d'emballage de palettes avec une part de marché de 57,35 %, en raison d'une forte préférence parmi les gros acheteurs industriels pour l'approvisionnement direct des fabricants afin d'assurer des solutions personnalisées, des avantages de prix en vrac et un soutien technique. Les canaux directs permettent aux utilisateurs finaux d'accéder à des systèmes d'emballage de palettes sur mesure, à des contrats d'approvisionnement à long terme et à des services après-vente. De plus, l'adoption croissante de relations directes avec les OEM et de plateformes de vente numériques dirigées par les fabricants renforce la domination de ce segment.

Le segment direct devrait croître à un TCAC de 5,6 %, appuyé par la préférence pour l'approvisionnement direct des fabricants, des solutions personnalisées et des accords d'approvisionnement à long terme entre acheteurs industriels nord-américains

Amérique du Nord Produits d'emballage Marché Analyse régionale

- Les États-Unis représentent le marché le plus important et le plus influent pour les produits d'emballage de palettes en Amérique du Nord, appuyé par sa base de fabrication étendue, sa consommation intérieure élevée et l'une des infrastructures de logistique et d'entreposage les plus avancées au monde. De forts flux commerciaux entre États et transfrontaliers, l'adoption généralisée de systèmes automatisés de manutention des matériaux et des réseaux de distribution à grande échelle pour le commerce de détail, l'alimentation et les boissons, les produits pharmaceutiques et les produits industriels continuent de stimuler la demande constante d'emballages de palettes partout au pays.

- Le Canada connaît une croissance constante de l'adoption des emballages de palettes, en raison de l'expansion de l'activité de commerce électronique, de la croissance des services logistiques de tiers et de l'augmentation des échanges transfrontaliers avec les États-Unis. Les investissements dans les centres de distribution modernes, la logistique de la chaîne du froid et les pratiques d'emballage durables accélèrent la demande de palettes normalisées, durables et réutilisables dans les secteurs de la transformation des aliments, des produits chimiques, des produits pharmaceutiques et du commerce de détail.

- Le Mexique devient un marché à forte croissance pour les emballages de palettes en Amérique du Nord, appuyé par l'expansion des activités manufacturières, une forte intégration dans les chaînes d'approvisionnement nord-américaines et l'augmentation des exportations d'automobiles, d'électronique et de biens de consommation. La croissance des parcs industriels, des centres logistiques et des investissements manufacturiers axés sur la quasi-sorcellerie accroît la demande de solutions d'emballage de palettes rentables et robustes, en plaçant les palettes comme une composante essentielle d'une manutention efficace des matériaux et de chaînes d'approvisionnement axées sur l'exportation dans le pays.

États-Unis Amérique du Nord Palettes Produits d'emballage Aperçu du marché

Le marché américain des produits d'emballage de palettes connaît une croissance forte et soutenue, stimulée par la production industrielle en volume élevé, une vaste base de consommateurs et l'une des infrastructures de logistique et d'entreposage les plus avancées au monde. Le leadership dans les secteurs de l'alimentation et des boissons, des produits pharmaceutiques, des produits chimiques, de la fabrication et de la distribution au détail génère une demande constante de systèmes normalisés de transport de palettes, d'emballage stretch et d'emballage automatisé de palettes. De plus, l'adoption généralisée de centres d'automatisation des entrepôts, de robotique et d'exécution à haut débit, particulièrement pour le commerce électronique et le commerce de détail omnicanal, accélère la demande de solutions d'emballage de palettes durables, stables et conformes aux normes de sécurité, et place les États-Unis comme le principal contributeur du marché nord-américain..

Canada Amérique du Nord Produits d'emballage Aperçu du marché

Le marché canadien des produits d'emballage de palettes ne cesse de croître, appuyé par la croissance des échanges transfrontaliers avec les États-Unis, l'augmentation des investissements dans les infrastructures modernes d'entreposage et l'adoption croissante de systèmes de stockage et de transport de palettes dans les secteurs de la transformation des aliments, de la vente au détail, des produits pharmaceutiques et de la fabrication industrielle. L'accent mis sur l'efficacité de la chaîne d'approvisionnement, la logistique de la chaîne du froid et la réduction des dommages pendant le transport renforce la demande d'emballages de palettes de haute qualité. En outre, l'accent mis par le Canada sur la durabilité, y compris les systèmes de palettes réutilisables et les matériaux d'emballage recyclables, encourage les entreprises à améliorer les solutions d'emballage de palettes, en favorisant la croissance à long terme du marché.

Amérique du Nord Palettes Emballage Produits Part de marché

L'industrie des produits d'emballage de palettes est principalement dirigée par des entreprises bien établies, notamment :

- Sigma Plastics Asia (Singapour)

- IPL Schoeller (Irlande)

- Novolex (États-Unis)

- Craemer GmbH (Allemagne)

- PalletOne (États-Unis)

- Groupe Aetna S.p.A. (Italie)

- Bekuplast sp. z o.o. (Pologne)

- Benoplast (France)

- Consudé (États-Unis)

- Systèmes d'emballage Fromm (Suisse)

- Palettes et conteneurs mondiaux (États-Unis)

- Greendot Biopak Pvt. Ltd. (Inde)

- Hexapak (Inde)

- HIVIC Plastic Manufacture Co., Ltd. (Chine)

- Groupe Intertape Polymer (Canada)

- Lantech (États-Unis)

- M Stretch S.p.A. (Italie)

- Groupe Maillis (France)

- Matere Packaging (Italie)

- Mosca GmbH (Allemagne)

- Orion Packaging Systems LLC (États-Unis)

- Paragon Films (États-Unis)

- Polyfavo (Inde)

- Polyreflex Hi-Tech Co., Ltd. (Inde)

- Industrie de l'emballage Rokson (Inde)

- TranPak Inc. (États-Unis)

- Transoplast (Pays-Bas)

- Trioworld (Suède)

- UCMPL (Inde)

- Wulftec International Inc. (Canada)

- Bunzl Australie et Nouvelle-Zélande (Australie)

- La société Fastenal (États-Unis)

- Uline (États-Unis)

- Veritiv Operating Company (États-Unis)

- W.W. Grainger, Inc. (États-Unis)

Derniers développements en Amérique du Nord Marché des produits d'emballage de palettes

- Décembre 2025 – Lantech a présenté ses packs stretch semi-automatiques de nouvelle génération, les SL400 et SL400LT, conçus pour remédier aux pénuries de main-d'œuvre et améliorer l'efficacité de l'emballage des palettes. Ces machines disposent d'automatisation avancée, de points de contact réduits et de technologies de stabilité de charge améliorées.

- En février 2025, Sigma Plastics Group, ainsi que sa filiale Mercury Plastics, ont acquis les actifs de Sun Plastics, Inc., basé en Californie, marquant la 43e acquisition de Sigmas et élargissant ses activités à 49 emplacements. Sun Plastics, fondée en 1979, se spécialise dans des sacs et des films LDPE 100% recyclables de haute qualité, adaptés à divers secteurs, notamment l'alimentation, la médecine, l'électronique et les marchés industriels. L'acquisition renforce la présence de Sigma en Amérique du Nord et améliore ses capacités en solutions d'emballage durables à valeur ajoutée. Cette démarche stratégique permettra à Sigma d'élargir la portée du marché, d'acquérir une expertise en matière de production et de créer de nouvelles possibilités de croissance.

- En mai 2025, Transoplast Group et Schoeller Allibert ont lancé un partenariat Platinum, Transoplast devenant le principal distributeur des produits Schoeller Allibert. Cette collaboration vise à fournir des solutions logistiques innovantes et durables dans toutes les industries, en améliorant l'efficacité et les performances de la chaîne d'approvisionnement. Transoplast étendra son inventaire à un centre logistique de 25 000 m2, permettant une livraison plus rapide, une personnalisation et l'accès à des produits Schoeller Allibert de haute qualité même pour les petites commandes. Le partenariat renforce les solutions centrées sur le client grâce à des options d'emballage personnalisées et évolutives.

- En octobre 2025, la Commission européenne a accordé une exemption complète pour l'emballage des palettes et les sangles des objectifs de réutilisation à 100 % en vertu de l'article 29, paragraphes 2 et 3, du règlement sur les emballages et les déchets d'emballages. Toutefois, l'objectif de réutilisation de 40 % pour les emballages de transport transfrontaliers prévu à l'article 29, paragraphe 1, est toujours à l'étude. Cette exemption permet à des entreprises comme Trioworld de continuer à produire et à fournir des films de palette haute performance sans modifications réglementaires immédiates, assurant la stabilité opérationnelle et soutenant l'innovation continue dans les solutions d'emballage durables.

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Table des matières

1 INTRODUCTION

1.1 OBJECTIFS DE L'ÉTUDE

1.2 DÉFINITION DU MARCHÉ

1.3 APERÇU DU MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD

1.4 MONNAIE ET PRÊT

1.5 LIMITATIONS

1.6 MARCHÉS COUVERTS

2 SEGMENTATION DU MARCHÉ

2.1 MARCHÉS COUVERTS

2.2 ANS CONSIDÉRÉS POUR L'ÉTUDE

2.3 MODÈLE DE VALIDATION DES DONNÉES DU TRIPOD DBMR

2.4 INTERVIEWS PRIMAIRES AVEC LES PRINCIPAUX DIRECTEURS DE L'AVIS

2.5 GRID DE POSITION DU MARCHÉ DBMR

2.6 ANALYSE DU PARTAGE DES VENDEURS

2.7 MODÈLE MULTIVARIAT

2.8 COURS D'EXÉCUTION

2.9 GRID DE COUVERTURE VERTIQUE DU MARCHÉ

2.1 SOURCES SECONDAIRES

2.11 OBSERVATIONS

3 RÉSUMÉ

4 PRIMAIRES

4.1 ANALYSE DES CINQ FORCES

4.1.1 INTENSITÉ DE LA RIVALISATION COMPÉTITIVE

4.1.2 POUVOIR D'ACHETS / CONSOMMATEURS

4.1.3 MENACES DES NOUVEAUX ENTRANTS

4.1.4 MENACES DES PRODUITS SUSCITUTAIRES

4.1.5 POUVOIR DE FABRICATION

4.1.6 CONCLUSION

4.2 ANALYSE PRICTUELLE

4.3 ANALYSE DE LA CHAINE DE VALEUR

4.3.1 MATÉRIEL VÉTÉRINAIRE ET DÉCHETS

4.3.2 FABRICATION ET TRAITEMENT

4.3.3 DISTRIBUTION ET INTÉGRATION LOGISTIQUE

4.3.4 INDUSTRIES DE LA FIN ET CHANEAUX DE VENTE

4.3.5 CONCLUSION

4.4 ANALYSE DE LA CHAINE D'APPROVISIONNEMENT

4.4.1 SOURCES ET ACHETS DE MATÉRIAUX RAW

4.4.2 TRAITEMENT ET FABRICATION DES PRODUITS (PRODUCTION)

4.4.3 LOGISTIQUE DE LA CHAÎNE DE DÉPLACEMENT ET DE DISTRIBUTION (TRANSPORTATION)

4.4.4 CHANEAUX D'ACHETEMENT ET D'ACHETS COMMERCIAUX (DISTRIBUTION ET VENTES)

4.4.5 CONCLUSION

4.5 CRITÈRES DE SÉLECTION DU VENDEUR

4.5.1 QUALITÉ ET CONFORMITÉ DES PRODUITS

4.5.2 RÉGIME DE PRODUITS ET DOUANISATION

4.5.3 PRICTION ET COÛT TOTAL DE LA PROPRIÉTÉ

4.5.4 RESPONSABILITÉ DE LA CHAINE D'APPROVISIONNEMENT

4.5.5 SOUTIEN TECHNIQUE ET SERVICE

4.5.6 DURABLE ET PRATIQUES ENVIRONNEMENTALES

4.5.7 RÉPUTATION DES VENDEURS ET STABILITÉ FINANCIÈRE

4.5.8 INTÉGRATION DE L'INNOVATION ET DE LA TECHNOLOGIE

4.5.9 ÉVALUATION DES RISQUES ET DE LA CONFORMITÉ

4.5.10 PARTENARIAT ET FIT STRATÉGIQUE

4.6 AVANTAGES TECHNOLOGIQUES

4.6.1 INNOVATION DES MATIÈRES DURABLES

4.6.2 AUTOMATISATION ET ROBOTICES DANS L'EMBALLAGE DE PALLET

4.6.2.1 Intégration avec la robotique et les lignes automatisées :

4.6.2.2 Commandes et interfaces de machines avancées :

4.6.3 ÉMBALLAGE SMART ET INTÉGRATION IOT

4.6.4 EFFICACITÉ ET TECHNOLOGIES DE RÉDUCTION DES DÉCHETS

4.6.5 SOUTIEN DE LA DURABLE PAR L'INNOVATION

4.7 TRAQUEMENT D'INNOVATION ET ANALYSE STRATÉGIQUE

4.7.1 PRINCIPAUX DELS ET ANALYSE DES ALLIANCES STRATÉGIQUES

4.7.2 DÉVELOPPEMENT ACTIF

4.7.3 TENDANCE DU DÉVELOPPEMENT

4.7.4 ÉLÉMENTS ET MILLETS

4.7.5 STRATÉGIES ET MÉTHODES D'INNOVATION

4.7.6 ÉVALUATION ET MITIGATION DES RISQUES

4.7.7 PERSPECTIVES FUTURES

4.8 CHANGEMENT CLIMATIQUE SCÉNARIO

4.8.1 TRANSFORMATION DE LA SOURCE DES MATÉRIAUX RAW

4.8.2 LA RESPONSABILITÉ DU CARBONE FOOTPRINT ACROSSE LE CYCLE DE VIE PALLET

4.8.3 INFLUENCE DE LA VOLATILITÉ CLIMATIQUE SUR LE RENDEMENT ET LA DESIGN DES PALLETS

4.8.4 RÉGLEMENTATION ET ALIGNEMENT POLITIQUE AVEC LES ENGAGEMENTS CLIMATIQUES

4.8.5 CHANGEMENT CLIMATIQUE EN CAS DE CATALYSE POUR L'INNOVATION ET LA REPOSITION STRATÉGIQUE

4.9 ANALYSE DES ÉCOSYSTÈMES DE L'INDUSTRIE

4.9.1 ENTREPRISES PROMINENTES

4.9.2 Petites et moyennes entreprises

4.9.3 UTILISATEURS DE FIN

5 TARIF ET IMPACT SUR LE MARCHÉ

5.1 TAUX TARIFAIRE ACTUEL (S) SUR LES MARCHÉS DU TOP-5

5.1.1 ÉTATS-UNIS (MAJOR IMPORTATEUR D'EMBALLAGE DE PALLET):

5.1.2 CHINE (MAJOR PRODUCTEUR & EXPORTATEUR)

5.1.3 INDE

5.1.4 UNION EUROPÉENNE

5.1.5 BRÉSIL

5.2 PERSPECTIVES: PRODUCTION LOCALE

5.3 CRITÈRES DE SÉLECTION DES VENDEURS DYNAMIQUES

5.4 IMPACT SUR LA CHAINE D'APPROVISIONNEMENT

5.4.1 Achats de matières premières:

5.4.2 FABRICATION ET PRODUCTION:

5.4.3 LOGISTIQUES ET DISTRIBUTION:

5.4.4 POSITION DES PRIX SUR LE MARCHÉ:

5.5 PARTICIPANTS DE L'INDUSTRIE: MOUVEMENTS PROACTIFS

5.5.1 OPTIMISATION DE LA CHAINE D ' APPUI

5.5.2 ÉTABLISSEMENTS COMMUNS DE VENTURE

5.6 IMPACT SUR LES PRIX

5.7 INCLINATION RÉGLEMENTAIRE

5.7.1 SITUATION GEOPOLITIQUE

5.7.2 PARTENARIATS COMMERCIAUX ENTRE PAYS

5.7.2.1 ACCORDS DE LIBRE-ÉCHANGE

5.7.2.2 ÉTABLISSEMENTS D'ALLIANCES

5.7.3 ACCRÉDITATION DE L'ÉTAT (Y COMPRIS LA MFTN)

5.7.4 COURS DOMESTIQUE DE CORRECTION

5.7.4.1 RÉGIMES INCENTIFS DE LA PRODUCTION

5.7.4.2 ÉTABLISSEMENT DES ZES ET DES PARCS INDUSTRIELS

6 COUVERTURE DU RÈGLEMENT

6.1 CODES DES PRODUITS

6.2 NORMES CERTIFIÉES

6.3 NORMES DE SÉCURITÉ

6.3.1 MATÉRIEL ET STOCKAGE

6.3.2 TRANSPORT ET PRÉCAUTIONS

6.3.3 IDENTIFICATION DU DANGER

7 APERÇU DU MARCHÉ

7.1 Conducteurs

7.1.1 EXPANSION DE LA FABRICATION DE L'AMÉRIQUE DU NORD ET DE L'EXPOSITION INDUSTRIELLE.

7.1.2 CROISSANCE DES RÉSEAUX LOGISTIQUES ORGANISÉS, DES RÉSEAUX D'ÉTABLISSEMENT ET DE DISTRIBUTION.

7.1.3 RENFORCEMENT DE LA PRÉFÉRENCE POUR LE CHARGEMENT UNITISÉ.

7.1.4 ADOPTION DE L'EMBALLAGE DE TRANSPORT réutilisable ET RETOURNABLE (RTP).

7.2 RÉSULTATS

7.2.1 VOLATILITÉ DANS LA DISPONIBILITÉ ET LA PRICTION DES MATÉRIAUX

7.2.2 NORMALISATION LIMITÉE DANS LES RÉGIONS ET LES INDUSTRIES DE LA FIN .

7.3 POSSIBILITÉ

7.3.1 VERS LES PALLETS PLASTIQUES ET COMPOSITIFS DANS LES INDUSTRIES RÉGULÉES

7.3.2 INTÉGRATION DES TECHNOLOGIES DE TRAITEMENT ET D'IDENTIFICATION .

7.3.3 DEMANDE D'EXPORTATION D'ÉCONOMIES ÉMERGÉES

7.4 DÉFIS

7.4.1 COÛTS DE RÉPONSE, DE LOGISTIQUE REVIERE ET DE RECOUVREMENT

7.4.2 PROBLÈMES ENVIRONNEMENTAUX ET ÉLIMINAIRES POUR LES PALLETS EN FIN DE LIF

8 MARCHÉ DES PALLETS D'AMÉRIQUE DU NORD, PAR TYPE DE PRODUITS

8.1 Aperçu général

8.2 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR TYPE DE PRODUITS, 2018-2033 (MILLIERS USD)

8.2.1 FILMS DE STRETTE

8.2.2 FEUILLES D'HOODAGE

8.2.3 PALLET EURO

8.2.4 BOÎTES DE PALLET

8.2.5 PALLETTES ET CAPS

8.2.6 FEUILLES ET FEUILLES DE TIER

8.2.7 GRANDES GRANDES

8.2.8 RENFORCEMENT DES HORAIRES

8.2.9 RÉSEAU DE PALLET

8.3 FILMS D'AMÉRIQUE DU NORD DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

8.3.1 ASIE-PACIFIQUE

8.3.2 AMÉRIQUE DU NORD

8.3.3 L'EUROPE

8.3.4 MOYEN-ORIENT ET AFRIQUE

8.3.5 AMÉRIQUE DU SUD

8.4 FEUILLES D'HOODAGE DE L'AMÉRIQUE DU NORD DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

8.4.1 ASIE-PACIFIQUE

8.4.2 AMÉRIQUE DU NORD

8.4.3 L'EUROPE

8.4.4 MOYEN-ORIENT ET AFRIQUE

8.4.5 AMÉRIQUE DU SUD

8.5 PALLET EURO DE L'AMÉRIQUE DU NORD DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

8.5.1 ASIE-PACIFIQUE

8.5.2 AMÉRIQUE DU NORD

8.5.3 EUROPE

8.5.4 MOYEN-ORIENT ET AFRIQUE

8.5.5 AMÉRIQUE DU SUD

8.6 BOÎTES DE PALLET DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLOIS USD)

8.6.1 ASIE-PACIFIQUE

8.6.2 AMÉRIQUE DU NORD

8.6.3 L'EUROPE

8.6.4 MOYEN-ORIENT ET AFRIQUE

8.6.5 AMÉRIQUE DU SUD

8.7 PALTES ET CAPES DE PALLET DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

8.7.1 ASIE-PACIFIQUE

8.7.2 AMÉRIQUE DU NORD

8.7.3 EUROPE

8.7.4 MOYEN-ORIENT ET AFRIQUE

8.7.5 AMÉRIQUE DU SUD

8.8 FEUILLES ET FEUILLES DE TIER DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en milliers de dollars)

8.8.1 ASIE-PACIFIQUE

8.8.2 AMÉRIQUE DU NORD

8.8.3 L'EUROPE

8.8.4 MOYEN-ORIENT ET AFRIQUE

8.8.5 AMÉRIQUE DU SUD

8.9 GRAPHIQUE DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE DE MACHINE, 2018-2033 (en MILLEUR)

8.9.1 AUTOMATIQUE COMPLÈTE

8.9.2 SÉMI AUTOMATIQUE

8.1 GRAPHIQUE AUTOMATIQUE COMPLÈTE DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS DE USD)

8.10.1 SYSTÈMES D'ÉLABORATION INTÉRIEURE

8.10.2 SYSTÈMES D'ÉCRIPTION MONOBLOQUE

8.11 GRAPHIQUE DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

8.11.1 ASIE-PACIFIQUE

8.11.2 AMÉRIQUE DU NORD

8.11.3 L'EUROPE

8.11.4 MOYEN-ORIENT ET AFRIQUE

8.11.5 AMÉRIQUE DU SUD

8.12 HOODERS D'AMÉRIQUE DU NORD DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE DE MACHINE, 2018-2033 (en MILLEUR)

8.12.1 AUTOMATIQUE COMPLÈTE

8.12.2 SÉMI AUTOMATIQUE

8.13 AMERIQUE DU NORD HOODERS FULLY AUTOMATIC STRETCH DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (en MILLIERS USD)

8.13.1 SYSTÈMES D'HORAGE EN LIGNE

8.13.2 SYSTÈMES D ' HODOLOGATION DES MONOBLOCS

8.14 HOODERS D'AMÉRIQUE DU NORD DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

8.14.1 ASIE-PACIFIQUE

8.14.2 AMÉRIQUE DU NORD

8.14.3 L'EUROPE

8.14.4 MOYEN-ORIENT ET AFRIQUE

8.14.5 AMÉRIQUE DU SUD

8.15 PALLET D'AMÉRIQUE DU NORD RÉSEAU SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLIERS USD)

8.15.1 ASIE-PACIFIQUE

8.15.2 AMÉRIQUE DU NORD

8.15.3 L'EUROPE

8.15.4 MOYEN-ORIENT ET AFRIQUE

8.15.5 AMÉRIQUE DU SUD

9 MARCHÉ DE L'EMBALLAGE DES PALLETTES D'AMÉRIQUE DU NORD, PAR TYPE DE MACHINE

9.1 Aperçu général

9.2 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR TYPE DE MACHINE, 2018-2033 (en MILLE)

9.2.1 AUTOMATIQUE COMPLÈTE

9.2.2 SÉMI AUTOMATIQUE

9.3 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (en MILLE USD)

9.3.1 SYSTÈMES D'HOMOLOGATION EN LIGNE

9.3.2 SYSTÈMES MONOBLOQUES D'HODOLOGATION

9.4 AUTOMATIQUE COMPLÈTE DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

9.4.1 ASIE-PACIFIQUE

9.4.2 AMÉRIQUE DU NORD

9.4.3 L'EUROPE

9.4.4 MOYEN-ORIENT ET AFRIQUE

9.4.5 AMÉRIQUE DU SUD

9.5 SÉMI AUTOMATIQUE DE L'AMÉRIQUE DU NORD DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

9.5.1 ASIE-PACIFIQUE

9.5.2 AMÉRIQUE DU NORD

9.5.3 EUROPE

9.5.4 MOYEN-ORIENT ET AFRIQUE

9.5.5 AMÉRIQUE DU SUD

10 PALLETTES D'AMÉRIQUE DU NORD, PAR TYPE DE FONCTION

10.1 Aperçu général

10.2 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR TYPE DE FONCTION, 2018-2033 (MILLIERS USD)

10.2.1 ÉLABORATION

10.2.2 STRAPPING

10.2.3 PROTECTION ET CUSHIONNEMENT

10.2.4 HORAIRE

10.2.5 AUTRES

10.3 GRAPHIQUE DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

10.3.1 ASIE-PACIFIQUE

10.3.2 AMÉRIQUE DU NORD

10.3.3 L'EUROPE

10.3.4 MOYEN-ORIENT ET AFRIQUE

10.3.5 AMÉRIQUE DU SUD

10.4 AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLIERS USD)

10.4.1 ASIE-PACIFIQUE

10.4.2 AMÉRIQUE DU NORD

10.4.3 L'EUROPE

10.4.4 MOYEN-ORIENT ET AFRIQUE

10.4.5 AMÉRIQUE DU SUD

10.5 PROTECTION DE L'AMÉRIQUE DU NORD ET CUSHIONAGE SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

10.5.1 ASIE-PACIFIQUE

10.5.2 AMÉRIQUE DU NORD

10.5.3 L'EUROPE

10.5.4 MOYEN-ORIENT ET AFRIQUE

10.5.5 AMÉRIQUE DU SUD

10.6 HOODAGE DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLE US)

10.6.1 ASIE-PACIFIQUE

10.6.2 AMÉRIQUE DU NORD

10.6.3 L'EUROPE

10.6.4 MOYEN-ORIENT ET AFRIQUE

10.6.5 AMÉRIQUE DU SUD

10.7 AMÉRIQUE DU NORD AUTRES SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

10.7.1 ASIE-PACIFIQUE

10.7.2 AMÉRIQUE DU NORD

10.7.3 EUROPE

10.7.4 MOYEN-ORIENT ET AFRIQUE

10.7.5 AMÉRIQUE DU SUD

11 MARCHÉ DE L'EMBALLAGE DES PALLES D'AMÉRIQUE DU NORD, PAR DEMANDE

11.1 Aperçu général

11.2 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR DEMANDE, 2018-2033 (en MILLE US)

11.2.1 ALIMENTS ET BOISSONS (1000)

11.2.2 DÉTAIL ET COMMERCE E

11.2.3 MARCHANDISES COMMERCIALES (PAG)

11.2.4 PHARMACEUTIQUES (2100)

11.2.5 PRODUITS CHIMIQUES (2000)

11.2.6 AGRICULTURE ET HORTICULTURE (0100)

11.2.7 FABRICATION INDUSTRIELLE (0001)

11.2.8 AUTOMOBILE (2900)

11.2.9 ÉLECTRONIQUES ET APPLICATIONS (2500)

11.2.10 AUTRES

11.3 ALIMENTS ET BOISSONS DE L'AMÉRIQUE DU NORD (1000) SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

11.3.1 ASIE-PACIFIQUE

11.3.2 AMÉRIQUE DU NORD

11.3.3 L'EUROPE

11.3.4 MOYEN-ORIENT ET AFRIQUE

11.3.5 AMÉRIQUE DU SUD

11.4 DÉTAILLAGE ET COMMERCE E-NORD-AMÉRIQUE DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE PALLET, PAR RÉGION, 2018-2033 (en milliers de dollars)

11.4.1 ASIE-PACIFIQUE

11.4.2 AMÉRIQUE DU NORD

11.4.3 L'EUROPE

11.4.4 MOYEN-ORIENT ET AFRIQUE

11.4.5 AMÉRIQUE DU SUD

11.5 MARCHANDISES DE CONSOMMATION DE L'AMÉRIQUE DU NORD (CPG) (1000) DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

11.5.1 ASIE-PACIFIQUE

11.5.2 AMÉRIQUE DU NORD

11.5.3 L'EUROPE

11.5.4 MOYEN-ORIENT ET AFRIQUE

11.5.5 AMÉRIQUE DU SUD

11.6 PHARMACEUTIQUES DE L'AMÉRIQUE DU NORD (2100) SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

11.6.1 ASIE-PACIFIQUE

11.6.2 AMÉRIQUE DU NORD

11.6.3 L'EUROPE

11.6.4 MOYEN-ORIENT ET AFRIQUE

11.6.5 AMÉRIQUE DU SUD

11.7 CHIMIQUES DE L'AMÉRIQUE DU NORD (2000) SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

11.7.1 ASIE-PACIFIQUE

11.7.2 AMÉRIQUE DU NORD

11.7.3 L'EUROPE

11.7.4 MOYEN-ORIENT ET AFRIQUE

11.7.5 AMÉRIQUE DU SUD

11.8 AGRICULTURE ET HORTICULTURE DE L'AMÉRIQUE DU NORD (0100) DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLIERS USD)

11.8.1 ASIE-PACIFIQUE

11.8.2 AMÉRIQUE DU NORD

11.8.3 EUROPE

11.8.4 MOYEN-ORIENT ET AFRIQUE

11.8.5 AMÉRIQUE DU SUD

11.9 FABRICATION INDUSTRIELLE DE L'AMÉRIQUE DU NORD (0001) SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLIERS USD)

11.9.1 ASIE-PACIFIQUE

11.9.2 AMÉRIQUE DU NORD

11.9.3 EUROPE

11.9.4 MOYEN-ORIENT ET AFRIQUE

11.9.5 AMÉRIQUE DU SUD

11.1 AMÉRIQUE DU NORD AUTOMOTIF (2900) SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

11.10.1 ASIE-PACIFIQUE

11.10.2 AMÉRIQUE DU NORD

11.10.3 EUROPE

11.10.4 MOYEN-ORIENT ET AFRIQUE

11.10.5 AMÉRIQUE DU SUD

11.11 ÉLECTRONIQUES ET APPLICATIONS DE L'AMÉRIQUE DU NORD (2500) SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

11.11.1 ASIE-PACIFIQUE

11.11.2 AMÉRIQUE DU NORD

11.11.3 EUROPE

11.11.4 MOYEN-ORIENT ET AFRIQUE

11.11.5 AMÉRIQUE DU SUD

11.12 AMÉRIQUE DU NORD AUTRES DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

11.12.1 ASIE-PACIFIQUE

11.12.2 AMÉRIQUE DU NORD

11.12.3 L'EUROPE

11.12.4 MOYEN-ORIENT ET AFRIQUE

11.12.5 AMÉRIQUE DU SUD

12 PALLETTES D'AMÉRIQUE DU NORD, PAR UTILISATION

12.1 Aperçu général

12.2 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR UTILISATION FINALE, 2018-2033

12.2.1 LOGISTIQUES ET PROVIDEURS 3PL

12.2.2 PLANTES DE FABRICATION

12.2.3 CENTRES DE DISTRIBUTION DE DÉTAILS

12.2.4 OPERATEURS DE CHAINES D'OLD

12.2.5 AUTRES

12.3 LOGISTIQUES DE L'AMÉRIQUE DU NORD ET PROVIDEURS DE 3PL SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLIERS USD)

12.3.1 ASIE-PACIFIQUE

12.3.2 AMÉRIQUE DU NORD

12.3.3 L'EUROPE

12.3.4 MOYEN-ORIENT ET AFRIQUE

12.3.5 AMÉRIQUE DU SUD

12.4 PLANTES DE FABRICATION DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

12.4.1 ASIE-PACIFIQUE

12.4.2 AMÉRIQUE DU NORD

12.4.3 L'EUROPE

12.4.4 MOYEN-ORIENT ET AFRIQUE

12.4.5 AMÉRIQUE DU SUD

12.5 CENTRAUX DE DISTRIBUTION DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

12.5.1 ASIE-PACIFIQUE

12.5.2 AMÉRIQUE DU NORD

12.5.3 EUROPE

12.5.4 MOYEN-ORIENT ET AFRIQUE

12.5.5 AMÉRIQUE DU SUD

12.6 OPÉRATEURS DE CHAIN D'OR DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

12.6.1 ASIE-PACIFIQUE

12.6.2 AMÉRIQUE DU NORD

12.6.3 EUROPE

12.6.4 MOYEN-ORIENT ET AFRIQUE

12.6.5 AMÉRIQUE DU SUD

12.7 AMÉRIQUE DU NORD AUTRES SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

12.7.1 ASIE-PACIFIQUE

12.7.2 AMÉRIQUE DU NORD

12.7.3 EUROPE

12.7.4 MOYEN-ORIENT ET AFRIQUE

12.7.5 AMÉRIQUE DU SUD

13 MARCHÉ DE L'EMBALLAGE DES PALLES D'AMÉRIQUE DU NORD, PAR CHANEAU DE DISTRIBUTION

13.1 Aperçu général

13.1.1 DIRECT

13.1.2 INDIRECT

13.2 DIRECT DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (en MILLE USD)

13.2.1 ÉLÉMENTS DE VENTE DE LA SOCIÉTÉ

13.2.2 CONTRATS DIRECTS D'OEM

13.2.3 SITES WEB D'ENTREPRISE

13.3 DIRECT DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

13.3.1 ASIE-PACIFIQUE

13.3.2 AMÉRIQUE DU NORD

13.3.3 L'EUROPE

13.3.4 MOYEN-ORIENT ET AFRIQUE

13.3.5 AMÉRIQUE DU SUD

13.4 INDIRECT DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS USD)

13.4.1 GÉNÉRAUX / DISTRIBUTEURS

13.4.2 CARACTÉRISTIQUES DE L'APPROVISIONNEMENT INDUSTRIEL

13.4.3 COMMERCE E DE TROISIÈME PARTIE

13.5 DIRECT DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLE US)

13.5.1 ASIE-PACIFIQUE

13.5.2 AMÉRIQUE DU NORD

13.5.3 EUROPE

13.5.4 MOYEN-ORIENT ET AFRIQUE

13.5.5 AMÉRIQUE DU SUD

14 MARCHÉ DE L'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR RÉGION

14.1 AMÉRIQUE DU NORD

14.1.1 États-Unis

14.1.2 CANADA

14.1.3 MEXIQUE

15 MARCHÉ DE L'EMBALLAGE DES PALLETS DE L'AMÉRIQUE DU NORD: PAYSAGE DES ENTREPRISES

15.1 ANALYSE DE PARTAGE DE LA COMPAGNIE FABRICANTE: MONDIALE

16 ANALYSE SWOT

17 PROFIL DE LA SOCIÉTÉ DE DISTRIBUTEUR

17.1 BUNZL AUSTRALIE ET NOUVELLE ZELANDE

17.1.1 COMPAGNIE

17.1.2 ANALYSE DES RECETTES

17.1.3 SOURCE: SITE WEB, RAPPORT ANNUEL, DÉPÔT SEC

17.1.4 PORTEFEUILLE DE PRODUITS

17.1.5 DÉVELOPPEMENT RÉCENT

17.2 COMPAGNIE FASTÉNALE

17.2.1 COMPAGNIE SNAPSHOT

17.2.2 ANALYSE DES RECETTES

17.2.3 PORTEFEUILLE DE PRODUITS

17.2.4 DÉVELOPPEMENT RÉCENT

17.3 ULINE

17.3.1 COMPAGNIE SNAPSHOT

17.3.2 PORTEFEUILLE DE PRODUITS/SERVICES

17.3.3 DÉVELOPPEMENT RÉCENT

17.4 Société d'exploitation VERITIV

17.4.1 COMPAGNIE SNAPSHOT

17.4.2 PORTEFEUILLE DE PRODUITS/SERVICES

17.4.3 DÉVELOPPEMENT RÉCENT

17.5 W.W. GRAINGER, INC.

17.5.1 COMPAGNIE SNAPSHOT

17.5.2 ANALYSE DES RECETTES

17.5.3 PORTEFEUILLE DE PRODUITS

17.5.4 DÉVELOPPEMENT RÉCENT

18 PROFIL DE LA COMPAGNIE FABRICANTE

18.1 ASIE DES PLASTIQUES SIGMA

18.1.1 COMPAGNIE SNAPSHOT

18.1.2 ANALYSE DU PARTAGE DES ENTREPRISES

18.1.3 PORTEFEUILLE DE PRODUITS

18.1.4 DÉVELOPPEMENT RÉCENT

18.2 IPL SCHOELLER.

18.2.1 COMPAGNIE SNAPSHOT

18.2.2 ANALYSE DU PARTAGE DES ENTREPRISES

18.2.3 PORTEFEUILLE DE PRODUITS

18.2.4 DÉVELOPPEMENT RÉCENT

18.3 NOVOLEX

18.3.1 COMPAGNIE SNAPSHOT

18.3.2 ANALYSE DU PARTAGE DES ENTREPRISES

18.3.3 PORTEFEUILLE DE PRODUITS

18.3.4 DÉVELOPPEMENT RÉCENT

18.4 CRAEMER GMBH.

18.4.1 COMPAGNIE SNAPSHOT

18.4.2 ANALYSE DU PARTAGE DES ENTREPRISES

18.4.3 PORTEFEUILLE DE PRODUITS

18.4.4 DÉVELOPPEMENT RÉCENT

18.5 PALLÉTONE

18.5.1 COMPAGNIE SNAPSHOT

18.5.2 ANALYSE DU PARTAGE DES ENTREPRISES

18.5.3 PORTEFEUILLE DE PRODUITS

18.5.4 DÉVELOPPEMENT RÉCENT

18.6 Groupe AETNA SPA

18.6.1 COMPAGNIE SNAPSHOT

18.6.2 PORTEFEUILLE DE PRODUITS

18.6.3 DÉVELOPPEMENT RÉCENT

18.7 BEKUPLAST SP. Z O. O.

18.7.1 COMPAGNIE SNAPSHOT

18.7.2 PORTEFEUILLE DE PRODUITS

18.7.3 DÉVELOPPEMENT RÉCENT

18.8 AVANTAGES.

18.8.1 COMPAGNIE SNAPSHOT

18.8.2 PORTEFEUILLE DE PRODUITS

18.8.3 DÉVELOPPEMENT RÉCENT

18.9 CONWED

18.9.1 COMPAGNIE SNAPSHOT

18.9.2 PORTEFEUILLE DE PRODUITS

18.9.3 DÉVELOPPEMENT RÉCENT

18.1 SYSTÈMES D' EMBALLAGE FROMM

18.10.1 COMPAGNIE SNAPSHOT

18.10.2 PORTEFEUILLE DE PRODUITS/SERVICES

18.10.3 DÉVELOPPEMENT RÉCENT

18.11 PALLETTES ET CONTENEURS D'AMÉRIQUE DU NORD.

18.11.1 COMPAGNIE SNAPSHOT

18.11.2 PORTEFEUILLE DE PRODUITS

18.11.3 DÉVELOPPEMENT RÉCENT

18.12 GREENDOT BIOPAK PVT. LTD.

18.12.1 COMPAGNIE SNAPSHOT

18.12.2 PORTEFEUILLE DE PRODUITS

18.12.3 DÉVELOPPEMENT RÉCENT

18.13 HEXAPAK

18.13.1 COMPAGNIE SNAPSHOT

18.13.2 PORTEFEUILLE DE PRODUITS/SERVICES

18.13.3 DÉVELOPPEMENT RÉCENT

18.14 FABRICATION PLASTIQUE HIVIQUE CO., LTD.

18.14.1 COMPAGNIE SNAPSHOT

18.14.2 PORTEFEUILLE DE PRODUITS/SERVICES

18.14.3 DÉVELOPPEMENT RÉCENT

18.15 GROUPE INTERTAPE POLYMER (IPG)

18.15.1 COMPAGNIE SNAPSHOT

18.15.2 PORTEFEUILLE DE PRODUITS/SERVICES

18.15.3 DÉVELOPPEMENT RÉCENT

18.16 LANTECH

18.16.1 COMPAGNIE SNAPSHOT

18.16.2 PORTEFEUILLE DE PRODUITS/SERVICES

18.16.3 DÉVELOPPEMENT RÉCENT

18.17 M STRETCH S.P.A.

18.17.1 COMPAGNIE SNAPSHOT

18.17.2 PORTEFEUILLE DE PRODUITS

18.17.3 DÉVELOPPEMENT RÉCENT

18.18 GROUPE DE MAILLIS

18.18.1 COMPAGNIE SNAPSHOT

18.18.2 PORTEFEUILLE DE PRODUITS/SERVICES

18.18.3 DÉVELOPPEMENT RÉCENT

18.19 EMBALLAGE DES MATÈRES

18.19.1 COMPAGNIE SNAPSHOT

18.19.2 PORTEFEUILLE DE PRODUITS

18.19.3 DÉVELOPPEMENT RÉCENT

18.2 MOSCA GMBH

18.20.1 COMPAGNIE SNAPSHOT

18.20.2 PORTEFEUILLE DE PRODUITS

18.20.3 DÉVELOPPEMENT RÉCENT

18.21 SYSTÈMES D'EMBALLAGE D'ORION LLC.

18.21.1 COMPAGNIE SNAPSHOT

18.21.2 PORTEFEUILLE DE PRODUITS

18.21.3 DÉVELOPPEMENT RÉCENT

18.22 FILMS DE PARAGON.

18.22.1 COMPAGNIE SNAPSHOT

18.22.2 PORTEFEUILLE DE PRODUITS

18.22.3 DÉVELOPPEMENT RÉCENT

18.23 POLYFAVO..

18.23.1 COMPAGNIE SNAPSHOT

18.23.2 PORTEFEUILLE DE PRODUITS

18.23.3 DÉVELOPPEMENT RÉCENT

18.24 POLYREFLEX HI-TECH CO., LTD .

18.24.1 COMPAGNIE SNAPSHOT

18.24.2 PORTEFEUILLE DE PRODUITS

18.24.3 DÉVELOPPEMENT RÉCENT

18.25 INDUSTRIE DE L'EMBALLAGE ROKSON

18.25.1 COMPAGNIE SNAPSHOT

18.25.2 PORTEFEUILLE DE PRODUITS

18.25.3 DÉVELOPPEMENT RÉCENT

18.26 TRANPAK INC.

18.26.1 COMPAGNIE SNAPSHOT

18.26.2 PORTEFEUILLE DE PRODUITS

18.26.3 DÉVELOPPEMENT RÉCENT

18.27 TRANSOPLAST

18.27.1 COMPAGNIE SNAPSHOT

18.27.2 PORTEFEUILLE DE PRODUITS

18.27.3 DÉVELOPPEMENT RÉCENT

18.28 TRIOWORLD

18.28.1 COMPAGNIE SNAPSHOT

18.28.2 PORTEFEUILLE DE PRODUITS

18,28.3 DÉVELOPPEMENT RÉCENT

18.29 UCMPL

18.29.1 COMPAGNIE SNAPSHOT

18.29.2 PORTEFEUILLE DE PRODUITS

18.29.3 DÉVELOPPEMENT RÉCENT

18.3 WULFTEC INTERNATIONAL INC

18.30.1 COMPAGNIE SNAPSHOT

18.30.2 PORTEFEUILLE DE PRODUITS/SERVICES

18.30.3 DÉVELOPPEMENT RÉCENT

19 QUESTIONNAIRE

20 RAPPORTS CONNEXES

Liste des tableaux

TABLEAU 1 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR TYPE DE PRODUITS, 2018-2033 (MILLIERS USD)

TABLEAU 2 FILMS D'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

TABLEAU 3 FILMS D'HOODAGE DE L'AMÉRIQUE DU NORD DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

TABLEAU 4 PALLET EURO DE L'AMÉRIQUE DU NORD DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 5 BOÎTES DE PALLET DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLIERS USD)

TABLEAU 6 LIMITES ET CAPES DE PALLET DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLIERS USD)

TABLEAU 7 FICHES DE SLIP D'AMÉRIQUE DU NORD ET FICHES DE TIER SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en milliers de dollars)

TABLEAU 8 GRAPHIQUE DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE DE MACHINE, 2018-2033 (en MILLIERS USD)

TABLEAU 9 GRAPHIQUE AUTOMATIQUE COMPLÈTE DE L'AMÉRIQUE DU NORD DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033

TABLEAU 10 GRAPHIQUE DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 11 HOODERS DE L'AMÉRIQUE DU NORD DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE DE MACHINE, 2018-2033 (en MILLIERS USD)

TABLEAU 12 AMERIQUE DU NORD HOODERS AUTOMATIQUES COMPLÈTS DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS USD)

TABLEAU 13 HOODERS DE L'AMÉRIQUE DU NORD DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 14 PALLET D'AMÉRIQUE DU NORD RÉSEAU SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DU PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 15 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR TYPE DE MACHINE, 2018-2033 (en MILLE)

TABLEAU 16 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (en MILLE USD)

TABLEAU 17 AUTOMATIQUE COMPLÈTE DE L'AMÉRIQUE DU NORD DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

TABLEAU 18 SÉMI AUTOMATIQUE DE L'AMÉRIQUE DU NORD DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 19 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR TYPE DE FONCTION, 2018-2033 (en MILLIERS USD)

TABLEAU 20 GRAPHIQUE DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLIERS USD)

TABLEAU 21 AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 22 PROTECTION DE L'AMÉRIQUE DU NORD ET CUSHIONAGE SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

TABLEAU 23 HOODAGE DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 24 AMÉRIQUE DU NORD AUTRES SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 25 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR DEMANDE, 2018-2033 (en MILLIERS USD)

TABLEAU 26 ALIMENTS ET BOISSONS DE L'AMÉRIQUE DU NORD (1000) SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en millions de dollars)

TABLEAU 27 DETAIL ET DE COMMERCE E-NORD-AMÉRIQUE DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 28 MARCHANDISES DE CONSOMMATION DE L'AMÉRIQUE DU NORD (GCP) (1000) SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 29 PHARMACEUTIQUES DE L'AMÉRIQUE DU NORD (2100) SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE PALLET, PAR RÉGION, 2018-2033 (en MILLE USD)

TABLEAU 30 CHIMIQUES DE L'AMÉRIQUE DU NORD (2000) SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 31 AGRICULTURE ET HORTICULTURE DE L'AMÉRIQUE DU NORD (0100) SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLIERS USD)

TABLEAU 32 FABRICATION INDUSTRIELLE DE L'AMÉRIQUE DU NORD (0001) SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (en MILLIERS USD)

TABLEAU 33 AMÉRIQUE DU NORD AUTOMOTIF (2900) SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 34 ÉLECTRONIQUES ET APPLICATIONS DE L'AMÉRIQUE DU NORD (2500) SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 35 AMÉRIQUE DU NORD AUTRES SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 36 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR UTILISATION FINALE, 2018-2033 (MILLIERS USD)

TABLEAU 37 LOGISTIQUES DE L'AMÉRIQUE DU NORD ET PROVIDEEURS DE 3PL SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 38 PLANTES DE FABRICATION DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 39 CENTRAUX DE DISTRIBUTION DE L'AMÉRIQUE DU NORD DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 40 OPÉRATEURS DE CHAINE D'OR DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE PALLET, PAR RÉGION, 2018-2033 (en MILLIERS USD)

TABLEAU 41 AMÉRIQUE DU NORD AUTRES SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE PALLET, PAR RÉGION, 2018-2033 (en MILLIERS USD)

TABLEAU 42 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR CHANEAU DE DISTRIBUTION, 2018-2033 (en MILLIERS USD)

TABLEAU 43 DIRECT D'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS USD)

TABLEAU 44 DIRECT DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 45 INDIRECT DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS USD)

TABLEAU 46 DIRECT DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR RÉGION, 2018-2033 (MILLIERS USD)

TABLEAU 47 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR PAYS, 2018-2033 (en MILLE USD)

TABLEAU 48 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR PAYS, 2018-2033 (MILLIERS USD)

TABLEAU 49 AMÉRIQUE DU NORD

TABLEAU 50 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR TYPE DE PRODUITS, 2018-2033 (MILLIERS USD)

TABLEAU 51 GRAPHIQUE DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE DE MACHINES, 2018-2033 (MILLIERS USD)

TABLEAU 52 GRAPHIQUE AUTOMATIQUE COMPLÈTE DE L'AMÉRIQUE DU NORD DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS USD)

TABLEAU 53 HOODERS DE L'AMÉRIQUE DU NORD DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE DE MACHINE, 2018-2033 (MILLIERS USD)

TABLEAU 54 AMERIQUE DU NORD HOODERS FULLY AUTOMATIC STRETCH DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS DE USD)

TABLEAU 55 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR TYPE DE MACHINE, 2018-2033 (en MILLEUR)

TABLEAU 56 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (en MILLE USD)

TABLEAU 57 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR TYPE DE FONCTION, 2018-2033 (MILLIERS USD)

TABLEAU 58 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR DEMANDE, 2018-2033 (MILLIERS USD)

TABLEAU 59 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE NORD, PAR UTILISATION FINALE, 2018-2033 (MILLIERS USD)

TABLEAU 60 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR CHANEAU DE DISTRIBUTION, 2018-2033 (en MILLIERS USD)

TABLEAU 61 DIRECT DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS USD)

TABLEAU 62 INDIRECT DE L'AMÉRIQUE DU NORD SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS USD)

TABLEAU 63 Marché américain des produits d'emballage en pâte, par type de produit, 2018-2033 (en milliers de dollars américains)

TABLEAU 64 WRAPPERS US STRETCH DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE DE MACHINE, 2018-2033 (MILLIERS USD)

TABLEAU 65 GRAPHIQUE AUTOMATIQUE COMPLÈTE DES ÉTATS-UNIS SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (en milliers de dollars)

TABLEAU 66 HOODERS DE STRETCH U.S. DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE DE MACHINE, 2018-2033 (MILLIERS DE USD)

TABLEAU 67 HOODERS AUTOMATIQUES COMPLÈTS DES ÉTATS-UNIS DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033

TABLEAU 68 Marché américain des produits d'emballage en pâte, par type de matière, 2018-2033 (en milliers de dollars É.-U.)

TABLEAU 69 U.S. FULLY AUTOMATIC DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE PALLET, PAR TYPE, 2018-2033 (en MILLIERS USD)

TABLEAU 70 Marché américain des produits d'emballage en pâte, par type de fonction, 2018-2033 (en milliers de dollars)

TABLEAU 71 Marché américain des produits d'emballage en pâte, par demande, 2018-2033

TABLEAU 72 Marché américain des produits d'emballage en pâte, par utilisation finale, 2018-2033 (en milliers de dollars É.-U.)

TABLEAU 73 Marché américain des produits d'emballage en pâte, par secteur, 2018-2033 (en millions de dollars)

TABLEAU 74 DIRECT U.S. SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS USD)

TABLEAU 75 INDIRECT DES ÉTATS-UNIS SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS USD)

TABLEAU 76 MARCHÉ CANADIEN DES PRODUITS D'EMBALLAGE PALLET, PAR TYPE DE PRODUITS, 2018-2033 (MILLIERS USD)

TABLEAU 77 PAR TYPE DE MACHINE, 2018-2033 (MILLE)

TABLEAU 78 GRAPHIQUE AUTOMATIQUE COMPLÈTE DU CANADA SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE PALLET, PAR TYPE, 2018-2033

TABLEAU 79 HOODERS DE CHAUSSURES DU CANADA SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE DE MACHINE, 2018-2033

TABLEAU 80 HOODERS FULLY AUTOMATIQUES DU CANADA DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS USD)

TABLEAU 81 MARCHÉ CANADIEN DES PRODUITS D'EMBALLAGE PALLET, PAR TYPE DE MACHINE, 2018-2033 (MILLIERS USD)

TABLEAU 82 MARCHÉ CANADIEN DES PRODUITS D'EMBALLAGE PALLET AUTOMATIQUE, PAR TYPE, 2018-2033

TABLEAU 83 MARCHÉ CANADIEN DES PRODUITS D'EMBALLAGE PALLET, PAR TYPE DE FONCTION, 2018-2033 (MILLIERS USD)

TABLEAU 84 MARCHÉ CANADIEN DES PRODUITS D'EMBALLAGE PALLET, PAR DEMANDE, 2018-2033 (MILLIERS USD)

TABLEAU 85 MARCHÉ CANADIEN DES PRODUITS D'EMBALLAGE PALLET, PAR UTILISATION FINALE, 2018-2033 (MILLIERS USD)

TABLEAU 86 MARCHÉ CANADIEN DES PRODUITS D'EMBALLAGE PALLET, PAR CHANEAU DE DISTRIBUTION, 2018-2033 (MILLIERS USD)

TABLEAU 87 DIRECT DU CANADA SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE PALLET, PAR TYPE, 2018-2033

TABLEAU 88 INDIRECT DU CANADA SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (en milliers de dollars)

TABLEAU 89 MARCHÉ DES PRODUITS D'EMBALLAGE MEXIQUE, PAR TYPE DE PRODUITS, 2018-2033 (MILLIERS USD)

TABLEAU 90 GRAPHIQUE MEXIQUE SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE DE MACHINE, 2018-2033 (en MILLIERS USD)

TABLEAU 91 GRAPHIQUE AUTOMATIQUE MEXIQUE COMPLÈTE DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS USD)

TABLEAU 92 HOODERS DE MEXIQUE DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE DE MACHINE, 2018-2033 (MILLIERS USD)

TABLEAU 93 MEXIQUE FULLY AUTOMATIC STRETCH HOODERS DANS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS USD)

TABLEAU 94 MARCHÉ DES PRODUITS D'EMBALLAGE MEXIQUE, PAR TYPE DE MACHINE, 2018-2033 (MILLIERS USD)

TABLEAU 95 MEXIQUE PLEIN AUTOMATIQUE SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS USD)

TABLEAU 96 MARCHÉ DES PRODUITS D'EMBALLAGE MEXIQUE, PAR TYPE DE FONCTION, 2018-2033 (MILLIERS USD)

TABLEAU 97 MARCHÉ MEXIQUE DE L'EMBALLAGE DES PRODUITS DE PALLET, PAR DEMANDE, 2018-2033

TABLEAU 98 MARCHÉ DES PRODUITS D'EMBALLAGE MEXIQUE, PAR UTILISATION FINALE, 2018-2033 (en milliers de dollars)

TABLEAU 99 MARCHÉ DES PRODUITS D'EMBALLAGE MEXIQUE, PAR CHANEAU DE DISTRIBUTION, 2018-2033 (MILLIERS USD)

TABLEAU 100 DIRECT MEXIQUE SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS USD)

TABLEAU 101 INDIRECT MEXIQUE SUR LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET, PAR TYPE, 2018-2033 (MILLIERS USD)

Liste des figures

FIGURE 1 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD: SEGMENTATION

FIGURE 2 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD: TRIANGULATION DES DONNÉES

FIGURE 3 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD: ANALYSE DES DROGUES

FIGURE 4 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD: ANALYSE DU MARCHÉ DES PAYS

FIGURE 5 MARCHÉ DE L'EMBALLAGE DES PRODUITS DE L'AMÉRIQUE DU NORD: ANALYSE DE LA RECHERCHE DES ENTREPRISES

GRAPHIQUE 6 MARCHÉ DES PRODUITS DE PALLET D'AMÉRIQUE DU NORD: DÉMOGRAPHIQUES INTERVIEW

FIGURE 7 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD: GRID DE POSITION DU MARCHÉ DU DBMR

FIGURE 8 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD: ANALYSE DU PARTAGE DES VENDEURS

FIGURE 9 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD: MODÈLE MULTIVARIVÉ

FIGURE 10 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD: COURS DE TYPE

FIGURE 11 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD: GRID DE COUVERTURE VERTIQUE

FIGURE 12 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD: SEGMENTATION

FIGURE 13 SEPT SEGMENTS COMPRIS LE MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, PAR TYPE DE PRODUITS (2025)

FIGURE 14 MARCHÉ DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD: RÉSUMÉ

FIGURE 15 DÉCISIONS STRATÉGIQUES

FIGURE 16 EXPANSION DE LA FABRICATION DE L'AMÉRIQUE DU NORD, CROISSANCE DE LOGISTIQUES ORGANISÉES, CHARGEMENT UNITIS ET ADOPTION D'EMBALLAGES DE TRANSPORT RÉUSSIBLES SONT EN VIGUEUR POUR CONDUIRE LE MARCHÉ DES PRODUITS D'AMÉRIQUE DU NORD POUR LA PÉRIODE 2026-2033

FIGURE 17 FILMS STRETCH EST EXPRIMÉ À COMPTER DE LA PLUS GRANDE PART DU MARCHÉ DES PRODUITS D'AMÉRIQUE DU NORD EN 2026 ET 2033

FIGURE 18 MARCHÉS DES PRODUITS D'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD, 2025-2033, PRIX DE VENTE MOYEN (USD/PER ROLL)

FIGURE 19 ÉCHANTILLONS, RESTRINTS, OBLIGATIONS ET DÉFIS DU MARCHÉ DE L'AMÉRIQUE DU NORD

FIGURE 20 MARCHÉ DE L'EMBALLAGE DES PALLETTES D'AMÉRIQUE DU NORD: PAR TYPE DE PRODUITS, 2025

FIGURE 21 MARCHÉ DE L'EMBALLAGE DES PALLETTES D'AMÉRIQUE DU NORD: PAR TYPE DE MACHINE, 2025

FIGURE 22 MARCHÉ DE L'EMBALLAGE DES PALLETTES D'AMÉRIQUE DU NORD: PAR TYPE DE FONCTION, 2025

FIGURE 23 MARCHÉ DE L'EMBALLAGE DES PALLETTES D'AMÉRIQUE DU NORD: PAR DEMANDE, 2025

FIGURE 24 MARCHÉ DE L'EMBALLAGE DES PALLETTES D'AMÉRIQUE DU NORD: PAR UTILISATION, 2025

FIGURE 25 MARCHÉ DE L'EMBALLAGE DES PALLES D'AMÉRIQUE DU NORD: PAR CHANEAU DE DISTRIBUTION , 2025

FIGURE 26 MARCHÉ DE L'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD: SNAPSHOT (2026)

FIGURE 27 MARCHÉ DE L'EMBALLAGE DE PALLET D'AMÉRIQUE DU NORD: PARTAGE DE L'ENTREPRISE 2025 (%)

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.