North America Pallet Packaging Products Market

Market Size in USD Billion

USD

4.49 Billion

USD

6.79 Billion

2025

2033

USD

4.49 Billion

USD

6.79 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.49 Billion | |

| USD 6.79 Billion | |

| % | |

|

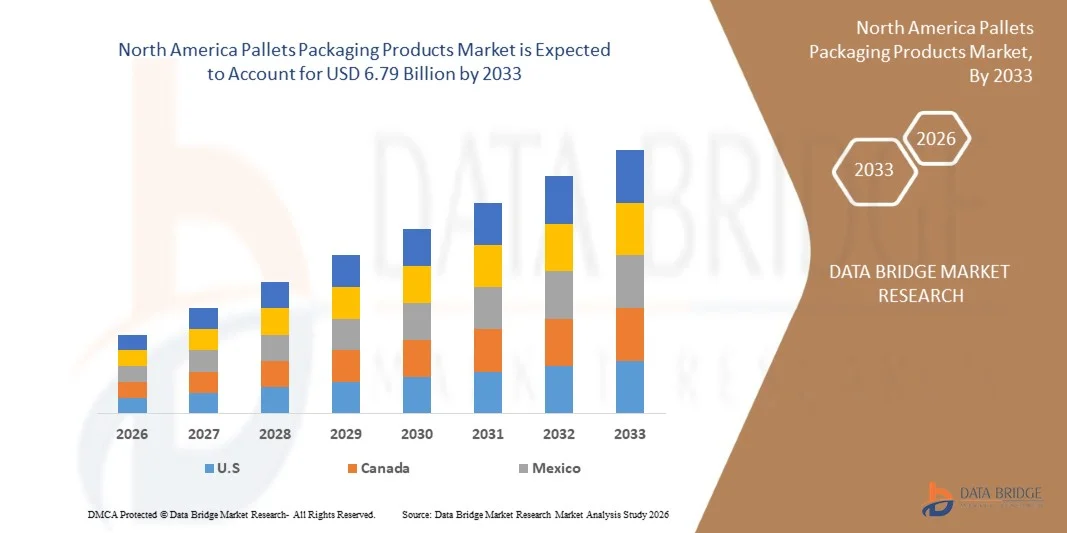

North America Pallets Packaging Products Market size

- The North America pallets packaging products market is expected to reach USD 6.79 Billion by 2033 from USD 4.49 Billion in 2025, growing with a substantial CAGR of 5.4% in the forecast period of 2026 to 2033

- The North America pallet packaging products market is experiencing steady and resilient growth, supported by strong industrial output, continuous expansion of warehousing and distribution infrastructure, and widespread adoption of standardized pallet systems across key sectors including food & beverages, pharmaceuticals, chemicals, manufacturing, retail, and fast-moving consumer goods. Rising cross-border trade between the U.S., Canada, and Mexico, along with the rapid expansion of e-commerce and omnichannel retail, is driving sustained demand for efficient, durable, and high-load pallet packaging solutions.

- Market expansion is further reinforced by sustainability-driven regulations and corporate ESG commitments, leading to increased adoption of recyclable, reusable, and lightweight pallet materials such as plastic, composite, and engineered wood. Heightened focus on worker safety, load stability, and damage reduction during automated and manual material handling is accelerating the use of high-performance pallet designs. In addition, investments in warehouse automation, robotic handling systems, and smart pallets with tracking capabilities are improving supply chain efficiency and supporting long-term growth of the pallet packaging products market across North America.

North America Pallets Packaging Products Market Analysis

- Pallets packaging is becoming increasingly critical across North America’s logistics and industrial ecosystems, enabling safe, efficient, and standardized handling of goods across warehousing, transportation, and distribution operations. Pallets enhance load stability, reduce product damage, and improve material-handling efficiency across key sectors such as manufacturing, food & beverages, pharmaceuticals, chemicals, construction, and retail.

- Expanding industrial production, rapid growth of e-commerce, and increasing warehouse automation across North America are fueling strong demand for pallet packaging solutions. Industries are increasingly adopting advanced pallet wrapping and stabilization systems to improve supply chain efficiency, reduce manual labor, and meet rising throughput requirements.

- Additionally, stringent regulatory standards related to worker safety, packaging waste reduction, and sustainability are accelerating the adoption of recyclable and lightweight pallet packaging materials. Companies are increasingly investing in eco-friendly pallets and recyclable stretch films to comply with EU environmental directives and corporate sustainability goals.

- U.S. is projected to lead the North America pallets packaging products market in 2025, accounting for 76.41% of the regional market share. This dominance is supported by the country’s strong manufacturing base, advanced logistics infrastructure, high adoption of automation in warehouses, and strict workplace safety regulations. Government initiatives promoting sustainable packaging and efficient supply chains further reinforce Germany’s leadership position within the North American market.

- The Stretch Films segment is expected to dominate the North America pallets packaging products market in 2026 with market share of 23.04%, driven by its cost-effectiveness, flexibility, strong load containment, and ease of application. Stretch films are widely used to secure palletized goods during storage and transit, particularly in high-volume logistics and automated warehousing environments, making them essential for ensuring product integrity and minimizing losses.

Report Scope and North America Pallets Packaging Products Market Segmentation

|

Attributes |

North America Pallets Packaging Products Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Pallets Packaging Products Market Trends

“Growing Adoption of Pallets Packaging Products Across North American Logistics and Industrial Operations”

- The steady expansion of manufacturing, warehousing, and logistics activities across North America is a major factor driving the adoption of pallet packaging solutions. As cross-border trade, e-commerce fulfillment, and industrial distribution networks continue to scale, companies increasingly rely on pallets packaging to ensure safe, efficient, and cost-effective handling of goods across complex supply chains and high-volume transportation corridors.

- Pallets packaging plays a critical role in protecting goods and ensuring operational continuity throughout storage and transportation processes. By enabling stable unit loads, minimizing product damage, and improving handling efficiency, pallets packaging reduces risks associated with manual handling while supporting uninterrupted operations across warehouses, distribution centers, manufacturing plants, and retail supply networks.

- The growing use of advanced logistics operations, including automated warehousing, high-bay storage systems, and just-in-time delivery models, has increased demand for high-performance pallet packaging solutions. Innovations in stretch films, pallet boxes, lids, and securing systems enhance load stability, safety, and efficiency under demanding logistics and transportation conditions.

- North American countries with strong industrial bases and logistics hubs—such as U.S., Canada, Mexico—are driving widespread adoption of pallet packaging solutions. Strict workplace safety regulations, sustainability mandates, and the need to optimize transportation efficiency are encouraging industries to adopt standardized, durable, and recyclable pallet packaging systems.

- Overall, the expanding scale of North America’s industrial production, trade, and logistics operations positions pallets packaging as an essential component of modern supply chain strategy. Pallet packaging supports product safety, operational efficiency, regulatory compliance, and sustainable growth across North America’s evolving manufacturing and distribution landscape.

North America Pallets Packaging Products Market Dynamics

Driver

“Growth of Organized Logistics, Warehousing, and Distribution Networks”

- The growth of organized logistics, warehousing, and distribution networks is boosting global demand for pallet packaging, as supply chains move from fragmented storage to centralized warehouses, large distribution centers, and professionally managed 3PL facilities.

- Pallets serve as the backbone of these modern logistics environments, enabling efficient stacking, racking, mechanized handling, and high-throughput order fulfillment, improving turnaround times and inventory control.

- Expansion of warehousing and distribution infrastructure, driven by e-commerce and 3PL operations, has increased pallet usage for easier consolidation, movement, and storage of goods across domestic and international supply chains.

- With industries increasingly relying on standardized material handling in centralized and mechanized logistics hubs, pallets remain an essential and foundational asset, ensuring sustained and predictable demand in modern supply chains.

Restraint/Challenge

“ Volatility in Raw Material Availability and Pricing”

- The volatility in raw material availability and pricing is a significant restraint affecting the pallets packaging market. Pallet production relies heavily on key materials such as timber, plastics, and recycled polymers, whose supply and costs are subject to fluctuations due to factors like seasonal timber shortages, changes in resin production, global trade dynamics, and inflationary pressures. Such unpredictability not only increases manufacturing costs but also affects procurement planning, pricing stability, and supply chain continuity for end users. As a result, manufacturers and logistics providers face challenges in maintaining consistent pallet quality, availability, and affordability, making raw material volatility a critical factor limiting market growth.

For instance,

- As noted by Packaging News UK indices in May 2025, procurement of specific pallet wood sizes has become more challenging for manufacturers alongside rising timber prices, indicating raw material availability issues that complicate production planning and cost stability.

- As highlighted by Global Wood in July 2024, pallet manufacturers in the UK and Ireland are facing “significant increases” in the cost of raw wood materials due to limited log availability, increased prices from overseas mills, and lower volumes of imported timber, leading to raw material cost volatility for pallets.

- In conclusion, volatility in raw material availability and pricing remains a critical restraint for the pallets packaging market. Fluctuations in timber, plastics, and recycled polymer costs—driven by supply shortages, trade dynamics, and production constraints—directly impact manufacturing expenses, pallet pricing, and procurement planning. This unpredictability challenges manufacturers in maintaining consistent product availability, cost control, and quality standards. As a result, raw material volatility not only limits market growth but also compels pallet producers and end users to adopt strategic sourcing, alternative materials, and efficient inventory management to mitigate risk and sustain supply chain continuity.

North America Pallets Packaging Products Market Scope

The North America pallets packaging products market is segmented into six notable segments based on the product type, machine type, function type, application, end use, and distribution channel.

- By product type

On the basis of product type, the market is segmented into stretch films, shrink hood films, euro pallets, pallet boxes, pallet lids & caps, slip sheets & tier sheets, stretch wrappers, stretch hooders, and pallet netting. In 2026, the stretch films segment is projected to dominate the global pallets packaging products market with the largest market share of 23.04%, due to their superior load stability, high stretchability, puncture resistance, and cost-effectiveness in securing palletized goods during storage and transportation. Stretch films are extensively used across food & beverage, pharmaceuticals, chemicals, and consumer goods industries to prevent load shifting, moisture ingress, and contamination. Additionally, their compatibility with both manual and automated pallet wrapping systems, along with growing demand for recyclable and downgauged films, further supports segment growth.

The stretch films segment is projected to grow at a CAGR of 5.9%, driven by rising warehouse automation, demand for lightweight and recyclable packaging, and widespread use across North American logistics, food, and pharmaceutical industries..

- By machine type

On the basis of machine type, the market is segmented into fully automatic and semi-automatic systems. In 2026, the fully automatic segment is projected to dominate the global pallets packaging products market with a market share of 64.78%, due to its ability to handle high-throughput palletizing operations with consistent wrapping quality, reduced labour dependency, and enhanced operational efficiency. Fully automatic pallet packaging systems are widely adopted in large-scale manufacturing and distribution facilities to minimize downtime, improve worker safety, and ensure uniform load containment. Integration with conveyor systems, robotics, PLC controls, and Industry 4.0-enabled monitoring further accelerates adoption among high-volume end users.

The fully automatic segment is expected to register a CAGR of 5.3%, supported by increasing automation in warehouses, labor cost optimization, and adoption of Industry 4.0-enabled pallet packaging systems across North America.

- By function type

On the basis of function type, the market is segmented into wrapping, strapping, protection & cushioning, hooding, and others. In 2026, the wrapping segment is projected to dominate the global pallets packaging products market with a market share of 45.41%, driven by its critical role in stabilizing pallet loads, protecting goods from dust, moisture, and mechanical damage, and enabling safe long-distance transportation. Wrapping solutions such as stretch and shrink wrapping are widely used across logistics, food & beverage, and industrial manufacturing due to their versatility, ease of application, and compatibility with various pallet sizes. Increasing emphasis on supply chain efficiency and damage reduction further contributes to the segment’s expansion.

The wrapping segment is projected to grow at a CAGR of 5.7%, driven by increasing focus on load stability, damage reduction, and efficient palletized transport within North American supply chains.

- By application

On the basis of application, the market is segmented into food & beverages, retail & e-commerce, consumer packaged goods (CPG), pharmaceuticals, chemicals, agriculture & horticulture, industrial manufacturing, automotive, electronics & appliances, and others. In 2026, the food & beverages segment is projected to dominate the global pallets packaging products market with the largest market share of 20.50%, owing to the high volume of palletized movement of packaged foods, beverages, and bulk consumables requiring secure, hygienic, and damage-resistant packaging solutions. Pallet packaging ensures product integrity during cold chain storage, warehousing, and long-haul transportation. The rising demand for packaged and ready-to-consume food products, along with stringent food safety and handling regulations, continues to drive adoption within this segment.

The food & beverages segment is expected to grow at a CAGR of 6.2%, driven by expansion of cold chain logistics, high consumption of packaged foods, and strict food safety regulations across North America.

- By end use

On the basis of end Use, the market is segmented into logistics & 3PL providers, manufacturing plants, retail distribution centers, cold chain operators, and others. In 2026, the logistics & 3PL providers segment is projected to dominate the global pallets packaging products market with the largest market share of 38.96%, due to the extensive handling, consolidation, and redistribution of palletized goods across multiple industries. Logistics providers rely heavily on pallet packaging solutions to ensure load stability, reduce transit damage, and improve warehouse efficiency. The rapid growth of e-commerce, cross-border trade, and third-party warehousing services further increases demand for reliable and scalable pallet packaging products.

The logistics & 3PL providers segment is projected to grow at a CAGR of 5.9%, driven by e-commerce growth, expansion of third-party logistics services, and increased cross-border trade within North America.

- By distribution channel

On the basis of distribution channel, the market is classified into direct and indirect channels. The direct channel is further segmented into company sales teams, direct OEM contracts, and company-owned websites, while the indirect channel is further segmented into wholesalers/distributors, industrial supply stores, and third-party e-commerce. In 2026, the direct segment is expected to dominate the global pallets packaging products market with a market share of 57.35%, due to strong preference among large industrial buyers for direct procurement from manufacturers to ensure customized solutions, bulk pricing advantages, and technical support. Direct channels enable end users to access tailored pallet packaging systems, long-term supply contracts, and after-sales services. Additionally, growing adoption of direct OEM relationships and manufacturer-led digital sales platforms strengthens the dominance of this segment.

The direct segment is expected to grow at a CAGR of 5.6%, supported by preference for direct manufacturer sourcing, customized solutions, and long-term supply agreements among North American industrial buyers

North America Pallets Packaging Products Market Regional Analysis

- The U.S. represents the largest and most influential market for pallet packaging products in North America, supported by its extensive manufacturing base, high domestic consumption, and one of the world’s most advanced logistics and warehousing infrastructures. Strong interstate and cross-border trade flows, widespread adoption of automated material-handling systems, and large-scale distribution networks for retail, food & beverages, pharmaceuticals, and industrial goods continue to drive consistent demand for pallet packaging across the country.

- Canada is witnessing steady growth in pallet packaging adoption, driven by expanding e-commerce activity, growth in third-party logistics services, and increasing cross-border trade with the United States. Investments in modern distribution centers, cold chain logistics, and sustainable packaging practices are accelerating demand for standardized, durable, and reusable pallets across food processing, chemicals, pharmaceuticals, and retail sectors.

- Mexico is emerging as a high-growth market for pallet packaging in North America, supported by expanding manufacturing activities, strong integration into North American supply chains, and rising exports of automotive, electronics, and consumer goods. Growth in industrial parks, logistics hubs, and nearshoring-driven manufacturing investments is increasing demand for cost-effective and robust pallet packaging solutions, positioning pallets as a critical component of efficient material handling and export-oriented supply chains in the country.

U.S. North America Pallets Packaging Products Market Insight

The U.S. pallets packaging products market is witnessing strong and sustained growth, driven by high-volume industrial output, a vast consumer base, and one of the most advanced logistics and warehousing infrastructures globally. Leadership in food & beverages, pharmaceuticals, chemicals, manufacturing, and retail distribution is generating consistent demand for standardized palletized transport, stretch wrapping, and automated pallet packaging systems. In addition, the widespread adoption of warehouse automation, robotics, and high-throughput fulfillment centers—particularly supporting e-commerce and omnichannel retail—is accelerating demand for durable, load-stable, and safety-compliant pallet packaging solutions, positioning the U.S. as the largest contributor to the North American market.

Canada North America Pallets Packaging Products Market Insight

The Canada pallets packaging products market is expanding steadily, supported by growing cross-border trade with the United States, increasing investment in modern warehousing infrastructure, and rising adoption of palletized storage and transportation systems across food processing, retail, pharmaceuticals, and industrial manufacturing sectors. Strong focus on supply chain efficiency, cold-chain logistics, and damage reduction during transportation is reinforcing demand for high-quality pallet packaging. Furthermore, Canada’s emphasis on sustainability, including reusable pallet systems and recyclable packaging materials, is encouraging businesses to upgrade pallet packaging solutions, supporting long-term market growth.

North America Pallets Packaging Products Market Share

The Pallets Packaging products industry is primarily led by well-established companies, including:

- Sigma Plastics Asia (Singapore)

- IPL Schoeller (Ireland)

- Novolex (U.S.)

- Craemer GmbH (Germany)

- PalletOne (U.S.)

- Aetna Group S.p.A. (Italy)

- Bekuplast sp. z o.o. (Poland)

- Benoplast (France)

- Conwed (U.S.)

- Fromm Packaging Systems (Switzerland)

- Global Pallets and Containers (U.S.)

- Greendot Biopak Pvt. Ltd. (India)

- Hexapak (India)

- Hivic Plastic Manufacture Co., Ltd. (China

- Intertape Polymer Group (Canada)

- Lantech (U.S.)

- M Stretch S.p.A. (Italy)

- Maillis Group (France)

- Matere Packaging (Italy)

- Mosca GmbH (Germany)

- Orion Packaging Systems LLC (U.S.)

- Paragon Films (U.S.)

- Polyfavo (India)

- Polyreflex Hi-Tech Co., Ltd. (India)

- Rokson Packaging Industry (India)

- TranPak Inc. (U.S.)

- Transoplast (Netherlands)

- Trioworld (Sweden)

- UCMPL (India)

- Wulftec International Inc. (Canada)

- Bunzl Australia & New Zealand (Australia)

- Fastenal Company (U.S.)

- Uline (U.S.)

- Veritiv Operating Company (U.S.)

- W.W. Grainger, Inc. (U.S.)

Latest Developments in the North America Pallets Packaging Products Market

- December, 2025 – Lantech introduced its next-generation semi-automatic stretch wrappers, the SL400 and SL400LT, designed to address labor shortages and improve pallet wrapping efficiency. These machines feature advanced automation, reduced operator touchpoints, and enhanced load-stability technologies.

- In February 2025, Sigma Plastics Group, along with its affiliate Mercury Plastics, acquired the assets of California-based Sun Plastics, Inc., marking Sigma’s 43rd acquisition and expanding its global operations to 49 locations. Sun Plastics, founded in 1979, specializes in high-quality, custom, 100% recyclable LDPE bags and films for diverse sectors including food, medical, electronics, and industrial markets. The acquisition strengthens Sigma’s presence in North America and enhances its capabilities in value-added, sustainable packaging solutions. This strategic move will provide Sigma with expanded market reach, advanced production expertise, and new growth opportunities.

- In May 2025, Transoplast Group and Schoeller Allibert launched a Platinum Partnership, with Transoplast becoming the main distributor for Schoeller Allibert products. This collaboration aims to deliver innovative, sustainable logistics solutions across industries, enhancing efficiency and supply chain performance. Transoplast will expand its inventory at a 25,000 m² logistics center, enabling faster delivery, customisation, and access to high-quality Schoeller Allibert products even for small orders. The partnership strengthens customer-centric solutions through personalised and scalable packaging options.

- In October 2025, the European Commission granted a full exemption for pallet wrapping and straps from the 100% reuse targets under Articles 29(2) and (3) of the Packaging and Packaging Waste Regulation (PPWR). However, the 40% reuse target for cross-border transport packaging under Article 29(1) is still under consideration. This exemption allows companies like Trioworld to continue producing and supplying high-performance pallet films without immediate regulatory changes, ensuring operational stability and supporting ongoing innovation in sustainable packaging solutions.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATIONS

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 YEARS CONSIDERED FOR THE STUDY

2.3 DBMR TRIPOD DATA VALIDATION MODEL

2.4 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.5 DBMR MARKET POSITION GRID

2.6 VENDOR SHARE ANALYSIS

2.7 MULTIVARIATE MODELING

2.8 OFFERING TIMELINE CURVE

2.9 MARKET VERTICAL COVERAGE GRID

2.1 SECONDARY SOURCES

2.11 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PORTER’S FIVE FORCES ANALYSIS

4.1.1 INTENSITY OF COMPETITIVE RIVALRY

4.1.2 BARGAINING POWER OF BUYERS / CONSUMERS

4.1.3 THREAT OF NEW ENTRANTS

4.1.4 THREAT OF SUBSTITUTE PRODUCTS

4.1.5 BARGAINING POWER OF SUPPLIERS

4.1.6 CONCLUSION

4.2 PRICING ANALYSIS

4.3 VALUE CHAIN ANALYSIS

4.3.1 RAW MATERIAL AND FEEDSTOCK SUPPLY

4.3.2 MANUFACTURING AND PROCESSING

4.3.3 DISTRIBUTION AND LOGISTICS INTEGRATION

4.3.4 END-USE INDUSTRIES AND SALES CHANNELS

4.3.5 CONCLUSION

4.4 SUPPLY CHAIN ANALYSIS

4.4.1 RAW MATERIAL SOURCING & PROCUREMENT

4.4.2 PROCESSING & PRODUCT MANUFACTURING (PRODUCTION)

4.4.3 SUPPLY CHAIN & DISTRIBUTION LOGISTICS (TRANSPORTATION)

4.4.4 RETAIL & COMMERCIAL BUYER CHANNELS (DISTRIBUTION & SALES)

4.4.5 CONCLUSION

4.5 VENDOR SELECTION CRITERIA

4.5.1 PRODUCT QUALITY & COMPLIANCE

4.5.2 PRODUCT RANGE & CUSTOMIZATION

4.5.3 PRICING & TOTAL COST OF OWNERSHIP

4.5.4 SUPPLY CHAIN RELIABILITY

4.5.5 TECHNICAL SUPPORT & SERVICE

4.5.6 SUSTAINABILITY & ENVIRONMENTAL PRACTICES

4.5.7 VENDOR REPUTATION & FINANCIAL STABILITY

4.5.8 INNOVATION & TECHNOLOGY INTEGRATION

4.5.9 RISK & COMPLIANCE ASSESSMENT

4.5.10 PARTNERSHIP & STRATEGIC FIT

4.6 TECHNOLOGICAL ADVANCEMENTS

4.6.1 SUSTAINABLE MATERIAL INNOVATION

4.6.2 AUTOMATION & ROBOTICS IN PALLET PACKAGING

4.6.2.1 Integration with Robotics and Automated Lines:

4.6.2.2 Advanced Machine Controls & Interfaces:

4.6.3 SMART PACKAGING & IOT INTEGRATION

4.6.4 EFFICIENCY & WASTE REDUCTION TECHNOLOGIES

4.6.5 SUPPORTING SUSTAINABILITY THROUGH INNOVATION

4.7 INNOVATION TRACKER AND STRATEGIC ANALYSIS

4.7.1 MAJOR DEALS AND STRATEGIC ALLIANCES ANALYSIS

4.7.2 ACTIVE DEVELOPMENT

4.7.3 STAGE OF DEVELOPMENT

4.7.4 TIMELINES AND MILESTONES

4.7.5 INNOVATION STRATEGIES AND METHODOLOGIES

4.7.6 RISK ASSESSMENT AND MITIGATION

4.7.7 FUTURE OUTLOOK

4.8 CLIMATE CHANGE SCENARIO

4.8.1 TRANSFORMATION OF RAW MATERIAL SOURCING

4.8.2 CARBON FOOTPRINT ACCOUNTABILITY ACROSS THE PALLET LIFECYCLE

4.8.3 INFLUENCE OF CLIMATE VOLATILITY ON PALLET PERFORMANCE AND DESIGN

4.8.4 REGULATORY AND POLICY ALIGNMENT WITH CLIMATE COMMITMENTS

4.8.5 CLIMATE CHANGE AS A CATALYST FOR INNOVATION AND STRATEGIC REPOSITIONING

4.9 INDUSTRY ECOSYSTEM ANALYSIS

4.9.1 PROMINENT COMPANIES

4.9.2 SMALL AND MEDIUM SIZE COMPANIES

4.9.3 END USERS

5 TARIFFS & IMPACT ON THE MARKET

5.1 CURRENT TARIFF RATE (S) IN TOP-5 COUNTRY MARKETS

5.1.1 UNITED STATES (MAJOR IMPORTER OF PALLET PACKAGING):

5.1.2 CHINA (MAJOR PRODUCER & EXPORTER)

5.1.3 INDIA

5.1.4 EUROPEAN UNION

5.1.5 BRAZIL

5.2 OUTLOOK: LOCAL PRODUCTION VS IMPORT RELIANCE

5.3 VENDOR SELECTION CRITERIA DYNAMICS

5.4 IMPACT ON SUPPLY CHAIN

5.4.1 RAW MATERIAL PROCUREMENT:

5.4.2 MANUFACTURING AND PRODUCTION:

5.4.3 LOGISTICS AND DISTRIBUTION:

5.4.4 PRICE PITCHING AND POSITION IN MARKET:

5.5 INDUSTRY PARTICIPANTS: PROACTIVE MOVES

5.5.1 SUPPLY CHAIN OPTIMIZATION

5.5.2 JOINT VENTURE ESTABLISHMENTS

5.6 IMPACT ON PRICES

5.7 REGULATORY INCLINATION

5.7.1 GEOPOLITICAL SITUATION

5.7.2 TRADE PARTNERSHIPS BETWEEN COUNTRIES

5.7.2.1 FREE TRADE AGREEMENTS

5.7.2.2 ALLIANCES ESTABLISHMENTS

5.7.3 STATUS ACCREDITATION (INCLUDING MFTN)

5.7.4 DOMESTIC COURSE OF CORRECTION

5.7.4.1 INCENTIVE SCHEMES TO BOOST PRODUCTION OUTPUTS

5.7.4.2 ESTABLISHMENT OF SEZs/INDUSTRIAL PARKS

6 REGULATION COVERAGE

6.1 PRODUCT CODES

6.2 CERTIFIED STANDARDS

6.3 SAFETY STANDARDS

6.3.1 MATERIAL HANDLING & STORAGE

6.3.2 TRANSPORT & PRECAUTIONS

6.3.3 HAZARD IDENTIFICATION

7 MARKET OVERVIEW

7.1 DRIVERS

7.1.1 EXPANSION OF NORTH AMERICA MANUFACTURING AND INDUSTRIAL OUTPUT.

7.1.2 GROWTH OF ORGANIZED LOGISTICS, WAREHOUSING, AND DISTRIBUTION NETWORKS.

7.1.3 INCREASING PREFERENCE FOR UNITIZED LOAD HANDLING.

7.1.4 RISING ADOPTION OF REUSABLE AND RETURNABLE TRANSPORT PACKAGING (RTP).

7.2 RESTRAINTS

7.2.1 VOLATILITY IN RAW MATERIAL AVAILABILITY AND PRICING

7.2.2 LIMITED STANDARDIZATION ACROSS REGIONS AND END-USE INDUSTRIES .

7.3 OPPORTUNITY

7.3.1 SHIFT TOWARD PLASTIC AND COMPOSITE PALLETS IN REGULATED INDUSTRIES

7.3.2 INTEGRATION OF TRACKING AND IDENTIFICATION TECHNOLOGIES .

7.3.3 RISING DEMAND FROM EMERGING ECONOMIES’ EXPORT-ORIENTED SECTORS

7.4 CHALLENGES

7.4.1 HIGH REPAIR, REVERSE LOGISTICS, AND ASSET RECOVERY COSTS

7.4.2 ENVIRONMENTAL AND DISPOSAL CONCERNS FOR END-OF-LIFE PALLETS

8 NORTH AMERICA PALLETS PACKAGING MARKET, BY PRODUCT TYPE

8.1 OVERVIEW

8.2 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

8.2.1 STRETCH FILMS

8.2.2 SHRINK HOOD FILMS

8.2.3 EURO PALLET

8.2.4 PALLET BOXES

8.2.5 PALLET LIDS & CAPS

8.2.6 SLIP SHEETS & TIER SHEETS

8.2.7 STRETCH WRAPPERS

8.2.8 STRETCH HOODERS

8.2.9 PALLET NETTING

8.3 NORTH AMERICA STRETCH FILMS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.3.1 ASIA-PACIFIC

8.3.2 NORTH AMERICA

8.3.3 EUROPE

8.3.4 MIDDLE EAST AND AFRICA

8.3.5 SOUTH AMERICA

8.4 NORTH AMERICA SHRINK HOOD FILMS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.4.1 ASIA-PACIFIC

8.4.2 NORTH AMERICA

8.4.3 EUROPE

8.4.4 MIDDLE EAST AND AFRICA

8.4.5 SOUTH AMERICA

8.5 NORTH AMERICA EURO PALLET IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.5.1 ASIA-PACIFIC

8.5.2 NORTH AMERICA

8.5.3 EUROPE

8.5.4 MIDDLE EAST AND AFRICA

8.5.5 SOUTH AMERICA

8.6 NORTH AMERICA PALLET BOXES IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.6.1 ASIA-PACIFIC

8.6.2 NORTH AMERICA

8.6.3 EUROPE

8.6.4 MIDDLE EAST AND AFRICA

8.6.5 SOUTH AMERICA

8.7 NORTH AMERICA PALLET LIDS & CAPS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.7.1 ASIA-PACIFIC

8.7.2 NORTH AMERICA

8.7.3 EUROPE

8.7.4 MIDDLE EAST AND AFRICA

8.7.5 SOUTH AMERICA

8.8 NORTH AMERICA SLIP SHEETS & TIER SHEETS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.8.1 ASIA-PACIFIC

8.8.2 NORTH AMERICA

8.8.3 EUROPE

8.8.4 MIDDLE EAST AND AFRICA

8.8.5 SOUTH AMERICA

8.9 NORTH AMERICA STRETCH WRAPPERS IN PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

8.9.1 FULLY AUTOMATIC

8.9.2 SEMI AUTOMATIC

8.1 NORTH AMERICA FULLY AUTOMATIC STRETCH WRAPPERS IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.10.1 INLINE WRAPPING SYSTEMS

8.10.2 MONOBLOC WRAPPING SYSTEMS

8.11 NORTH AMERICA STRETCH WRAPPERS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.11.1 ASIA-PACIFIC

8.11.2 NORTH AMERICA

8.11.3 EUROPE

8.11.4 MIDDLE EAST AND AFRICA

8.11.5 SOUTH AMERICA

8.12 NORTH AMERICA STRETCH HOODERS IN PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

8.12.1 FULLY AUTOMATIC

8.12.2 SEMI AUTOMATIC

8.13 NORTH AMERICA FULLY AUTOMATIC STRETCH HOODERS IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.13.1 INLINE HOODING SYSTEMS

8.13.2 MONOBLOC HOODING SYSTEMS

8.14 NORTH AMERICA STRETCH HOODERS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.14.1 ASIA-PACIFIC

8.14.2 NORTH AMERICA

8.14.3 EUROPE

8.14.4 MIDDLE EAST AND AFRICA

8.14.5 SOUTH AMERICA

8.15 NORTH AMERICA PALLET NETTING IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.15.1 ASIA-PACIFIC

8.15.2 NORTH AMERICA

8.15.3 EUROPE

8.15.4 MIDDLE EAST AND AFRICA

8.15.5 SOUTH AMERICA

9 NORTH AMERICA PALLETS PACKAGING MARKET, BY MACHINE TYPE

9.1 OVERVIEW

9.2 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

9.2.1 FULLY AUTOMATIC

9.2.2 SEMI AUTOMATIC

9.3 NORTH AMERICA FULLY AUTOMATIC IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.3.1 INLINE HOODING SYSTEMS

9.3.2 MONOBLOC HOODING SYSTEMS

9.4 NORTH AMERICA FULLY AUTOMATIC IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.4.1 ASIA-PACIFIC

9.4.2 NORTH AMERICA

9.4.3 EUROPE

9.4.4 MIDDLE EAST AND AFRICA

9.4.5 SOUTH AMERICA

9.5 NORTH AMERICA SEMI AUTOMATIC IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.5.1 ASIA-PACIFIC

9.5.2 NORTH AMERICA

9.5.3 EUROPE

9.5.4 MIDDLE EAST AND AFRICA

9.5.5 SOUTH AMERICA

10 NORTH AMERICA PALLETS PACKAGING MARKET, BY FUNCTION TYPE

10.1 OVERVIEW

10.2 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY FUNCTION TYPE, 2018-2033 (USD THOUSAND)

10.2.1 WRAPPING

10.2.2 STRAPPING

10.2.3 PROTECTION & CUSHIONING

10.2.4 HOODING

10.2.5 OTHERS

10.3 NORTH AMERICA WRAPPING IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.3.1 ASIA-PACIFIC

10.3.2 NORTH AMERICA

10.3.3 EUROPE

10.3.4 MIDDLE EAST AND AFRICA

10.3.5 SOUTH AMERICA

10.4 NORTH AMERICA STRAPPING IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.4.1 ASIA-PACIFIC

10.4.2 NORTH AMERICA

10.4.3 EUROPE

10.4.4 MIDDLE EAST AND AFRICA

10.4.5 SOUTH AMERICA

10.5 NORTH AMERICA PROTECTION & CUSHIONING IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.5.1 ASIA-PACIFIC

10.5.2 NORTH AMERICA

10.5.3 EUROPE

10.5.4 MIDDLE EAST AND AFRICA

10.5.5 SOUTH AMERICA

10.6 NORTH AMERICA HOODING IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.6.1 ASIA-PACIFIC

10.6.2 NORTH AMERICA

10.6.3 EUROPE

10.6.4 MIDDLE EAST AND AFRICA

10.6.5 SOUTH AMERICA

10.7 NORTH AMERICA OTHERS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.7.1 ASIA-PACIFIC

10.7.2 NORTH AMERICA

10.7.3 EUROPE

10.7.4 MIDDLE EAST AND AFRICA

10.7.5 SOUTH AMERICA

11 NORTH AMERICA PALLETS PACKAGING MARKET, BY APPLICATION

11.1 OVERVIEW

11.2 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

11.2.1 FOOD & BEVERAGES (1000)

11.2.2 RETAIL & E-COMMERCE

11.2.3 CONSUMER PACKAGED GOODS (CPG)

11.2.4 PHARMACEUTICALS (2100)

11.2.5 CHEMICALS (2000)

11.2.6 AGRICULTURE & HORTICULTURE (0100)

11.2.7 INDUSTRIAL MANUFACTURING (0001)

11.2.8 AUTOMOTIVE (2900)

11.2.9 ELECTRONICS & APPLIANCES (2500)

11.2.10 OTHERS

11.3 NORTH AMERICA FOOD & BEVERAGES (1000) IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.3.1 ASIA-PACIFIC

11.3.2 NORTH AMERICA

11.3.3 EUROPE

11.3.4 MIDDLE EAST AND AFRICA

11.3.5 SOUTH AMERICA

11.4 NORTH AMERICA RETAIL & E-COMMERCE IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.4.1 ASIA-PACIFIC

11.4.2 NORTH AMERICA

11.4.3 EUROPE

11.4.4 MIDDLE EAST AND AFRICA

11.4.5 SOUTH AMERICA

11.5 NORTH AMERICA CONSUMER PACKAGED GOODS (CPG) (1000) IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.5.1 ASIA-PACIFIC

11.5.2 NORTH AMERICA

11.5.3 EUROPE

11.5.4 MIDDLE EAST AND AFRICA

11.5.5 SOUTH AMERICA

11.6 NORTH AMERICA PHARMACEUTICALS (2100) IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.6.1 ASIA-PACIFIC

11.6.2 NORTH AMERICA

11.6.3 EUROPE

11.6.4 MIDDLE EAST AND AFRICA

11.6.5 SOUTH AMERICA

11.7 NORTH AMERICA CHEMICALS (2000) IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.7.1 ASIA-PACIFIC

11.7.2 NORTH AMERICA

11.7.3 EUROPE

11.7.4 MIDDLE EAST AND AFRICA

11.7.5 SOUTH AMERICA

11.8 NORTH AMERICA AGRICULTURE & HORTICULTURE (0100) IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.8.1 ASIA-PACIFIC

11.8.2 NORTH AMERICA

11.8.3 EUROPE

11.8.4 MIDDLE EAST AND AFRICA

11.8.5 SOUTH AMERICA

11.9 NORTH AMERICA INDUSTRIAL MANUFACTURING (0001) IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.9.1 ASIA-PACIFIC

11.9.2 NORTH AMERICA

11.9.3 EUROPE

11.9.4 MIDDLE EAST AND AFRICA

11.9.5 SOUTH AMERICA

11.1 NORTH AMERICA AUTOMOTIVE (2900) IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.10.1 ASIA-PACIFIC

11.10.2 NORTH AMERICA

11.10.3 EUROPE

11.10.4 MIDDLE EAST AND AFRICA

11.10.5 SOUTH AMERICA

11.11 NORTH AMERICA ELECTRONICS & APPLIANCES (2500) IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.11.1 ASIA-PACIFIC

11.11.2 NORTH AMERICA

11.11.3 EUROPE

11.11.4 MIDDLE EAST AND AFRICA

11.11.5 SOUTH AMERICA

11.12 NORTH AMERICA OTHERS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.12.1 ASIA-PACIFIC

11.12.2 NORTH AMERICA

11.12.3 EUROPE

11.12.4 MIDDLE EAST AND AFRICA

11.12.5 SOUTH AMERICA

12 NORTH AMERICA PALLETS PACKAGING MARKET, BY END USE

12.1 OVERVIEW

12.2 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY END USE, 2018-2033 (USD THOUSAND)

12.2.1 LOGISTICS & 3PL PROVIDERS

12.2.2 MANUFACTURING PLANTS

12.2.3 RETAIL DISTRIBUTION CENTERS

12.2.4 COLD CHAIN OPERATORS

12.2.5 OTHERS

12.3 NORTH AMERICA LOGISTICS & 3PL PROVIDERS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.3.1 ASIA-PACIFIC

12.3.2 NORTH AMERICA

12.3.3 EUROPE

12.3.4 MIDDLE EAST AND AFRICA

12.3.5 SOUTH AMERICA

12.4 NORTH AMERICA MANUFACTURING PLANTS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.4.1 ASIA-PACIFIC

12.4.2 NORTH AMERICA

12.4.3 EUROPE

12.4.4 MIDDLE EAST AND AFRICA

12.4.5 SOUTH AMERICA

12.5 NORTH AMERICA RETAIL DISTRIBUTION CENTERS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.5.1 ASIA-PACIFIC

12.5.2 NORTH AMERICA

12.5.3 EUROPE

12.5.4 MIDDLE EAST AND AFRICA

12.5.5 SOUTH AMERICA

12.6 NORTH AMERICA COLD CHAIN OPERATORS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.6.1 ASIA-PACIFIC

12.6.2 NORTH AMERICA

12.6.3 EUROPE

12.6.4 MIDDLE EAST AND AFRICA

12.6.5 SOUTH AMERICA

12.7 NORTH AMERICA OTHERS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.7.1 ASIA-PACIFIC

12.7.2 NORTH AMERICA

12.7.3 EUROPE

12.7.4 MIDDLE EAST AND AFRICA

12.7.5 SOUTH AMERICA

13 NORTH AMERICA PALLETS PACKAGING MARKET, BY DISTRIBUTION CHANNEL

13.1 OVERVIEW

13.1.1 DIRECT

13.1.2 INDIRECT

13.2 NORTH AMERICA DIRECT IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

13.2.1 COMPANY'S SALES TEAMS

13.2.2 DIRECT OEM CONTRACTS

13.2.3 COMPANY-OWNED WEBSITES

13.3 NORTH AMERICA DIRECT IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

13.3.1 ASIA-PACIFIC

13.3.2 NORTH AMERICA

13.3.3 EUROPE

13.3.4 MIDDLE EAST AND AFRICA

13.3.5 SOUTH AMERICA

13.4 NORTH AMERICA INDIRECT IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

13.4.1 WHOLESALERS / DISTRIBUTORS

13.4.2 INDUSTRIAL SUPPLY STORES

13.4.3 THIRD-PARTY E-COMMERCE

13.5 NORTH AMERICA DIRECT IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

13.5.1 ASIA-PACIFIC

13.5.2 NORTH AMERICA

13.5.3 EUROPE

13.5.4 MIDDLE EAST AND AFRICA

13.5.5 SOUTH AMERICA

14 NORTH AMERICA PALLET PACKAGING MARKET, BY REGION

14.1 NORTH AMERICA

14.1.1 U.S.

14.1.2 CANADA

14.1.3 MEXICO

15 NORTH AMERICA PALLET PACKAGING MARKET: COMPANY LANDSCAPE

15.1 MANUFACTURER COMPANY SHARE ANALYSIS: GLOBAL

16 SWOT ANALYSIS

17 DISTRIBUTOR COMPANY PROFILE

17.1 BUNZL AUSTRALIA & NEW ZEALAND

17.1.1 COMPANY SNAPSHOT

17.1.2 REVENUE ANALYSIS

17.1.3 SOURCE: COMPANY WEBSITE, ANNUAL REPORT, SEC FILING

17.1.4 PRODUCT PORTFOLIO

17.1.5 RECENT DEVELOPMENT

17.2 FASTENAL COMPANY

17.2.1 COMPANY SNAPSHOT

17.2.2 REVENUE ANALYSIS

17.2.3 PRODUCT PORTFOLIO

17.2.4 RECENT DEVELOPMENT

17.3 ULINE

17.3.1 COMPANY SNAPSHOT

17.3.2 PRODUCT/SERVICE PORTFOLIO

17.3.3 RECENT DEVELOPMENT

17.4 VERITIV OPERATING COMPANY

17.4.1 COMPANY SNAPSHOT

17.4.2 PRODUCT/SERVICE PORTFOLIO

17.4.3 RECENT DEVELOPMENT

17.5 W.W. GRAINGER, INC.

17.5.1 COMPANY SNAPSHOT

17.5.2 REVENUE ANALYSIS

17.5.3 PRODUCT PORTFOLIO

17.5.4 RECENT DEVELOPMENT

18 MANUFACTURER COMPANY PROFILE

18.1 SIGMA PLASTICS ASIA

18.1.1 COMPANY SNAPSHOT

18.1.2 COMPANY SHARE ANALYSIS

18.1.3 PRODUCT PORTFOLIO

18.1.4 RECENT DEVELOPMENT

18.2 IPL SCHOELLER.

18.2.1 COMPANY SNAPSHOT

18.2.2 COMPANY SHARE ANALYSIS

18.2.3 PRODUCT PORTFOLIO

18.2.4 RECENT DEVELOPMENT

18.3 NOVOLEX

18.3.1 COMPANY SNAPSHOT

18.3.2 COMPANY SHARE ANALYSIS

18.3.3 PRODUCT PORTFOLIO

18.3.4 RECENT DEVELOPMENT

18.4 CRAEMER GMBH.

18.4.1 COMPANY SNAPSHOT

18.4.2 COMPANY SHARE ANALYSIS

18.4.3 PRODUCT PORTFOLIO

18.4.4 RECENT DEVELOPMENT

18.5 PALLETONE

18.5.1 COMPANY SNAPSHOT

18.5.2 COMPANY SHARE ANALYSIS

18.5.3 PRODUCT PORTFOLIO

18.5.4 RECENT DEVELOPMENT

18.6 AETNA GROUP SPA

18.6.1 COMPANY SNAPSHOT

18.6.2 PRODUCT PORTFOLIO

18.6.3 RECENT DEVELOPMENT

18.7 BEKUPLAST SP. Z O. O.

18.7.1 COMPANY SNAPSHOT

18.7.2 PRODUCT PORTFOLIO

18.7.3 RECENT DEVELOPMENT

18.8 BENOPLAST.

18.8.1 COMPANY SNAPSHOT

18.8.2 PRODUCT PORTFOLIO

18.8.3 RECENT DEVELOPMENT

18.9 CONWED

18.9.1 COMPANY SNAPSHOT

18.9.2 PRODUCT PORTFOLIO

18.9.3 RECENT DEVELOPMENT

18.1 FROMM PACKAGING SYSTEMS

18.10.1 COMPANY SNAPSHOT

18.10.2 PRODUCT/SERVICE PORTFOLIO

18.10.3 RECENT DEVELOPMENT

18.11 NORTH AMERICA PALLETS AND CONTAINERS.

18.11.1 COMPANY SNAPSHOT

18.11.2 PRODUCT PORTFOLIO

18.11.3 RECENT DEVELOPMENT

18.12 GREENDOT BIOPAK PVT. LTD.

18.12.1 COMPANY SNAPSHOT

18.12.2 PRODUCT PORTFOLIO

18.12.3 RECENT DEVELOPMENT

18.13 HEXAPAK

18.13.1 COMPANY SNAPSHOT

18.13.2 PRODUCT/SERVICE PORTFOLIO

18.13.3 RECENT DEVELOPMENT

18.14 HIVIC PLASTIC MANUFACTURE CO., LTD.

18.14.1 COMPANY SNAPSHOT

18.14.2 PRODUCT/SERVICE PORTFOLIO

18.14.3 RECENT DEVELOPMENT

18.15 INTERTAPE POLYMER GROUP (IPG)

18.15.1 COMPANY SNAPSHOT

18.15.2 PRODUCT/SERVICE PORTFOLIO

18.15.3 RECENT DEVELOPMENT

18.16 LANTECH

18.16.1 COMPANY SNAPSHOT

18.16.2 PRODUCT/SERVICE PORTFOLIO

18.16.3 RECENT DEVELOPMENT

18.17 M STRETCH S.P.A.

18.17.1 COMPANY SNAPSHOT

18.17.2 PRODUCT PORTFOLIO

18.17.3 RECENT DEVELOPMENT

18.18 MAILLIS GROUP

18.18.1 COMPANY SNAPSHOT

18.18.2 PRODUCT/SERVICE PORTFOLIO

18.18.3 RECENT DEVELOPMENT

18.19 MATERE PACKAGING

18.19.1 COMPANY SNAPSHOT

18.19.2 PRODUCT PORTFOLIO

18.19.3 RECENT DEVELOPMENT

18.2 MOSCA GMBH

18.20.1 COMPANY SNAPSHOT

18.20.2 PRODUCT PORTFOLIO

18.20.3 RECENT DEVELOPMENT

18.21 ORION PACKAGING SYSTEMS LLC.

18.21.1 COMPANY SNAPSHOT

18.21.2 PRODUCT PORTFOLIO

18.21.3 RECENT DEVELOPMENT

18.22 PARAGON FILMS.

18.22.1 COMPANY SNAPSHOT

18.22.2 PRODUCT PORTFOLIO

18.22.3 RECENT DEVELOPMENT

18.23 POLYFAVO..

18.23.1 COMPANY SNAPSHOT

18.23.2 PRODUCT PORTFOLIO

18.23.3 RECENT DEVELOPMENT

18.24 POLYREFLEX HI-TECH CO., LTD .

18.24.1 COMPANY SNAPSHOT

18.24.2 PRODUCT PORTFOLIO

18.24.3 RECENT DEVELOPMENT

18.25 ROKSON PACKAGING INDUSTRY

18.25.1 COMPANY SNAPSHOT

18.25.2 PRODUCT PORTFOLIO

18.25.3 RECENT DEVELOPMENT

18.26 TRANPAK INC.

18.26.1 COMPANY SNAPSHOT

18.26.2 PRODUCT PORTFOLIO

18.26.3 RECENT DEVELOPMENT

18.27 TRANSOPLAST

18.27.1 COMPANY SNAPSHOT

18.27.2 PRODUCT PORTFOLIO

18.27.3 RECENT DEVELOPMENT

18.28 TRIOWORLD

18.28.1 COMPANY SNAPSHOT

18.28.2 PRODUCT PORTFOLIO

18.28.3 RECENT DEVELOPMENT

18.29 UCMPL

18.29.1 COMPANY SNAPSHOT

18.29.2 PRODUCT PORTFOLIO

18.29.3 RECENT DEVELOPMENT

18.3 WULFTEC INTERNATIONAL INC

18.30.1 COMPANY SNAPSHOT

18.30.2 PRODUCT/SERVICE PORTFOLIO

18.30.3 RECENT DEVELOPMENT

19 QUESTIONNAIRE

20 RELATED REPORTS

List of Table

TABLE 1 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 2 NORTH AMERICA STRETCH FILMS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 3 NORTH AMERICA SHRINK HOOD FILMS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 4 NORTH AMERICA EURO PALLET IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 5 NORTH AMERICA PALLET BOXES IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 6 NORTH AMERICA PALLET LIDS & CAPS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 7 NORTH AMERICA SLIP SHEETS & TIER SHEETS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 8 NORTH AMERICA STRETCH WRAPPERS IN PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

TABLE 9 NORTH AMERICA FULLY AUTOMATIC STRETCH WRAPPERS IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 10 NORTH AMERICA STRETCH WRAPPERS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 11 NORTH AMERICA STRETCH HOODERS IN PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

TABLE 12 NORTH AMERICA FULLY AUTOMATIC STRETCH HOODERS IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 13 NORTH AMERICA STRETCH HOODERS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 14 NORTH AMERICA PALLET NETTING IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 15 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

TABLE 16 NORTH AMERICA FULLY AUTOMATIC IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 17 NORTH AMERICA FULLY AUTOMATIC IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 18 NORTH AMERICA SEMI AUTOMATIC IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 19 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY FUNCTION TYPE, 2018-2033 (USD THOUSAND)

TABLE 20 NORTH AMERICA WRAPPING IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 21 NORTH AMERICA STRAPPING IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 22 NORTH AMERICA PROTECTION & CUSHIONING IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 23 NORTH AMERICA HOODING IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 24 NORTH AMERICA OTHERS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 25 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 26 NORTH AMERICA FOOD & BEVERAGES (1000) IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 27 NORTH AMERICA RETAIL & E-COMMERCE IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 28 NORTH AMERICA CONSUMER PACKAGED GOODS (CPG) (1000) IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 29 NORTH AMERICA PHARMACEUTICALS (2100) IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 30 NORTH AMERICA CHEMICALS (2000) IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 31 NORTH AMERICA AGRICULTURE & HORTICULTURE (0100) IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 32 NORTH AMERICA INDUSTRIAL MANUFACTURING (0001) IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 33 NORTH AMERICA AUTOMOTIVE (2900) IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 34 NORTH AMERICA ELECTRONICS & APPLIANCES (2500) IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 35 NORTH AMERICA OTHERS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 36 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY END USE, 2018-2033 (USD THOUSAND)

TABLE 37 NORTH AMERICA LOGISTICS & 3PL PROVIDERS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 38 NORTH AMERICA MANUFACTURING PLANTS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 39 NORTH AMERICA RETAIL DISTRIBUTION CENTERS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 40 NORTH AMERICA COLD CHAIN OPERATORS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 41 NORTH AMERICA OTHERS IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 42 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 43 NORTH AMERICA DIRECT IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 44 NORTH AMERICA DIRECT IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 45 NORTH AMERICA INDIRECT IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 46 NORTH AMERICA DIRECT IN PALLET PACKAGING PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 47 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY COUNTRY, 2018-2033 (USD THOUSAND)

TABLE 48 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY COUNTRY, 2018-2033 (USD THOUSAND)

TABLE 49 NORTH AMERICA

TABLE 50 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 51 NORTH AMERICA STRETCH WRAPPERS IN PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

TABLE 52 NORTH AMERICA FULLY AUTOMATIC STRETCH WRAPPERS IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 53 NORTH AMERICA STRETCH HOODERS IN PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

TABLE 54 NORTH AMERICA FULLY AUTOMATIC STRETCH HOODERS IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 55 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

TABLE 56 NORTH AMERICA FULLY AUTOMATIC IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 57 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY FUNCTION TYPE, 2018-2033 (USD THOUSAND)

TABLE 58 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 59 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY END USE, 2018-2033 (USD THOUSAND)

TABLE 60 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 61 NORTH AMERICA DIRECT IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 62 NORTH AMERICA INDIRECT IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 63 U.S. PALLET PACKAGING PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 64 U.S. STRETCH WRAPPERS IN PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

TABLE 65 U.S. FULLY AUTOMATIC STRETCH WRAPPERS IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 66 U.S. STRETCH HOODERS IN PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

TABLE 67 U.S. FULLY AUTOMATIC STRETCH HOODERS IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 68 U.S. PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

TABLE 69 U.S. FULLY AUTOMATIC IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 70 U.S. PALLET PACKAGING PRODUCTS MARKET, BY FUNCTION TYPE, 2018-2033 (USD THOUSAND)

TABLE 71 U.S. PALLET PACKAGING PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 72 U.S. PALLET PACKAGING PRODUCTS MARKET, BY END USE, 2018-2033 (USD THOUSAND)

TABLE 73 U.S. PALLET PACKAGING PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 74 U.S. DIRECT IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 75 U.S. INDIRECT IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 76 CANADA PALLET PACKAGING PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 77 CANADA STRETCH WRAPPERS IN PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

TABLE 78 CANADA FULLY AUTOMATIC STRETCH WRAPPERS IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 79 CANADA STRETCH HOODERS IN PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

TABLE 80 CANADA FULLY AUTOMATIC STRETCH HOODERS IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 81 CANADA PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

TABLE 82 CANADA FULLY AUTOMATIC IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 83 CANADA PALLET PACKAGING PRODUCTS MARKET, BY FUNCTION TYPE, 2018-2033 (USD THOUSAND)

TABLE 84 CANADA PALLET PACKAGING PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 85 CANADA PALLET PACKAGING PRODUCTS MARKET, BY END USE, 2018-2033 (USD THOUSAND)

TABLE 86 CANADA PALLET PACKAGING PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 87 CANADA DIRECT IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 88 CANADA INDIRECT IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 89 MEXICO PALLET PACKAGING PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 90 MEXICO STRETCH WRAPPERS IN PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

TABLE 91 MEXICO FULLY AUTOMATIC STRETCH WRAPPERS IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 92 MEXICO STRETCH HOODERS IN PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

TABLE 93 MEXICO FULLY AUTOMATIC STRETCH HOODERS IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 94 MEXICO PALLET PACKAGING PRODUCTS MARKET, BY MACHINE TYPE, 2018-2033 (USD THOUSAND)

TABLE 95 MEXICO FULLY AUTOMATIC IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 96 MEXICO PALLET PACKAGING PRODUCTS MARKET, BY FUNCTION TYPE, 2018-2033 (USD THOUSAND)

TABLE 97 MEXICO PALLET PACKAGING PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 98 MEXICO PALLET PACKAGING PRODUCTS MARKET, BY END USE, 2018-2033 (USD THOUSAND)

TABLE 99 MEXICO PALLET PACKAGING PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 100 MEXICO DIRECT IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 101 MEXICO INDIRECT IN PALLET PACKAGING PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

List of Figure

FIGURE 1 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET: SEGMENTATION

FIGURE 2 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET: DATA TRIANGULATION

FIGURE 3 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET: DROC ANALYSIS

FIGURE 4 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET: COUNTRYWISE MARKET ANALYSIS

FIGURE 5 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET: DBMR MARKET POSITION GRID

FIGURE 8 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET: VENDOR SHARE ANALYSIS

FIGURE 9 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET: MULTIVARIVATE MODELING

FIGURE 10 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET: TYPE TIMELINE CURVE

FIGURE 11 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET: VERTICAL COVERAGE GRID

FIGURE 12 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET: SEGMENTATION

FIGURE 13 SEVEN SEGMENTS COMPRISE THE NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET, BY PRODUCT TYPE (2025)

FIGURE 14 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET: EXECUTIVE SUMMARY

FIGURE 15 STRATEGIC DECISIONS

FIGURE 16 EXPANSION OF NORTH AMERICA MANUFACTURING, GROWTH OF ORGANIZED LOGISTICS, UNITIZED LOAD HANDLING, AND ADOPTION OF REUSABLE TRANSPORT PACKAGING ARE EXPECTED TO DRIVE THE NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET DURING THE FORECAST PERIOD OF 2026 TO 2033

FIGURE 17 STRETCH FILMS IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE NORTH AMERICA PALLET PACKAGING PRODUCTS MARKET IN 2026 & 2033

FIGURE 18 NORTH AMERICA PALLET PACKAGING PRODUCTS MARKETSS, 2025-2033, AVERAGE SELLING PRICE (USD/PER ROLL)

FIGURE 19 DRIVERS, RESTRINTS, OPPORTUNITIES AND CHALLENGES OF NORTH AMERICA PALLETS PACKAGING MARKET

FIGURE 20 NORTH AMERICA PALLETS PACKAGING MARKET: BY PRODUCT TYPE, 2025

FIGURE 21 NORTH AMERICA PALLETS PACKAGING MARKET: BY MACHINE TYPE, 2025

FIGURE 22 NORTH AMERICA PALLETS PACKAGING MARKET: BY FUNCTION TYPE, 2025

FIGURE 23 NORTH AMERICA PALLETS PACKAGING MARKET: BY APPLICATION, 2025

FIGURE 24 NORTH AMERICA PALLETS PACKAGING MARKET: BY END USE, 2025

FIGURE 25 NORTH AMERICA PALLETS PACKAGING MARKET: BY DISTRIBUTION CHANNEL , 2025

FIGURE 26 NORTH AMERICA PALLET PACKAGING MARKET: SNAPSHOT (2026)

FIGURE 27 NORTH AMERICA PALLET PACKAGING MARKET: COMPANY SHARE 2025 (%)

North America Pallet Packaging Products Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Pallet Packaging Products Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Pallet Packaging Products Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.