アジア太平洋コンシューマー電子パッケージング市場規模、株式・動向分析レポート

Market Size in USD Billion

CAGR :

%

USD

12.55 Billion

USD

36.05 Billion

2024

2032

USD

12.55 Billion

USD

36.05 Billion

2024

2032

| 2025 –2032 | |

| USD 12.55 Billion | |

| USD 36.05 Billion | |

| % | |

|

アジアパシフィックコンシューマー電子包装市場セグメンテーション、タイプ(段ボール箱、板紙箱、熱成形トレイ、ブリスターパック、防護包装、バッグ、袋、ポーチ、フィルム、泡包装、エアバブルポーチ、その他)、包装材料(プラスチック、紙、アルミホイル、セルロース、その他)、層(プライマリパッケージング、セカンダリ包装、およびテラシー包装)、技術(アクティブ、インテリジェント包装、その他)、印刷、その他(その他)、印刷、電子印刷、電子印刷、電子印刷、その他)

アジアパシフィックコンシューマー電子包装市場規模

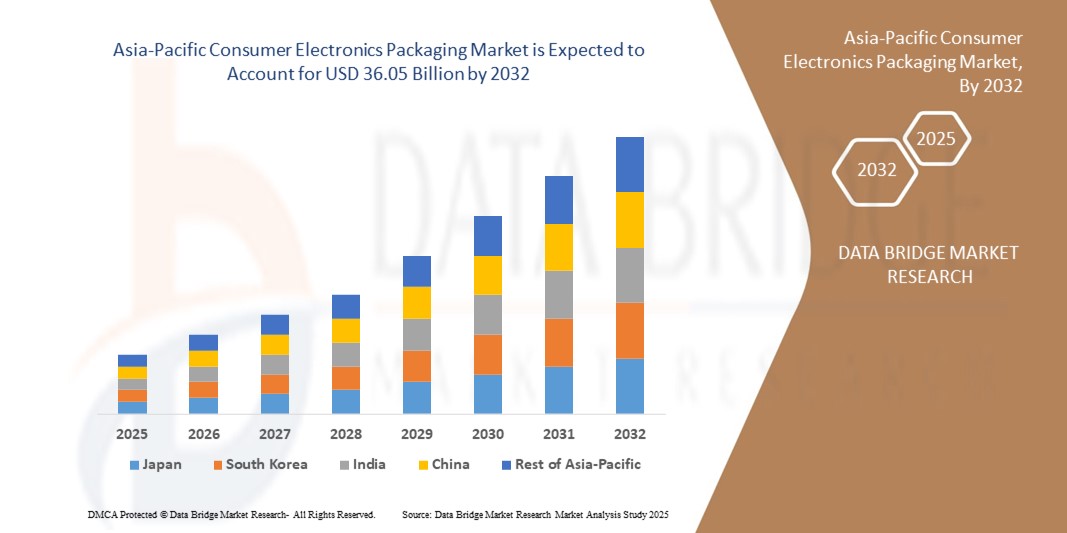

- アジア・パシフィックの消費者向け電子機器包装市場規模は、2024年のUSD 12.55億そして到達する予定2032年までのUSD 36.05億, お問い合わせCAGRの14.1%予報期間中

- 市場成長は交通機関、貯蔵および小売表示の間に敏感な消費者電子工学を保護するために安全、耐久および持続可能な包装の解決のための上昇の要求によって主に燃料を供給されます。 スマートフォン、ノートパソコン、ウェアラブル、家電製品の販売を増加させ、製品の安全性を確保し、消費者体験を向上させる革新的なパッケージの必要性を促進

- また、板紙やパルプ成形、繊維製紙などの環境にやさしい材料の採用は、メーカーが規制圧力に対応し、消費者の好みをシフトする業界を再構築しています。 これらの収束要因は、先進的かつ持続可能なパッケージングフォーマットの上昇を加速し、これにより、業界の成長を著しく向上しています

アジアパシフィックコンシューマー電子パッケージング市場分析

- 消費者電子機器包装は、段ボール箱、ブリスターパック、クラムシェル、熱成形トレイ、保護包装、および柔軟なソリューションなど、さまざまな材料とフォーマットで構成されています。 また、視覚的に魅力的で機能的なデザインを通じて、ブランディングと消費者のエンゲージメントに重要な役割を果たしています

- 消費者用電子機器包装のエスケーラブル要求は、主に電子商取引の急速な拡大によって駆動され、電子機器の生産を増加させ、リサイクル性と持続可能性に重点を置いています。 軽量、費用効果が大きい、および優れた包装のフォーマットの連続的な革新は開発され、新興国を渡る市場の強い成長見通しを補強します

- 中国は消費者電子包装の市場を支配しました 2024年に、強力な電子機器製造拠点、大規模輸出、革新的なパッケージング技術の迅速な採用により、

- インドは、急速に都市化、中級人口の拡大、スマートフォンなどの消費者向けデバイスに対する需要の高まりなどにより、予測期間中に消費者向け電子機器包装市場で最も急速に成長している国であることが期待されています

- プラスチックセグメントは、柔軟性、軽量性、防塵、湿気、衝撃に対する強力な保護機能により、2024年に44.1%の市場シェアで市場を支配しました。 熱成形トレイ、フィルム、ブリスターパックなどのプラスチックフォーマットは、汎用性と費用効果の高いため、モバイルデバイスやアクセサリに広く採用されています。 第一次および二次包装のフォーマットのための材料の適応性はまたそれを電子工学の製造業者のための好まれた選択にします

レポートスコープと消費者電子パッケージング市場セグメンテーション

| アトリビュート | 消費者電子包装の主要市場洞察 |

| カバーされる区分 |

|

| カバーされた国 | アジアパシフィック

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、データブリッジ市場調査によってキュレーションされた市場レポートには、インポートエクスポート分析、生産能力概要、生産消費分析、価格推移分析、気候変動シナリオ、サプライチェーン分析、バリューチェーン分析、バリューチェーン分析、原材料/消耗品概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークなどがあります。 |

アジア太平洋コンシューマー電子パッケージング市場動向

消費者エレクトロニクス産業の成長

- 消費者エレクトロニクス産業の着実な成長は、革新的で保護的、視覚的に包装ソリューションをアピールするための直接運転需要です。 スマートフォン、ノートパソコン、ウェアラブルの売上拡大に伴い、ブランド価値向上や消費者の不定食体験の向上に向け、敏感なデバイスを保護するパッケージにブランドが増えています。

- 例えば、Samsung と Apple は、スマートフォン用のパッケージを再設計し、プラスチックの使用を大幅に削減し、繊維ベースのデザインを採用しています。 これらの変化は、大手企業が持続可能性の目標とパッケージングイノベーションを一直線に合わせている方法を反映しており、消費者の需要に応え、プレミアムなアンボックス化体験を提供

- 電子機器の小型化により、小型・軽量・保護包装の要求が生まれました。 衝撃吸収剤のインサート、成形パルプトレイ、およびリサイクル紙ベースのソリューションは、ポリスチレンまたは泡の代替品として新興され、輸送中の安全性を確保し、バルクを追加することなく貯蔵します

- 持続可能性は重要なトレンドになり、企業がリサイクル可能でミニマリストなパッケージングにシフトしています。 グローバルな持続可能性のコミットメントと環境にやさしいソリューションのための消費者の好みに合わせて、包装メーカーをプッシュして材料の使用を最適化し、サプライチェーンにおける廃棄物発生を削減します。

- タンパー明白なシール、QR対応のパッケージおよび追跡システムのようなよりスマートな包装の解決を可能にしま、すべては透明物およびプロダクト信頼性を高めます。 このような革新は、企業が在庫管理を合理化できるようにしながら、電子機器の真正性で消費者の自信を向上させます

- 全体的に、消費者エレクトロニクス産業の成長は、パッケージングを戦略的差別化要因に変えています。 安全性、持続性、ブランディングニーズの組み合わせは、革新的なデザインを採用し、この拡大市場で競争力のあるポジショニングをパッケージングするブランドを説得しています。

アジア太平洋コンシューマー電子パッケージング市場ダイナミクス

ドライバー

Eコマースセクターの拡大

- 電子商取引プラットフォームの急速な拡大は、消費者電子パッケージングの重要なドライバーとして登場しました。 オンラインで装置を購入するより多くの消費者によって、強く、改ざん防止および保護包装のための要求は倉庫からの顧客の家に安全な配達を保障するために集中しました

- たとえば、Amazonは「Frustration-Free Packaging」プログラムを導入し、プラットフォームを通じて出荷される電子製品の安全性の高いレベルを維持しながら、材料の使用を最小限に抑えています。 このイニシアチブは、電子商取引におけるパッケージングイノベーションが業界の期待をグローバルに再構築する方法を強調しています。

- eコマースの上昇は、リターンとダメージ率を削減するパッケージングフォーマットの重要性が増加しました。 堅い波形箱、緩衝されたインサートおよび防水外的な覆いはますますクロスボーダーの交通機関および長距離配達の間に壊れやすい電子装置を保障するために利用されます

- また、オンライン・エクスクルーシブ・エレクトロニクスの発売とお祝いシーズンの売上へのシフトは、スケーラブル、軽量、機能的なパッケージングソリューションで高い需要を寄せています。 この要求を満たすと、物流やメーカーや小売業者のコスト効率を最適化しながら、タイムリーな納期を確保

- 結論として、電子商取引の拡大は、安全性、ブランディング、および効率的な電子商取引の処理を提供する包装の役割を増幅しています。 この傾向は、パッケージが成功したオンライン小売戦略と長期顧客の保持に不可欠残っていることを保証します

拘束/チャレンジ

製品の種類と標準化

- 消費者電子パッケージングの大きな課題の1つは、製品サイズ、形状、および実用性レベルの広範な特徴に対応しています。 ウェアラブルから大型家電に至るまで、デバイスの多様性は、標準化された保護包装ソリューションの設計プロセスを複雑化します。

- たとえば、Dellは、軽量なラップトップからバルクモニターに至るまで、さまざまな製品ポートフォリオにわたってパッケージの保護ニーズで、持続可能性の目標のバランスを整える課題に直面しています。 これは、複数のデバイスカテゴリにケータリングしながら標準化を保証する業界全体の闘争を反映しています

- 多くの場合、新しいフォーム要因と壊れやすいコンポーネントをもたらす電子デバイスの定数進化は、パッケージフォーマットの頻繁な再設計が必要です。 これにより、メーカーのコストを上げ、製品範囲全体で効率的なパッケージングソリューションをスケールダウンすることができます。

- 包装材料および保護ベンチマークの普遍的な標準の欠如は性能の矛盾に導きます、ある解決は出荷の間に装置を適切に保護するために失敗しました。 このリスクは、より高いリターン率、増加された物流コスト、および顧客の不満を引き起こす可能性があります

- 標準化に向けた取り組みは、業界にとってますますます重要である一方で、製品価値の確保に取り組みます。 このバランスを達成するには、モジュール設計、複数の製品カテゴリに適応可能な持続可能な材料、およびパッケージングイノベーションが効果的かつスケーラブルなままであることを保証するために、保護ベンチマークに関する業界レベルのコラボレーションへの投資が必要になります

アジアパシフィックコンシューマー電子包装市場スコープ

市場はタイプ、包装材料、層、技術、印刷の技術、配分チャネルおよび適用に基づいて区分されます。

- タイプ別

タイプに基づいて、消費者電子機器包装市場は、段ボール箱、板紙箱、熱成形トレイ、ブリスターパックとクラムシェル、保護包装、バッグ、袋、袋、袋、フィルム、泡包装、空気泡袋などに分かれています。 コルゲートボックスのセグメントは、2024年に最大の市場収益シェアを占め、優れた強度、再生性、テレビ、デスクトップ、家庭用電化製品などのバルク電子を出荷するための広範な使用によって駆動しました。 長距離輸送中に圧力を積み重ね、脆弱な商品を保護する能力は、メーカーにとって好ましい選択になります。 持続可能で軽量な包装に重点を置き、耐久性のある段ボール箱の残高の費用効率性を高める。

ブリスターパックとクラムシェルセグメントは、携帯電話、ウェアラブル、アクセサリーパッケージの採用により燃料供給され、2025年から2032年までの最速成長率を目撃することを期待しています。 これらのソリューションは、優れた製品可視性、改ざん抵抗、およびコンパクト性を提供し、小売ディスプレイに最適です。 彼らの透明設計は、盗難を軽減しながら、消費者のアピールを強化し、自動化されたパッケージングプロセスとの互換性は、効率性をサポートします。 消費者向け電子機器のプレミアムプレゼンテーションの需要が増え、ブリスターパックとクラムシェルが急激な拡大が見込まれる見込みです。

- 包装材料によって

包装材料に基づいて、市場はプラスチック、ペーパー、アルミ ホイル、セルロースおよび他のに分けられます。 プラスチックセグメントは、2024年に44.1%の最大の市場収益シェアを保持し、柔軟性、軽量性、防塵、湿気、衝撃に対する強力な保護機能に起因しています。 熱成形トレイ、フィルム、ブリスターパックなどのプラスチックフォーマットは、汎用性と費用効果の高いため、モバイルデバイスやアクセサリに広く採用されています。 第一次および二次包装のフォーマットのための材料の適応性はまたそれを電子工学の製造業者のための好まれた選択にします。

紙のセグメントは、環境に配慮し、リサイクル可能な包装代替品の需要が高まっている2025年から2032年までの最速成長率を目撃する見込みです。 シングルユースプラスチックの制限を増加させることで、紙板や紙パルプのソリューションへのシフトを加速し、消費者向け電子機器包装におけるパルプソリューションを形成しています。 紙ベースのフォーマットは、持続可能性と生分解性のために、より小さな電子機器やアクセサリの牽引を得ています。 コーティングされたおよび設計されていたボール紙の連続的な革新によって高められた耐久性および湿気の抵抗、区分は重要な成長のために置きます。

- 層別

層に基づいて、市場は第一次包装、二次包装およびtertiary包装に分けられます。 第一次パッケージング部門は、2024年に最大の収益シェアを占め、スマートフォン、カメラ、損傷、ほこり、静電放電からウェアラブルなどの電子機器を保護するための直接的な役割を担っています。 プライマリパッケージは、重要なブランディング要素として機能する魅力的なアンボックス設計により、消費者体験を向上させます。 メーカーは、市場でのセグメントの位置を強化し、洗練された、コンパクトで保護設計に投資しています。

二次包装部門は、バルク処理、物流、小売ディスプレイの重要性によって駆動され、2025から2032までの最速のレートで成長することを期待しています。 この層で使用される波形のカートンそしてmultipacksは小売の有効な積み重ね、安全な交通機関および高められた棚の存在を提供します。 eコマースと国際出荷の拡大に伴い、強力で軽量な二次パッケージの需要は高まっています。 再生可能で持続可能な二次材料の採用を上げると、このセグメントの成長軌跡をさらに加速します。

- テクノロジー

技術の基づいて、市場は活動的な包装、理性的な包装、変更された大気包装、抗菌包装、無菌包装および他に分けられます。 変更された大気包装の区分は、酸化、湿気および微生物の危険から敏感な電子工学を保護することの有効性による2024年に最大の収益のシェアを支配しました。 この技術は、半導体および精密部品のために特に価値があります、延長棚の生命およびプロダクト安定性を保障します。 静電防止機能との統合により、消費者エレクトロニクス業界における採用を強化します。

インテリジェントなパッケージングセグメントは、スマートタグ、センサー、QRコード、NFC機能の採用率が増加し、2025から2032までの最速成長率を記録することが期待されます。 これらの技術は、偽造とリアルタイムの追跡と認証を有効にするのに役立ちます。これは、電子サプライチェーンにおいてます重要になります。 インテリジェントなパッケージングは、製品の詳細と使用説明書を提供することにより、消費者のエンゲージメントを高めます。 接続可能でトレース可能なパッケージングソリューションのトレンドは、このセグメントの急速なアップテークを燃料化しています。

- 印刷技術によって

印刷技術に基づき、市場はフレキソグラフィ、グラビアなどの分野に分けられます。 フレキソプリンティングセグメントは、2024年に最大の市場シェアを占め、コスト効率性、適応性を複数の基材に備え、高品質のグラフィックをスケールで提供する能力を発揮しました。 波形箱および適用範囲が広い包装で広く利用された、それは消費者電子工学の急な回転率そしてサポート ブランディングの努力を可能にします。 視覚的に訴求するパッケージングの重要性は、フレキソソリューションの需要を促進し続けています。

グラビア印刷の印刷の区分は2025から2032までの最も速い成長率を目撃するために、精密な細部、金属効果および高解像の優れた質の印刷物を作り出す機能が原因で期待されます。 高級な提示が重要である上限の消費者電子工学の包装で特に好まれます。 コストが高いにもかかわらず、長い生産のグラビアの一貫した品質は、それがプレミアムパッケージアプリケーションのために魅力的になります。 電子の豪華で審美的な包装の解決のための上昇の要求は区分の成長を促進するために期待されます。

- 流通チャネル

流通チャネルに基づいて、市場は電子商取引、スーパーマーケット/スーパーマーケット、専門店、および他に分けられます。 eコマースセグメントは、スマートフォン、ラップトップ、アクセサリーなどのオンラインショッピングの人気が高まっている2024年に最大の収益シェアを占めています。 このチャネルでのパッケージングは、トランジット、軽量材料、および消費者に優しいアンボクシング体験における製品安全に焦点を当てています。 デジタル小売プラットフォームの迅速な浸透と宅配の利便性は、セグメントの優位性を強化し続けています。

スーパーマーケットやスーパーマーケットのセグメントは、2025年から2032年にかけて最も速い成長率を投稿すると予想されます。消費者は、購入前に電子機器の店頭評価を優先しています。 棚準備ができて包装、タンパー明白なフォーマットおよび優れた表示はこの区分の運転の要求です。 新興国における組織的な小売インフラの拡大は、このチャネルのための重要な成長機会を提供します。 棚の可視性を高める包装の革新は採用を加速します。

- 用途別

適用に基づいて、市場は携帯電話、コンピュータ、テレビ、DTH およびセットトップ ボックス、音楽システム、プリンター、走査器およびコピー機械、ゲーム コンソールおよびおもちゃ、カムコーダーおよびカメラ、電子ウェアラブル、デジタル媒体のアダプターおよび他に区分されます。 携帯電話セグメントは、高出荷量と頻繁な製品の発売によって駆動され、2024年に最大の収益シェアを支配しました。 スマートフォン向けパッケージングは、コンパクトさ、プレミアムフィニッシュ、保護機能を重視し、ブランドイメージや消費者体験を向上させます。 スマートフォン業界における継続的なイノベーションサイクルは、このセグメントのパッケージングに強い需要を維持します。

電子ウェアラブルセグメントは、フィットネストラッカー、スマートウォッチ、および健康監視機器の採用により燃料を供給し、2025から2032までの最速のレートで成長する予定です。 ウェアラブルな電子機器は、コンパクトで軽量で持続可能なパッケージを必要とし、製品設計と美学を強調しています。 ウェアラブル技術の急速な革新と共に、健康およびライフスタイル プロダクトの高める消費者焦点は専門にされた包装の解決のための要求を運転しています。 セグメントは、プレミアムとミッドレンジのウェアラブルカテゴリの両方で強い成長から恩恵を受けます。

アジア太平洋コンシューマー電子パッケージング市場地域分析

- 中国は、その強力な電子機器製造拠点、大規模な輸出、革新的なパッケージング技術の急速な採用によって駆動され、2024年に最大の収益シェアで消費者電子包装市場を支配しました

- 国の優位性は、保護、持続可能な、費用対効果の高いパッケージの大量要求する主要な消費者エレクトロニクスブランドと契約メーカーの存在によって強化されます

- スマートフォン、ノートパソコン、ウェアラブルの国内消費量を増加させ、多様なパッケージングフォーマットの需要をさらに高めます。 スマートな包装および環境に優しい材料の強い投資は地域市場での中国のリーダーシップを統合し、堅牢な電子商取引の成長は地位を強化し続けます

日本コンシューマー電子包装市場インサイト

日本市場は、2025年から2032年にかけて、先進エレクトロニクス分野を牽引し、高品質で精密なパッケージングソリューションに重点を置いた成長を着実に期待しています。 日本メーカーは、ウェアラブル、カメラ、ゲーム機などの製品に、プレミアム、コンパクト、サステナブルなパッケージを採用しています。 市場は、製品の魅力とブランドの信頼を高める革新的な包装のための強力な消費者需要の恩恵。 再生可能で生分解性のある素材に重点を置いた日本は、環境に優しい包装の採用を主導しています。 ローカルパッケージング会社とグローバルエレクトロニクスブランドとのコラボレーションにより、日本の市場における着実な成長をさらに強化。

インドコンシューマー電子パッケージング市場インサイト

インドは、2025年から2032年にかけて、アジアパシフィックの消費者向け電子パッケージング市場で最速のCAGRを登録し、急速に都市化し、中級人口の拡大、スマートフォンなどの消費者向け機器の需要の高まりを想定しています。 「インドのMake in India」などの取り組みに基づく国内電子機器製造の拡大は、費用対効果の高い保護パッケージの必要性を大幅に増加させました。 ライジング電子商取引浸透は、耐久性と軽量のパッケージングフォーマットの採用を加速しています。 紙ベースのリサイクル可能な材料の持続可能性と上昇の投資に重点を置き、市場開拓を図っています。 小売ネットワークを拡大し、グローバルパッケージング会社とのコラボレーションにより、インドは急速に成長する地域として位置します。

アジア太平洋コンシューマー電子パッケージング市場シェア

消費者用電子機器包装業界は、主に、以下を含む老舗の企業によって導かれています。

- Smurfit Kappaグループ(アイルランド)

- モンディグループ(オーストリア)

- DS Smith(イギリス)

- ウェストロック(米国)

- Huhtamäki Oyj (フィンランド)

- Amcor plc(スイス)

- カディスホールディングスS.A.(ルクセンブルグ)

- サニカグループ(スペイン)

- セダグループ(イタリア)

- LGR包装(フランス)

アジア太平洋コンシューマー電子パッケージング市場の最新動向

- 2025年2月 シーメンスのデジタル工業 ソフトウェアは、TSMC の InFO パッケージング技術、統合 Innovator3D IC、Xpedition Package Designer、HyperLynx DRC、Calibre nmDRC ソフトウェアで認定された自動ワークフローを導入しました。 半導体パッケージング設計市場において、より効率的で正確なチップスケールの統合を可能にすることにより、Siemensのポジションを強化します。 発売は、自動で高精度な電子包装ソリューションの需要を反映し、半導体メーカーの市場投入時間向上、先進的なIC包装ワークフローにおけるシーメンスの競争力を強化

- 2024年9月、Scrona AGはElectroninks社と提携し、RDL修理、微細加工、充填、3Dインターコネクトなどの用途を中心に、次世代半導体パッケージの材料およびプロセスを進化させました。 このコラボレーションは、チューリッヒと台湾の共同研究開発により、チップパッケージの小型化と性能向上に大きな一歩を踏み出します。 ScronaのEHDプリントヘッド技術をElectroninksの先端材料と組み合わせることで、パートナーシップは半導体製造の革新を加速し、より微細な精度と高密度の相互接続のための業界のニーズに対応

- 2024年7月、Googleは2024年のグリーンレポートで発表しました。このピクセル電話包装は現在99%のプラスチックフリーで、パッケージ重量と量を50%以上削減しました。 このイニシアチブは、Googleが繊維ベースの持続可能な代替物への移行をもたらすので、消費者の電子機器包装市場に著しく影響を与えます。 2025年までに全てのプラスチック包装をなくすために、同社の誓約に合致し、スマートフォン業界向けに新しい持続可能性のベンチマークを設定し、競合他社に影響を与え、プレミアムデバイスパッケージの環境にやさしい慣行を採用

- 2023年11月、DS Smithは、VersuniのPhilipsホームアプライアンスライン用の紙ベースのパッケージを再設計し、エアフライヤーや掃除機などの製品をカバーしました。 新しい設計は繊維の緩衝と従来の保護材料を取り替え、QRコード指示を組み込み、再生性を後押しする間インク使用法を最小限に抑えます。 この開発により、DS Smithの持続可能なパッケージング市場における役割を強化し、環境に配慮した消費者向けソリューションを提供します。 ファイバーベースのパッケージングのイノベーションは、家庭用電化製品パッケージのグリーン代替のための規制圧力と消費者の要求の両方に対処する方法を強調しています

- 2020年2月、Mondiは、持続可能な段ボール包装ソリューションを生産するために、メキシコの段ボール包装会社であるCartroと協業しました。 この戦略的パートナーシップは、カルトロの地域の専門知識を活用して、ラテンアメリカ包装市場でモンディの足跡を強化しました。 イニシアチブは、消費者向け商品や電子機器のリサイクル可能な段ボール包装のための成長した需要をサポートし、最終的にはモンディの長期収益成長に貢献し、循環型経済主導のパッケージングイノベーションへのコミットメントを強化

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。