Asia

Market Size in USD Billion

CAGR :

%

USD

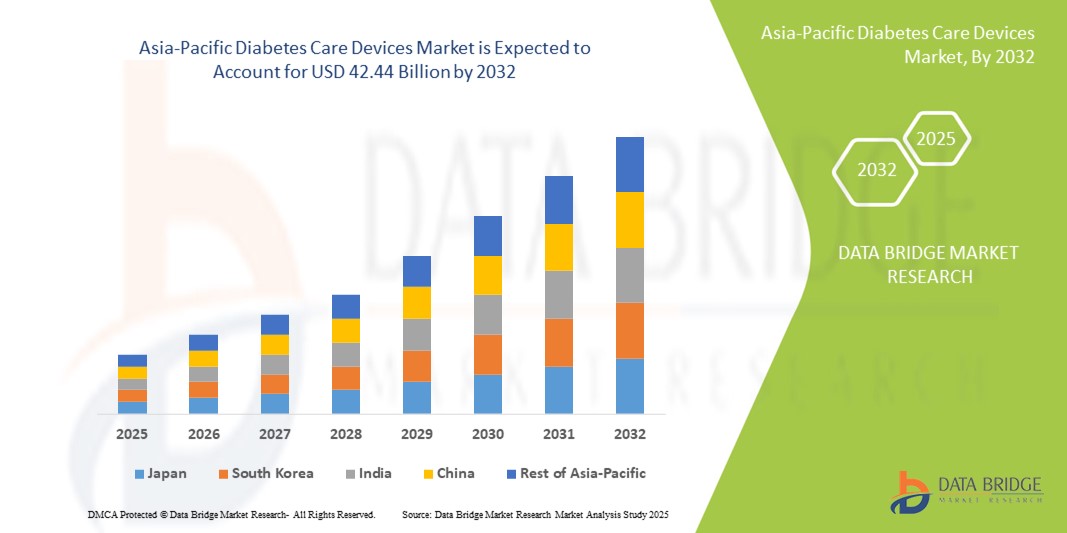

23.62 Billion

USD

42.44 Billion

2024

2032

USD

23.62 Billion

USD

42.44 Billion

2024

2032

| 2025 –2032 | |

| USD 23.62 Billion | |

| USD 42.44 Billion | |

| % | |

|

Asia-Pacific Diabetes Care Device Market Segmentation, By Management Device (Insulin Pump, Insulin Pen, Insulin Syringe, Jet Injector), モニタリングデバイス(自己監視血糖値と連続グルコースモニタリング), エンドユーザー(病院・クリニック・家庭・個人), 流通チャネル(機関販売・小売販売) - 業界動向と予測 203232

アジアパシフィック糖尿病ケア機器市場規模

- アジア・パシフィック・糖尿病ケア機器市場規模が評価されました2024年のUSD 23.62億そして到達する予定2032年までに42.44億米ドル, お問い合わせカリフォルニア 7.60%予報期間中

- この堅牢な成長は、主に地域における糖尿病の蔓延、糖尿病ケア技術の進歩、および糖尿病管理の改善を目的とした公的および民間セクターからの重要な投資によって推進されています

- さらに、費用対効果の高いユーザーフレンドリーな糖尿病ケアソリューションの需要は、これらのデバイスを住宅や臨床設定の両方で糖尿病を管理するための重要なツールとして確立しています

アジア太平洋糖尿病ケアデバイス市場分析

- 糖尿病の心配装置、インシュリン ポンプ、インシュリンのペン、インシュリンのスポイト、ジェットの注入器を含む、自己モニタリング血糖(SMBG) 装置および連続的なグルコースの監視(CGM) システム, 臨床と家庭の設定の両方で効果的な糖尿病管理のためにますますます重要になっています。 精度, 利便性, デジタルヘルスプラットフォームとの統合

- 糖尿病ケア機器の需要は、中国、インド、日本などの国における糖尿病の増大の蔓延により、適切な疾患管理に対する意識を高め、技術的に高度でユーザーフレンドリーで最小限の侵襲的なソリューションを優先しています。

- 中国は、2024年にアジア太平洋糖尿病治療装置市場を支配し、地域における最大の糖尿病人口による38.5%の収益分配、ヘルスケアインフラの拡大、糖尿病管理の促進、先進的な監視およびインスリン配送装置の高度採用を主導

- インドは、予測期間中にアジア・パシフィック・糖尿病ケア機器市場で最も急速に成長している国であることが期待されています。, 増加する使い捨て収入によってサポート, 医療のアクセシビリティを向上させます。, 自己監視と家庭ベースの糖尿病管理ソリューションの意識の増加

- セルフモニトリング血液グルコース(SMBG)デバイスは、2024年にアジア太平洋糖尿病治療装置市場を占め、52.5%の市場シェアで、病院、診療所、家庭/個人的な設定を横断する使いやすさ、使いやすさ、使いやすさ、導入の容易さによって駆動

レポートスコープとアジア太平洋糖尿病ケアデバイス市場セグメント

| アトリビュート | アジア・パシフィック・ダイベレス・ケア・デバイス・キーマーケット・インサイト |

| カバーされる区分 |

|

| カバーされた国 | アジアパシフィック

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがキュレーションする市場レポートには、詳細なエキスパート分析、価格設定分析、ブランドシェア分析、消費者調査、デモグラフィ分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークが含まれます。 |

アジアパシフィック糖尿病ケアデバイス市場動向

スマートモニタリングとモバイルヘルスプラットフォームの統合

- アジア・パシフィックの糖尿病ケア機器市場における重要な傾向は、モバイルヘルス(mHealth)アプリケーションとクラウドベースのプラットフォームを備えたデバイスの統合の増加であり、患者とヘルスケアプロバイダーの両方の糖尿病のリアルタイムモニタリングと管理を強化しています。

- 例えば、Dexcom G6やAbbott FreeStyle LibreなどのCGMデバイスは、スマートフォンアプリとのシームレスな接続を提供し、ユーザーはグルコースレベルを追跡し、アラートを受信し、臨床医とリモートでデータを共有することができます。

- モバイルアプリの統合により、パーソナライズされたインサイト、トレンド分析、および高血糖値または低血糖値低下症の予測アラートを可能にし、患者の遵守と積極的な疾患管理を改善

- 糖尿病ケア機器とmHealthプラットフォームの両立により、患者データの集中管理を容易にし、臨床医が複数の患者を同時に監視し、タイムリーな介入を可能に

- 接続、インテリジェント、および患者中心の糖尿病ケアソリューションに対するこの傾向は、メドトロニックやロッシュなどの企業と、モバイル対応のインシュリンポンプとCGMシステムを開発する家庭ベースの病気管理のための期待を変革しています

- 患者やヘルスケアプロバイダが、利便性、データ主導のインサイトを優先し、リモート管理するにつれて、統合、アプリ接続されたデバイスに対する需要は、病院、診療所、およびホーム設定に急速に増加しています。

アジア・パシフィック・ダイベレス・ケア・デバイス・マーケット・ダイナミクス

ドライバー

糖尿病と病気管理の意識を高める

- 中国、インド、日本などの国々で糖尿病の普及が進んでおり、病気対策に関する意識が高まり、アジア太平洋地域における糖尿病ケア機器の採用が重要なドライバーです。

- たとえば、診断された糖尿病症例の増加は、政府やヘルスケアプロバイダが早期発見と監視プログラムを促進し、SMBGデバイスやインシュリンデリバリーシステムに対する高需要につながります。

- 患者は、高度CGMシステム、インシュリンペン、ポンプの蓄積を運転する自己監視およびインシュリン管理のための正確で、信頼できる、およびユーザー フレンドリー装置を、捜しています

- さらに、都市圏における医療インフラの拡大と保険の拡大に伴い、糖尿病ケア機器へのアクセスが広く、住宅や臨床導入の両立を支援

- 予防ケアとホームベースの監視ソリューションの高まりは、糖尿病ケアデバイスを効果的に管理し、合併症を軽減し、生活の質を向上させるための重要なツールです。

- コネクティッドインシュリンペン、AIベースのインシュリンドスリン推奨事項、およびモバイルアプリとの統合により、市場成長と患者エンゲージメントをさらに加速

拘束/チャレンジ

農村地域の高コストと限られた意識

- CGMシステムおよびインシュリンポンプを含む高度糖尿病の心配装置の比較的高い費用は、特にアジア・パシフィック諸国の開発の価格の敏感な人口間の採用への挑戦を、おおいます

- たとえば、多くの農村の患者と低所得世帯は、手頃な価格の制約による手動グルコース監視と注射に依存し、技術的に高度なデバイスの貫通を制限する

- 費用の障壁は、適切なデバイスの使用、自己監視、および半都市および地方地域の疾患管理慣行に関する限られた意識と教育によって混合されます

- ヘルスケアプロバイダーおよびデバイスメーカーは、これらの採用障壁を克服するために、患者教育プログラム、手頃な価格の製品ライン、および流通ネットワークに投資しなければなりません

- ターゲットを絞った介入がなければ、デバイスアクセシビリティと使用の分裂は、都市需要が上昇しているにもかかわらず、市場のフル成長の可能性を低下させる可能性があります

- 政府のイニシアチブ、補助金、および認知キャンペーンを通じた豊かさと意識のギャップへの対処は、多様なアジア太平洋地域における持続可能な採用の推進に不可欠です。

アジア太平洋糖尿病ケア機器市場スコープ

市場は管理装置、監視装置、エンド ユーザーおよび配分チャネルに基づいて区分されます。

- 管理デバイス別

管理装置に基づいて、市場はインシュリン ポンプ、インシュリン ペン、インシュリンのスポイトおよびジェット注入器に分けられます。 インスリンペンセグメントは、2024年に最大25%の収益シェアで市場を支配し、その利便性、使いやすさ、伝統的なシリンジと比較して移植性を促進しました。 インスリンペンは正確な投薬を可能にし、注入の不快感を減らし、そして毎日のインシュリン管理のための患者によって広く好まれます。 セグメントはまた、デジタル線量追跡アプリケーションとの互換性から恩恵を受け、家庭や臨床設定で採用を増加させます。 糖尿病の自己管理とユーザーフレンドリーなソリューションのための好みの意識を成長させ、さらにインスリンペン優勢をサポートします。 また、インスリンペンは、その信頼性とドージングエラーのリスクを削減し、病院やクリニックでますます採用されています。

インスリンポンプセグメントは、タイプ1およびタイプ2糖尿病患者の継続的なインスリン配送システムを採用することにより、2025から2032までの18%の最速成長率を目撃することを期待しています。 ポンプは精密で、プログラム可能なインシュリンの線量を提供し、自動化されたグルコース管理のためのCGMシステムと統合できます。 アドバンスAI・AI有効なポンプは予測的なインシュリン配達および高められた忍耐強い便利を可能にします。 生活の質の向上、注射の低減、およびモバイルアプリケーションとの統合のための忍耐強い好みの上昇も急速な成長に貢献します。 ヘルスケアプロバイダーは、集中的な糖尿病管理のためのインシュリンポンプをさらに推奨しています。

- 監視装置による

監視装置に基づいて、市場は自己監視血糖(SMBG)装置および連続的なブドウ糖のモニタリング(CGM)システムに分けられます。 SMBGのセグメントは、2024年に52.5%の収益シェアで市場を支配し、手頃な価格、使いやすさ、そして病院、クリニック、および家庭/個人的な設定を横断する広範な採用を支持しました。 SMBGデバイスは、毎日のグルコースの変動を監視し、それに応じてインスリンの用量やダイエットを調整するための患者のためのインスタントフィードバックを提供します。 彼らの移植性、最小限のトレーニング要件、および治療プログラムとの互換性は、多くの糖尿病患者のための最初の選択肢となります。 特に新興アジア・太平洋諸国における糖尿病の自己管理を促進する政府やNGOプログラムのメリット SMBG機器の高信頼・市場参入支援の継続的優位性を確立

CGMセグメントは、2025年から2032年までの19%の最速のCAGRを目撃し、技術の進歩とリアルタイムのグルコースモニタリングの需要が高まります。 CGMデバイスは、低血症および高血症に対する継続的なデータ、トレンドアラート、および自動通知を提供し、疾患管理結果を改善します。 モバイルアプリケーション、クラウドプラットフォーム、インシュリンポンプとの統合により、患者様の利便性と臨床的意思決定を強化します。 継続的な監視のメリットを広く認識し、ホームケアや病院の設定の採用の増加が急激な成長に貢献します。 積極的な予防ケアに投資する患者様の意欲を高めることで、CGMの採用にも対応しています。

- エンドユーザーによる

エンドユーザーに基づいて、市場は病院、クリニック、家庭/個人の設定に分けられます。 病院の区分は高度の監視およびインシュリンの配達装置の高度の監視および頻繁な使用のための高い要求に、2024年に45%のシェアが付いている市場を支配しました。 病院は構造化された心配、忍耐強い教育を提供し、技術的に高度装置にアクセスし、それらに装置の使用のための第一次チャネルを作ります。 糖尿病患者の入院率を増加させ、SMBGおよびCGM装置をインパティエントケアで採用することで、セグメントの優位性を促進します。 病院はまた、患者の付着を装置の使用に間接的に高める家ベースの自己管理のための訓練を支えます。

家庭/個人セグメントは、2025年から2032年にかけて最も速い成長率を目撃する見込みで、糖尿病のセルフケア、遠隔医療の採用、SMBG、CGM、インスリンペンへの便利なアクセスの意識が高まっています。 ユーザフレンドリーでモバイル接続されたデバイスと組み合わせて、ホームベースの監視と管理のための患者様の好みを高め、このセグメントを急速に拡大しています。 デジタルヘルスプラットフォームとのリモートモニタリングと統合の利便性は、患者のエンゲージメントと遵守を強化します。 ホームベースのケアは、病院の訪問に対する依存性を減らし、患者がその状態を積極的に管理し、セグメントの成長を促進します。

- 流通チャネル

流通チャネルに基づいて、市場は、機関の販売および小売販売に分けられます。 機関販売部門は2024年に市場を支配し、60%のシェアを持ち、病院、クリニック、および患者管理および機関プログラムのためのヘルスケア組織によるバルク購入によって支えられました。 機関チャネルは、デバイストレーニング、メンテナンス、および病院ITシステムとの統合を容易にします。 政府プログラムと糖尿病のためのNGOとのパートナーシップは、さらに、機関のチャネル優勢を強化します。

小売販売部門は、2025年から2032年までの最も速いCAGRを目撃し、薬局、オンラインプラットフォーム、および特殊な糖尿病ストアを通じてデバイスの増加の可用性によって駆動されると予想されます。 小売チャネルは、特にSMBGデバイス、インシュリンペン、CGMシステム用のデバイスに便利なアクセスを提供します。 アジア・パシフィックの電子商取引普及、消費者の認知度を高め、手頃な価格のプログラムと相まって、小売成長を加速しています。 小売販売はまた、自己管理の傾向とテレメディシンの統合に役立ちます, それらを急速に拡大チャネルにします.

アジア太平洋糖尿病ケアデバイス市場地域分析

- 中国は、2024年にアジア太平洋糖尿病治療装置市場を支配し、地域における最大の糖尿病人口による38.5%の収益分配、ヘルスケアインフラの拡大、糖尿病管理の促進、先進的な監視およびインスリン配送装置の高度採用を主導

- SMBGシステム、CGMデバイス、インスリンペンなどの先進デバイスが提供した高精度、使いやすさ、リアルタイムモニタリング能力を高度に評価し、家庭や臨床設定で効果的な糖尿病管理をサポート

- これにより、糖尿病管理の普及、糖尿病管理の普及、および、アジア・パシフィックにおける病院、クリニック、家庭/人的設定などの重要なツールとして糖尿病治療装置を整備し、より一層の普及が進んでいます。

中国糖尿病ケアデバイス市場洞察

中国は、2024年にアジア・パシフィック・糖尿病ケア機器市場を支配し、最大38.5%の収益シェアを占め、国の広大な糖尿病人口と疾患管理の意識を高めています。 病院や診療所は、SMBG機器、CGMシステム、インシュリンペンを採用し、患者ケアを改善しています。 早期診断、予防プログラム、および払い戻し方針を推進する政府の取り組みは、アクセシビリティを高めています。 アーバン化、使い捨て収入の上昇、およびモバイルヘルスプラットフォームとのデバイスの統合により、さらなる採用をサポートします。 手頃な価格の機器の国内製造も、半都市や農村の人口へのリーチを拡大します。

インド糖尿病ケアデバイス市場インサイト

インド糖尿病ケア機器市場は、急速な都市化、糖尿病の蔓延の増加、中級人口の増加によって推進され、2024年に著しいシェアを獲得しました。 病院、クリニック、ホームセッティングなど、SMBG機器やインシュリンペンが広く使用されています。 政府主導の健康プログラム、認知キャンペーン、および治療の採用により、患者のアクセスとエンゲージメントを高めます。 国内メーカーの手頃な価格のデバイスオプションと小売および電子商取引チャネルの拡大により、市場成長をさらに加速します。 スマートなヘルスケアのインフラへの押しは高度CGMシステムおよび接続されたインシュリン配達装置を採用します。

日本糖尿病ケア機器市場情報

日本糖尿病ケア機器市場は、高齢化の人口と強固なヘルスケア意識の中で糖尿病の有病率が高まっています。 CGM システムおよびインシュリン ポンプは精密なブドウ糖管理のための病院、医院およびホーム設定でますます採用されます。 モバイルアプリケーションとテレメディシンプラットフォームとの統合により、患者の監視と遵守が向上します。 革新的なテクノロジー主導のヘルスケアソリューションは、コネクティッド、ユーザーフレンドリーなデバイスの採用を促進します。 都市化とライフスタイルの変化を上げることで、家庭ベースの糖尿病ケアソリューションの需要が高まっています。

韓国糖尿病ケアデバイス市場インサイト

韓国糖尿病ケア機器市場は、糖尿病の予防と強力な医療インフラの上昇による大きな成長を目撃しています。 病院やクリニックは、SMBGとCGMシステムの主要ユーザーであり、インシュリンペンとポンプは、ホームユーザーの間で人気を博しています。 糖尿病の意識、予防プログラム、および償還支援の採用を促進する政府の取り組み。 テクノロジーに精通した人口は、モバイル接続とアプリ統合デバイスを支持し、市場浸透を促進します。 高度、ユーザーフレンドリーな糖尿病ケアソリューションのための都市化と高い使い捨て所得のさらなるドライブ需要の増加。

アジア太平洋糖尿病ケアデバイス市場シェア

アジア・パシフィック・ダイベレス・ケア・デバイス・業界は、主に、以下を含む広範な企業によって導かれています。

- アボット(米国)

- 株式会社デックスコム(米国)

- Medtronic(アイルランド)

- F.ホフマン・ラ・ロチェ株式会社(スイス)

- 株式会社インスレット(米国)

- 株式会社センスニックス(米国)

- アセンシア糖尿病ケア(スイス)

- Ypsomed AG(スイス)

- 株式会社アークレイ(日本)

- Sinocare Inc.(中国)

- 株式会社ニプロ(日本)

- BD(アメリカ)

- ノボノルディスク A/S(デンマーク)

- サンオフィ(フランス)

- エリ・リリー・アンド・カンパニー(米国)

- 株式会社テルモ(日本)

- 株式会社ライフスキャン(米国)

- 株式会社オムロンヘルスケア(日本)

- B. ブラウンSE(ドイツ)

アジア太平洋糖尿病ケアデバイス市場における最近の発展とは?

- 2025年8月、Abbottは、インドのFreeStyle Libre 2 Plusセンサーを発売し、NFCとBluetooth経由でスマートフォンアプリに毎分自動グルコース読み取りを提供し、オプションのアラームと15日間のウェアラブルセンサーフォーマット

- 2025年7月、MNNIT PrayagrajとRam Manohar Lohia Institute of Medical Sciencesの研究者、Lucknowは新しい非侵襲的なグルコース監視装置を発表しました。これにより、指のつまみとインデックスフィンガーの間に設置された電磁センシングを使用して、指のつまみの必要性を排除します。 投影された費用は、特に低所得糖尿病患者の患者にアクセス可能である

- 2025年6月、Tracky(DrStore Healthcare Servicesのヘルステックブランド)は、インド初のBluetooth接続連続グルコースモニターを発売し、スマートフォンによるリアルタイムでスキャンフリーグルコース追跡、予防的な健康と広範なアクセシビリティをターゲットに

- 2025年4月、Ambrosiaは、インド初の24×7リアルタイムグルコース&ストレスモニタリングサービスを導入し、ウェアラブルセンサー、AI分析、リモートモニタリングによる継続的なグルコースモニタリングと統合デジタルヘルスサービスのストレスモニタリングを効果的に組み合わせました。

- 2024年7月、デンマークの糖尿病会社ノボノルディスクは、インドネシアの州有地バイオファーマとの理解の覚書に署名し、地域糖尿病治療サプライチェーンを強化し、東南アジアにおけるインシュリン療法へのアクセスを改善する

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。