North America Dental Equipment Market Size, Share and Trends Analysis Report

Market Size in USD Billion

CAGR :

%

USD

2.83 Billion

USD

4.24 Billion

2025

2033

USD

2.83 Billion

USD

4.24 Billion

2025

2033

| 2026 –2033 | |

| USD 2.83 Billion | |

| USD 4.24 Billion | |

| % | |

|

North America Dental Equipment Market Segmentation By Product (Diagnostic Dental Equipment and Therapeutic Dental Equipment), Treatment (Orthodontic, Endodontic, Peridontic, Prosthodontic), End User (Hospitals and Clinics, Dental Laboratories, and Other) - Industry Trends and Forecast to 2033

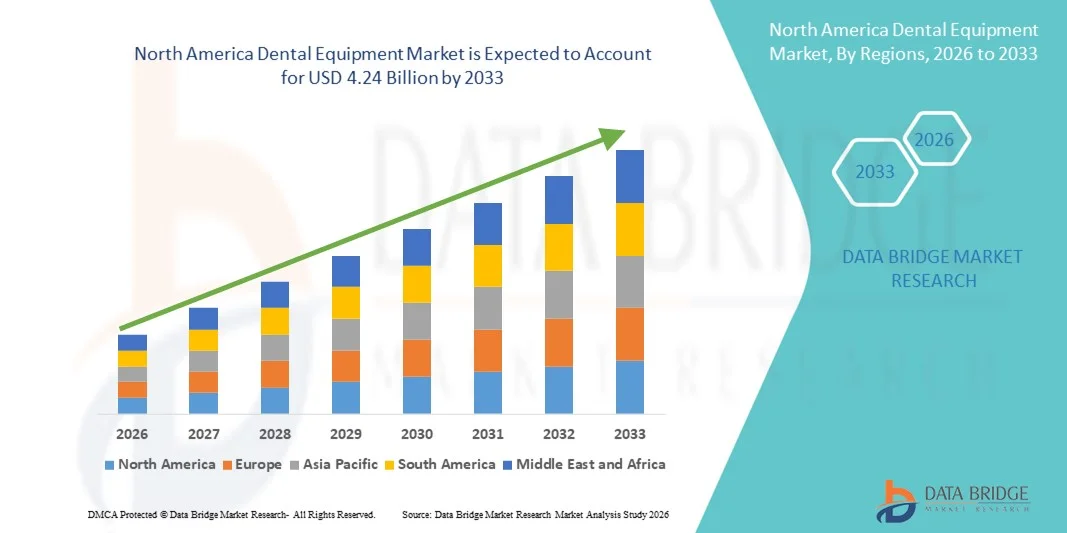

North America Dental Equipment Market Size

- The North America dental equipment market size was valued at USD 2.83 billion in 2025 and is expected to reach USD 4.24 billion by 2033, at a CAGR of 5.17% during the forecast period

- The market growth is largely fueled by the increasing prevalence of dental disorders, rising awareness of oral hygiene, and continuous technological advancements in dental treatment systems, leading to improved clinical efficiency and patient care across dental clinics and hospitals

- Furthermore, growing demand for minimally invasive and cosmetic dental procedures, increasing investments in modern dental infrastructure, and rising adoption of digitally integrated dental equipment are establishing advanced dental systems as essential components of contemporary dental practice. These converging factors are accelerating the uptake of Dental Equipment solutions, thereby significantly boosting the industry's growth

North America Dental Equipment Market Analysis

- Dental equipment, including dental chairs, handpieces, CAD/CAM systems, and sterilization units, are increasingly vital components of modern dental clinics and hospitals due to their role in improving treatment precision, workflow efficiency, and patient comfort

- The escalating demand for dental equipment is primarily fueled by the rising prevalence of dental disorders, growing awareness of preventive oral care, increasing demand for cosmetic dentistry, and continuous technological advancements in digitally integrated dental systems

- The U.K. dominated the dental equipment market with the largest revenue share of 29.8% in 2025, characterized by advanced dental care infrastructure, high adoption of digital dentistry solutions, strong presence of established dental equipment manufacturers, and increasing demand for cosmetic, restorative, and preventive dental procedures across NHS-supported and private clinics. Growing integration of CAD/CAM systems, digital scanners, and advanced dental chairs further strengthens the country’s leadership position

- Germany is expected to be the fastest-growing country in the Dental Equipment market during the forecast period, expanding at a CAGR of 9.2% from 2026 to 2033, driven by rising investments in dental clinic modernization, increasing awareness of oral healthcare, strong domestic manufacturing capabilities, and growing adoption of technologically advanced treatment systems across urban and semi-urban regions

- The therapeutic dental equipment segment dominated the largest market revenue share of 57.3% in 2025, driven by the high volume of restorative, surgical, and cosmetic dental procedures performed globally

Report Scope and Dental Equipment Market Segmentation

|

Attributes |

Dental Equipment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

• Dentsply Sirona Inc. (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Dental Equipment Market Trends

Technological Advancements and Digital Transformation in Dental Practices

- A significant and accelerating trend in the dental equipment market is the rapid shift toward technologically advanced and fully digital dental systems. Modern dental clinics are increasingly adopting innovative equipment such as digital chairs with integrated delivery systems, electric handpieces, laser dentistry devices, and computer-assisted treatment units to enhance precision, efficiency, and patient comfort

- For instance, the growing adoption of CAD/CAM systems in restorative dentistry enables same-day crown fabrication, reducing treatment time and improving clinical workflow efficiency. Similarly, advanced dental lasers are being widely used for soft tissue surgeries and periodontal treatments, minimizing bleeding, discomfort, and recovery time for patients

- The integration of ergonomic and patient-centric equipment designs is also transforming dental environments. Modern dental chairs now feature programmable positioning, improved lumbar support, and integrated imaging displays, allowing clinicians to perform procedures more comfortably while enhancing the overall patient experience

- Furthermore, automation and digital connectivity across equipment platforms are streamlining practice management. Dental units connected with practice management software enable better treatment planning, electronic record maintenance, and improved diagnostic coordination, thereby enhancing operational productivity

- The increasing preference for minimally invasive and high-precision procedures is encouraging manufacturers to develop advanced instruments that offer superior control and reduced procedure times. This technological evolution is reshaping clinical standards and raising expectations for quality dental care delivery

- Overall, the transition toward advanced, efficient, and digitally integrated dental equipment is strengthening clinical outcomes and redefining operational efficiency within dental practices across the region

North America Dental Equipment Market Dynamics

Driver

Rising Prevalence of Dental Disorders and Expanding Cosmetic Dentistry Demand

- The increasing incidence of dental disorders, including cavities, periodontal diseases, tooth loss, and oral infections, is a primary driver fueling growth in the Dental Equipment market. Growing awareness about oral hygiene and preventive dental care has led to a higher number of dental visits globally

- For instance, the rising number of dental implant placements and orthodontic treatments has significantly increased demand for specialized surgical instruments, dental chairs, sterilization systems, and endodontic equipment across clinics and specialty centers

- The rapid growth of cosmetic dentistry, including procedures such as teeth whitening, veneers, and smile makeovers, is further accelerating equipment upgrades in private dental practices. Cosmetic treatments require advanced polishing systems, imaging-compatible chairs, and high-precision instruments to deliver aesthetic accuracy

- In addition, the expanding geriatric population, which is more susceptible to tooth decay, edentulism, and gum diseases, is creating sustained demand for restorative and prosthodontic equipment. Aging demographics are contributing to higher volumes of denture fittings, implants, and periodontal treatments

- Increasing healthcare expenditure, growth of dental service organizations (DSOs), and expansion of multi-specialty dental clinics are also encouraging investments in modern equipment infrastructure. Many clinics are upgrading to technologically advanced systems to remain competitive and enhance service delivery

- Together, these factors—rising disease prevalence, aesthetic awareness, and expanding dental service networks—are strongly propelling the Dental Equipment market forward

Restraint/Challenge

High Capital Investment and Equipment Maintenance Costs

- The high initial cost associated with advanced dental equipment remains a significant challenge for market expansion, particularly for small and independent dental practices. Sophisticated systems such as CAD/CAM units, dental lasers, and implantology equipment require substantial upfront capital investment

- For instance, establishing a fully equipped modern dental operatory involves expenses related not only to treatment units but also to sterilization systems, suction units, compressors, and specialized instruments, which can strain financial resources for new or small-scale clinics

- Ongoing maintenance, calibration, and equipment servicing costs further add to operational expenses. Regular replacement of components and compliance with safety and sterilization standards increase the total cost of ownership over time

- Limited access to financing options in certain developing regions may restrict the ability of dental professionals to invest in technologically advanced systems, slowing adoption rates in emerging markets

- In addition, rapid technological advancements can lead to equipment obsolescence, compelling clinics to upgrade systems frequently to maintain competitive standards and meet evolving patient expectations

- Addressing these financial and operational challenges through flexible financing models, equipment leasing options, and cost-effective technological innovations will be crucial to ensuring sustainable growth in the Dental Equipment market

North America Dental Equipment Market Scope

The market is segmented on the basis of product, treatment, and end user.

- By Product

On the basis of product, the Dental Equipment market is segmented into diagnostic dental equipment and therapeutic dental equipment. The therapeutic dental equipment segment dominated the largest market revenue share of 57.3% in 2025, driven by the high volume of restorative, surgical, and cosmetic dental procedures performed globally. Therapeutic equipment such as dental chairs, handpieces, lasers, and CAD/CAM systems are essential for treatment delivery. Rising prevalence of dental caries, periodontal diseases, and tooth loss significantly supports demand. Increasing adoption of minimally invasive procedures further accelerates equipment utilization. Growing geriatric population requiring restorative treatments strengthens segment growth. Technological advancements improving precision and efficiency enhance adoption. Expansion of private dental clinics globally boosts procurement rates. Higher patient spending on cosmetic and implant procedures sustains revenue generation. Integration of digital workflows in treatment planning supports equipment upgrades. Favorable reimbursement in developed regions further contributes to dominance. Continuous innovation in ergonomic and automated systems consolidates market leadership. Overall, increasing procedure volumes and technological advancements maintain the segment’s leading position.

The diagnostic dental equipment segment is anticipated to witness the fastest CAGR of 9.8% from 2026 to 2033, fueled by rising emphasis on early disease detection and preventive dentistry. Increasing routine dental check-ups globally drive demand for advanced diagnostic tools. Technological advancements in digital imaging and chairside diagnostics enhance accuracy. Growing awareness about oral health supports higher screening rates. Expansion of dental insurance coverage in emerging economies encourages early diagnosis. Rising integration of AI-based diagnostic systems accelerates adoption. Demand for compact and portable diagnostic devices boosts installations in small clinics. Government oral health programs further stimulate growth. Increasing dental tourism contributes to higher diagnostic equipment usage. Collaboration between manufacturers and dental service organizations strengthens distribution. Continuous upgrades from analog to digital diagnostic systems support expansion. Overall, preventive care trends and technological innovation position diagnostic equipment as the fastest-growing segment.

- By Treatment

On the basis of treatment, the Dental Equipment market is segmented into orthodontic, endodontic, periodontic, and prosthodontic. The prosthodontic segment dominated the largest market revenue share of 34.6% in 2025, driven by rising demand for dental implants, crowns, and bridges. Increasing tooth loss among the aging population significantly supports growth. Growing awareness regarding aesthetic restoration enhances procedure volumes. Technological advancements in implant systems and CAD/CAM prosthetics improve outcomes. Rising disposable income in developing regions fuels cosmetic and restorative dentistry demand. Expansion of specialized prosthodontic clinics strengthens equipment adoption. Increasing dental tourism supports higher procedure rates. Integration of digital impression systems enhances workflow efficiency. Favorable reimbursement policies in developed markets further drive growth. Continuous product innovation improves durability and patient comfort. Rising prevalence of lifestyle-related dental issues supports sustained demand. Overall, the segment maintains dominance due to high-value restorative procedures.

The orthodontic segment is expected to register the fastest CAGR of 10.7% from 2026 to 2033, driven by increasing demand for clear aligners and aesthetic braces. Growing awareness about dental aesthetics among adolescents and adults accelerates growth. Technological advancements in digital scanning and 3D printing enhance treatment precision. Rising disposable income supports elective orthodontic treatments. Expansion of orthodontic specialty clinics globally boosts equipment demand. Increasing social media influence drives smile correction procedures. Growing adoption of minimally visible orthodontic solutions strengthens uptake. Advancements in treatment planning software improve clinical efficiency. Rising prevalence of malocclusion cases supports demand. Collaborations between dental equipment manufacturers and orthodontic service providers enhance availability. Continuous innovation in aligner technology sustains growth momentum. Overall, aesthetic-driven demand positions orthodontics as the fastest-growing treatment segment.

- By End User

On the basis of end user, the Dental Equipment market is segmented into hospitals and clinics, dental laboratories, and other end users. The hospitals and clinics segment held the largest market revenue share of 61.2% in 2025, supported by high patient footfall and comprehensive treatment facilities. Increasing number of private dental clinics globally drives equipment installations. Growing prevalence of oral diseases sustains demand for advanced dental systems. Availability of skilled professionals enhances service capacity. Integration of digital and automated equipment improves efficiency. Rising adoption of cosmetic and implant procedures boosts revenue generation. Government investments in public dental healthcare infrastructure strengthen growth. Favorable reimbursement frameworks in developed regions support utilization. Expansion of multi-specialty dental chains accelerates procurement. Continuous equipment upgrades ensure competitive service offerings. Increasing patient awareness about preventive care drives clinic visits. Overall, centralized treatment capabilities maintain segment dominance.

The dental laboratories segment is anticipated to witness the fastest CAGR of 9.5% from 2026 to 2033, driven by rising demand for customized prosthetics and orthodontic appliances. Increasing adoption of CAD/CAM and 3D printing technologies accelerates growth. Growing collaboration between clinics and laboratories enhances workflow integration. Rising volume of restorative and cosmetic procedures boosts laboratory output. Technological advancements improve production efficiency and precision. Expansion of dental outsourcing services strengthens segment demand. Increasing focus on high-quality aesthetic restorations supports growth. Investment in digital manufacturing systems enhances productivity. Growing dental tourism in emerging economies contributes to laboratory expansion. Continuous innovation in materials and fabrication techniques sustains growth. Rising demand for personalized dental solutions further accelerates CAGR. Overall, digital transformation and customization trends position dental laboratories as the fastest-growing end user segment.

North America Dental Equipment Market Regional Analysis

- Europe dominated the dental equipment market with the largest revenue share of 34.6% in 2025, driven by its highly developed dental healthcare infrastructure, strong presence of specialized dental clinics, and continuous technological advancements in treatment systems. The region benefits from high patient awareness regarding preventive and restorative dental care, which has led to increased demand for advanced dental chairs, handpieces, sterilization systems, and CAD/CAM equipment. In addition, the growing volume of cosmetic dentistry procedures and implant surgeries has significantly contributed to consistent upgrading of dental equipment across clinics and specialty center

- The region’s leadership is further supported by substantial healthcare expenditure, early adoption of digital dentistry solutions, and expansion of multi-specialty dental service organizations. Dental professionals across Europe are increasingly investing in ergonomic and digitally integrated equipment to enhance procedural precision, reduce treatment time, and improve patient comfort. The presence of leading dental equipment manufacturers and strong distribution networks also strengthens market growth and innovation in the region

- Moreover, the rising geriatric population and increasing incidence of dental disorders such as periodontal disease and edentulism continue to drive the need for restorative and prosthodontic equipment. Continuous investments in clinic modernization and regulatory compliance standards further reinforce Europe’s dominant position in the global Dental Equipment market

U.K. Dental Equipment Market Insight

The U.K. dental equipment market dominated the European Dental Equipment market with the largest revenue share of 29.8% in 2025, characterized by advanced dental care infrastructure, high adoption of digital dentistry solutions, strong presence of established dental equipment manufacturers, and increasing demand for cosmetic, restorative, and preventive dental procedures across NHS-supported and private clinics. The country has witnessed significant integration of CAD/CAM systems, digital scanners, advanced dental chairs, and implantology equipment to improve workflow efficiency and patient outcomes. Growing emphasis on preventive dentistry and modernization of dental practices continues to strengthen the U.K.’s leadership position.

Germany Dental Equipment Market Insight

Germany dental equipment market is expected to be the fastest-growing country in the European Dental Equipment market during the forecast period, expanding at a CAGR of 9.2% from 2026 to 2033. Growth is driven by rising investments in dental clinic modernization, increasing awareness of oral healthcare, strong domestic manufacturing capabilities, and growing adoption of technologically advanced treatment systems across urban and semi-urban regions. Expanding demand for implantology, prosthodontics, and aesthetic dentistry, along with integration of digital workflows, is expected to significantly contribute to sustained market expansion in Germany throughout the forecast period.

North America Dental Equipment Market Share

The Dental Equipment industry is primarily led by well-established companies, including:

- Dentsply Sirona Inc. (U.S.)

- Envista Holdings Corporation (U.S.)

- 3M Company (U.S.)

- Henry Schein, Inc. (U.S.)

- Planmeca Oy (Finland)

- KaVo Dental GmbH (Germany)

- Align Technology, Inc. (U.S.)

- Carestream Dental LLC (U.S.)

- Midmark Corporation (U.S.)

- GC Corporation (Japan)

- Ivoclar Vivadent AG (Liechtenstein)

- Acteon Group (France)

- NSK Ltd. (Japan)

- Yoshida Dental Mfg. Co., Ltd. (Japan)

- Coltene Group (Switzerland)

- Belmont Equipment (U.S.)

- Vatech Co., Ltd. (South Korea)

- Septodont Holding (France)

- Young Innovations, Inc. (U.S.)

- Shofu Inc. (Japan)

Latest Developments in North America Dental Equipment Market

- In March 2025, Planmeca unveiled a completely new generation of dental units at IDS 2025, including the Pro40 chair unit, enhanced CAD/CAM workflow integrations, and new CBCT and intra-oral imaging devices within its Viso family — along with updates to Romexis® imaging and planning software to support digital dentistry

- In March 2025, KaVo presented a range of innovations under its “Elements of Excellence” campaign at IDS 2025: the new amiQa dental unit, enhanced ProXam imaging systems (Pro and 3DQ Pro), and AI-driven analysis tools (ProFace & ProCeph) integrated into practice software to improve diagnostics and workflow efficiency

- In February 2025, Carestream Dental introduced enhancements in CBCT imaging, implant planning, and AI-driven software tools, including integration with Pearl AI, aimed at advancing diagnostic accuracy and practice productivity in dental radiology

- In January 2025, Septodont Inc. and Premier Dental launched BufferPro, a new sterile single-use buffering solution that optimizes local anesthetic performance in dentistry by raising pH for faster onset and improved patient comfort

- In January 2024, Planmeca announced the acquisition of a leading dental imaging software company to expand its digital imaging and data management capabilities — reinforcing its position in integrated dental equipment solutions

- In July 2024, Henry Schein and Align Technology’s collaboration highlighted the integration of digital scanning and clinical workflow platforms, driving broader adoption of digital diagnostics and restorative planning tools in practices

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。