欧州医療機器保守市場の規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

73.22 Billion

USD

153.56 Billion

2025

2033

USD

73.22 Billion

USD

153.56 Billion

2025

2033

| 2026 –2033 | |

| USD 73.22 Billion | |

| USD 153.56 Billion | |

| % | |

|

欧州医療機器保守市場のセグメンテーション:サービスタイプ別(予防保守、是正保守、性能/運用保守)、サービスプロバイダー別(社内サービスプロバイダー、外部サービスプロバイダー)、機器タイプ別(画像診断装置、内視鏡機器、電気医療機器、外科手術器具、その他の医療機器)、保守レベル別(レベル3、専門保守、レベル2、技術者、レベル1、ユーザー(または第一線))、エンドユーザー別(病院、診療所、検査室、その他の医療センター)-業界動向と2033年までの予測

欧州医療機器保守市場規模

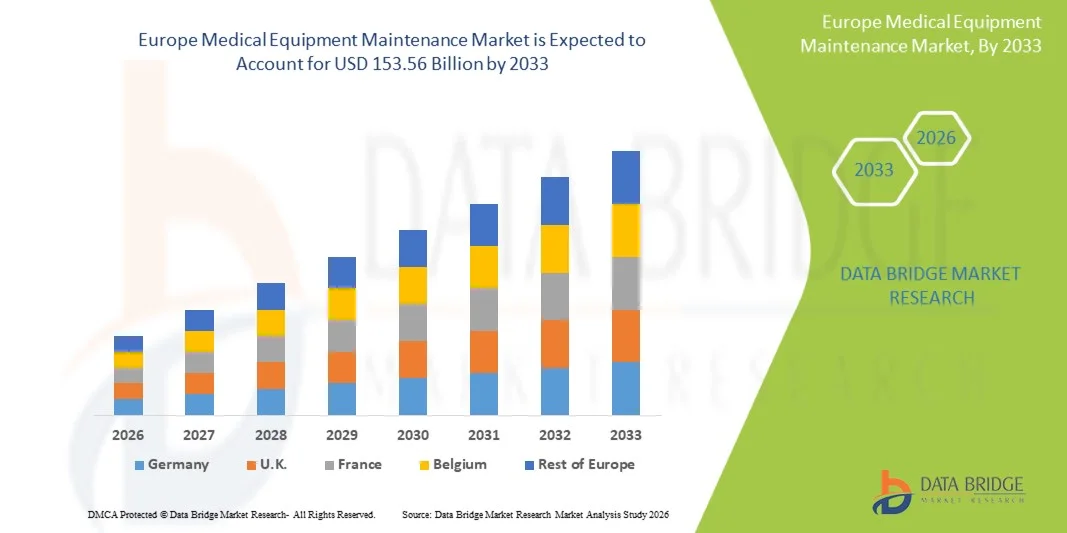

- 欧州の医療機器保守市場規模は、2025年には732億2000万米ドルと評価され、予測期間中の年平均成長率(CAGR)9.70%で、2033年には1535億6000万米ドル に達すると予測されている 。

- 市場の成長は、病院や診断センターにおける高度な医療機器の導入増加に加え、医療施設全体で機器の信頼性、規制遵守、患者の安全性を確保する必要性の高まりによって大きく促進されている。

- さらに、医療機関による予防保守サービス、機器ライフサイクル管理、および技術サポートのアウトソーシングへの重視の高まりは、専門的な保守ソリューションを現代の医療インフラの重要な構成要素として確立しつつあります。これらの要因が複合的に作用することで、医療機器保守サービスの導入が加速し、業界の成長を大きく促進しています。

欧州医療機器保守市場分析

- 診断・治療機器の点検、校正、修理、予防保守を含む医療機器保守サービスは、ヨーロッパ中の医療システムにおいて、病院、検査室、専門クリニックにおける業務効率、規制遵守、患者の安全を確保するためにますます不可欠となっている。

- 医療機器の保守に対する需要の高まりは、主に、技術的に高度な医療機器の導入の増加、医療提供者に対する機器のダウンタイムを最小限に抑えるという圧力の高まり、そして高額な医療資産の運用寿命を延ばす必要性の高まりによって促進されている。

- ドイツは、2025年に欧州の医療機器保守市場において最大の収益シェア38.7%を占め、市場を席巻した。これは、強力な医療インフラ、高い医療機器普及率、そして主要な医療技術企業の存在が特徴であり、病院や診断センターは効率性の向上と運用コストの削減のために、保守サービスを専門業者にアウトソーシングするケースが増えている。

- 英国は、医療インフラへの投資の増加、診断サービスの拡大、そして厳格な医療規制への準拠を維持するための予防的な機器保守への注目の高まりにより、予測期間中、欧州の医療機器保守部門で最も急速に成長する市場の一つになると予想されています。

- 予防保全分野は、2025年に欧州医療機器保守市場で45.3%の市場シェアを占め、市場を牽引しました。これは、医療施設が機器のダウンタイムを削減し、重要な医療機器の継続的な運用を確保するために、定期点検、早期故障検出、計画的な保守にますます注力していることが要因です。

レポートの範囲と欧州医療機器保守市場のセグメンテーション

|

属性 |

欧州医療機器メンテナンス市場の主要インサイト |

|

対象分野 |

|

|

対象国 |

ヨーロッパ

|

|

主要市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

Data Bridge Market Researchが作成した市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要企業などの市場シナリオに関する洞察に加え、専門家による詳細な分析、患者疫学、パイプライン分析、価格分析、規制枠組みも含まれています。 |

欧州医療機器保守市場の動向

「IoTと予知保全技術の導入」

- 欧州の医療機器保守市場における重要かつ加速的なトレンドは、IoT対応デバイスと予測保守プラットフォームの導入拡大であり、これにより機器の性能を継続的に監視し、潜在的な故障を早期に検出することが可能になる。

- 例えば、GEヘルスケアのIoT対応画像システムは、キャリブレーションや部品の摩耗に関するリアルタイムのアラートを提供し、病院が事前にメンテナンスを計画し、ダウンタイムを最小限に抑えることを可能にします。

- 予測分析の統合により、保守サービス提供者はサービススケジュールを最適化し、予期せぬ故障を減らし、機器の寿命を延ばすことができるだけでなく、使用パターンや機器の効率に関する実用的な洞察も得ることができます。

- 保守プラットフォームと病院情報システムのシームレスな統合により、部門横断的な複数の機器の一元的な追跡が可能になり、規制基準への準拠が確保され、運用効率が向上します。

- クラウドベースの保守ソリューションの利用拡大により、機器データへのリモートアクセスが可能になり、集中監視と是正措置への迅速な対応が可能になる。

- デバイスメーカーとサードパーティの保守プロバイダーとの連携が強化され、ソフトウェアアップデート、キャリブレーション、オンサイトサービスを含む包括的なソリューションが提供され、より統合されたサービスモデルが構築されている。

- コネクテッドでデータ駆動型の予測保守ソリューションへのこうした傾向は、医療施設の運営に対する期待を根本的に変革し、医療提供者がよりスマートなサービスモデルを採用するよう促している。

- IoTベースの予測保守とAI支援型モニタリングに対する需要は、医療管理者が機器の継続的な機能と費用対効果の高いサービスをますます重視するようになるにつれて、病院、診断検査機関、専門クリニック全体で急速に高まっている。

欧州医療機器保守市場の動向

ドライバ

「機器の複雑化と規制基準の強化に伴う需要増加」

- 医療機器の複雑化が進むにつれ、運用上の信頼性と患者の安全性に関する厳格な規制要件が加わり、専門的な機器保守サービスの需要が高まっている。

- 例えば、シーメンス・ヘルスケアーズは、EUの医療機器規制に対応し、運用リスクを低減するために、高度な画像処理機器および検査機器の予防保守プログラムを拡大していると報告した。

- 医療施設が高度な診断・治療機器に投資するにつれ、ダウンタイムを最小限に抑え、ISOおよびMDR規格への準拠を確保する必要性から、病院は専門の保守業者に頼らざるを得なくなっている。

- さらに、ヨーロッパ全域における病院インフラの拡張と外来診断センターの増加は、設置済み機器の定期保守契約の普及率向上に貢献している。

- 遠隔監視、校正、緊急修理などのアウトソーシングサービス契約の利便性、コスト最適化、および機器のライフサイクル延長は、公的および民間の医療施設の両方で市場成長を促進する重要な要因となっている。

- 管理者の間で業務効率、患者安全、規制遵守に関する意識が高まっていることは、ヨーロッパにおける医療機器専門保守サービスの拡大をさらに後押ししている。

- ヨーロッパ全域における高度な医療インフラとデジタル病院構想への投資の増加は、臨床業務の中断を防ぐための信頼性の高い保守サービスへの需要をさらに高めている。

- 高額医療機器の購入ではなくリースという傾向は、保守サービス提供業者にとって新たな機会を生み出している。リース契約には保守サービス契約が含まれることが多く、定期的なメンテナンスとダウンタイムの最小化が保証されるためだ。

抑制/挑戦

「高額な維持費と熟練労働者の不足」

- 高度な医療機器の専門的な保守サービスの費用が比較的高額であることは、特に小規模な診療所や予算に制約のある医療施設にとって、普及の妨げとなっている。

- 例えば、フィリップスやキヤノンが提供するハイエンドのMRIやCTスキャナーの保守契約には多額の年間費用がかかるため、中規模病院での導入が制限される場合がある。

- さらに、ヨーロッパでは熟練した生物医学エンジニアや認定技術者が不足しているため、予防保守や是正保守のタイムリーな実施が制限され、機器のダウンタイムが増加する可能性がある。

- ISO 13485やEU MDRなどの厳格な規制基準を遵守しつつ、タイムリーな保守サービスを提供することは、業務の複雑さを増し、一部の医療機関がサービスのアウトソーシングを躊躇する要因となる可能性がある。

- 費用対効果が高く、研修に重点を置いたソリューションもいくつか登場しているものの、サービス料金の高さや資格のある人材の不足といった認識が、特に都市化が進んでいない地域では、普及を阻害し続けている。

- 人材育成、コスト最適化、およびテクノロジーを活用したサービスソリューションを通じてこれらの課題を克服することは、欧州医療機器保守市場の持続的な成長にとって不可欠となるでしょう。

- 異なるプロバイダー間での保守基準とサービス品質のばらつきは、医療施設間の不整合や信頼の低下を招き、市場拡大を制限する可能性がある。

- Budgetary constraints and delayed government reimbursements for public hospitals may restrict spending on comprehensive maintenance services, slowing adoption rates in certain European regions

Europe Medical Equipment Maintenance Market Scope

The market is segmented on the basis of service type, service providers, device type, level of maintenance, and end user.

- By Service Type

On the basis of service type, the Europe medical equipment maintenance market is segmented into preventive, corrective, and performance/operational maintenance. The preventive maintenance segment dominated the market with the largest share of 45.3% in 2025, driven by the growing emphasis on scheduled inspections, calibration, and early fault detection to minimize equipment downtime. Hospitals and diagnostic centers prioritize preventive maintenance to comply with regulatory standards and ensure uninterrupted operation of critical devices such as MRI and CT scanners. Preventive maintenance also extends the lifecycle of expensive medical equipment and reduces the risk of sudden failures, making it a preferred choice among large healthcare facilities. In addition, predictive maintenance technologies, including IoT-enabled monitoring, are increasingly being integrated within preventive services, further enhancing their adoption. The segment’s growth is supported by both public and private healthcare institutions seeking cost-efficient and reliable maintenance strategies.

The corrective maintenance segment is expected to witness the fastest growth during 2026–2033, driven by the rising adoption of complex and high-tech medical devices that require rapid repair services to minimize operational disruption. Corrective maintenance addresses unexpected equipment failures and ensures that hospitals maintain continuity in patient care. With increasing reliance on advanced imaging and surgical equipment, timely corrective services are critical to prevent clinical delays. Growth is further fueled by the outsourcing of repair services to specialized providers and the adoption of service contracts that include emergency support. Healthcare facilities in fast-developing regions are particularly adopting corrective maintenance due to increasing device complexity and operational pressure.

- By Service Providers

On the basis of service providers, the market is segmented into in-house service providers and external service providers. The external service providers segment dominated the Europe medical equipment maintenance market with the largest revenue share in 2025, owing to hospitals and clinics increasingly outsourcing maintenance to specialized third-party companies. Outsourcing ensures access to certified technicians, compliance with regulatory standards, and timely service for high-value medical devices without the burden of hiring and training in-house staff. External providers often offer comprehensive contracts covering preventive, corrective, and performance maintenance, along with software updates and calibration services. The growing complexity of medical devices and the rise in IoT-enabled equipment are further encouraging hospitals to rely on external expertise. In addition, outsourcing allows healthcare facilities to optimize operational costs while ensuring minimal equipment downtime.

The in-house service providers segment is anticipated to witness the fastest growth over the forecast period, driven by large hospitals and healthcare chains aiming to reduce dependency on external vendors and retain control over critical equipment servicing. In-house teams allow rapid response to equipment issues, improve turnaround time for maintenance requests, and ensure closer monitoring of device performance. Growth is supported by the increasing availability of training programs for biomedical engineers and technicians within Europe. Hospitals in Germany, France, and the UK are investing in internal maintenance capabilities for key devices, particularly imaging and surgical equipment, to enhance operational reliability and compliance with strict medical regulations.

- By Device Type

On the basis of device type, the Europe medical equipment maintenance market is segmented into imaging equipment, endoscopic devices, electromedical equipment, surgical instruments, and other medical equipment. The imaging equipment segment dominated the market in 2025, owing to the high cost, complexity, and critical nature of devices such as MRI, CT, and X-ray machines. Maintenance of imaging equipment is essential for accurate diagnostics, patient safety, and regulatory compliance. Hospitals and diagnostic centers prioritize preventive and corrective maintenance contracts to minimize downtime, reduce repair costs, and extend equipment lifespan. The growing adoption of high-tech imaging systems across Europe, combined with predictive maintenance technologies, further drives market dominance. In addition, equipment manufacturers and service providers offer integrated maintenance packages, ensuring continuous device performance.

The surgical instruments segment is expected to witness the fastest growth during 2026–2033, driven by the rising number of minimally invasive surgeries and adoption of advanced robotic-assisted surgical systems. Surgical instruments require frequent inspection, calibration, and sterilization to ensure precision and patient safety, making maintenance services increasingly critical. Growth is further fueled by the expanding number of surgical procedures and the need for highly specialized maintenance providers. The integration of smart monitoring and IoT-based tracking for surgical tools is also contributing to rapid adoption. Healthcare facilities in countries such as the UK, France, and the Nordics are increasingly investing in professional maintenance services for surgical instruments to enhance procedural efficiency and reduce operational risks.

- By Level of Maintenance

On the basis of level of maintenance, the market is segmented into Level 3 (Specialized), Level 2 (Technician), and Level 1 (User or First-line). The Level 3 (Specialized) segment dominated the market with the largest share in 2025, driven by the need for highly trained engineers to service complex medical devices such as MRI, CT scanners, and robotic surgical systems. Specialized maintenance ensures regulatory compliance, precise calibration, and timely repairs for high-value equipment, reducing operational risks in critical care settings. Providers of Level 3 services often offer bundled preventive and corrective maintenance contracts, which are preferred by large hospitals and diagnostic chains. The segment’s growth is further supported by the increasing reliance on advanced equipment with sophisticated software and electronic components that require expert handling.

The Level 1 (User or First-line) segment is expected to witness the fastest growth during 2026–2033, due to rising adoption of user-friendly monitoring tools and self-service maintenance protocols for basic medical devices. Hospitals and clinics are encouraging first-line personnel to perform routine inspections, cleaning, and minor troubleshooting to reduce dependency on specialized engineers and improve response time. Growth is further accelerated by the development of smart IoT-enabled devices that provide automated alerts, enabling non-specialists to perform initial maintenance actions effectively. This trend is particularly prominent in outpatient clinics, laboratory setups, and smaller healthcare centers.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, laboratories, and other healthcare centers. The hospitals segment dominated the Europe medical equipment maintenance market in 2025, accounting for the largest revenue share due to the high concentration of advanced diagnostic, imaging, and surgical equipment. Hospitals require comprehensive maintenance services, including preventive, corrective, and performance maintenance, to ensure uninterrupted clinical operations and patient safety. The high cost and complexity of medical devices, combined with strict regulatory compliance requirements, make hospitals the primary consumers of professional maintenance services. Large hospital chains are increasingly adopting service contracts with external providers and integrating predictive maintenance technologies to minimize downtime and optimize operational efficiency.

The clinics segment is anticipated to witness the fastest growth during 2026–2033, driven by the expansion of outpatient diagnostic centers, specialty clinics, and smaller healthcare facilities across Europe. Clinics increasingly rely on advanced medical devices such as ultrasound, endoscopic, and laboratory equipment, which require regular maintenance to ensure performance and safety. Growth is further supported by the outsourcing of maintenance services and adoption of IoT-enabled monitoring systems that facilitate remote equipment tracking. Rapid urbanization, rising patient volumes, and increased investment in private healthcare facilities are accelerating the uptake of maintenance services in this segment.

Europe Medical Equipment Maintenance Market Regional Analysis

- Germany dominated the Europe medical equipment maintenance market with the largest revenue share of 38.7% in 2025, characterized by its strong healthcare infrastructure, high medical device adoption rates, and the presence of leading medical technology companies

- Healthcare providers in Germany highly prioritize reliable maintenance services to ensure uninterrupted operation of critical equipment such as MRI, CT scanners, surgical instruments, and laboratory devices, which are essential for patient safety and clinical efficiency

- This dominance is further supported by the presence of leading medical technology companies, increasing outsourcing of maintenance services to specialized providers, and rising investments in hospital modernization, establishing professional medical equipment maintenance as the preferred solution for both public and private healthcare facilities

The Germany Medical Equipment Maintenance Market Insight

The Germany medical equipment maintenance market dominated Europe with the largest revenue share of 38.7% in 2025, driven by the country’s advanced healthcare infrastructure, high adoption of sophisticated medical devices, and strict regulatory standards. Hospitals and diagnostic centers prioritize uninterrupted operation of critical devices such as MRI, CT scanners, surgical instruments, and laboratory equipment to ensure patient safety and compliance. The market is further supported by outsourcing of maintenance services to specialized providers, integration of predictive maintenance solutions, and increasing investments in hospital modernization. German healthcare providers also emphasize operational efficiency, regulatory adherence, and high-quality service contracts, fueling strong demand for preventive, corrective, and performance maintenance services. The preference for professional, privacy-focused, and technologically advanced maintenance solutions aligns with local expectations, establishing Germany as the key market within Europe.

U.K. Medical Equipment Maintenance Market Insight

The U.K. medical equipment maintenance market is expected to grow at a noteworthy CAGR during the forecast period, driven by increasing focus on patient safety, regulatory compliance, and uninterrupted operation of medical devices in hospitals and clinics. Rising concerns over equipment downtime and high repair costs are encouraging adoption of preventive and corrective maintenance services. The country benefits from a strong presence of specialized service providers and outsourcing infrastructure, along with adoption of IoT-enabled monitoring systems for diagnostic and imaging equipment. Investments in digital healthcare initiatives, hospital modernization, and streamlined service contracts further stimulate market growth. U.K. healthcare providers increasingly rely on professional maintenance services to ensure efficiency, minimize downtime, and extend the lifecycle of critical medical devices.

France Medical Equipment Maintenance Market Insight

The France medical equipment maintenance market is projected to expand steadily during the forecast period, fueled by growing installation of advanced medical devices and increasing regulatory scrutiny across hospitals and clinics. French healthcare providers prioritize preventive maintenance and performance monitoring to maintain compliance and operational efficiency. Outsourcing of maintenance services to certified external providers is becoming prevalent, enabling timely calibration, repairs, and software updates for high-value equipment. Government initiatives supporting hospital infrastructure modernization, coupled with rising investments in diagnostic and imaging technologies, further boost demand. The market is also benefiting from adoption of predictive maintenance technologies and IoT-based monitoring, ensuring continuous device reliability and improved patient care.

Italy Medical Equipment Maintenance Market Insight

The Italy medical equipment maintenance market is expected to witness significant growth over the forecast period, driven by rising adoption of advanced imaging, surgical, and laboratory equipment across public and private healthcare facilities. Hospitals and diagnostic centers are emphasizing preventive maintenance and rapid corrective services to ensure uninterrupted operation and patient safety. The market is supported by specialized maintenance providers offering integrated service contracts covering calibration, repair, and performance optimization. Increasing awareness of regulatory compliance, operational efficiency, and equipment lifecycle management is propelling adoption. Furthermore, Italy is witnessing growing investments in hospital modernization and digital healthcare infrastructure, strengthening demand for professional maintenance services.

Europe Medical Equipment Maintenance Market Share

The Europe Medical Equipment Maintenance industry is primarily led by well-established companies, including:

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Medtronic (Ireland)

- B. Braun SE (Germany)

- Drägerwerk AG & Co. KGaA (Germany)

- Metesa (Norway)

- Siemens Healthineers AG (Germany)

- Esaote SPA (Italy)

- Althea Group (Italy)

- Wisag (Germany)

- VI.TECH GmbH (Germany)

- Ergea Group (U.K.)

- EULEN Group (Spain)

- STERIS plc (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Agfa-Gevaert Group (Belgium)

- Medisafe International (U.K.)

- Roeser Medical Group (Germany)

- Alldevice (Estonia)

- Nordic Service Group (Denmark)

What are the Recent Developments in Europe Medical Equipment Maintenance Market?

- In January 2026, the European Commission proposed major amendments to simplify and streamline medical device regulations impacting hospitals and manufacturers, a development expected to indirectly improve hospital compliance and equipment maintenance processes across Europe. The regulatory changes aim to reduce administrative burdens and improve device availability in clinical settings

- In December 2025, data showed a new safety concern as eight in ten NHS hospitals in England were found to be relying on outdated medical imaging and radiotherapy machines, prompting government commitments to upgrade equipment and accelerate maintenance and modernization efforts. MRI scanners and X‑ray machines over a decade old were still in use, raising risks of diagnostic errors and emphasizing the importance of effective maintenance and renewal programs

- In July 2025, the EU announced plans to strengthen strategic stockpiling of medical equipment and supplies as part of broader preparedness efforts for future health crises, potentially influencing maintenance and readiness strategies in national healthcare systems. This initiative reflects heightened focus on ensuring availability and operational reliability of critical medical devices across Europe

- 2025年6月、アンドラプラデーシュ州メドテックゾーン(AMTZ)とユニバーサル臨床工学連盟(UCEF)は、災害や公衆衛生上の緊急事態発生時に医療機器の保守・修理を迅速に支援するためのグローバルイニシアチブである国際バイオメッドクロス(IBC)を立ち上げ、機器保守インフラに関する協力関係の強化を示した。

- 2025年6月、イングランドの国民保健サービス(NHS)は、機器の故障に関連した数千件の患者被害と死亡事例を明らかにし、全国の病院医療機器における深刻な保守・安全上の欠陥を浮き彫りにした。2022年から2025年の間に、除細動器や呼吸器などの重要な機器の故障により、約4,000人の患者が被害を受け、87人が死亡した。この事態を受け、インフラへの投資強化と保守管理の近代化を求める声が高まっている。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。