世界の3Dゲーム機市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

1.08 Billion

USD

1.88 Billion

2024

2032

USD

1.08 Billion

USD

1.88 Billion

2024

2032

| 2025 –2032 | |

| USD 1.08 Billion | |

| USD 1.88 Billion | |

| % | |

|

グローバル3Dゲームコンソール市場のセグメント化、コンポーネント(ハードウェアとソフトウェア)、テクノロジー(仮想現実と拡張現実、自動立体視、アクティブシャッターテクノロジー、Leap Motion、Project Holodeck、KINECTモーションゲーミング、Oculus Rift、偏光シャッター、Xbox IllumiRoom)、プラットフォーム(Microsoft Xbox、Nintendo Wii、Sony Playstation)、コンソール(携帯型、家庭用、専用、マイクロ)、エンドユーザー(ヘルスケア、ゲーム、モバイル) - 2032年までの業界動向と予測

3Dゲーム機市場規模

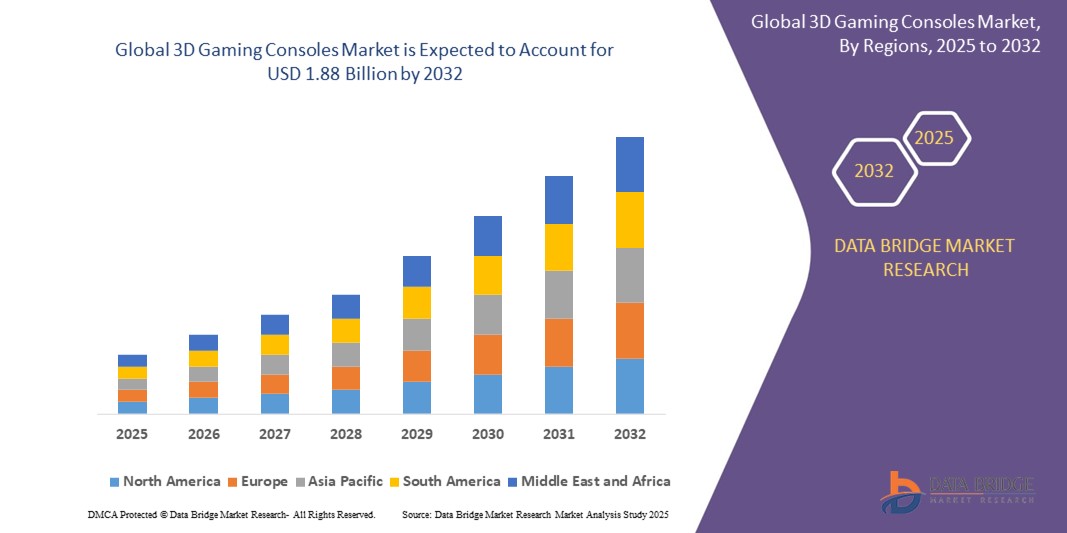

- 世界の3Dゲーム機市場規模は2024年に10億8000万米ドルと評価され、予測期間中に7.20%のCAGRで成長し、2032年には18億8000万米ドル に達すると予想されています 。

- 市場の成長は、没入型ゲーム体験の需要の高まり、グラフィックスとディスプレイの技術進歩、コンソールゲームにおける仮想現実 (VR)と拡張現実(AR)の統合の人気の高まりによって主に推進されています。

- さらに、世界中で拡大するゲーマーコミュニティと、革新的なゲーム技術への主要プレーヤーによる投資の増加が、市場拡大をさらに促進しています。

3Dゲーム機市場分析

- 3Dゲームコンソール市場は、没入型技術の進歩と強化されたユーザーインターフェースにより着実に成長しており、ゲーマーにより魅力的でリアルな体験を提供しています。ゲームコンソールに仮想現実と拡張現実の機能が統合されているため、革新的でインタラクティブなゲームプレイオプションの需要が高まっています。

- 市場の主要企業は、より幅広い顧客層を引き付けるために、グラフィックスと処理能力を向上させた高性能コンソールの開発に注力しています。これにより、業界内での競争と協力が促進され、継続的なイノベーションと製品提供の拡大が促進されています。

- 北米は、高品質のインタラクティブエンターテイメントに対する強い消費者需要と、先進的なゲーム技術の早期導入に支えられ、2025年には世界の3Dゲームコンソール市場で43%の最大の収益シェアを獲得し、市場を席巻するだろう。

- アジア太平洋地域は、急速な技術導入、可処分所得の増加、ゲーマーコミュニティの拡大により、世界の3Dゲーム機市場で最も高い成長率を示すことが予想されています。

- ハードウェアセグメントは、高度なプロセッサ、高解像度ディスプレイ、モーショントラッキングセンサーへの投資増加により、2024年には58%という最大の市場収益シェアを占めることになります。特にプロゲーマーや愛好家の間では、没入型ゲーム機の需要が高まり続けており、高性能ゲーム機のニーズが高まっています。

レポートの範囲と3Dゲーム機市場のセグメンテーション

|

属性 |

3Dゲーム機の主要市場分析 |

|

対象セグメント |

|

|

対象国 |

北米

ヨーロッパ

アジア太平洋

中東およびアフリカ

南アメリカ

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

データブリッジマーケットリサーチがまとめた市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、専門家による詳細な分析、価格設定分析、ブランドシェア分析、消費者調査、人口統計分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選択基準、PESTLE分析、ポーター分析、規制の枠組みも含まれています。 |

3Dゲーム機市場の動向

「没入型でインタラクティブなゲーム体験の台頭」

- 3Dゲーム機市場は、従来のゲームプレイの枠を超えた没入感とインタラクティブ性を備えたゲーム体験の提供にますます注力しています。このトレンドは、現実世界のシナリオを再現したリアルなビジュアルとダイナミックな環境への需要の高まりによって推進されています。

- 仮想現実と拡張現実の技術をゲーム機に統合することで、ゲーマーがデジタル世界と関わる方法に革命が起こっている。

- 例えば、ゲーム機は現在、プレイヤーがゲーム内で物理的に移動したりインタラクトしたりできるVRヘッドセットをサポートしており、没入感を高めている。

- 開発者は、洗練された3Dグラフィックスと空間オーディオを備えたゲームを設計し、多感覚体験を生み出しています。

- この傾向は、プロセッサの改良やモーションセンサーコントローラなどのハードウェア機能の継続的な革新を促し、よりスムーズで応答性の高いゲームプレイを可能にします。

- その結果、ゲーム機は単なる娯楽以上のものを提供し、ユーザー間の社会的交流や体験的な関与を促進するプラットフォームへと進化している。

3Dゲーム機市場の動向

ドライバ

「強化されたゲーム体験への需要の高まり」

- 消費者は、高品質のグラフィックスとインタラクティブなゲームプレイを組み合わせた、没入感がありリアルなゲーム体験をますます求めており、それがエンゲージメントと満足度の向上につながっています。

- 例えば、PlayStation 5とXbox Series Xは、レイトレーシング技術と超高速SSDを搭載し、視覚的に豊かでシームレスな3D世界をサポートしています。

- リアリズムへの需要により、メーカーは強力なGPU、高解像度ディスプレイ、高精度なモーションセンサーなどの高度なハードウェアをコンソールに統合するようになりました。

- 仮想現実や拡張現実などの技術は、より深い没入感と新しいインタラクションモードを提供することで3Dゲームを強化し、幅広いゲーマーにアピールします。

- 例えば、MetaのVRをゲームプラットフォームに統合することで、没入型プレイの範囲が拡大しました。

- 詳細なストーリーとリアルなキャラクターアニメーションを備えた洗練された3Dゲームの提供は、ハードウェアのイノベーションをサポートし、コンテンツエコシステムを強化します。

- マルチプレイヤーやオンラインゲームの人気により、シームレスな3D接続とリアルタイムのソーシャルインタラクションを保証するコンソールの需要が高まり、継続的な市場の革新と開発が促進されています。

抑制/挑戦

「高度な3Dゲーム機の高コスト」

- 3Dゲーム機は、高度なハードウェアとVR/ARの統合によって価格が高騰しており、予算に敏感な消費者にとって手の届きにくいものとなっている。

- 例えば、PlayStation VR2バンドルやXbox Series Xなどのゲーム機は、多くの人にとって手の届かない高額な価格となっている。

- 追加のアクセサリや3D対応ゲームを購入する必要があるため、総所有コストがさらに増加し、消費者の幅広い採用を阻害する。

- 価格に敏感な地域では、価格が限られているため市場浸透率が低く、3Dゲームコンソールのユーザーベースの成長が制限されています。

- 進化する技術標準に対応するために頻繁にハードウェアをアップグレードする必要があるため、消費者の長期的な支出が増加する。

- モバイルやPCゲームプラットフォームなどの安価な代替手段は、低コストで魅力的な体験を提供し、競争を激化させ、潜在的な購入者をコンソールゲームから遠ざけている。

3Dゲーム機市場の展望

市場は、コンポーネント、テクノロジー、プラットフォーム、コンソール、エンドユーザーに基づいてセグメント化されています。

- コンポーネント別

On the basis of components, the 3D gaming consoles market is segmented into hardware and software. The hardware segment holds the largest market revenue share of 58% in 2024, driven by growing investments in advanced processors, high-resolution displays, and motion tracking sensors. Demand for immersive gaming setups continues to rise, particularly among professional gamers and enthusiasts, boosting the need for high-performance gaming consoles.

The software segment is expected to witness the fastest growth rate from 2025 to 2032, supported by the increasing development of 3D game titles and interactive environments. Game developers are focusing on user experience through AI-driven narratives, realistic character animations, and VR/AR integration, making software a key driver for market expansion.

- By Technologies

On the basis of technologies, the 3D gaming consoles market is segmented into virtual & augmented reality, auto stereoscopy, active shutter technology, Leap Motion, Project Holodeck, KINECT Motion Gaming, Oculus Rift, Polarized Shutter, and Xbox IllumiRoom. Virtual & augmented reality segment dominates the largest market share of 67% in 2024 due to their ability to deliver fully immersive gameplay and real-world interactions. Consumer preference for more engaging gaming environments continues to boost adoption of these technologies.

The leap motion segment is expected to witness the fastest growth rate from 2025 to 2032, as its gesture-based control system offers intuitive interaction without physical controllers. This technology is gaining traction among developers aiming to enhance realism and reduce hardware dependency in gaming consoles.

- By Platforms

On the basis of platforms, the 3D gaming consoles market is segmented into Microsoft Xbox, Nintendo Wii, and Sony PlayStation. Sony PlayStation held the largest market revenue share in 2024, benefiting from a strong global user base, exclusive 3D game titles, and advanced VR support. Its frequent innovation and ecosystem integration continue to attract new and existing gamers.

The Nintendo Wii segment is expected to witness the fastest growth rate from 2025 to 2032, with a growing focus on family-friendly gaming, motion-based controls, and fitness-oriented titles. This segment gains popularity in regions favouring interactive, group-oriented experiences.

- By Consoles

On the basis of consoles, the 3D gaming consoles market is segmented into hand-held, home, dedicated, and micro. The home console segment dominates the largest market revenue share of 45% in 2024, driven by consumer demand for high-performance entertainment systems with advanced graphics and network capabilities. Home consoles support multiplayer features, streaming services, and 3D content, making them highly preferred.

The hand-held consoles segment is expected to witness the fastest growth rate from 2025 to 2032, supported by the rising demand for on-the-go gaming, portability, and cloud-based 3D content. Increasing smartphone penetration and mobile gaming habits also boost this segment’s potential.

- By End-Users

On the basis of end-users, the 3D gaming consoles market is segmented into healthcare, gaming, and mobile. The gaming segment accounted for the largest market revenue share in 2024, supported by a rising number of gamers, esports tournaments, and demand for immersive storytelling and lifelike simulations.

The healthcare segment is expected to witness the fastest growth rate from 2025 to 2032, driven by applications in rehabilitation, mental health, and surgical simulations. The integration of 3D consoles with training modules and patient engagement tools highlights their potential beyond entertainment.

3D Gaming Consoles Market Regional Analysis

- North America dominates the global 3D gaming consoles market with the largest revenue share of 43% in 2025, fuelled by strong consumer demand for high-quality interactive entertainment and early adoption of advanced gaming technologies

- The region benefits from a robust gaming ecosystem, featuring well-established console manufacturers, publishers, and a large base of engaged players

- In addition, the growing influence of esports, increasing demand for multiplayer online gaming, and the widespread availability of high-speed internet continue to boost sales of 3D-enabled gaming consoles across the U.S. and Canada

U.S. 3D Gaming Consoles Market Insight

The U.S. 3D gaming consoles market accounted for the majority revenue share in North America in 2025, driven by a tech-forward population and high consumer spending on home entertainment systems. The rapid growth of subscription-based gaming services, coupled with strong console sales during product launches from leading brands such as Microsoft and Sony, continues to shape the market landscape. In addition, the popularity of cloud gaming, VR/AR integration, and cross-platform compatibility is increasing the appeal of 3D consoles among both casual and hardcore gamers.

Europe 3D Gaming Consoles Market Insight

The Europe 3D gaming consoles market is expected to witness the fastest growth rate from 2025 to 2032, supported by a well-established gaming culture and rising adoption of immersive technologies. Increasing demand for console-based entertainment in both single-player and multiplayer formats is boosting sales across major economies such as the U.K., Germany, and France. In addition, expanding broadband infrastructure, growing investments in gaming studios, and the popularity of esports events are further propelling the adoption of 3D gaming consoles throughout the region.

Germany 3D Gaming Consoles Market Insight

The Germany 3D gaming consoles market is expected to witness the fastest growth rate from 2025 to 2032, underpinned by a strong digital ecosystem and a tech-savvy population. German consumers are increasingly embracing high-performance gaming systems, especially among younger demographics and digital natives. The rising demand for immersive, cinematic gaming experiences, supported by console upgrades and VR capabilities, is accelerating adoption. Moreover, government initiatives focused on digital innovation and gaming development are strengthening Germany's position as a key European market for 3D console manufacturers.

U.K. 3D Gaming Consoles Market Insight

The U.K. 3D gaming consoles market is expected to witness the fastest growth rate from 2025 to 2032, driven by increasing demand for interactive and home-based entertainment. British consumers are investing in premium gaming experiences, supported by strong broadband infrastructure and rising popularity of subscription-based gaming platforms. The market is also benefiting from the U.K.'s vibrant game development sector, alongside growing interest in esports and online multiplayer titles. Furthermore, the integration of consoles with smart TVs and home systems is enhancing user experiences and driving wider adoption.

Asia-Pacific 3D Gaming Consoles Market Insight

The Asia-Pacific 3D gaming consoles market is expected to witness the fastest growth rate from 2025 to 2032, driven by the surging popularity of immersive gaming, rising disposable incomes, and the growing presence of tech-savvy youth populations. Countries such as China, Japan, and South Korea are leading this momentum through rapid advancements in gaming hardware and infrastructure. The region’s strong gaming culture, expanding esports ecosystem, and increasing smartphone and internet penetration further accelerate adoption. In addition, government initiatives supporting digital innovation and the rising availability of localized gaming content are enhancing consumer engagement across the region.

China 3D Gaming Consoles Market Insight

The China 3D gaming consoles market captured the largest revenue share in Asia-Pacific in 2025, driven by a growing middle class, widespread digital access, and rising consumer demand for next-generation entertainment experiences. China's dynamic gaming ecosystem—home to major developers such as Tencent and NetEase—is fueling demand for high-performance consoles. Moreover, increased investment in cloud gaming and VR/AR integration, coupled with government-backed smart city initiatives, is promoting broader 3D console adoption across urban households, internet cafés, and esports arenas.

Japan 3D Gaming Consoles Market Insight

日本の3Dゲーム機市場は、長年にわたるゲーム業界の伝統と、ソニーや任天堂といった大手企業の存在を背景に、2025年から2032年にかけて最も高い成長率を達成すると予想されています。日本の消費者は革新的なエンターテインメント技術をいち早く取り入れており、没入感の高い高解像度のゲーム体験への需要の高まりに貢献しています。スマートホームエコシステムとゲーム機の統合、そしてコンパクトで多機能なゲーム環境への嗜好が相まって、家庭用ゲーム機と携帯型ゲーム機の両方の分野で売上を牽引しています。さらに、日本の強力なデジタルインフラと高齢化社会は、アクセスしやすくユーザーフレンドリーなエンターテインメントシステムへの関心を高めています。

3Dゲーム機の市場シェア

3D ゲーム コンソール業界は、主に次のような定評のある企業によって牽引されています。

- Activision Publishing, Inc.(米国)

- NVIDIAコーポレーション(米国)

- ソニー・インタラクティブエンタテインメント株式会社(日本)

- 任天堂(日本)

- アバターリアリティ社(米国)

- Facebook Technologies, LLC(米国)

- エレクトロニック・アーツ社(米国)

- Kava, LLC(米国)

- ロジテック(スイス)

- リンデンリサーチ社(米国)

- A4TECH(台湾)

- Guillemot Corporation SA (フランス)

- ユニティ・テクノロジーズ(米国)

- GameBender LLC(米国)

- スライトリー・マッド・スタジオ(イギリス)

- Google(米国)

- アップル社(米国)

- Razer Inc.(米国)

- マッドキャッツグローバルリミテッド(米国)

- マイクロソフト(米国)

世界の3Dゲーム機市場の最新動向

- 2022年、アル・ファカー・タバコ・トレーディングは、ドバイ免税店限定で「ダブルキック」という新製品ラインを発売しました。この新製品ラインでは、2種類の異なるフレーバー(ツーアップル、ミント、グレープ&ミント)が、便利な200g入りで提供されます。トラベルリテールのポートフォリオを拡大することで、アル・ファカーは免税市場における顧客の選択肢を広げ、より幅広い顧客層を獲得することを目指しました。今回の発売により、トラベルリテール分野における同社のプレゼンスが強化され、フレーバー付きタバコ製品に対する消費者の嗜好の変化に対応することで、成長が促進されると期待されています。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。