Global Active Implantable Medical Devices Market Size, Share and Trends Analysis Report

Market Size in USD Billion

CAGR :

%

USD

27.69 Billion

USD

51.25 Billion

2025

2033

USD

27.69 Billion

USD

51.25 Billion

2025

2033

| 2026 –2033 | |

| USD 27.69 Billion | |

| USD 51.25 Billion | |

| % | |

|

Global Active Implantable Medical Devices Market Segmentation, By Product (Implantable Cardioverter Defibrillators, Ventricular Assist Devices, Implantable Cardiac Pacemakers, Dental Implants, Implantable Hearing Devices, Ventricular Assist Devices, and Neurostimulators), End User (Hospitals, Ambulatory Centers, Cardiac Centers, Dental Clinics, and Others)- Industry Trends and Forecast to 2033

Active Implantable Medical Devices Market Size

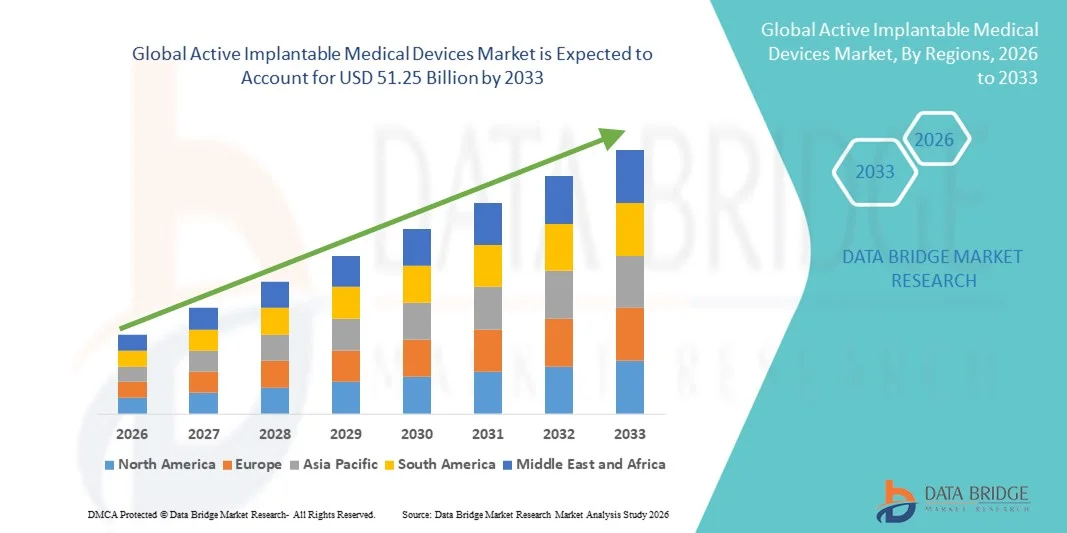

- The global active implantable medical devices market size was valued at USD 27.69 billion in 2025 and is expected to reach USD 51.25 billion by 2033, at a CAGR of 8.00% during the forecast period

- The market growth is primarily driven by the rising prevalence of chronic diseases such as cardiovascular disorders, neurological conditions, and hearing impairments, along with the increasing geriatric population worldwide that requires long-term therapeutic and monitoring solutions

- Furthermore, continuous technological advancements in miniaturization, wireless connectivity, battery longevity, and biocompatible materials, coupled with growing demand for minimally invasive procedures and improved patient outcomes, are positioning active implantable medical devices as critical components of modern healthcare, thereby significantly accelerating overall market expansion

Active Implantable Medical Devices Market Analysis

- Active implantable medical devices, including pacemakers, implantable cardioverter defibrillators, neurostimulators, cochlear implants, and implantable drug delivery systems, are increasingly essential components of modern healthcare due to their ability to provide continuous therapeutic intervention, physiological monitoring, and life-sustaining support within the human body

- The rising demand for active implantable medical devices is primarily driven by the growing global burden of cardiovascular diseases, neurological disorders, and hearing impairments, alongside the expanding geriatric population and increasing preference for minimally invasive and long-term treatment solutions

- North America dominated the active implantable medical devices market with the largest revenue share of 38.76% in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, favorable reimbursement frameworks, and strong presence of leading medical device manufacturers, with the U.S. witnessing significant adoption of technologically advanced implantable cardiac and neurostimulation devices

- Asia-Pacific is expected to be the fastest growing region in the active implantable medical devices market during the forecast period due to improving healthcare infrastructure, rising patient awareness, expanding medical tourism, and increasing investments in advanced surgical and implant technologies

- Implantable Cardiac Pacemakers segment dominated the active implantable medical devices market with a market share of 41.5% in 2025, attributed to the high prevalence of cardiac arrhythmias, growing elderly population, and continuous advancements in device miniaturization, battery longevity, and remote monitoring capabilities

Report Scope and Active Implantable Medical Devices Market Segmentation

|

Attributes |

Active Implantable Medical Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Active Implantable Medical Devices Market Trends

Advancement Through Miniaturization and AI-Enabled Remote Monitoring

- A significant and accelerating trend in the global active implantable medical devices market is the integration of advanced miniaturization technologies and artificial intelligence (AI)-enabled remote monitoring systems, substantially enhancing clinical precision, patient comfort, and long-term therapeutic outcomes

- For instance, next-generation implantable cardioverter defibrillators and neurostimulators are being designed with smaller form factors and Bluetooth-enabled connectivity, allowing physicians to remotely monitor device performance and patient physiological data in real time

- AI integration in implantable devices enables predictive analytics for early detection of arrhythmias, seizure patterns, or abnormal neural activity, while also optimizing stimulation parameters based on individual patient response. For instance, certain implantable cardiac devices utilize machine learning algorithms to detect irregular heart rhythms and automatically adjust therapy delivery, improving overall treatment efficacy. Furthermore, wireless telemetry capabilities allow clinicians to conduct remote follow-ups, minimizing hospital visits and enhancing patient convenience

- The seamless integration of implantable devices with digital health platforms and hospital information systems facilitates centralized monitoring and data-driven decision-making. Through secure cloud-based dashboards, healthcare providers can manage multiple patients simultaneously, review device diagnostics, and personalize treatment regimens, thereby creating a more connected and responsive healthcare ecosystem

- This trend toward smarter, smaller, and more connected implantable systems is fundamentally transforming expectations for chronic disease management and long-term care. Consequently, leading manufacturers are developing AI-enabled implantable solutions with enhanced battery longevity, MRI compatibility, and advanced remote programming capabilities

- The demand for technologically advanced, minimally invasive, and remotely manageable implantable devices is rising rapidly across both developed and emerging healthcare markets, as providers increasingly prioritize efficiency, patient safety, and value-based care delivery

- Furthermore, increasing collaboration between medical device companies and digital health firms is accelerating innovation in data analytics, cybersecurity frameworks, and interoperable implantable systems, strengthening the overall market landscape

Active Implantable Medical Devices Market Dynamics

Driver

Rising Prevalence of Chronic Diseases and Aging Population

- The increasing global burden of cardiovascular diseases, neurological disorders, and sensory impairments, coupled with the rapidly expanding geriatric population, is a significant driver for the heightened demand for active implantable medical devices

- For instance, in recent years, major medical device manufacturers have expanded their cardiac rhythm management and neurostimulation portfolios to address the growing incidence of arrhythmias, Parkinson’s disease, epilepsy, and chronic pain, strengthening their global market presence

- As life expectancy rises and chronic conditions become more prevalent, implantable devices provide long-term therapeutic solutions that improve survival rates, restore physiological function, and enhance patient quality of life compared to conventional treatment approaches

- Furthermore, advancements in minimally invasive surgical techniques and improved reimbursement frameworks are making implantation procedures safer, more accessible, and financially viable across diverse healthcare systems

- The ability of implantable devices to deliver continuous monitoring, automated therapy adjustments, and reduced hospital readmissions is a key factor accelerating adoption in both developed and emerging regions. The growing emphasis on early diagnosis and preventive cardiology further contributes to sustained market expansion

- Collectively, these demographic and clinical trends are reinforcing the critical role of active implantable medical devices in modern healthcare, thereby driving consistent and long-term market growth

- Increasing healthcare expenditure and government initiatives focused on improving cardiac and neurological care infrastructure are further supporting the widespread adoption of advanced implantable technologies

- Moreover, growing awareness among patients regarding early disease detection and the availability of technologically advanced treatment options is encouraging higher acceptance rates of implantable therapeutic devices

Restraint/Challenge

High Cost Burden and Stringent Regulatory Approval Requirements

- Concerns surrounding the high cost of device implantation procedures and the stringent regulatory approval processes pose significant challenges to broader market penetration of active implantable medical devices

- For instance, regulatory authorities in major markets require extensive clinical trials, long-term safety data, and rigorous post-market surveillance before approving new implantable technologies, increasing development timelines and overall costs

- The complex approval pathways and compliance requirements can delay product launches and limit smaller manufacturers from entering the market, thereby constraining innovation and competitive dynamics

- In addition, the substantial upfront cost of advanced implantable devices and associated surgical procedures can create financial barriers for patients and healthcare systems, particularly in low- and middle-income countries

- Concerns related to device recalls, battery failures, or long-term biocompatibility issues may also affect patient confidence and physician adoption, emphasizing the importance of stringent quality assurance and continuous monitoring

- Overcoming these challenges through cost optimization strategies, streamlined regulatory collaboration, and expanded reimbursement coverage will be essential to ensure sustained innovation and broader accessibility of active implantable medical technologies

- Furthermore, cybersecurity risks associated with connected implantable devices present emerging challenges, requiring robust data protection frameworks and continuous software validation

- Variability in reimbursement policies and unequal access to advanced healthcare facilities across regions may limit equitable adoption, particularly in developing economies where specialized implantation expertise is limited

Active Implantable Medical Devices Market Scope

The market is segmented on the basis of product and end user.

- By Product

On the basis of product, the global active implantable medical devices market is segmented into implantable cardioverter defibrillators, ventricular assist devices, implantable cardiac pacemakers, dental implants, implantable hearing devices, ventricular assist devices, and neurostimulators. The implantable cardiac pacemakers segment dominated the market with the largest revenue share of 41.5% in 2025, driven by the high global prevalence of cardiac arrhythmias and conduction disorders. Pacemakers are widely adopted due to their proven clinical efficacy, long-standing safety profile, and continuous technological advancements such as MRI compatibility and remote monitoring capabilities. The growing geriatric population, which is more susceptible to heart rhythm abnormalities, further strengthens demand for pacemaker implantation procedures. In addition, improved battery longevity and miniaturization have enhanced patient comfort and reduced replacement frequency. Favorable reimbursement policies in developed healthcare systems also contribute to the strong dominance of this segment across North America and Europe.

The neurostimulators segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the increasing prevalence of neurological disorders such as Parkinson’s disease, epilepsy, chronic pain, and depression. Neurostimulation therapies offer minimally invasive and reversible treatment alternatives compared to long-term pharmacological interventions, driving higher patient and physician acceptance. Technological innovations including closed-loop stimulation systems and AI-enabled adaptive programming are enhancing therapeutic precision and patient outcomes. Expanding clinical indications and regulatory approvals for new neurological and psychiatric applications are further broadening the addressable patient pool. Growing awareness regarding advanced pain management solutions and increasing investments in neuroscience research are also accelerating segment growth. In addition, rising healthcare infrastructure development in emerging economies is supporting greater adoption of advanced neurostimulation implants.

- By End User

On the basis of end user, the global active implantable medical devices market is segmented into hospitals, ambulatory centers, cardiac centers, dental clinics, and others. The hospitals segment dominated the market with the largest revenue share in 2025, attributed to the availability of advanced surgical infrastructure, skilled healthcare professionals, and comprehensive post-operative care facilities. Most complex implant procedures, including pacemaker and defibrillator implantations, are primarily performed in hospital settings due to the need for specialized equipment and intensive monitoring. Hospitals also benefit from favorable reimbursement frameworks and established procurement channels with major medical device manufacturers. The presence of multidisciplinary care teams ensures optimal management of high-risk patients undergoing implant surgeries. Furthermore, hospitals often serve as primary referral centers for chronic disease management, reinforcing their leading market position. Continuous investments in advanced operating rooms and digital health integration further strengthen hospital dominance in this segment.

The ambulatory centers segment is expected to witness the fastest CAGR from 2026 to 2033, driven by the growing shift toward minimally invasive procedures and outpatient surgical settings. Technological advancements have reduced procedure complexity and recovery time, making certain implantations feasible in specialized ambulatory environments. These centers offer cost-effective alternatives to traditional hospital-based procedures, attracting both patients and healthcare providers seeking reduced hospitalization expenses. Increasing patient preference for shorter hospital stays and faster recovery periods is further contributing to segment growth. Expansion of specialized cardiac and neurology ambulatory facilities in developed markets is enhancing procedural capacity outside traditional hospital settings. In addition, supportive regulatory reforms and evolving reimbursement models are encouraging the decentralization of implantable device procedures, accelerating growth within ambulatory care environments.

Active Implantable Medical Devices Market Regional Analysis

- North America dominated the active implantable medical devices market with the largest revenue share of 38.76% in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, favorable reimbursement frameworks, and strong presence of leading medical device manufacturers

- Patients and healthcare providers in the region highly value the clinical reliability, long-term therapeutic benefits, and remote monitoring capabilities offered by active implantable medical devices, particularly for cardiac rhythm management and neurostimulation therapies

- This widespread adoption is further supported by high healthcare expenditure, favorable reimbursement frameworks, a well-established regulatory environment, and the presence of leading medical device manufacturers, positioning implantable technologies as a preferred treatment option across hospitals and specialized care centers

U.S. Active Implantable Medical Devices Market Insight

The U.S. active implantable medical devices market captured the largest revenue share within North America in 2025, fueled by the high prevalence of cardiovascular diseases, neurological disorders, and strong adoption of advanced implantable technologies. Patients and healthcare providers increasingly prioritize long-term therapeutic solutions such as pacemakers, implantable cardioverter defibrillators, and neurostimulators to manage chronic conditions effectively. The presence of leading medical device manufacturers, robust reimbursement frameworks, and substantial healthcare expenditure further propels market expansion. Moreover, the growing integration of remote monitoring platforms and AI-enabled cardiac management systems is significantly contributing to the market’s continued growth.

Europe Active Implantable Medical Devices Market Insight

The Europe active implantable medical devices market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising incidence of chronic diseases and strong regulatory standards ensuring device safety and efficacy. Increasing geriatric population levels, coupled with the demand for minimally invasive therapeutic interventions, are fostering adoption across the region. European healthcare systems emphasize early diagnosis and long-term disease management, supporting implantable cardiac and neurostimulation device uptake. Growth is observed across hospitals and specialized cardiac centers, with implantable technologies being incorporated into both advanced tertiary care institutions and regional healthcare facilities.

U.K. Active Implantable Medical Devices Market Insight

The U.K. active implantable medical devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing cardiovascular disease prevalence and expanding access to advanced treatment options. Public healthcare support through structured reimbursement systems encourages adoption of implantable cardiac and neurological devices. In addition, rising awareness regarding early intervention for arrhythmias and movement disorders is influencing treatment preferences. The country’s focus on digital health transformation and remote patient monitoring is expected to continue stimulating demand for technologically advanced implantable solutions.

Germany Active Implantable Medical Devices Market Insight

The Germany active implantable medical devices market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure and increasing investment in medical innovation. Germany’s emphasis on high-quality clinical standards and advanced surgical procedures promotes widespread adoption of pacemakers, defibrillators, and neurostimulators. The integration of implantable devices with digital health systems is becoming increasingly prevalent, supported by research collaborations and technological advancements. In addition, rising elderly demographics and strong insurance coverage frameworks align with sustained demand for long-term implantable therapeutic solutions.

Asia-Pacific Active Implantable Medical Devices Market Insight

The Asia-Pacific active implantable medical devices market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by expanding healthcare infrastructure, rising disposable incomes, and increasing prevalence of chronic diseases in countries such as China, Japan, and India. Government initiatives focused on improving cardiac and neurological care services are accelerating adoption across emerging economies. Furthermore, growing medical tourism and investments in advanced surgical facilities are strengthening regional demand. As APAC continues to enhance domestic manufacturing capabilities and access to innovative implantable technologies, affordability and patient access are expected to improve significantly.

Japan Active Implantable Medical Devices Market Insight

The Japan active implantable medical devices market is gaining momentum due to the country’s rapidly aging population, high life expectancy, and advanced healthcare system. The Japanese market places significant emphasis on early diagnosis and precision treatment, encouraging adoption of implantable cardiac and neurostimulation devices. Integration of remote monitoring technologies and minimally invasive implantation procedures is further fueling growth. Moreover, Japan’s strong regulatory framework and continuous investment in medical research are expected to support sustained expansion in both hospital and specialized care settings.

India Active Implantable Medical Devices Market Insight

The India active implantable medical devices market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s rising burden of cardiovascular diseases, expanding middle-class population, and improving healthcare access. India represents one of the fastest-growing markets for cardiac rhythm management and neurostimulation devices, with increasing adoption across private and tertiary hospitals. Government initiatives aimed at strengthening cardiac care infrastructure and expanding insurance coverage are key growth drivers. In addition, the presence of domestic manufacturers and growing availability of cost-effective implantable solutions are propelling market development across urban and semi-urban regions.

Active Implantable Medical Devices Market Share

The Active Implantable Medical Devices industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Boston Scientific Corporation (U.S.)

- Cochlear Limited (Australia)

- Medtronic (Ireland)

- BIOTRONIK SE & Co. KG (Germany)

- LivaNova PLC (U.K.)

- Axonics, Inc. (U.S.)

- Nevro Corp. (U.S.)

- Inspire Medical Systems, Inc. (U.S.)

- NeuroPace, Inc. (U.S.)

- MicroPort CRM (China)

- Jarvik Heart, Inc. (U.S.)

- Berlin Heart GmbH (Germany)

- Calon Cardio-Technology Ltd (U.K.)

- CARMAT (France)

- Envoy Medical Corporation (U.S.)

- Oticon Medical (Denmark)

- Nurotron Biotechnology Co., Ltd. (China)

- Blackrock Neurotech (U.S.)

- CVRx, Inc. (U.S.)

What are the Recent Developments in Global Active Implantable Medical Devices Market?

- In July 2025, Cochlear Limited received U.S. FDA approval for the Cochlear™ Nucleus® Nexa™ System, the first “smart” cochlear implant with upgradeable firmware and internal memory, setting a new standard in implantable hearing technology and future-proof feature enhancements

- In March 2025, Medtronic Japan Co., Ltd. announced the launch of the Aurora EV-ICD™ MRI device and the Epsila EV™ MRI Lead in Japan, offering a novel extravascular implantable cardioverter-defibrillator system that reduces procedural invasiveness for treating ventricular arrhythmias

- In March 2025, Medtronic introduced the Aurora EV-ICD system in Japan, marking a regional expansion and broader availability of innovative extravascular ICD technology designed for safer cardiac arrhythmia treatment

- In May 2023, MicroPort CRM received U.S. FDA approval for its Alizea™ and Celea™ implantable pacemakers, bringing modern, smaller, and discrete pacemaker technology to the U.S. market with improved implant ease and patient comfort

- In January 2024, Medtronic plc received *U.S. FDA approval for its Percept™ RC rechargeable deep brain stimulation (DBS) neurostimulator with exclusive BrainSense™ technology, marking a major innovation in implantable neurostimulation by enabling sensing-enabled therapy personalization for movement disorders such as Parkinson’s disease, essential tremor, and epilepsy

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。