Global Anthrax Treatment Market Size, Share and Trends Analysis Report

Market Size in USD Billion

CAGR :

%

USD

450.45 Million

USD

751.11 Million

2025

2033

USD

450.45 Million

USD

751.11 Million

2025

2033

| 2026 –2033 | |

| USD 450.45 Million | |

| USD 751.11 Million | |

| % | |

|

Global Anthrax Treatment Market Segmentation, By Type (Cutaneous Anthrax, Pulmonary Anthrax and Intestinal Anthrax), Route of Administration (Oral, Parenteral and Others), End User (Government Organization, Hospitals, Academic and Research Institutes and Others) - Industry Trends and Forecast to 2033

Anthrax Treatment Market Size

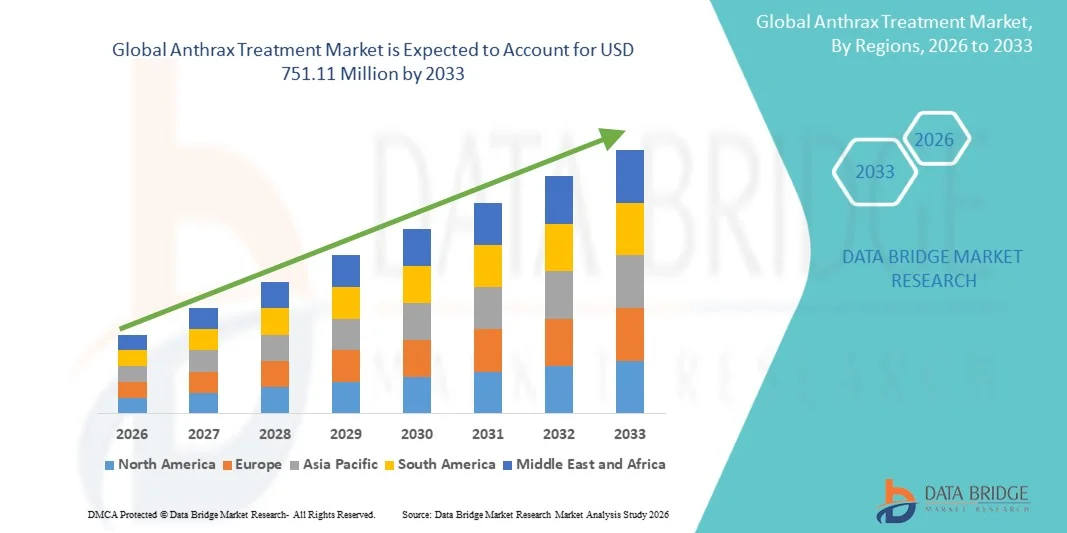

- The global anthrax treatment market size was valued at USD 450.45 million in 2025 and is expected to reach USD 751.11 million by 2033, at a CAGR of 6.6% during the forecast period

- The market growth is largely driven by increasing prevalence of anthrax infections in both humans and livestock, coupled with heightened awareness regarding timely diagnosis and treatment. Rapid advancements in antimicrobial therapies and vaccines are further contributing to the expansion of effective treatment options

- In addition, government initiatives, public health programs, and rising demand for advanced biologics and antibiotics for anthrax management are strengthening the market position. These combined factors are accelerating the adoption of innovative anthrax therapies, thereby significantly boosting the industry's growth

Anthrax Treatment Market Analysis

- Anthrax treatments, including antibiotics, antitoxins, and vaccines, are critical for managing Bacillus anthracis infections in humans and livestock, playing a vital role in public health safety and biodefense preparedness due to their effectiveness in preventing severe complications and fatalities

- The escalating demand for anthrax treatments is primarily fueled by increasing awareness of bioterrorism threats, rising incidence of zoonotic infections, and government initiatives promoting rapid diagnosis and timely therapeutic intervention

- North America dominated the anthrax treatment market with the largest revenue share of 38.7% in 2025, driven by well-established healthcare infrastructure, strategic stockpiling programs, early adoption of advanced biologics, and significant investments in R&D by key pharmaceutical companies, particularly in the U.S., where government and private collaborations are enhancing treatment accessibility and innovation

- Asia-Pacific is expected to be the fastest growing region in the anthrax treatment market during the forecast period due to rising livestock production, increasing prevalence of anthrax outbreaks, and strengthening healthcare systems in countries such as India and China

- Cutaneous Anthrax segment dominated the market with a share of 42.5% in 2025, driven by its higher incidence among human anthrax cases and the availability of established treatment protocols

Report Scope and Anthrax Treatment Market Segmentation

|

Attributes |

Anthrax Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Anthrax Treatment Market Trends

“Advancements in Biologics and Combination Therapies”

- A significant and accelerating trend in the global anthrax treatment market is the development of novel biologics, antitoxins, and combination therapies, which are improving survival rates and treatment efficacy for Bacillus anthracis infections

- For instance, monoclonal antibody therapies such as raxibacumab are increasingly being adopted alongside standard antibiotics to provide targeted neutralization of anthrax toxins, enhancing patient outcomes

- Combination therapies are enabling treatment protocols that address both inhalational and systemic forms of anthrax, reducing mortality and complications in exposed populations

- Research efforts are focused on improving stability, shelf life, and rapid deployability of these biologics, which is critical for mass prophylaxis in bioterrorism scenarios

- This trend toward more effective and multifunctional anthrax therapies is reshaping treatment standards, prompting pharmaceutical companies such as Emergent BioSolutions to advance next-generation antitoxin and vaccine solutions

- The demand for innovative biologics and combination therapies is growing rapidly across both civilian and defense sectors, as governments and healthcare providers prioritize effective countermeasures against anthrax exposure

- For instance, integration of next-generation anthrax vaccines with rapid diagnostic platforms allows earlier intervention and better patient outcomes in outbreak scenarios

- Enhanced research collaborations between biotech firms and government agencies are accelerating the development of novel therapeutics targeting resistant Bacillus anthracis strains

Anthrax Treatment Market Dynamics

Driver

“Increasing Awareness of Bioterrorism and Zoonotic Risks”

- The rising awareness of anthrax as a bioterrorism threat and zoonotic disease in livestock is a significant driver for heightened demand for vaccines, antibiotics, and antitoxins

- For instance, in March 2025, the U.S. Department of Health and Human Services announced an expansion of its Strategic National Stockpile with additional anthrax antitoxins to enhance emergency preparedness

- As public health agencies emphasize early detection and timely treatment, healthcare providers are more actively stocking and administering anthrax therapeutics

- Growing livestock production and associated anthrax outbreaks in regions such as Asia-Pacific are increasing demand for prophylactic vaccines and treatment protocols

- Government-led awareness programs and biodefense initiatives are making anthrax treatments an essential component of national health security strategies

- The combination of rising bioterrorism preparedness and zoonotic disease management is strongly propelling market growth across both commercial and government segments. For instance, educational campaigns on proper handling of livestock and early reporting of symptoms are driving adoption of prophylactic anthrax measures

- Increasing collaboration between international health organizations and local governments is facilitating faster distribution and accessibility of anthrax treatments in high-risk areas

- For instance, partnerships between vaccine manufacturers and NGOs enable rapid deployment of vaccines during sudden outbreaks in rural regions

- Expansion of national stockpiling programs in emerging economies is boosting market demand for anthrax treatments and related healthcare services

Restraint/Challenge

“High Treatment Costs and Regulatory Hurdles”

- The high cost of advanced anthrax treatments, including monoclonal antibodies and combination therapies, poses a significant barrier to widespread adoption in both developing and price-sensitive regions

- For instance, access to raxibacumab or anthrax vaccines can be limited due to pricing, regulatory approvals, and distribution challenges in low-income countries

- Stringent regulatory requirements for clinical trials, emergency use authorizations, and safety testing slow down the introduction of new therapies to the market

- Limited manufacturing capacity for antitoxins and vaccines can constrain supply during sudden outbreak situations, impacting timely access

- While government stockpiling programs help mitigate shortages, the relatively premium cost of innovative anthrax treatments can hinder adoption by hospitals and smaller healthcare providers

- Overcoming these challenges through cost optimization, streamlined regulatory pathways, and increased production capacity is essential for sustained market expansion. For instance, delays in obtaining WHO prequalification for vaccines can slow international distribution in outbreak-prone regions

- Inconsistent reimbursement policies and limited insurance coverage for advanced anthrax therapies can restrict patient access, especially in developing countries

- For instance, complex import-export regulations can delay delivery of critical anthrax antitoxins during emergency situations

- Limited awareness among rural healthcare providers regarding proper administration protocols may reduce treatment effectiveness and slow market penetration

Anthrax Treatment Market Scope

The market is segmented on the basis of type, route of administration, and end user.

- By Type

On the basis of type, the anthrax treatment market is segmented into Cutaneous Anthrax, Pulmonary Anthrax, and Intestinal Anthrax. The Cutaneous Anthrax segment dominated the market with the largest market revenue share of 42.5% in 2025, owing to the higher prevalence of cutaneous cases among human anthrax infections. Cutaneous anthrax is easier to detect and treat compared to other forms, making it the primary focus of healthcare providers and public health initiatives. Standard treatment protocols using antibiotics are well-established for this type, ensuring predictable patient outcomes. In addition, awareness campaigns targeting farmers, veterinarians, and rural communities have contributed to early diagnosis and treatment, boosting market demand. The availability of prophylactic vaccines and supportive therapies for cutaneous anthrax further strengthens this segment's position.

The Pulmonary Anthrax segment is anticipated to witness the fastest growth rate of 19.8% from 2026 to 2033, driven by increasing concerns over bioterrorism and inhalational exposure risks. Pulmonary anthrax, being the most severe form, demands advanced therapies such as monoclonal antibodies and combination treatments alongside antibiotics. Rising investments in biodefense programs, rapid diagnostic tools, and government stockpiling of antitoxins are fueling the adoption of treatments for pulmonary anthrax. Heightened global awareness and preparedness initiatives in hospitals and defense organizations are accelerating demand. Furthermore, research into novel antitoxin therapies specifically targeting inhalational anthrax is attracting significant attention, further driving growth in this segment.

- By Route of Administration

On the basis of route of administration, the anthrax treatment market is segmented into oral, parenteral, and others. The Oral segment held the largest market revenue share of 46.1% in 2025, primarily due to its convenience for post-exposure prophylaxis and ease of administration during mass exposure scenarios. Oral antibiotics are widely used for both cutaneous and inhalational anthrax cases and are often stockpiled in national emergency reserves. The simplicity of oral dosing, coupled with broad availability and affordability, contributes to its dominant position. Oral administration also supports outpatient treatment protocols, enabling faster community-level response during outbreaks.

The Parenteral segment is expected to witness the fastest CAGR from 2026 to 2033, driven by its critical role in severe anthrax cases, particularly pulmonary and systemic infections. Intravenous or intramuscular administration allows higher bioavailability of antitoxins and antibiotics, essential for acute cases requiring hospitalization. Rising hospitalizations and the need for rapid therapeutic intervention during bioterrorism or outbreak events are accelerating the adoption of parenteral therapies. Moreover, combination therapies delivered parenterally, including monoclonal antibodies and supportive biologics, are gaining traction due to their efficacy in severe anthrax management.

- By End User

On the basis of end user, the anthrax treatment market is segmented into government organizations, hospitals, academic and research institutes, and others. Hospitals dominated the market with a share of 50.3% in 2025, as they serve as primary treatment centers for acute anthrax cases and maintain essential stockpiles of antibiotics and antitoxins. Hospitals also play a key role in post-exposure prophylaxis, management of severe infections, and administration of combination therapies. The growing awareness of anthrax symptoms among healthcare providers and increased training in emergency response protocols further support the hospital segment.

The Government Organizations segment is expected to witness the fastest growth rate from 2026 to 2033, driven by strategic national stockpiling programs and biodefense initiatives. Governments are increasingly investing in vaccines, antitoxins, and emergency response measures to mitigate bioterrorism threats. Collaborative programs between governments and private biotech firms for research, stockpiling, and rapid deployment are boosting demand in this segment. Furthermore, international partnerships and grants for anthrax preparedness in high-risk regions are accelerating growth, making government organizations a critical and rapidly expanding end-user segment.

Anthrax Treatment Market Regional Analysis

- North America dominated the anthrax treatment market with the largest revenue share of 38.7% in 2025, driven by well-established healthcare infrastructure, strategic stockpiling programs, early adoption of advanced biologics, and significant investments in R&D by key pharmaceutical companies

- Healthcare providers and government agencies in the region prioritize early detection, rapid treatment, and emergency stockpiling of antibiotics, vaccines, and antitoxins, ensuring timely management of anthrax cases

- This widespread adoption is further supported by strong R&D investments, collaborations between public and private sectors, and awareness programs on bioterrorism and zoonotic disease risks, establishing anthrax treatments as an essential component of national health security strategies in both civilian and defense sectors

U.S. Anthrax Treatment Market Insight

The U.S. anthrax treatment market captured the largest revenue share of 79% in 2025 within North America, fueled by strong government initiatives for biodefense preparedness and strategic stockpiling of vaccines, antibiotics, and antitoxins. Healthcare providers prioritize rapid diagnosis and treatment of anthrax cases, particularly in high-risk zones and laboratories. The growing focus on bioterrorism preparedness, coupled with rising awareness of zoonotic infections, is driving demand for advanced therapies. Moreover, collaboration between federal agencies and private pharmaceutical companies for R&D and emergency distribution further propels market expansion. The presence of well-established healthcare infrastructure and advanced treatment protocols ensures timely administration of therapies during outbreaks.

Europe Anthrax Treatment Market Insight

欧州の炭疽治療市場は、厳格な公衆衛生規制と人獣共通感染症および職業上のリスクに対する意識の高まりを背景に、予測期間を通じて大幅な年平均成長率(CAGR)で拡大すると予測されています。病院や研究機関における先進的な抗生物質、ワクチン、抗毒素の採用拡大が市場の成長を促進しています。欧州諸国は、生物学的脅威への備えを重視し、備蓄プログラムを強化し、新規抗毒素の研究を支援しています。さらに、家畜における炭疽病の蔓延と、農業および獣医分野における予防措置が相まって、市場の普及をさらに加速させています。公衆衛生ネットワーク全体にわたる診断および治療戦略の統合は、地域的な対応能力を強化します。

英国炭疽病治療市場に関する洞察

英国の炭疽病治療市場は、政府主導の生物防衛プログラムや、家畜や実験室における炭疽病リスクへの意識の高まりを背景に、予測期間中に著しい年平均成長率(CAGR)で成長すると予想されています。公衆衛生機関は、ワクチン接種、予防的抗生物質投与、迅速な介入プロトコルを積極的に推進しています。英国の強力な研究インフラに加え、病院、学術機関、政府機関間の連携も、市場の成長を支え続けると見込まれています。潜在的な生物学的脅威に対する備蓄や緊急対応計画への投資の増加も、炭疽病治療の普及をさらに促進しています。稀ではあるものの影響の大きい感染症への備えに重点を置く英国の姿勢は、市場の持続的な拡大を後押ししています。

ドイツ炭疽病治療市場に関する洞察

ドイツの炭疽病治療市場は、バイオテロのリスクや農業・研究室における職業的曝露に対する意識の高まりを背景に、予測期間中に著しい年平均成長率(CAGR)で拡大すると見込まれています。ドイツの高度に発達した医療制度は、予防措置と緊急時対応への強い重点と相まって、炭疽病治療薬の普及を後押ししています。病院、研究機関、政府の備蓄プログラムは、ワクチンと抗毒素に対する市場需要を牽引しています。さらに、バイオセーフティ、疾病監視、迅速な介入を促進する取り組みが、治療へのアクセスを向上させています。先進的な治療法を国家緊急対応戦略に統合することで、市場はさらに強化されます。

アジア太平洋地域における炭疽病治療市場の洞察

アジア太平洋地域の炭疽治療薬市場は、畜産生産の増加、炭疽病発生件数の増加、中国、インド、日本などの国々における医療制度の強化を背景に、2026年から2033年の予測期間中に年平均成長率(CAGR)23%という最速の成長を遂げると見込まれています。疾病予防と迅速対応プログラムに関する政府の取り組みの拡大が、市場の普及を後押ししています。同地域の医薬品製造能力の拡大は、ワクチンと抗毒素の入手可能性と価格の手頃さを向上させています。さらに、医療従事者、獣医師、農村地域における意識の高まりが、予防および治療措置の導入を加速させています。備蓄と迅速な流通のための官民連携による戦略的な協力も、市場の成長をさらに促進しています。

日本の炭疽病治療市場に関する洞察

日本の炭疽病治療市場は、先進的な医療インフラ、生物兵器対策への強い取り組み、そして感染症管理に関する厳格な規制プロトコルを背景に、勢いを増している。日本市場では、迅速な診断、予防的治療、そしてワクチンや抗毒素の緊急備蓄が重視されている。病院や研究施設における高度な診断・治療ソリューションの統合が成長を牽引している。さらに、農業および検査分野における公衆衛生啓発プログラムや備えの取り組みが、早期介入を促進している。日本の医療および生物製剤開発における技術力は、次世代抗毒素や併用療法の導入を支えている。

インドの炭疽病治療市場に関する洞察

インドの炭疽病治療市場は、畜産業の拡大、炭疽病の頻発、疾病予防・管理に関する政府の取り組みの強化を背景に、2025年にはアジア太平洋地域で最大の市場収益シェアを占める見込みです。インドでは、農村部の医療インフラ整備とワクチン接種プログラムへの注力が高まっており、炭疽病治療へのアクセスが向上しています。公立病院と私立病院の両方で、高度な抗生物質、抗毒素、ワクチンの導入が進んでいます。さらに、農家や獣医師を対象とした啓発キャンペーンにより、早期発見と迅速な治療が促進されています。国内の医薬品製造能力の拡大と、備蓄および迅速な展開に対する政府の支援が相まって、インド市場の成長を牽引する主要因となっています。

炭疽病治療薬の市場シェア

炭疽菌治療業界は主に、以下のような実績のある企業によって牽引されています。

- Emergent BioSolutions Inc.(米国)

- Elusys Therapeutics, Inc. (米国)

- ポートン・バイオファーマ・リミテッド(英国)

- ファイザー社(米国)

- バイエルAG(ドイツ)

- サノフィ(フランス)

- サン・ファーマシューティカル・インダストリーズ社(インド)

- ソリジェニックス社(米国)

- テバ・ファーマシューティカル・インダストリーズ社(イスラエル)

- 武田薬品工業株式会社(日本)

- アレンビック・ファーマシューティカルズ社(インド)

- ルパン・リミテッド(インド)

- パラテック・ファーマシューティカルズ社(米国)

- Altimmune, Inc. (U.S.)

- Hikma Pharmaceuticals PLC (U.K.)

- CSL Seqirus (Australia)

- Bharat Biotech International Ltd. (India)

- Novavax, Inc. (U.S.)

- Panacea Biotec Ltd. (India)

- Tonix Pharmaceuticals Holding Corp. (U.S.)

What are the Recent Developments in Global Anthrax Treatment Market?

- In September 2025, Emergent BioSolutions secured a USD 30 million contract modification from BARDA to continue supplying CYFENDUS® anthrax vaccine doses with deliveries planned through early 2026, further strengthening U.S. medical countermeasure stocks

- In January 2025, Emergent BioSolutions announced exercise of a USD 20 million contract option to supply BioThrax® (Anthrax Vaccine Adsorbed) to the U.S. Department of Defense for pre‑exposure prophylaxis use among service members, reinforcing military readiness against anthrax threats

- In December 2024, the U.S. Biomedical Advanced Research and Development Authority (BARDA) awarded a USD 50 million contract option to Emergent BioSolutions to procure additional doses of CYFENDUS® (Anthrax Vaccine Adsorbed, Adjuvanted), supporting biodefense stockpile preparedness with deliveries slated through April 2025

- In September 2024, the U.S. CDC and Louisiana Department of Health reported a rare clinical use of the monoclonal antibody antitoxin obiltoxaximab to successfully treat a severe case of welder’s anthrax, demonstrating real‑world therapeutic application of approved anthrax antitoxins

- In November 2023, BARDA exercised a USD 75 million option under an existing agreement with Emergent BioSolutions for additional doses of the newly FDA‑approved Cyfendus anthrax vaccine, marking a major federal procurement following its 2023 approval

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。