世界の自動車用クランクトリガー市場の規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

2.04 Billion

USD

3.16 Billion

2025

2033

USD

2.04 Billion

USD

3.16 Billion

2025

2033

| 2026 –2033 | |

| USD 2.04 Billion | |

| USD 3.16 Billion | |

| % | |

|

世界の自動車用クランクトリガー市場のセグメンテーション:VDC電力(7.5~15VDC、15~30VDC、30VDC超)、トリガーホイール径(6インチ、6.5インチ、7インチ、8インチ、8インチ超)、車両タイプ(乗用車、小型商用車、大型商用車、オフロード車、農業用車両)、販売チャネル(OEM、アフターマーケット、オフライン販売、オンライン販売)別 - 業界動向と2033年までの予測

自動車用クランクトリガー市場規模

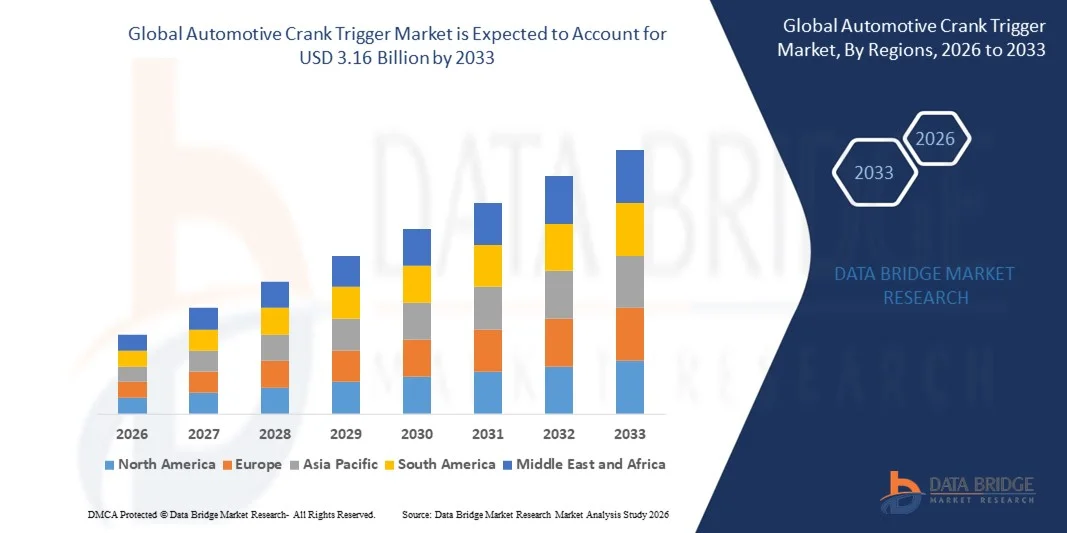

- 世界の自動車用クランクトリガー市場規模は、2025年には20億4,000万米ドルと評価され、予測期間中の年平均成長率(CAGR)5.60%で、2033年には31億6,000万米ドル に達すると予測されている。

- 市場の成長は、主に先進的なエンジン管理システムに対する需要の高まりと世界的な自動車生産の増加によって促進されている。

- 乗用車、商用車、電気自動車におけるエンジン効率と性能向上を目的としたクランクトリガーシステムの採用拡大は、市場拡大をさらに後押ししている。

自動車用クランクトリガー市場分析

- 自動車各分野における排出ガス削減、燃費向上、エンジン性能向上への注目の高まりにより、市場は着実に成長している。

- センサー技術と精密エンジン部品の研究開発への投資増加は、クランクトリガーシステムの世界的な進歩と普及に貢献している。

- 北米は、乗用車に対する旺盛な需要、厳しい排出ガス規制、そしてエンジン性能と効率への注目の高まりを背景に、2025年には自動車用クランクトリガー市場で最大の収益シェア35.8%を占め、市場を牽引した。

- アジア太平洋地域は、自動車生産の増加、都市化、可処分所得の増加、自動車製造およびアフターマーケット部門の拡大を背景に、世界の自動車用クランクトリガー市場において最も高い成長率を示すと予想されている。

- 7.5~15VDCセグメントは、乗用車や小型商用車における幅広い使用を背景に、2025年に最大の市場収益シェアを占めました。これらのトリガーは、標準的な自動車用電気システムとの信頼性の高い電圧互換性を提供し、幅広い車種において安定したエンジン性能と正確なタイミング制御を保証します。

レポートの範囲と自動車用クランクトリガー市場のセグメンテーション

|

属性 |

自動車用クランクトリガーの主要市場インサイト |

|

対象分野 |

|

|

対象国 |

北米

ヨーロッパ

アジア太平洋

中東およびアフリカ

南アメリカ

|

|

主要市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

Data Bridge Market Researchチームが作成した市場レポートには、市場価値、成長率、市場セグメント、地理的範囲、市場プレーヤー、市場シナリオといった市場に関する洞察に加え、詳細な専門家分析、輸出入分析、価格分析、生産消費分析、PESTLE分析が含まれています。 |

自動車用クランクトリガー市場の動向

高度なエンジン管理システムに対する需要の高まり

- 車両の性能と効率への注目の高まりは、自動車用クランクトリガー市場を大きく変えつつあり、メーカーは高精度で信頼性の高いトリガーシステムをますます好むようになっています。自動車用クランクトリガーは、エンジンタイミングの最適化、燃費の向上、そして車両全体の性能向上に貢献できることから、ますます注目を集めています。この傾向は、乗用車、商用車、産業用途など、あらゆる分野での採用を促進し、メーカーは進化する自動車規格に対応した新しい設計でイノベーションを起こすよう促されています。

- 排出ガス規制と燃費に対する意識の高まりにより、ハイブリッド車、電気自動車、従来型自動車における高度なクランクセンサーの需要が加速している。自動車メーカーは、エンジン制御を強化し、厳しい排出ガス基準に適合する部品を積極的に求めており、サプライヤーは精密なエンジニアリングと耐久性の向上に注力している。

- 性能と信頼性のトレンドは購買決定に影響を与えており、メーカーは堅牢な設計、長寿命、最新のエンジンシステムとの互換性を重視している。これらの要素は、競争の激しい自動車部品市場においてブランドが製品を差別化し、OEMパートナーシップを強化するのに役立つだけでなく、研究開発および試験施設への投資も促進している。

- For instance, in 2024, Bosch in Germany and Denso in Japan expanded their crank trigger product lines for next-generation internal combustion engines and hybrid vehicles. These launches were introduced in response to growing demand for high-performance, fuel-efficient, and emission-compliant vehicles, with distribution across OEMs and aftermarket channels. The products were also marketed as precision-engineered solutions, enhancing brand reliability and repeat business among automakers

- While demand for automotive crank triggers is growing, sustained market expansion depends on continuous R&D, cost-effective production, and maintaining performance under extreme conditions. Manufacturers are also focusing on improving scalability, supply chain efficiency, and developing innovative solutions that balance cost, quality, and durability for broader adoption

Automotive Crank Trigger Market Dynamics

Driver

Growing Adoption of Advanced Engine Management Systems

- Rising demand for precision engine control is a major driver for the automotive crank trigger market. Manufacturers are increasingly integrating advanced crank triggers to enhance ignition timing, fuel injection, and overall engine efficiency, supporting emission reduction and performance optimization

- Expanding applications in passenger cars, commercial vehicles, and hybrid/electric vehicles are influencing market growth. Crank triggers help maintain accurate engine synchronization, enabling manufacturers to meet regulatory standards for fuel efficiency and emission control

- Automotive OEMs and aftermarket suppliers are actively promoting crank trigger solutions through product innovation, testing certifications, and strategic partnerships. These efforts are supported by the growing preference for high-performance and durable vehicle components, and they also encourage collaborations to improve technological capabilities and reliability

- For instance, in 2023, NGK in Japan and Delphi Technologies in U.S. reported increased adoption of advanced crank triggers in internal combustion engines. This expansion followed higher demand for fuel-efficient, emission-compliant, and high-performance vehicles, driving repeat purchases and product differentiation. Both companies also highlighted durability and precision in marketing campaigns to strengthen OEM trust and brand recognition

- Although rising performance and regulatory trends support growth, wider adoption depends on cost optimization, supply of high-quality materials, and scalable manufacturing processes. Investment in advanced manufacturing, precision testing, and materials sourcing will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

High Cost and Technological Complexity Compared to Conventional Components

- The relatively higher cost of advanced automotive crank triggers compared to conventional mechanical alternatives remains a key challenge, limiting adoption among price-sensitive vehicle segments. Higher material costs and complex engineering contribute to elevated pricing

- Limited awareness and technical understanding among some aftermarket operators restrict adoption in certain regions. This also leads to slower innovation uptake in emerging markets where educational initiatives on high-precision crank triggers are minimal

- Supply chain and manufacturing complexities also impact market growth, as crank triggers require precise machining, quality testing, and adherence to stringent OEM standards. Logistical and production challenges increase operational costs, requiring investment in advanced manufacturing facilities

- For instance, in 2024, distributors in India and Brazil supplying automotive components reported slower uptake due to higher prices and limited awareness of performance advantages. Stringent testing requirements and production scalability were additional barriers. These factors also prompted some vehicle manufacturers to limit sourcing from smaller suppliers, affecting market penetration

- Overcoming these challenges will require cost-efficient production, expanded supplier networks, and focused educational initiatives for OEMs and aftermarket operators. Collaboration with component suppliers, certification bodies, and automakers can help unlock the long-term growth potential of the global automotive crank trigger market. Furthermore, developing cost-competitive, high-performance solutions will be essential for widespread adoption

Automotive Crank Trigger Market Scope

The automotive crank trigger market is segmented into four notable segments based on VDC power, trigger wheel diameter, vehicle type, and sales channel.

- By VDC Power

On the basis of VDC power, the market is segmented into 7.5 to 15 VDC, 15 to 30 VDC, and more than 30 VDC. The 7.5 to 15 VDC segment held the largest market revenue share in 2025, driven by its widespread use in passenger vehicles and light commercial vehicles. These triggers offer reliable voltage compatibility with standard automotive electrical systems, ensuring stable engine performance and precise timing control for a broad range of vehicles.

The 15 to 30 VDC segment is expected to witness the fastest growth rate from 2026 to 2033, owing to its adoption in heavy commercial vehicles, OTR (off-the-road) vehicles, and specialized industrial engines. The higher voltage triggers enable better durability and performance in demanding applications, making them increasingly preferred for larger engines and industrial equipment.

- By Trigger Wheel Diameter

On the basis of trigger wheel diameter, the market is segmented into 6-inch, 6.5-inch, 7-inch, 8-inch, and more than 8 inches. The 6-inch segment held the largest market revenue share in 2025 due to its compatibility with standard passenger vehicle engines and its cost-effectiveness. Smaller diameters allow precise rotation sensing and easy integration with compact engine designs.

The 8-inch segment is expected to witness the fastest growth rate from 2026 to 2033, driven by adoption in larger commercial vehicles and high-performance engines requiring enhanced signal accuracy. Larger diameter trigger wheels provide better angular resolution, supporting precise engine timing and advanced fuel management systems.

- By Vehicle Type

On the basis of vehicle type, the market is segmented into passenger vehicles, light commercial vehicles, heavy commercial vehicles, OTR (off-the-road) vehicles, and farm services vehicles. The passenger vehicles segment held the largest market revenue share in 2025, supported by high production volumes and growing demand for fuel-efficient, emission-compliant vehicles. Crank triggers in this segment improve engine performance and compliance with emission regulations.

The heavy commercial vehicles segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing adoption of advanced engine management systems in trucks, buses, and construction machinery. These triggers enable accurate timing for large engines, ensuring reliability and efficiency under demanding operational conditions.

- By Sales Channel

On the basis of sales channel, the market is segmented into OEM, aftermarket, offline sales, and online sales. The OEM segment held the largest market revenue share in 2025 due to strong partnerships with vehicle manufacturers and the integration of crank triggers into new engines during production. OEM supply ensures product quality, compatibility, and warranty support.

The aftermarket segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for replacement and upgrade components in aging vehicles. Growth in online sales and digital marketplaces is also accelerating aftermarket adoption, making crank triggers more accessible to vehicle owners and repair shops globally.

Automotive Crank Trigger Market Regional Analysis

- North America dominated the automotive crank trigger market with the largest revenue share of 35.8% in 2025, driven by strong demand for passenger vehicles, stringent emission regulations, and a growing focus on engine performance and efficiency

- Consumers and manufacturers in the region are increasingly prioritizing advanced ignition systems, reliability, and precision in engine timing, which enhances fuel efficiency, reduces emissions, and ensures compliance with regulatory standards

- This widespread adoption is further supported by high automotive production rates, technological advancements, and the growing preference for OEM-quality components, establishing crank triggers as a critical component in modern engines

U.S. Automotive Crank Trigger Market Insight

The U.S. automotive crank trigger market captured the largest revenue share in 2025 within North America, fueled by the rapid production of passenger and light commercial vehicles. Increasing adoption of advanced engine management systems and the demand for improved fuel efficiency are driving market growth. The integration of crank triggers with electronic ignition and engine control modules ensures precise timing, enhancing vehicle performance. Moreover, stringent regulatory norms related to emissions and safety are accelerating the replacement of conventional triggers with high-precision automotive crank triggers.

Europe Automotive Crank Trigger Market Insight

The Europe automotive crank trigger market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stricter emission standards and rising adoption of high-performance engines. Growth in the passenger and commercial vehicle sectors, combined with technological advancements in engine control systems, is fostering demand. European manufacturers are also focused on improving durability, accuracy, and compatibility with hybrid and electric vehicle powertrains. The increasing trend toward vehicle electrification and precision engine components is positively influencing market expansion.

U.K. Automotive Crank Trigger Market Insight

The U.K. automotive crank trigger market is expected to witness substantial growth from 2026 to 2033, driven by rising automotive production and demand for fuel-efficient engines. Growing awareness regarding vehicle performance, safety, and emission compliance is pushing OEMs and aftermarket suppliers to adopt high-precision crank triggers. The integration of triggers with advanced engine management systems and diagnostics further supports market growth. In addition, the country’s strong automotive R&D infrastructure and focus on innovation are facilitating widespread adoption of technologically advanced components.

Germany Automotive Crank Trigger Market Insight

The Germany automotive crank trigger market is projected to witness rapid growth from 2026 to 2033, fueled by strong automotive manufacturing and the increasing focus on emission reduction. German automakers are investing in engine technologies that enhance performance and fuel efficiency, supporting demand for high-quality crank triggers. The market is also driven by the preference for durable, precise, and reliable ignition components compatible with modern internal combustion engines. Growing trends in hybrid vehicles and advanced engine control systems further bolster market expansion.

Asia-Pacific Automotive Crank Trigger Market Insight

アジア太平洋地域の自動車用クランクトリガー市場は、中国、インド、日本などの国々における急速な都市化、自動車生産の増加、可処分所得の上昇を背景に、2026年から2033年にかけて著しい成長が見込まれています。乗用車および商用車セグメントの拡大に加え、自動車製造を支援する政府の取り組みも需要を押し上げています。地域メーカーによるコスト効率が高く高品質なクランクトリガーの入手可能性は、OEMおよびアフターマーケット企業にとってのアクセス性を向上させています。さらに、先進的なエンジン制御技術の採用は、エンジンタイミングシステムの精度と信頼性を高めています。

日本自動車用クランクトリガー市場インサイト

日本の自動車用クランクトリガー市場は、先進的な自動車技術、燃費向上への注力、そして信頼性の高い車両部品への高い需要を背景に、2026年から2033年にかけて力強い成長が見込まれています。日本の自動車メーカーは、精密なエンジンタイミングと性能最適化を重視しており、これが先進的なクランクトリガーの採用を促進しています。ハイブリッドエンジンや次世代内燃機関との統合も、需要をさらに高めています。加えて、日本の強力な自動車研究開発エコシステムと、品質・耐久性へのこだわりも、市場の持続的な成長に貢献しています。

中国自動車用クランクトリガー市場インサイト

中国の自動車用クランクトリガー市場は、車両生産の急速な増加、都市化、先進エンジン技術の普及拡大を背景に、2025年にはアジア太平洋地域で最大の収益シェアを占める見込みです。国内自動車メーカーは、燃費向上と厳しい排出ガス規制への対応のため、精密エンジン部品に多額の投資を行っています。競争力のある価格と高品質のクランクトリガーが入手可能になったことで、乗用車、商用車、オフロード車など、幅広い車種への採用が進んでいます。さらに、自動車製造と技術革新を支援する政府の取り組みも、市場拡大を後押ししています。

自動車用クランクトリガーの市場シェア

自動車用クランクトリガー業界は、主に以下のような実績のある企業によって牽引されています。

- ホリー・パフォーマンス・プロダクツ社(米国)

- シボレー・パフォーマンス(米国)

- モパー(米国)

- COMPパフォーマンスグループ(米国)

- モロソ(米国)

- Rエンジニアリングワークス(米国)

- 重慶広連慶鈴汽車部品有限公司(中国)

- 北京イーリーチテクノロジー株式会社(中国)

- 温州百安汽車零部件有限公司(中国)

- AEMパフォーマンスエレクトロニクス(米国)

- MSDパフォーマンス(米国)

- ドーマン・プロダクツ(米国)

- アクトロン・オートモーティブ(米国)

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。