Global Automotive Crank Trigger Market

Market Size in USD Billion

USD

2.04 Billion

USD

3.16 Billion

2025

2033

USD

2.04 Billion

USD

3.16 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.04 Billion | |

| USD 3.16 Billion | |

| % | |

|

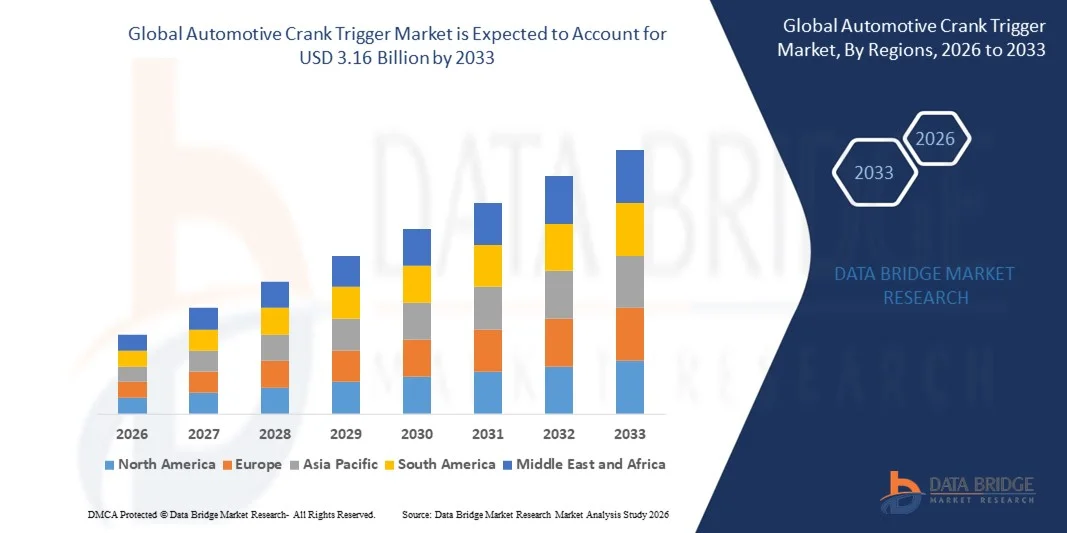

Automotive Crank Trigger Market Size

- The global automotive crank trigger market size was valued at USD 2.04 billion in 2025 and is expected to reach USD 3.16 billion by 2033, at a CAGR of 5.60% during the forecast period

- The market growth is largely fuelled by the increasing demand for advanced engine management systems and rising vehicle production globally

- Growing adoption of crank trigger systems in passenger cars, commercial vehicles, and electric vehicles to improve engine efficiency and performance is further supporting market expansion

Automotive Crank Trigger Market Analysis

- The market is experiencing steady growth due to the increasing focus on emission reduction, fuel efficiency, and enhanced engine performance across automotive segments

- Rising investment in R&D for sensor technologies and precision engine components is contributing to the advancement and adoption of crank trigger systems globally

- North America dominated the automotive crank trigger market with the largest revenue share of 35.8% in 2025, driven by strong demand for passenger vehicles, stringent emission regulations, and a growing focus on engine performance and efficiency

- Asia-Pacific region is expected to witness the highest growth rate in the global automotive crank trigger market, driven by increasing vehicle production, urbanization, rising disposable incomes, and expanding automotive manufacturing and aftermarket sectors

- The 7.5 to 15 VDC segment held the largest market revenue share in 2025, driven by its widespread use in passenger vehicles and light commercial vehicles. These triggers offer reliable voltage compatibility with standard automotive electrical systems, ensuring stable engine performance and precise timing control for a broad range of vehicles

Report Scope and Automotive Crank Trigger Market Segmentation

|

Attributes |

Automotive Crank Trigger Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Automotive Crank Trigger Market Trends

Rising Demand for Advanced Engine Management Systems

- The growing focus on vehicle performance and efficiency is significantly shaping the automotive crank trigger market, as manufacturers increasingly prefer high-precision, reliable triggering systems. Automotive crank triggers are gaining traction due to their ability to optimize engine timing, improve fuel efficiency, and enhance overall vehicle performance. This trend strengthens their adoption across passenger cars, commercial vehicles, and industrial applications, encouraging manufacturers to innovate with new designs that cater to evolving automotive standards

- Increasing awareness around emissions regulations and fuel economy has accelerated the demand for advanced crank triggers in hybrid, electric, and conventional vehicles. Automakers are actively seeking components that enhance engine control and comply with stringent emission norms, prompting suppliers to focus on precision engineering and durability improvements

- Performance and reliability trends are influencing purchasing decisions, with manufacturers emphasizing robust designs, extended lifecycle, and compatibility with modern engine systems. These factors are helping brands differentiate products in a competitive automotive component market and strengthen OEM partnerships, while also driving investment in R&D and testing facilities

- For instance, in 2024, Bosch in Germany and Denso in Japan expanded their crank trigger product lines for next-generation internal combustion engines and hybrid vehicles. These launches were introduced in response to growing demand for high-performance, fuel-efficient, and emission-compliant vehicles, with distribution across OEMs and aftermarket channels. The products were also marketed as precision-engineered solutions, enhancing brand reliability and repeat business among automakers

- While demand for automotive crank triggers is growing, sustained market expansion depends on continuous R&D, cost-effective production, and maintaining performance under extreme conditions. Manufacturers are also focusing on improving scalability, supply chain efficiency, and developing innovative solutions that balance cost, quality, and durability for broader adoption

Automotive Crank Trigger Market Dynamics

Driver

Growing Adoption of Advanced Engine Management Systems

- Rising demand for precision engine control is a major driver for the automotive crank trigger market. Manufacturers are increasingly integrating advanced crank triggers to enhance ignition timing, fuel injection, and overall engine efficiency, supporting emission reduction and performance optimization

- Expanding applications in passenger cars, commercial vehicles, and hybrid/electric vehicles are influencing market growth. Crank triggers help maintain accurate engine synchronization, enabling manufacturers to meet regulatory standards for fuel efficiency and emission control

- Automotive OEMs and aftermarket suppliers are actively promoting crank trigger solutions through product innovation, testing certifications, and strategic partnerships. These efforts are supported by the growing preference for high-performance and durable vehicle components, and they also encourage collaborations to improve technological capabilities and reliability

- For instance, in 2023, NGK in Japan and Delphi Technologies in U.S. reported increased adoption of advanced crank triggers in internal combustion engines. This expansion followed higher demand for fuel-efficient, emission-compliant, and high-performance vehicles, driving repeat purchases and product differentiation. Both companies also highlighted durability and precision in marketing campaigns to strengthen OEM trust and brand recognition

- Although rising performance and regulatory trends support growth, wider adoption depends on cost optimization, supply of high-quality materials, and scalable manufacturing processes. Investment in advanced manufacturing, precision testing, and materials sourcing will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

High Cost and Technological Complexity Compared to Conventional Components

- The relatively higher cost of advanced automotive crank triggers compared to conventional mechanical alternatives remains a key challenge, limiting adoption among price-sensitive vehicle segments. Higher material costs and complex engineering contribute to elevated pricing

- Limited awareness and technical understanding among some aftermarket operators restrict adoption in certain regions. This also leads to slower innovation uptake in emerging markets where educational initiatives on high-precision crank triggers are minimal

- Supply chain and manufacturing complexities also impact market growth, as crank triggers require precise machining, quality testing, and adherence to stringent OEM standards. Logistical and production challenges increase operational costs, requiring investment in advanced manufacturing facilities

- For instance, in 2024, distributors in India and Brazil supplying automotive components reported slower uptake due to higher prices and limited awareness of performance advantages. Stringent testing requirements and production scalability were additional barriers. These factors also prompted some vehicle manufacturers to limit sourcing from smaller suppliers, affecting market penetration

- Overcoming these challenges will require cost-efficient production, expanded supplier networks, and focused educational initiatives for OEMs and aftermarket operators. Collaboration with component suppliers, certification bodies, and automakers can help unlock the long-term growth potential of the global automotive crank trigger market. Furthermore, developing cost-competitive, high-performance solutions will be essential for widespread adoption

Automotive Crank Trigger Market Scope

The automotive crank trigger market is segmented into four notable segments based on VDC power, trigger wheel diameter, vehicle type, and sales channel.

- By VDC Power

On the basis of VDC power, the market is segmented into 7.5 to 15 VDC, 15 to 30 VDC, and more than 30 VDC. The 7.5 to 15 VDC segment held the largest market revenue share in 2025, driven by its widespread use in passenger vehicles and light commercial vehicles. These triggers offer reliable voltage compatibility with standard automotive electrical systems, ensuring stable engine performance and precise timing control for a broad range of vehicles.

The 15 to 30 VDC segment is expected to witness the fastest growth rate from 2026 to 2033, owing to its adoption in heavy commercial vehicles, OTR (off-the-road) vehicles, and specialized industrial engines. The higher voltage triggers enable better durability and performance in demanding applications, making them increasingly preferred for larger engines and industrial equipment.

- By Trigger Wheel Diameter

On the basis of trigger wheel diameter, the market is segmented into 6-inch, 6.5-inch, 7-inch, 8-inch, and more than 8 inches. The 6-inch segment held the largest market revenue share in 2025 due to its compatibility with standard passenger vehicle engines and its cost-effectiveness. Smaller diameters allow precise rotation sensing and easy integration with compact engine designs.

The 8-inch segment is expected to witness the fastest growth rate from 2026 to 2033, driven by adoption in larger commercial vehicles and high-performance engines requiring enhanced signal accuracy. Larger diameter trigger wheels provide better angular resolution, supporting precise engine timing and advanced fuel management systems.

- By Vehicle Type

On the basis of vehicle type, the market is segmented into passenger vehicles, light commercial vehicles, heavy commercial vehicles, OTR (off-the-road) vehicles, and farm services vehicles. The passenger vehicles segment held the largest market revenue share in 2025, supported by high production volumes and growing demand for fuel-efficient, emission-compliant vehicles. Crank triggers in this segment improve engine performance and compliance with emission regulations.

The heavy commercial vehicles segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing adoption of advanced engine management systems in trucks, buses, and construction machinery. These triggers enable accurate timing for large engines, ensuring reliability and efficiency under demanding operational conditions.

- By Sales Channel

On the basis of sales channel, the market is segmented into OEM, aftermarket, offline sales, and online sales. The OEM segment held the largest market revenue share in 2025 due to strong partnerships with vehicle manufacturers and the integration of crank triggers into new engines during production. OEM supply ensures product quality, compatibility, and warranty support.

The aftermarket segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for replacement and upgrade components in aging vehicles. Growth in online sales and digital marketplaces is also accelerating aftermarket adoption, making crank triggers more accessible to vehicle owners and repair shops globally.

Automotive Crank Trigger Market Regional Analysis

- North America dominated the automotive crank trigger market with the largest revenue share of 35.8% in 2025, driven by strong demand for passenger vehicles, stringent emission regulations, and a growing focus on engine performance and efficiency

- Consumers and manufacturers in the region are increasingly prioritizing advanced ignition systems, reliability, and precision in engine timing, which enhances fuel efficiency, reduces emissions, and ensures compliance with regulatory standards

- This widespread adoption is further supported by high automotive production rates, technological advancements, and the growing preference for OEM-quality components, establishing crank triggers as a critical component in modern engines

U.S. Automotive Crank Trigger Market Insight

The U.S. automotive crank trigger market captured the largest revenue share in 2025 within North America, fueled by the rapid production of passenger and light commercial vehicles. Increasing adoption of advanced engine management systems and the demand for improved fuel efficiency are driving market growth. The integration of crank triggers with electronic ignition and engine control modules ensures precise timing, enhancing vehicle performance. Moreover, stringent regulatory norms related to emissions and safety are accelerating the replacement of conventional triggers with high-precision automotive crank triggers.

Europe Automotive Crank Trigger Market Insight

The Europe automotive crank trigger market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stricter emission standards and rising adoption of high-performance engines. Growth in the passenger and commercial vehicle sectors, combined with technological advancements in engine control systems, is fostering demand. European manufacturers are also focused on improving durability, accuracy, and compatibility with hybrid and electric vehicle powertrains. The increasing trend toward vehicle electrification and precision engine components is positively influencing market expansion.

U.K. Automotive Crank Trigger Market Insight

The U.K. automotive crank trigger market is expected to witness substantial growth from 2026 to 2033, driven by rising automotive production and demand for fuel-efficient engines. Growing awareness regarding vehicle performance, safety, and emission compliance is pushing OEMs and aftermarket suppliers to adopt high-precision crank triggers. The integration of triggers with advanced engine management systems and diagnostics further supports market growth. In addition, the country’s strong automotive R&D infrastructure and focus on innovation are facilitating widespread adoption of technologically advanced components.

Germany Automotive Crank Trigger Market Insight

The Germany automotive crank trigger market is projected to witness rapid growth from 2026 to 2033, fueled by strong automotive manufacturing and the increasing focus on emission reduction. German automakers are investing in engine technologies that enhance performance and fuel efficiency, supporting demand for high-quality crank triggers. The market is also driven by the preference for durable, precise, and reliable ignition components compatible with modern internal combustion engines. Growing trends in hybrid vehicles and advanced engine control systems further bolster market expansion.

Asia-Pacific Automotive Crank Trigger Market Insight

The Asia-Pacific automotive crank trigger market is expected to witness significant growth from 2026 to 2033, driven by rapid urbanization, increasing vehicle production, and rising disposable incomes in countries such as China, India, and Japan. Expansion of the passenger and commercial vehicle segments, coupled with government initiatives supporting automotive manufacturing, is boosting demand. The availability of cost-effective, high-quality crank triggers from regional manufacturers enhances accessibility for OEMs and aftermarket players. Furthermore, the adoption of advanced engine control technologies is promoting precision and reliability in engine timing systems.

Japan Automotive Crank Trigger Market Insight

The Japan automotive crank trigger market is expected to witness strong growth from 2026 to 2033 due to the country’s advanced automotive technology, focus on fuel efficiency, and high demand for reliable vehicle components. Japanese manufacturers prioritize precision engine timing and performance optimization, driving adoption of advanced crank triggers. Integration with hybrid and next-generation internal combustion engines further enhances demand. In addition, Japan’s strong automotive R&D ecosystem and emphasis on quality and durability contribute to sustained market growth.

China Automotive Crank Trigger Market Insight

The China automotive crank trigger market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid growth in vehicle production, urbanization, and increasing adoption of advanced engine technologies. Domestic automakers are investing heavily in precision engine components to enhance fuel efficiency and meet stringent emission standards. The availability of competitively priced, high-quality crank triggers is facilitating adoption across passenger, commercial, and off-road vehicles. Furthermore, government initiatives supporting automotive manufacturing and technological upgrades are driving market expansion.

Automotive Crank Trigger Market Share

The Automotive Crank Trigger industry is primarily led by well-established companies, including:

- HOLLEY PERFORMANCE PRODUCTS, INC. (U.S.)

- Chevrolet Performance (U.S.)

- Mopar (U.S.)

- COMP Performance Group (U.S.)

- Moroso (U.S.)

- R ENGINEERING WORKS (U.S.)

- Chongqing Guanglian Qingling Auto Parts Co., Ltd. (China)

- Beijing Ereach Technology Co., Ltd. (China)

- Wenzhou Baian Auto Parts Co., Ltd. (China)

- AEM Performance Electronics (U.S.)

- MSD Performance (U.S.)

- Dorman Products (U.S.)

- Actron Automotive (U.S.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.