グローバルバッテリー材料市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

61.86 Billion

USD

141.22 Billion

2025

2033

USD

61.86 Billion

USD

141.22 Billion

2025

2033

| 2026 –2033 | |

| USD 61.86 Billion | |

| USD 141.22 Billion | |

| % | |

|

グローバル電池材料市場セグメンテーション、材料タイプ(Cathode、Anode、Electrolyte、セパレータ、その他)、電池の種類(リチウムイオン、鉛酸、ニッケルメタルハイド(NiMH)、ニッケルカドミウム(Ni-Cd)、その他)、アプリケーション(ポータブルデバイス、自動車、電子アイテム、パワーストレージ、その他) - 業界動向と2033への予測

電池材料 市場のサイズ

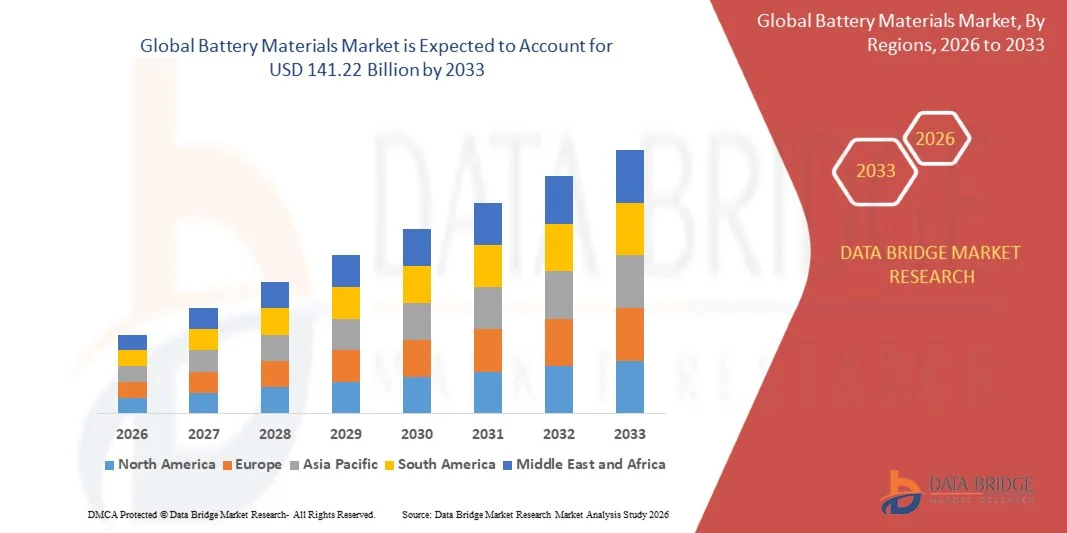

- グローバルバッテリー材料市場規模が評価されました2025年のUSD 61.86億そして到達する予定2033年までのUSD 141.22億, お問い合わせカリフォルニア 10.87%予報期間中

- 市場成長は、電気自動車、再生可能エネルギー貯蔵システム、およびキャソード、アノード、および電解質などの高性能電池材料の強力な要求を駆動するポータブル電子機器の急速な採用によって主に燃料を供給されます

- さらに、高ニッケルカソード、シリコン系アノード、ソリッドステート電解液などの次世代電池技術の投資が増加し、エネルギー密度、耐久性、安全性を高め、先進電池材料の採用と生産を加速し、業界の成長を著しく向上しています。

電池材料 市場分析

- 陰極、陽極、電解質および分離器の部品を含む電池材料は、自動車、電子工学およびエネルギー貯蔵の塗布で使用されるリチウム イオン、ニッケル ベースのおよび他の電池の化学品の性能、効率および長寿のために重要なです

- 電池材料の拡張需要は、主に電気モビリティへの世界的なシフトによって燃料を供給され、消費者の電子貫通を高め、再生可能エネルギーの統合に注力し、材料の性能と持続可能性を向上させるために研究開発の上昇投資と相まって

- アジア・パシフィックが電池材料市場を支配 2025年に、電気自動車の急速な採用による、消費者電子機器の生産を拡大し、電池材料の製造ハブの強い存在

- 北米は、EV導入の増加、再生可能エネルギー貯蔵システムの拡大、リチウムイオンおよび先進電池化学に対する堅牢な要求により、予測期間におけるバッテリー材料市場で最も急速に成長する地域であると予想されます

- リチウムイオンセグメントは、2025年に55.5%の市場シェアで市場を支配し、高エネルギー密度、長いサイクル寿命、および消費者の電子機器、電気自動車、エネルギー貯蔵アプリケーション全体に汎用性があります。 主要な電池メーカーによる研究・生産における強力な投資によるセグメントメリットにより、継続的な性能改善とコスト削減を実現します。 リチウムイオン電池は軽量設計および急速な充満機能による携帯用装置そして自動車セクターで好まれます

レポートスコープ・電池材料市場セグメント

| アトリビュート | 電池材料の主要市場の洞察 |

| カバーされる区分 |

|

| カバーされた国 | 北アメリカ

ヨーロッパ

アジアパシフィック

中東・アフリカ

南米

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、データブリッジ市場調査によってキュレーションされた市場レポートには、インポートエクスポート分析、生産能力概要、生産消費分析、価格推移分析、気候変動シナリオ、サプライチェーン分析、バリューチェーン分析、バリューチェーン分析、原材料/消耗品概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークなどがあります。 |

電池材料市場動向

「高エネルギー密度電池材料の調達要求」

- 電池材料市場における重要な傾向は、電気自動車、家電製品、エネルギー貯蔵システムで使用される電池のパフォーマンス、長寿、安全性を向上させることができる高エネルギー密度材料の需要の増加です。 メーカーやエンドユーザは、より長い運転範囲、高速充電、およびより高い出力を可能にする材料を優先し、陰極、陽極および電解技術の革新を推進しています

- たとえば、CATLは、電気自動車電池のエネルギー密度を高め、EV電池のパフォーマンスと競争力を強化するニッケルリッチNMC陰極材料に投資しています。 このような材料は、長持ちする高容量電池の消費者の期待に応えるために不可欠です

- 高度なシリコンベースの陽極の採用は、より高い容量と高速充電サイクルを可能にし、次世代のリチウムイオン電池の重要な活性化剤としてこれらの材料を配置するにつれて急速に増加しています

- 電池メーカーは、特に極端な動作条件下で、電池の効率と熱管理を改善する高電圧および高安定性電解液に焦点を当てています

- 再生可能エネルギー部門は、太陽光や風力発電から電力を蓄えるために、より高いエネルギー密度の電池を必要とするエネルギー貯蔵ソリューションの需要を駆動しています。 これは、グリッドスケールストレージアプリケーション用の高度なバッテリー材料の大規模な採用を奨励しています

- BASFやUmicoreなどのグローバルリーダーからの投資で、堅固でハイブリッドなバッテリー化学品の研究と開発が進んでおり、より安全で、よりエネルギー密度の高い、電気自動車や産業用ストレージアプリケーション向けの長持ちする材料を生産することを目指しています。

電池材料 市場 動的

ドライバー

「電気自動車とエネルギー貯蔵システムの導入」

- 電動モビリティと再生可能エネルギー貯蔵への世界的なシフトは、高性能なバッテリー材料の未曾有需要を主導しています。 この傾向は、厳格な排出規制、政府のインセンティブ、持続可能な輸送とエネルギーソリューションのための消費者の好みの増加によってサポートされています

- たとえば、テスラのギガファトリは、パナソニックやCATLなどの企業が供給する高度なカソードと陽極材料に大きく依存し、EVバッテリーの生産をスケールアップし、より長い運転範囲と充電能力を実現します。 オートメーカーとバッテリー素材のサプライヤー間の戦略的コラボレーションは、業界のイノベーションと採用を加速しています

- 公共輸送および商用フリートでの電動化は、最適化された材料組成を必要とする大型バッテリーパックの需要を増加させています。 高エネルギー密度および熱安定性を提供する電池材料は、これらの運用要件を満たすことが重要です

- 住宅、商用、およびユーティリティアプリケーション向けの静止エネルギー貯蔵システムの展開を増加させ、高度なバッテリー材料のさらなる要求を刺激します。 連続放電サイクルで長いサイクル寿命と信頼性を発揮する材料は、このセグメントでは特に価値があります。

- ソリッドステート電池、ハイブリッドEV、ポータブルエレクトロニクスなどの新興技術への電池材料の統合は、メーカーが効率性を改善し、コストを削減し、採用率を高めるソリューションを求めるため、市場ドライバを強化します

拘束/チャレンジ

「重要な原料に対するサプライチェーン依存性」

- 電池材料市場は、地理的に濃縮され、価格の揮発性であるリチウム、コバルト、ニッケル、グラファイトなどの重要な原材料に依存することによる重要な課題に直面しています。 この依存性は、大規模なバッテリー生産における供給リスクと潜在的なボトルネックを作成します

- たとえば、Umicoreと浙江Huayouコバルトは、カソード材料のコバルトの可用性に影響を与える経験豊富なサプライチェーン制約を持っています。 そのような混乱は、バッテリーメーカーのコストと生産のタイムラインを増加させることができます

- これらの原材料の抽出および処理には、運用の複雑性を高める、実質的な資本投資、規制遵守、および環境管理が必要です。 メーカーは、高品質の材料の安定供給を確保しながら、地政学的、貿易、環境的課題をナビゲートする必要があります

- バッテリーメーカー、EVメーカー、電子機器会社の間で原料の高競争は、価格を駆動し、市場の不確実性を作成することができ、利益率とバッテリー生産のスケーラビリティに影響を与える

- 市場は、重要な材料のリサイクルと再利用に関する制約に遭遇し続けています。 BASFなどの企業は、電池のリサイクル技術を推進していますが、これらのソリューションをスケーリングし、グローバルな需要に応える課題を解決し、サプライチェーンや材料の可用性に圧力をかけます。

電池材料 市場規模

市場は材料のタイプ、電池のタイプおよび適用に基づいて区分されます。

- 物質的なタイプによって

材料の種類に基づいて、電池材料市場は陰極、陽極、分離器および他のに分けられます。 陰極セグメントは、バッテリーのエネルギー密度、寿命、全体的なパフォーマンスを決定する重要な役割によって駆動され、2025年に最大の収益シェアで市場を支配しました。 製造業者は、電池の効率と安全に対する直接的な影響によるリチウムイオン電池の高品質の陰極材料を優先することが多い。 市場は、自動車メーカーや電子機器のプロデューサーとして高度な陰極の需要が長持ちし、高容量のエネルギー貯蔵ソリューションを求めています。 リチウム ニッケルのマンガンコバルト酸化物(NMC)およびリチウム鉄の隣酸塩(LFP)のような陰極材料は電気車および消費者電子工学を渡って広く、市場の優位性をセメントで囲んでいます。 コスト最適化と生産方法の改善により、大型バッテリー製造における採用も加速しました。

アノードセグメントは、2026年から2033年までの最速成長を目撃し、シリコン系およびグラファイトシリコンハイブリッドアノードへの研究を増加させ、バッテリー容量と充電サイクルを向上させます。 たとえば、BTR新エネルギー材料などの企業は、次世代の陽極技術に投資し、高性能リチウムイオン電池の需要が高まっています。 ポータブルエレクトロニクスの輸送と拡大の高度陽極ソリューションの必要性を促進し、予測期間の堅牢な成長のためにこのセグメントを配置します。

- 電池のタイプによって

電池のタイプに基づいて、市場はリチウム イオン、鉛酸、ニッケルの金属の水化物(NiMH)、ニッケル カドミウム(Ni-Cd)に、等分けられます。 リチウムイオンセグメントは、2025年に55.5%の最大の収益シェアで市場を支配し、高エネルギー密度、長いサイクル寿命、および消費者エレクトロニクス、電気自動車、およびエネルギー貯蔵アプリケーション全体の汎用性によって駆動しました。 主要な電池メーカーによる研究・生産における強力な投資によるセグメントメリットにより、継続的な性能改善とコスト削減を実現します。 リチウムイオン電池は軽量設計および急速な充満機能による携帯用装置そして自動車セクターで好まれます。 安全性の向上と進化するバッテリー管理システムにより、市場優位性を強化 再生可能エネルギー蓄電システムの採用拡大も、リチウムイオン技術の普及にも貢献しています。

鉛酸セグメントは、自動車スターター電池および固定エネルギー貯蔵の継続的な需要によって駆動され、2026年から2033年までの最速成長を目撃する見込みです。 たとえば、Exide Technologies は、産業用およびバックアップ電源アプリケーション向けの鉛酸ソリューションを革新し続けています。 セグメントの低生産コスト、リサイクル性、および確立されたサプライチェーンは、特にコスト効率が重要である新興経済において、その成長の可能性に貢献します。

- 用途別

適用に基づいて、電池材料の市場は携帯用装置、自動車、電子工学項目、力の貯蔵および他に分けられます。 自動車部門はEV導入を支える電気自動車の生産および政府のインセンティブの急速な拡大によって運転される2025の最大の収益のシェアと市場を支配しました。 自動車電池は、より長い運転範囲、より速い充満および高められた安全を達成する高性能材料を要求し、陰極、および電解質の技術の実質的な投資を運転します。 Tesla や BYD などの大手 EV メーカーは、高度な電池化学品やサプライチェーンに投資し、高品質の材料を保護し、自動車部門の優位性を強化しています。 欧州・北米・アジア太平洋地域における車両の高度化に重点を置き、市場成長を加速

ポータブルデバイスセグメントは、スマートフォン、タブレット、ノートパソコン、ウェアラブルエレクトロニクスの需要が高まっている2026年から2033年までの最速成長を目撃する見込みです。 例えば、Samsung SDI は、コンシューマーエレクトロニクスの小型、大容量のリチウムイオン電池のバッテリー材料ソリューションを引き続き拡大しています。 ポータブルアプリケーションで軽量で効率的で長持ちするバッテリーの必要性は、このセグメントの強力な成長をサポートする高度な陰極および陽極材料の迅速な採用を促進します。

電池材料 市場 地域分析

- アジア・パシフィックは、2025年に最大の収益シェアを誇るバッテリー材料市場を占め、電気自動車の急速な採用、消費者向け電子機器の生産拡大、電池材料製造ハブの強力な存在を率いています。

- リチウムイオンおよび高度電池材料の生産の上昇の上昇の投資および良質の電池の部品の成長の輸出は市場拡大を加速します

- EVおよびエネルギー貯蔵プロジェクトのための熟練した労働、有利な政府のインセンティブの可用性、および開発途上国の急速な産業化は自動車、電子工学およびエネルギー貯蔵セクターを渡る電池材料の高められた消費に寄与します

中国電池材料市場洞察

中国は、リチウムイオン電池の生産およびEVの採用のグローバルリーダーとして位置を借りて、2025年にアジア太平洋電池材料市場で最大のシェアを開催しました。 国の強固な産業基盤、電池の原料のための広範な供給の鎖およびきれいなエネルギーおよびEVの製造を支える政府の方針は主要な成長の運転者です。 また、国内および国際市場の両方において、カソード、アノード、および電解物の生産設備の継続的な投資によって強化される。

インドの電池材料市場洞察

インドは、EV導入を急速に拡大し、電子機器製造を増加させ、電池材料インフラへの投資を増加させることで、アジア太平洋地域で最速の成長を目撃しています。 国内電池の生産のための国家電気モビリティミッションやインセンティブなどの政府の取り組みは、高品質のバッテリー材料の需要を強化しています。 また、高度な電池化学品で研究開発を成長させ、リチウムイオンコンポーネントの輸出可能性を増加させることで、堅牢な市場拡大に貢献しています。

ヨーロッパ電池材料市場の洞察

欧州のバッテリー材料市場は、厳格な規制枠組み、高性能EVバッテリーの需要増加、持続可能なエネルギー貯蔵ソリューションへの投資の増加により、着実に拡大しています。 特に自動車および産業エネルギー貯蔵の適用のための環境の承諾、高度電池の設計および良質材料の調達を、強調します。 電池のリサイクルを含む循環経済慣行に重点を置き、市場成長をさらに高めます。

ドイツ電池材料市場インサイト

ドイツの電池材料市場はEVの製造、強い化学および材料の企業の伝統および輸出指向の生産モデルのリーダーシップによって運転されます。 国は、カソード、アノード、および電解技術における継続的な革新を促進し、学術機関とバッテリー材料メーカーとの間で、R&Dネットワークとコラボレーションを十分に確立しています。 高容量のリチウム イオン電池および新興の固体電池の塗布の使用のために要求は特に強いです。

U.K.電池材料市場情報

U.K.市場は、成熟した自動車およびクリーンエネルギー部門によって支持され、EVバッテリーサプライチェーンのポストブレキジットをローカライズし、高性能バッテリー材料の需要が高まっています。 次世代電池材料の研究開発、産業学連携、および投資に重点を置き、米国はヨーロッパ電池材料の風景で重要な役割を果たし続けています。

北米電池材料市場インサイト

北米は2026年から2033年にかけて最も速いCAGRで成長し、EV導入の増加、再生可能エネルギー貯蔵システムの拡大、リチウムイオンおよび先進電池の化学品の堅牢な要求により推進されています。 自動車OEMと電池材料メーカーの技術と革新、クリーンエネルギーのための政府のインセンティブに重点を置いています。 また、材料調達におけるバッテリー生産と戦略的投資の回収は、市場拡大を支援しています。

U.S.電池材料市場情報

米国は、2025年に北米市場で最大のシェアを占め、その広範なEV市場、強力な研究開発インフラ、および電池材料生産における重要な投資によって支持されています。 持続可能性、規制遵守、イノベーションを重視した国は、自動車およびエネルギー貯蔵用途における高品質のカソード、アノード、および電解質材料の採用を奨励しています。 主要なバッテリーメーカーと成熟した流通ネットワークのプレゼンスは、米国で有数の地位をさらに固着させます。

電池材料 市場シェア

電池材料の企業は主に下記のものを含んでいます:

- ウミコアコバルト&スペシャリティマテリアル(CSM)(ベルギー)

- NEI株式会社(米国)

- 上海山山技術有限公司(中国)

- ニンポーRonbayの新しいエネルギー技術Co.、株式会社(中国)

- 旭化成株式会社(日本)

- 日立エナジー株式会社(スイス)

- CNGRの高度材料Co.、株式会社(中国)

- 浙江Huayou Cobalt Co.、株式会社(中国)

- 株式会社ニチア(日本)

- GotionのハイテクなCo.、株式会社(中国)

- 三菱ケミカル株式会社(日本)

- 株式会社クレハ(日本)

- BASF SE(ドイツ)

- 東京化学工業株式会社(日本)

- POSCO Future M Co., Ltd.(韓国)

- 東レ工業株式会社(日本)

グローバル電池材料市場の最新動向

- 2025年11月、LG ChemとSinopecは、ナトリウムイオン電池のキーカソードと陽極材料を進化させるために戦略的共同開発契約を締結しました。 このコラボレーションは、リチウムイオンの代替としてナトリウムイオン技術の商品化を加速し、電池材料の景観を多様化することができます。 効率的で高性能なナトリウムイオン材料の開発により、生産能力を拡大し、リチウムの信頼性を削減し、エネルギー貯蔵および電気自動車のアプリケーションの新しい機会を創出し、産業における材料需要のダイナミクスを潜在的に再構築することが期待されます。

- 2025年11月、ノボ・モンド・グラナイト株式会社(NMG)は、パナソニック・エナジー社と多年にわたる商用契約を整備し、積極的な陽極材料生産を進めています。 同社は、フェーズ2の運用と将来のボリュームのための安全な結合の取消契約の下で、専用の初期生産能力を計画しています。 この開発は、重要な陽極材料のサプライチェーンの確実性を強化し、生産のスケーリングをサポートし、成長するEVおよびエネルギー貯蔵の需要に対応し、高品質で一貫性のある材料を可能にし、最終的に世界中のバッテリーメーカーの競争力を強化

- 2024年12月、中国の現代Amperex Technology Co. Limited(CATL)は、電池材料および機器サプライヤーに技術革新を推進し、サプライチェーンを強化するための金融サポートを開始しました。 このイニシアチブは激しいEV価格競争の中で圧力を軽減し、途切れない材料供給を保証するように設計されています。 CATLは、上流サプライヤーをサポートすることにより、先進的なカソード、アノード、および電解質材料の迅速な開発を奨励し、生産効率を改善し、コストを削減し、グローバルなバッテリー材料における市場リーダーを強化しています。

- 2024年6月、旭化成は独自の高イオン導電性電解液を用いたリチウムイオン電池の概念実証を行いました。 新しい技術は、低温でバッテリーの耐久性と出力を向上し、小型で低コストのバッテリーパックを実現します。 この進歩は自動車、携帯用装置およびエネルギー貯蔵の塗布のより広い採用を支える現在のLIBの主性能そしてエネルギー密度の挑戦に直接対処し、市場のより能率的で、競争電池材料を提供するために会社を置くために

- 2024年4月、ドイツ・シュワルジデイドの電池リサイクル用試作金属精製事業を開始 エンド・オブ・ライフのリチウム・イオン電池および生産のスクラップのための革新的なリサイクルの技術を最大限に活用することに焦点を合わせます。 リチウム、ニッケル、コバルトなどの貴金属を回収・再処理することにより、BASFのイニシアチブは材料の円滑性に貢献し、バージン原料の依存性を削減し、持続可能な電池生産をサポートし、EVやエネルギー貯蔵における成長した需要を満たすことが不可欠です。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。