世界の血液採取装置市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

6.90 Billion

USD

11.13 Billion

2024

2032

USD

6.90 Billion

USD

11.13 Billion

2024

2032

| 2025 –2032 | |

| USD 6.90 Billion | |

| USD 11.13 Billion | |

| % | |

|

世界の血液採取装置市場のセグメンテーション、製品別(採血管、システムタイプ、針と注射器、血液バッグ、採血システム/モニター、ランセット)、方法別(手動採血、自動採血)、用途別(診断、治療)、エンドユーザー別(病院、血液銀行センター、学術機関、在宅ケア) - 2032年までの業界動向と予測

採血機器市場規模

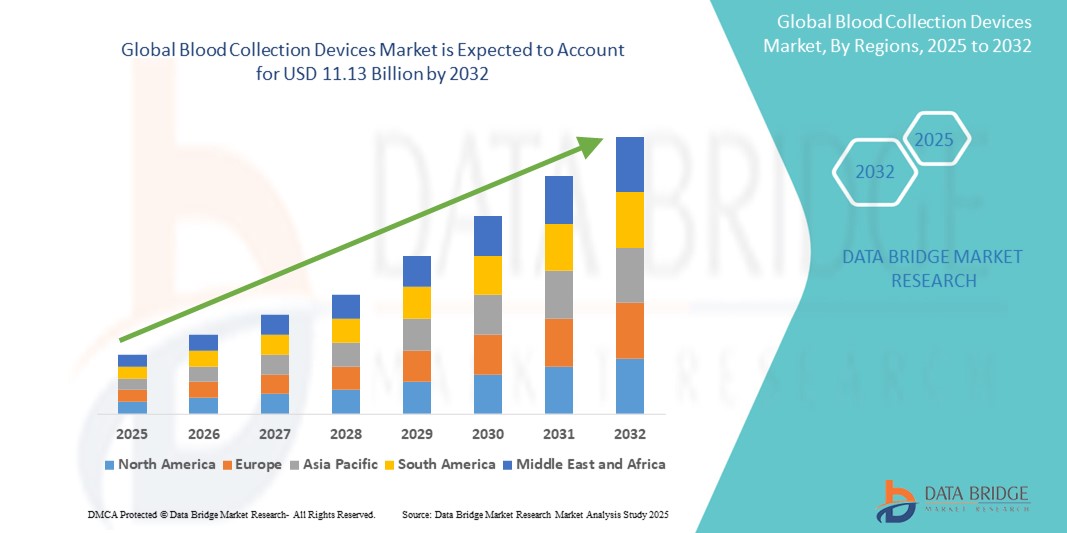

- 世界の血液採取装置市場規模は2024年に69億米ドルと評価され、予測期間中に 6.16%のCAGRで成長し、2032年には111億3000万米ドル に達すると予想されています。

- 血液採取装置市場の成長は、慢性疾患や感染症の蔓延の増加と医療技術の進歩によって主に推進されており、診断検査や治療手順の需要の増加につながっています。

- さらに、医療費の増加と、早期診断と定期的な健康モニタリングの重要性に対する消費者の意識の高まりにより、採血機器は現代の医療システムに不可欠な要素として確立されつつあります。これらの要因が重なり、採血機器ソリューションの普及が加速し、業界の成長を大きく後押ししています。

採血機器市場分析

- 血液サンプルの採取と処理のためのさまざまな器具と消耗品を含む採血装置は、安全性、効率性、および疾病管理と患者ケアにおける重要な役割の向上により、診断と治療の両方の環境における現代の医療システムのますます重要な構成要素となっています。

- 血液採取装置の需要の高まりは、慢性疾患や感染症の世界的な蔓延、病気の早期発見に対する意識の高まり、そしてより効率的で患者に優しい採取方法につながる継続的な技術進歩によって主に促進されています。

- 北米は、高度な医療インフラ、多額の研究開発投資、主要な業界プレーヤーの強力な存在を特徴とし、2024年には40.7%という最大の収益シェアで血液採取装置市場を支配しています。

- アジア太平洋地域は、都市化の進展、可処分所得の増加、感染症の蔓延率の上昇、中国、インド、日本などの国々における高度な血液採取技術の需要の高まりにより、予測期間中に血液採取装置市場で最も急速に成長する地域になると予想されており、2025年から2032年にかけて8.6%のCAGRが予測されています。

- 採血管セグメントは、慢性疾患の増加と日常的な診断の必要性に牽引され、2024年には33.8%のシェアを獲得し、採血機器市場を牽引するセグメントとなっています。採血管技術の革新と規制ガイドラインの遵守も、その優位性を支えています。

レポートの範囲と採血装置市場のセグメンテーション

|

属性 |

採血機器の主要市場分析 |

|

対象セグメント |

|

|

対象国 |

北米

ヨーロッパ

アジア太平洋

中東およびアフリカ

南アメリカ

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

データブリッジマーケットリサーチがまとめた市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、専門家による詳細な分析、価格設定分析、ブランドシェア分析、消費者調査、人口統計分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選択基準、PESTLE分析、ポーター分析、規制の枠組みも含まれています。 |

採血機器市場動向

「高度な自動化システムとスマートデータ分析との統合の深化」

- 世界の採血機器市場における重要な加速トレンドとして、高度な自動化システムとスマートデータ分析との統合が深化しています。こうした技術の融合により、採血手順における効率性、精度、そして患者体験が大幅に向上しています。

- For instance, automated phlebotomy devices are being developed that utilize advanced imaging to identify optimal venipuncture sites, allowing for more accurate and consistent blood draws. Similarly, smart blood collection tubes are integrating features that enable automatic sample labeling and tracking, streamlining the pre-analytical phase of laboratory testing

- The integration of advanced analytics in blood collection devices enables features such as learning optimal venipuncture parameters based on patient demographics and vein characteristics, predicting potential complications, and providing intelligent alerts for deviations in sample quality. For instance, some advanced systems utilize algorithms to improve vein visualization accuracy over time and can send intelligent alerts if a collection error is detected. Furthermore, automation capabilities offer healthcare professionals the ease of hands-free operation for repetitive tasks, allowing them to focus more on patient interaction and critical decision-making

- The seamless integration of blood collection devices with laboratory information systems (LIS) and electronic health records (EHR) facilitates centralized control over various aspects of the diagnostic workflow. Through a single interface, users can manage patient orders, track samples, and access results, creating a unified and automated diagnostic experience

- This trend towards more intelligent, intuitive, and interconnected blood collection systems is fundamentally reshaping user expectations for efficiency and patient comfort in diagnostics. Consequently, companies are developing automated blood collection devices with features such as robotic venipuncture for consistent draws and automated sample processing to reduce manual handling

Blood Collection Devices Market Dynamics

Driver

“Growing Need Due to Rising Disease Prevalence and Diagnostic Demands”

- The increasing global prevalence of various chronic and infectious diseases, coupled with a growing emphasis on early diagnosis and routine health check-ups, is a significant driver for the heightened demand for blood collection devices

- For instance, the rising incidence of diabetes, cardiovascular diseases, and various infectious diseases (such as, influenza, COVID-19, HIV/AIDS) necessitates frequent blood testing for diagnosis, monitoring, and treatment management. Such persistent health challenges are expected to drive the blood collection devices industry growth in the forecast period

- As healthcare providers become more aware of the importance of precise and timely diagnostic results, and seek enhanced patient safety during collection, modern blood collection devices offer advanced features such as safety-engineered needles, pre-barcoded tubes, and sterile collection systems, providing a compelling upgrade over traditional methods

- Furthermore, the growing popularity of point-of-care (PoC) diagnostics and the desire for streamlined laboratory workflows are making advanced blood collection devices an integral component of these systems, offering seamless integration with automated analyzers and laboratory information systems

- The convenience of less invasive collection methods (such as capillary blood collection), reduced risk of needlestick injuries, and the ability to ensure sample integrity are key factors propelling the adoption of blood collection devices in hospitals, clinics, and even home care settings. The trend towards decentralized testing and the increasing availability of user-friendly blood collection options further contributes to market growth

Restraint/Challenge

“Concerns Regarding Sample Integrity and High Initial Costs”

- Concerns surrounding the potential for sample integrity issues (for instance, hemolysis, clotting, contamination) during blood collection pose a significant challenge to broader market penetration of certain advanced devices. As blood collection relies on precise techniques and sterile conditions, improper collection or handling can lead to inaccurate test results, raising anxieties among healthcare professionals about diagnostic reliability

- For instance, reports of compromised samples due to incorrect collection tube usage or improper storage conditions can make some healthcare facilities hesitant to adopt new or more complex blood collection methodologies without extensive training

- Addressing these concerns through robust quality control, standardized training protocols, and clear device instructions is crucial for building user trust. Companies often emphasize their devices' design for ease-of-use and features that minimize sample degradation. In addition, the relatively high initial cost of some advanced automated blood collection systems and specialized devices compared to traditional manual methods can be a barrier to adoption for budget-sensitive healthcare facilities, particularly in developing regions or smaller clinics. While basic blood collection consumables remain affordable, premium features such as integrated vein visualization, robotic systems, or advanced safety mechanisms often come with a higher price tag

- While prices for some components are gradually decreasing, the perceived premium for sophisticated automation and safety technology can still hinder widespread adoption, especially for those who do not see an immediate return on investment for the advanced features offered

- Overcoming these challenges through enhanced training programs, clear demonstration of cost-effectiveness and patient safety benefits, and the development of more affordable, high-quality blood collection options will be vital for sustained market growth

Blood Collection Devices Market Scope

The market for blood collection devices is segmented into four notable segments based on product, method, application, and end-user.

- By Product

On the basis of product, the global blood collection devices market is segmented into blood collection tubes, needles and syringes, blood bags, blood collection systems/monitors and lancets. The blood collection tubes segment dominates the largest market revenue share of 33.8% in 2024, driven by the increasing prevalence of chronic diseases requiring routine diagnostics and continuous advancements in tube technology. These tubes are essential for various tests, and innovations in additives and designs enhance sample stability and laboratory efficiency.

The lancets segment is anticipated to witness the fastest growth rate of 7.9% from 2025 to 2032, fueled by the rising incidence of chronic diseases such as diabetes, which drives demand for frequent capillary blood sampling for monitoring. This growth is also supported by the increasing popularity of at-home testing and minimally invasive collection methods.

- By Method

On the basis of method, the global blood collection devices market is segmented into manual blood collection and automated blood collection. The manual blood collection segment held the largest market revenue share of 67.1% in 2024, driven by its cost-effectiveness, widespread applicability across various healthcare settings, and patient comfort. This method remains widely used in hospitals, clinics, and diagnostic laboratories, supported by ongoing advancements in needle technology and simplified collection procedures.

The automated blood collection segment is expected to witness the fastest CAGR of 7.7% from 2025 to 2032, driven by the increasing demand for safer, more efficient, and standardized collection procedures. Automation reduces human error, enhances sample quality, and improves workflow efficiency, making it increasingly attractive for high-volume settings.

- By Application

On the basis of application, the Global blood collection devices market is segmented into diagnostics and therapeutics. The diagnostics segment leads the market with 65.6% market share in 2024, driven by the continuously rising demand for blood tests to diagnose a wide array of chronic diseases such as cancer, diabetes, and cardiovascular conditions. Blood samples are crucial for confirming diagnoses, monitoring disease progression, and guiding treatment decisions across various medical specialties.

The therapeutics segment is expected to record the fastest CAGR of approximately 7.2% from 2025 to 2032, fueled by the rising demand for blood monitoring in therapeutic procedures, such as transfusions, apheresis, and innovations in personalized medicine requiring specific blood component collection.

- By End-User

On the basis of end-user, the global blood collection devices market is segmented into hospitals, blood bank centers, academics, and home care. The hospital segment accounted for the largest market revenue share of 34.2% in 2024, driven by the high volume of diagnostic tests performed daily, increased blood transfusion needs related to surgeries and chronic conditions, and the comprehensive range of medical services offered. Hospitals serve as primary points of care for a large patient influx requiring blood collection.

The blood bank center segment is expected to register the fastest CAGR of 7.5% during the forecast period, fueled by advancements in blood sampling technologies and the rising number of specialized diagnostic tests conducted in these dedicated facilities.

Blood Collection Devices Market Regional Analysis

- North America dominates the blood collection devices market with the largest revenue share of 40.7% in 2024, driven by its highly advanced healthcare infrastructure and significant investments in research and development

- Healthcare providers in the region highly value the enhanced patient safety features, improved accuracy, and streamlined workflows offered by modern blood collection devices, which seamlessly integrate with electronic health records and laboratory information systems

- This widespread adoption is further supported by high healthcare expenditure, a strong focus on preventive diagnostics and early disease detection, and the prominent presence of key industry players actively engaged in developing innovative blood collection technologies. This positions blood collection devices as an essential component for efficient and safe patient care across North America

U.S. Blood Collection Devices Market Insight

The U.S. blood collection devices market captured the largest revenue share of 72.6% in 2024 within North America, fueled by the swift adoption of advanced diagnostic technologies and the expanding healthcare infrastructure. Healthcare providers are increasingly prioritizing patient safety and efficiency through integrated, high-quality blood collection systems. The growing preference for advanced pre-analytical solutions, combined with robust demand for automated systems and integrated data management, further propels the blood collection devices industry. Moreover, the increasing integration of healthcare IT systems and a strong focus on clinical outcomes are significantly contributing to the market's expansion.

Europe Blood Collection Devices Market Insight

The Europe blood collection devices market is projected to expand at a substantial CAGR from 2025 to 2032, primarily driven by the rising prevalence of chronic and infectious diseases and the escalating need for enhanced diagnostic capabilities in hospitals and laboratories. The increase in aging populations, coupled with the demand for safer and more efficient blood collection methods, is fostering the adoption of advanced devices. European healthcare systems are also drawn to the precision and reliability these devices offer. The region is experiencing significant growth across hospital, diagnostic center, and blood bank applications, with advanced blood collection devices being incorporated into both new facility designs and existing laboratory upgrades.

U.K. Blood Collection Devices Market Insight

The U.K. blood collection devices market is anticipated to grow at a noteworthy CAGR from 2025 to 2032, driven by the escalating demand for advanced diagnostics and a desire for heightened patient comfort and safety during blood draws. In addition, concerns regarding healthcare efficiency and reduced risk of needlestick injuries are encouraging both healthcare providers and patients to choose modern blood collection solutions. The U.K.'s embrace of advanced medical technologies, alongside its robust healthcare infrastructure, is expected to continue to stimulate market growth.

Germany Blood Collection Devices Market Insight

The Germany blood collection devices market is expected to expand at a considerable CAGR from 2025 to 2032, fueled by increasing awareness of diagnostic accuracy and the demand for technologically advanced, high-quality solutions. Germany’s well-developed healthcare infrastructure, combined with its emphasis on innovation and stringent quality standards, promotes the adoption of advanced blood collection devices, particularly in hospitals and clinical laboratories. The integration of blood collection solutions with laboratory automation systems is also becoming increasingly prevalent, with a strong preference for secure, patient-focused solutions aligning with local healthcare expectations.

Asia-Pacific Blood Collection Devices Market Insight

The Asia-Pacific blood collection devices market is poised to grow at the fastest CAGR of 8.6% during the forecast period of 2025 to 2032, driven by increasing urbanization, rising disposable incomes, and significant technological advancements in countries such as China, Japan, and India. The region's growing healthcare expenditure, supported by government initiatives promoting access to diagnostics, is driving the adoption of advanced blood collection devices. Furthermore, as APAC emerges as a manufacturing hub for medical components and systems, the affordability and accessibility of blood collection devices are expanding to a wider healthcare consumer base.

China Blood Collection Devices Market Insight

中国の採血機器市場は、2024年にアジア太平洋地域において大きな収益シェアを占めました。これは、同国の中流階級の拡大、急速な都市化、そして医療技術の導入率の高さに起因しています。中国は医療機器の最大市場の一つであり、採血機器は病院、診断センター、そして血液バンクにおいてますます不可欠なものになりつつあります。医療インフラの近代化への取り組み、ますます洗練された採血オプションの提供、そして強力な国内メーカーの存在が、中国市場の成長を牽引する主要な要因となっています。

インドの血液採取機器市場の洞察

インドの採血機器市場は、医療インフラの急速な改善、早期疾患診断への意識の高まり、そして膨大な患者層を背景に、2025年から2032年にかけて8.15%という最高の年平均成長率(CAGR)を達成すると予想されています。感染症や慢性疾患の罹患率の増加に伴い、血液検査の需要は増加しています。医療へのアクセスと費用対効果の向上を目指す政府の取り組みと、診断ラボや病院への民間投資の増加は、インド全土における採血機器の普及を大きく促進しています。

採血装置の市場シェア

血液採取装置業界は、主に、次のような老舗企業によって牽引されています。

- アボット(米国)

- メドトロニック(アイルランド)

- BD(米国)

- テルモ株式会社(日本)

- ニプロ(日本)

- QIAGEN(ドイツ)

- メディカルSrl(イタリア)

- テルモBCT社(米国)

- フレゼニウス・カビAG(ドイツ)

- グリフォルスSA(スペイン)

- 江蘇省マイクセーフ医療技術有限公司(中国)

- SARSTEDT AG & Co. KG (ドイツ)

- リトラクタブル・テクノロジーズ社(米国)

- FL MEDICAL srl Unipersonale (イタリア)

- ABメディカルアカデミー(オランダ)

世界の血液採取装置市場の最新動向

- 2024年4月、Streckは、室温での保存中に血漿タンパク質濃度を安定化させるよう設計された、新しい直接採血用全血採血管「Protein Plus BCT」を発売しました。この発売により、同社の製品ポートフォリオが拡大し、市場における競争力が強化されます。

- 2024年4月、ベクトン・ディッキンソン・アンド・カンパニー(BD )は、インドでBDバキュテイナー・ウルトラタッチ・プッシュボタン採血セットを発売しました。この革新的な製品は、より細い採血針の使用を可能にするBD RightGaugeテクノロジーと、患者の刺入痛を大幅に軽減するBD PentaPointテクノロジーを採用しています。

- 2025年1月、フレゼニウス・カビは、血漿採取効率を最適化することを目的としたオーロラXi血漿交換システムの代替アルゴリズムであるアダプティブノモグラムに対してFDAが510(k)承認を付与したと発表した。

- 2025年3月、BD (ベクトン・ディッキンソン・アンド・カンパニー)とバブソン・ダイアグノスティクスは、 BDミニドロー毛細管血液採取システムで採取した数滴の血液を使用する一般的な血液検査が、静脈からの大量採取と同等の精度を示し、患者の検査へのアクセスを改善する可能性があることを示す新たな研究結果を発表しました。

- 2024年10月、テルモ血液細胞テクノロジーズは、ブラッドセンターズ・オブ・アメリカと共同で、Reveos自動血液処理システムの米国市場導入を開始しました。10年以上にわたり世界中で使用されているReveosは、効率性と血小板供給の強化を目指しています。

- 2023年11月、BDはPIVO Proニードルフリー採血デバイスを発表しました。このデバイスは、従来の針を使用せずに患者の末梢静脈ラインから直接血液サンプルを採取することを可能にします。このデバイスは、BDの既存のPIVOテクノロジーを基盤としています。

- 2023年1月、CapitainerはAstraZenecaと協力し、Capitainerの新しいデバイスを使用して、AstraZenecaの臨床薬物プログラムに関連するバイオマーカーのプロトコルを開発しました。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。