Global Combat Support Vehicle Market Size, Share and Trends Analysis Report

Market Size in USD Billion

CAGR :

%

USD

19.92 Billion

USD

30.21 Billion

2025

2033

USD

19.92 Billion

USD

30.21 Billion

2025

2033

| 2026 –2033 | |

| USD 19.92 Billion | |

| USD 30.21 Billion | |

| % | |

|

Global Combat Support Vehicle Market Segmentation, By Material (Metals, Ceramics, and Composites), Vehicle (Tanks, Armored Fighting Vehicles, and Civilian and Law Enforcement Vehicles), Application (Military and Non-Military) - Industry Trends and Forecast to 2033

What is the Global Combat Support Vehicle Market Size and Growth Rate?

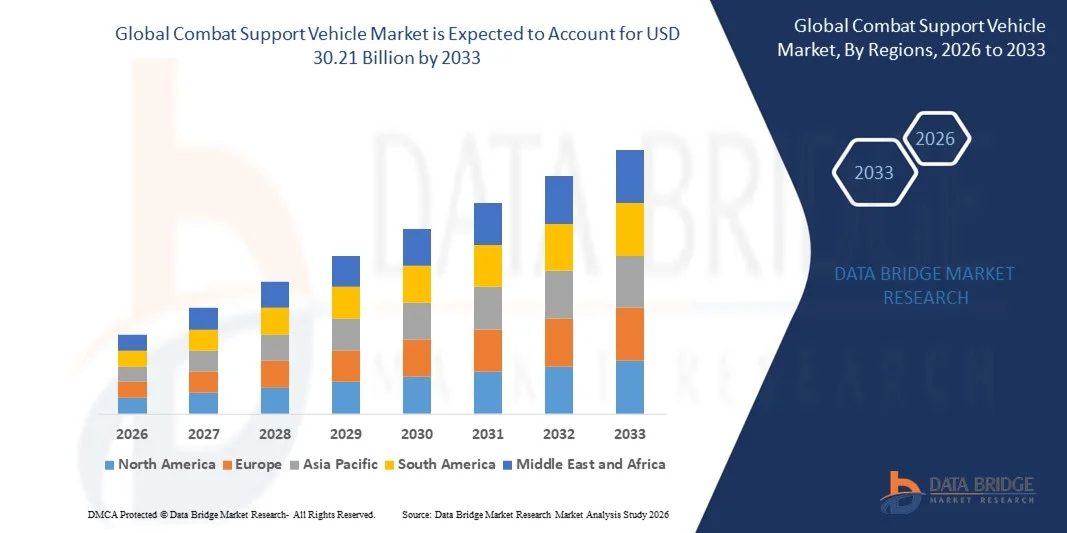

- The global combat support vehicle market size was valued at USD 19.92 billion in 2025 and is expected to reach USD 30.21 billion by 2033, at a CAGR of 5.34% during the forecast period

- Major factors that are expected to boost the growth of the combat support vehicle market in the forecast period are the rise in the demand for the combat support vehicle because of the increase in the instances of cross-border conflicts

- Furthermore, the increase in the prevalence of asymmetric warfare around the world is further propelling the growth of the combat support vehicle market

What are the Major Takeaways of Combat Support Vehicle Market?

- The shortage of major OEMs of combat support vehicles and the rise in the incidences of the mechanical, electrical and other types of failure in combat support vehicles is further responsible for the growth of the combat support vehicle market in the timeline period

- In addition, the military modernization plans around the world, the rise in the acceptance of combat support vehicles by the defence forces of several countries and the advancement of modular and scalable combat support vehicles which will further provide potential opportunities for the growth of the combat support vehicle market

- North America dominated the Combat Support Vehicle market with a 35.25% revenue share in 2025, driven by strong defense modernization programs, procurement of armored fleets, and continuous innovation in high-mobility support platforms across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 8.36% from 2026 to 2033, driven by growing defense modernization programs, cross-border security requirements, and rapid procurement of high-mobility, modular armored platforms across China, Japan, India, South Korea, and Southeast Asia

- The Metals segment dominated the market with a 48.6% share in 2025, as high-strength steel and aluminum alloys remain the primary materials for armored hulls, chassis structures, and load-bearing components

Report Scope and Combat Support Vehicle Market Segmentation

|

Attributes |

Combat Support Vehicle Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Combat Support Vehicle Market?

Integration of Modular, Network-Enabled, and Multi-Role Combat Support Vehicles

- The combat support vehicle market is witnessing a strong shift toward modular, mission-configurable platforms designed to perform logistics, engineering, recovery, medical evacuation, and command support operations within a single adaptable architecture

- Manufacturers are introducing network-enabled vehicles equipped with advanced communication systems, battlefield management software, situational awareness sensors, and remote weapon station compatibility

- Growing demand for high-mobility, armored, and lightweight platforms capable of operating in asymmetric warfare, cross-border conflicts, and peacekeeping missions is accelerating innovation

- For instance, companies such as Oshkosh Corporation, Rheinmetall AG, BAE Systems, and General Dynamics Corporation have introduced next-generation armored support vehicles with enhanced survivability, digital integration, and hybrid mobility options

- Increasing focus on multi-domain operations and rapid deployment forces is driving procurement of interoperable and strategically deployable combat support fleets

- As modern warfare becomes increasingly technology-driven and mobility-centric, Combat Support Vehicles will remain critical for ensuring operational sustainability, force protection, and real-time battlefield coordination

What are the Key Drivers of Combat Support Vehicle Market?

- Rising defense modernization programs across the U.S., Europe, and Asia-Pacific are increasing investments in armored logistics vehicles, bridge-laying systems, engineering support units, and recovery platforms

- For instance, during 2024–2025, defense procurement initiatives in the U.S., Germany, and the U.K. emphasized upgrading armored vehicle fleets with improved blast protection, digital communication suites, and enhanced mobility systems

- Growing geopolitical tensions, border security concerns, and NATO force readiness initiatives are accelerating demand for high-performance combat service support vehicles

- Advancements in lightweight composite armor, hybrid propulsion systems, autonomous navigation, and telematics-based fleet management are strengthening vehicle efficiency and survivability

- Rising emphasis on rapid humanitarian assistance, disaster relief operations, and UN peacekeeping missions is expanding the operational scope of combat support platforms

- Supported by sustained global defense budgets and strategic military transformation programs, the Combat Support Vehicle market is expected to witness steady long-term growth

Which Factor is Challenging the Growth of the Combat Support Vehicle Market?

- High acquisition and lifecycle maintenance costs associated with advanced armored platforms, integrated electronics, and hybrid mobility systems limit procurement volumes for developing economies

- For instance, during 2024–2025, fluctuations in raw material prices, supply chain disruptions, and electronic subsystem shortages increased production costs for several global armored vehicle manufacturers

- Stringent regulatory requirements, export restrictions, and complex defense procurement procedures delay contract approvals and international sales

- Integration challenges related to cybersecurity protection, interoperability with legacy military fleets, and battlefield communication systems increase development timelines

- Competition from refurbished legacy fleets and upgrade programs creates pricing pressure for new-generation vehicle manufacturers

- To address these challenges, companies are focusing on modular production, localized manufacturing partnerships, cost-optimized variants, and digital lifecycle support solutions to enhance global adoption of combat support vehicles

How is the Combat Support Vehicle Market Segmented?

The market is segmented on the basis of material, vehicle, and application.

- By Material

On the basis of material, the combat support vehicle market is segmented into Metals, Ceramics, and Composites. The Metals segment dominated the market with a 48.6% share in 2025, as high-strength steel and aluminum alloys remain the primary materials for armored hulls, chassis structures, and load-bearing components. Metals offer proven durability, blast resistance, cost efficiency, and ease of large-scale manufacturing. Their widespread availability and established supply chains further support dominance across both developed and emerging defense markets.

The Composites segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for lightweight armored platforms, improved fuel efficiency, and enhanced mobility. Advanced composite materials provide superior strength-to-weight ratios, corrosion resistance, and ballistic performance, making them ideal for next-generation modular combat support vehicles designed for rapid deployment and multi-role operations.

- By Vehicle

On the basis of vehicle type, the market is segmented into Tanks, Armored Fighting Vehicles (AFVs), and Civilian and Law Enforcement Vehicles. The Armored Fighting Vehicles segment dominated the market with a 44.2% share in 2025, supported by rising procurement of infantry fighting vehicles, armored personnel carriers, and recovery vehicles for logistics and battlefield support missions. AFVs provide a balance of mobility, protection, and mission adaptability, making them central to modern combat support operations.

The Civilian and Law Enforcement Vehicles segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for armored vehicles in border security, counter-terrorism, riot control, disaster response, and peacekeeping missions. Governments worldwide are strengthening internal security infrastructure, thereby accelerating procurement of specialized support vehicles beyond traditional military applications.

- By Application

On the basis of application, the combat support vehicle market is segmented into Military and Non-Military. The Military segment dominated the market with a 72.5% share in 2025, owing to sustained defense modernization programs, armored fleet upgrades, and increasing geopolitical tensions. Combat support vehicles play a critical role in logistics transport, engineering support, recovery operations, and battlefield medical evacuation within armed forces worldwide.

The Non-Military segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by rising utilization in disaster relief operations, humanitarian missions, infrastructure protection, and high-risk industrial environments. Expanding demand from paramilitary forces, homeland security agencies, and emergency response organizations is further contributing to the steady growth of non-military combat support platforms.

Which Region Holds the Largest Share of the Combat Support Vehicle Market?

- North America dominated the Combat Support Vehicle market with a 35.25% revenue share in 2025, driven by strong defense modernization programs, procurement of armored fleets, and continuous innovation in high-mobility support platforms across the U.S. and Canada. High adoption of modular, network-enabled, and multi-role vehicles enhances operational efficiency for military logistics, engineering support, and battlefield recovery operations

- Leading companies in North America, such as Oshkosh Corporation, General Dynamics Corporation, and Lockheed Martin Corporation, are introducing next-generation combat support vehicles with hybrid mobility, advanced communication suites, and modular mission payloads, strengthening the region’s technological leadership

- High concentration of engineering talent, robust defense R&D ecosystems, and sustained investment in digital integration and autonomous vehicle technologies further reinforce North America’s dominance in the Combat Support Vehicle market

U.S. Combat Support Vehicle Market Insight

The U.S. is the largest contributor in North America, supported by extensive armored fleet upgrades, high demand for rapid deployment platforms, and modernization of logistics and recovery vehicles. Continuous investment in autonomous vehicle technologies, battlefield management systems, and hybrid propulsion solutions drives demand for advanced Combat Support Vehicles capable of multi-role operations. Presence of major defense contractors, innovation hubs, and government procurement programs further accelerates market growth.

Canada Combat Support Vehicle Market Insight

Canada contributes significantly to regional growth due to investments in domestic defense programs, armored vehicle upgrades, and multi-role support platforms. Deployment of vehicles for disaster response, peacekeeping missions, and training exercises is increasing. Government-backed R&D initiatives, skilled engineering workforce, and collaboration with North American defense manufacturers support rising adoption of Combat Support Vehicles across both military and paramilitary operations.

Asia-Pacific Combat Support Vehicle Market

Asia-Pacific is projected to register the fastest CAGR of 8.36% from 2026 to 2033, driven by growing defense modernization programs, cross-border security requirements, and rapid procurement of high-mobility, modular armored platforms across China, Japan, India, South Korea, and Southeast Asia. Rising investments in hybrid mobility, autonomous support vehicles, and battlefield communication systems fuel adoption.

China Combat Support Vehicle Market Insight

China is the largest contributor in Asia-Pacific, supported by extensive domestic defense manufacturing, advanced electronics integration, and government-backed military modernization programs. Increasing demand for multi-role combat support platforms, rapid deployment logistics vehicles, and network-enabled systems is driving market growth. Competitive local production and strategic exports further expand market penetration.

Japan Combat Support Vehicle Market Insight

Japan demonstrates steady growth due to modernization of armored support fleets, integration of advanced electronics, and high-reliability engineering practices. Adoption of hybrid and network-enabled vehicles for disaster response, industrial logistics, and defense applications reinforces market expansion.

India Combat Support Vehicle Market Insight

India is emerging as a key growth hub with expanding domestic defense manufacturing, rising armored vehicle procurement, and government-backed initiatives supporting multi-role combat support platforms. Increasing demand for autonomous support vehicles, rapid deployment logistics, and mission-configurable platforms accelerates market adoption.

South Korea Combat Support Vehicle Market Insight

South Korea contributes significantly due to strong defense modernization programs, high adoption of network-enabled support vehicles, and advanced armored platforms. Rising demand for modular, lightweight, and multi-role vehicles drives adoption across both military and paramilitary sectors. Technological innovation and domestic manufacturing capabilities support sustained regional growth.

Which are the Top Companies in Combat Support Vehicle Market?

The combat support vehicle industry is primarily led by well-established companies, including:

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman (U.S.)

- General Dynamics Corporation (U.S.)

- BAE Systems (U.K.)

- Rheinmetall AG (Germany)

- Oshkosh Corporation (U.S.)

- UralVagonZavod (Russia)

- Ukroboronprom (Ukraine)

- Norinco Private Limited (China)

- Textron Inc. (U.S.)

- Autonomous Solutions Inc. (U.S.)

- Clearpath Robotics Inc. (Canada)

- ICOR Technology (Canada)

- Leonardo S.p.A. (Italy)

- Cobham Limited (U.K.)

- FLIR Systems, Inc. (U.S.)

- ECA Group (France)

- L3Harris Technologies, Inc. (U.S.)

- HORIBA Ltd. (Japan)

- Nexter Group (France)

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。