世界の家畜用医薬品市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

20.90 Billion

USD

34.85 Billion

2025

2033

USD

20.90 Billion

USD

34.85 Billion

2025

2033

| 2026 –2033 | |

| USD 20.90 Billion | |

| USD 34.85 Billion | |

| % | |

|

世界の家畜用医薬品市場のセグメンテーション:製品タイプ別(抗感染薬、殺寄生虫薬、抗炎症薬、麻酔薬、鎮痛薬、ホルモン剤および関連製品、その他)、動物タイプ別(家畜および馬)、投与経路別(経口、非経口、局所、その他)、流通チャネル別(動物病院、動物診療所、薬局およびドラッグストア、その他) - 業界動向と2033年までの予測

家畜用医薬品市場規模

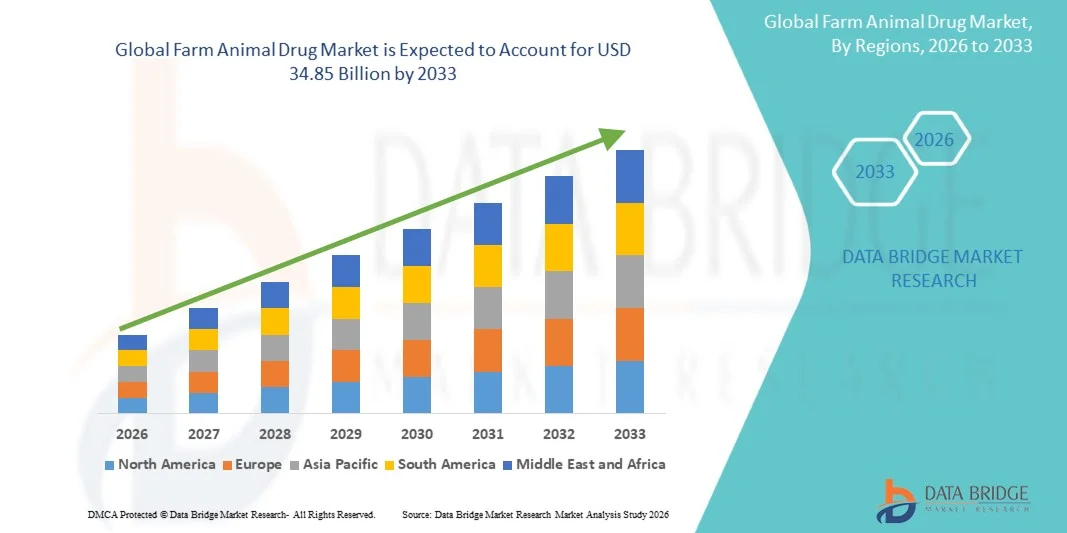

- 世界の家畜用医薬品市場規模は、2025年には209億米ドルと評価され、予測期間中の年平均成長率(CAGR)6.60%で、2033年には348億5000万米ドル に達すると予測されている 。

- 市場の成長は、畜産物に対する需要の増加、家畜に対する予防医療の普及拡大、および獣医用医薬品における技術進歩によって大きく牽引されている。

- さらに、動物の健康に対する意識の高まり、畜産生産性を支援する政府の取り組み、そして家畜の感染症対策の必要性などが、家畜用医薬品の需要を押し上げています。これらの要因が相まって、動物用医薬品の普及を加速させ、業界の成長を大きく促進しています。

家畜用医薬品市場分析

- 家畜用医薬品(抗感染薬、殺寄生虫薬、抗炎症薬、麻酔薬、鎮痛薬、ホルモン剤、その他関連製品を含む)は、家畜の健康維持、生産性向上、そして現代の畜産におけるバイオセキュリティ確保に不可欠である。

- 家畜用医薬品の需要増加は、主に家畜数の増加、予防医療の普及、そして農家における疾病管理と動物福祉への意識の高まりによって促進されている。

- 北米は、高度な獣医療インフラ、革新的な動物用医薬品ソリューションの高い普及率、家畜の健康を促進する強力な規制枠組みに支えられ、2025年には39.8%という最大の収益シェアで家畜用医薬品市場を席巻した。特に米国では、家禽や牛に対する抗感染症薬および殺寄生虫薬の需要が大幅に増加した。

- アジア太平洋地域は、食肉消費量の増加、畜産の拡大、動物衛生プログラムを支援する政府の取り組みの増加により、予測期間中に家畜用医薬品市場で最も急速に成長する地域になると予想されています。

- 抗感染症薬分野は、細菌感染症の予防と治療、および家畜の生産性全般を支える上で重要な役割を担っていることから、2025年には市場シェア42.9%を占め、家畜用医薬品市場を牽引した。

レポートの範囲と家畜用医薬品市場のセグメンテーション

|

属性 |

家畜用医薬品の主要市場インサイト |

|

対象分野 |

|

|

対象国 |

北米

ヨーロッパ

アジア太平洋

中東およびアフリカ

南アメリカ

|

|

主要市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

Data Bridge Market Researchが作成した市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要企業などの市場シナリオに関する洞察に加え、専門家による詳細な分析、患者疫学、パイプライン分析、価格分析、規制枠組みも含まれています。 |

家畜用医薬品市場の動向

「精密畜産とデジタル健康モニタリングの普及拡大」

- 世界の家畜用医薬品市場における重要かつ加速的なトレンドは、精密畜産ツールとデジタル健康モニタリングシステムの統合であり、これにより獣医用医薬品のより的確で効率的な投与が可能になる。

- 例えば、センサーを搭載したスマート首輪や耳標は、動物のバイタルサイン、活動レベル、病気の症状を監視し、獣医師が必要に応じてのみ抗感染症薬や駆虫薬を投与できるようにすることで、薬剤の過剰使用を減らすことができる。

- デジタルプラットフォームは、家畜の健康データを追跡し、ワクチン接種スケジュールを最適化し、疾病発生の予測アラートを提供するなど、動物福祉と生産性全般を向上させるためにますます活用されている。

- The combination of farm management software and veterinary drug administration creates a data-driven ecosystem that improves decision-making and reduces costs associated with indiscriminate drug use

- This trend towards tech-enabled, precision-based livestock healthcare is reshaping farmer expectations regarding animal health management, prompting companies such as Zoetis to develop connected drug delivery systems integrated with herd management platforms

- The demand for farm animal drugs that can be monitored, optimized, and administered through digital and precision tools is growing rapidly across livestock operations worldwide, as producers increasingly prioritize efficiency, health outcomes, and regulatory compliance

- Emerging AI-driven predictive analytics are helping forecast disease outbreaks and optimize drug usage schedules, further enhancing the efficiency and cost-effectiveness of farm animal healthcare

Farm Animal Drug Market Dynamics

Driver

“Increasing Demand Due to Growing Livestock Production and Animal Health Awareness”

- The rising global demand for meat, dairy, and other livestock products, coupled with growing awareness of preventive animal healthcare, is a key driver for the farm animal drug market

- For instance, in March 2025, Boehringer Ingelheim launched an expanded line of anti-infectives and parasiticides for poultry and swine, aimed at improving herd immunity and overall productivity, highlighting the role of preventive care

- Increasing incidence of infectious and parasitic diseases in livestock is encouraging farmers to adopt comprehensive drug regimens, including vaccines and parasiticides, to maintain herd health and reduce economic losses

- Government programs promoting animal health standards, veterinary support services, and regulatory guidelines for livestock medication are further boosting demand for farm animal drugs

- Enhanced focus on food safety, animal welfare, and sustainable livestock practices is driving adoption of modern veterinary pharmaceuticals, ensuring both consumer confidence and improved productivity

- The convenience of ready-to-use formulations, easy-to-administer oral or injectable drugs, and broader availability through veterinary networks are key factors propelling market growth in both developed and developing regions

- Growing partnerships between pharmaceutical companies and feed producers are driving integrated solutions for herd health management, expanding access to farm animal drug

- Rising consumer preference for ethically and sustainably produced animal products is encouraging the use of preventive veterinary drugs and natural alternatives, creating new growth opportunities

Restraint/Challenge

“Antimicrobial Resistance and Regulatory Compliance Hurdles”

- Concerns growing concern of antimicrobial resistance (AMR) due to overuse or misuse of antibiotics in livestock is a significant challenge to market growth

- For instance, reports of multidrug-resistant bacterial strains in poultry and cattle have made some producers cautious about excessive anti-infective use, limiting market expansion for conventional antibiotics

- Strict regulations on drug residues in animal products, withdrawal periods, and veterinary prescription requirements pose compliance challenges for manufacturers and farmers alike

- Addressing these challenges through alternative therapies, stricter prescription controls, and the development of residue-free or natural drug options is crucial for maintaining market trust and sustainability

- High costs associated with novel drug formulations, vaccines, or bioactive feed additives may also act as barriers to adoption, particularly for small-scale farmers in emerging markets

- Overcoming these hurdles through awareness programs, regulatory support, and innovation in safe and effective veterinary pharmaceuticals is vital for long-term market growth

- Limited access to veterinary services and trained personnel in rural regions may delay proper drug administration, affecting market penetration

- Resistance from farmers to adopt newer, more expensive drug formulations without demonstrable short-term ROI can hinder widespread adoption of advanced veterinary drugs

Farm Animal Drug Market Scope

The market is segmented on the basis of product type, animal type, route of administration, and distribution channel.

- By Product Type

On the basis of product type, the farm animal drug market is segmented into anti-infectives, parasiticides, anti-inflammatories, anesthetics, analgesics, hormones and related products, and others. The anti-infective segment dominated the market with the largest market revenue share of 42.9% in 2025, driven by the essential role of antibiotics and related drugs in preventing and treating bacterial infections in livestock and poultry. Farmers prioritize anti-infectives due to their proven effectiveness in reducing mortality and improving productivity across large herds. Anti-infectives are widely used across multiple animal species, making them a cornerstone of veterinary care. Regulatory support for disease prevention and improved farm biosecurity also fuels the adoption of anti-infectives. Established pharmaceutical companies continue to innovate with broad-spectrum formulations to meet farmer needs efficiently. The market sees sustained demand due to ongoing disease outbreaks and the importance of maintaining herd health.

The parasiticides segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising awareness of parasite control and preventive health practices in livestock and equine populations. Parasiticides address a broad spectrum of internal and external parasites that can significantly impact animal productivity and welfare. The increasing global livestock population and expansion of intensive farming systems are driving higher usage. Improved formulations offering easier administration and longer efficacy periods are enhancing adoption. Veterinary campaigns and farmer education programs further support market growth. In addition, parasitic infections directly impact food safety and economic outcomes, making parasiticides a rapidly growing focus in the farm animal drug sector.

- By Animal Type

On the basis of animal type, the farm animal drug market is segmented into livestock animals and equine. The livestock animals segment dominated the market with the largest revenue share in 2025, owing to the sheer volume of cattle, poultry, swine, and small ruminants requiring regular drug interventions for disease prevention and growth optimization. Livestock farmers invest heavily in preventive drugs, including vaccines, anti-infectives, and parasiticides, to reduce economic losses due to disease outbreaks. Government programs supporting livestock health and food safety standards further boost demand in this segment. The segment benefits from extensive veterinary support, availability of specialized products, and ongoing research into livestock disease management. Established veterinary pharmaceutical companies focus primarily on livestock due to the high-volume and recurring demand. Anti-infectives and anti-parasitic drugs remain the most widely used product types in this segment.

The equine segment is expected to witness the fastest growth during the forecast period, driven by increasing investments in horse breeding, racing, and recreational equestrian activities. Equine health management requires specialized drugs such as anti-inflammatories, analgesics, and vaccines, creating a niche but high-value market. Rising awareness of animal welfare and equine performance optimization fuels adoption. Advanced veterinary practices and specialized equine clinics contribute to the growth of this segment. Moreover, the growth in equestrian sports and recreational horse ownership in emerging markets is accelerating the demand for high-quality veterinary drugs.

- By Route of Administration

On the basis of route of administration, the farm animal drug market is segmented into oral, parenteral, topical, and others. The oral segment dominated the market with the largest revenue share in 2025, due to its ease of administration in large herds, suitability for preventive treatments, and compatibility with feed or water delivery systems. Oral drugs, including anti-infectives and parasiticides, enable mass medication efficiently and reduce stress on animals compared to injections. Farmers prefer oral administration for routine disease prevention and growth management. Technological improvements in palatability and stability further support adoption. The segment also benefits from established supply chains and formulations that allow consistent dosing. Regulatory approvals for oral drug use in livestock enhance farmer confidence and adoption rates.

The parenteral segment is expected to witness the fastest growth from 2026 to 2033, fueled by the demand for vaccines, biologics, and targeted therapeutic interventions that require injections. Parenteral administration ensures precise dosing and rapid bioavailability, critical for treating infections and acute conditions. Veterinary professionals prefer this route for high-value animals and during disease outbreaks. Innovations in needle-free injection devices and combination vaccines are further boosting adoption. Parenteral formulations are increasingly integrated into preventive herd health programs. Rising veterinary awareness and government support for vaccination campaigns also contribute to segment growth.

- By Distribution Channel

On the basis of distribution channel, the farm animal drug market is segmented into veterinary hospitals, veterinary clinics, pharmacies and drug stores, and others. The veterinary hospitals segment dominated the market with the largest revenue share in 2025, due to the availability of specialized treatments, professional supervision, and high-value services for livestock and equine animals. Hospitals serve as centralized points for mass vaccination, treatment of complex diseases, and delivery of injectable or specialty drugs. The segment benefits from trust and established relationships with farmers and large-scale livestock operations. Hospital-based distribution ensures compliance with regulatory standards and proper drug administration. Moreover, veterinary hospitals often provide integrated herd health management services that drive repeat sales.

The pharmacies and drug stores segment is expected to witness the fastest growth during the forecast period, fueled by easier access for small-scale farmers and rural livestock owners seeking over-the-counter veterinary drugs. These outlets offer convenience, availability of essential products, and a wide range of preventive and therapeutic drugs. The growth of online veterinary pharmacies and e-commerce platforms further supports this segment. Education campaigns promoting safe use of veterinary drugs also contribute to adoption. Increasing rural livestock populations and limited access to veterinary professionals in remote areas are driving demand through pharmacies and drug stores.

Farm Animal Drug Market Regional Analysis

- North America dominated the farm animal drug market with the largest revenue share of 39.8% in 2025, supported by advanced veterinary infrastructure, high adoption of innovative animal health solutions, and strong regulatory frameworks promoting livestock health

- Farmers in the region prioritize the health and productivity of livestock through regular use of anti-infectives, parasiticides, and vaccines, supported by access to veterinary services and modern drug formulations

- This widespread adoption is further reinforced by government initiatives promoting animal welfare and food safety, high awareness among livestock producers, and a focus on reducing disease-related economic losses, establishing farm animal drugs as an essential component of livestock management in both large-scale and commercial farms

U.S. Farm Animal Drug Market Insight

The U.S. farm animal drug market captured the largest revenue share of 82% in 2025 within North America, fueled by the country’s well-established livestock industry and high adoption of preventive veterinary healthcare. Farmers are increasingly prioritizing herd health through the use of anti-infectives, parasiticides, and vaccines to reduce disease outbreaks and improve productivity. The growing focus on food safety, animal welfare, and regulatory compliance further propels the market. Moreover, rising investments in livestock technology, veterinary infrastructure, and herd health management programs are significantly contributing to the market's expansion.

Europe Farm Animal Drug Market Insight

The Europe farm animal drug market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strict animal health regulations and the need to prevent livestock diseases. The increase in intensive livestock farming, coupled with growing awareness of preventive healthcare practices, is fostering the adoption of farm animal drugs. European farmers are also adopting modern veterinary solutions to ensure productivity and food safety. The region is witnessing significant growth across poultry, swine, and cattle sectors, with farm animal drugs being increasingly integrated into herd health management programs.

U.K. Farm Animal Drug Market Insight

The U.K. farm animal drug market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness of animal welfare and the increasing adoption of preventive veterinary care. Concerns regarding livestock disease outbreaks are encouraging farmers to use anti-infectives, parasiticides, and vaccines more rigorously. The UK’s strong regulatory framework and support for sustainable livestock practices, alongside growing veterinary services, are expected to continue stimulating market growth. Moreover, both commercial farms and small-scale livestock owners are increasingly adopting modern drug solutions for disease control and productivity enhancement.

Germany Farm Animal Drug Market Insight

The Germany farm animal drug market is expected to expand at a considerable CAGR during the forecast period, fueled by stringent regulations on animal health and growing awareness of sustainable livestock management. Germany’s advanced veterinary infrastructure and emphasis on innovation promote the adoption of farm animal drugs, particularly vaccines, anti-infectives, and anti-parasitics. The integration of herd management software with veterinary treatments is also becoming increasingly prevalent. Farmers are seeking solutions that ensure productivity, food safety, and compliance with EU regulations, which is driving demand for modern veterinary pharmaceuticals.

Asia-Pacific Farm Animal Drug Market Insight

The Asia-Pacific farm animal drug market is poised to grow at the fastest CAGR of 25% during the forecast period of 2026 to 2033, driven by increasing livestock production, rising demand for meat and dairy products, and technological advancements in countries such as China, India, and Japan. The region’s growing adoption of preventive animal healthcare, supported by government initiatives promoting livestock health and biosecurity, is driving market growth. Furthermore, as APAC emerges as a manufacturing hub for veterinary pharmaceuticals, affordability and accessibility of farm animal drugs are expanding to a wider farmer base.

Japan Farm Animal Drug Market Insight

The Japan farm animal drug market is gaining momentum due to the country’s focus on high-quality livestock production, advanced veterinary infrastructure, and adoption of preventive healthcare practices. The Japanese market places a significant emphasis on biosecurity and animal welfare, and the adoption of vaccines and anti-infectives is driven by large-scale poultry and swine operations. Integration of herd management systems with drug administration practices is fueling growth. Moreover, Japan’s aging farming population is likely to spur demand for more efficient, easy-to-administer, and safe veterinary drug solutions in both commercial and small-scale livestock farms.

India Farm Animal Drug Market Insight

The India farm animal drug market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding livestock population, rising meat and dairy demand, and rapid adoption of veterinary pharmaceuticals. India stands as one of the largest markets for preventive animal healthcare, and farm animal drugs are becoming increasingly popular among both commercial and smallholder farmers. Government initiatives promoting livestock health, the push towards organized dairy and poultry farms, and the availability of affordable drug options, alongside strong domestic manufacturing, are key factors propelling the market in India.

Farm Animal Drug Market Share

The Farm Animal Drug industry is primarily led by well-established companies, including:

- Zoetis Services LLC (U.S.)

- Elanco Animal Health (U.S.)

- Ceva Santé Animale (France)

- Vetoquinol (France)

- Merck Animal Health (U.S.)

- Boehringer Ingelheim (Germany)

- Virbac (France)

- Dechra Pharmaceuticals plc (U.K.)

- Phibro Animal Health Corporation (U.S.)

- Norbrook Laboratories Ltd. (U.K.)

- Neogen Corporation (U.S.)

- Huvepharma Inc (U.S.)

- Ouro Fino Saúde Animal Participações SA (Brazil)

- Laboratorios Hipra S.A. (Spain)

- Laboratorios Calier S.A. (Spain)

- Laboratorios Syva S.A. (Spain)

- Jurox Pty Ltd (Australia)

- Kyoritsu Seiyaku Corporation (Japan)

- SeQuent Scientific Limited (India)

- Zydus Animal Health and Investments Limited (India)

What are the Recent Developments in Farm Animal Drug Market?

- In January 2026, the European Medicines Agency (EMA) reported its key 2025 recommendations, noting that 30 veterinary medicines including 16 vaccines were recommended for marketing authorization, the highest number in consecutive years, indicating strong innovation momentum in veterinary pharmaceuticals

- In December 2025, EXZOLT™ CATTLE‑CA1 (fluralaner topical solution) received conditional FDA approval for prevention and treatment of New World screwworm larvae in cattle, offering a novel parasiticide option for livestock producers facing emergent pest threats

- In August 2025, the U.S. Department of Health and Human Services authorized Emergency Use Authorizations (EUAs) for animal drugs to counter screwworm infestations (despite no confirmed U.S. cases), allowing veterinarians to use approved or foreign drugs proactively to protect livestock health

- In July 2025, the Government of India banned 18 antibiotics, 18 antivirals, and one anti‑protozoan drug for livestock use in certain animals to enhance food safety and curb antimicrobial resistance, representing a major regulatory shift impacting farm animal drug use practices

- In April 2025, the U.S. Food and Drug Administration approved new animal drug products for livestock use, including Zoetis’s Simparica TRIO® for cattle (reducing ammonia emissions and improving feed efficiency) and Flunine‑S™ for swine respiratory disease control, marking significant new drug entries in farm animal healthcare

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。