北米皮膚充填剤市場の規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

3.70 Billion

USD

8.77 Billion

2025

2033

USD

3.70 Billion

USD

8.77 Billion

2025

2033

| 2026 –2033 | |

| USD 3.70 Billion | |

| USD 8.77 Billion | |

| % | |

|

北米皮膚充填剤市場のセグメンテーション:製品タイプ別(生分解性皮膚充填剤と非生分解性皮膚充填剤)、材料タイプ別(天然皮膚充填剤と合成皮膚充填剤)、用途別(フェイスリフト、鼻形成術、再建手術、顔のしわの修正、唇の増強、たるんだ皮膚、頬のくぼみ、皮膚の平滑化、歯科治療、美容修復、唇のふっくら化、瘢痕治療、顎の増大、脂肪萎縮治療、耳たぶの若返り、その他)、薬剤タイプ別(ブランド医薬品とジェネリック医薬品)、エンドユーザー別(皮膚科クリニック、外来手術センター、病院、学術研究機関、その他)、流通チャネル別(直接入札、ドラッグストア、小売薬局、オンライン薬局、その他) - 業界動向と2033年までの予測

北米の皮膚充填剤市場規模

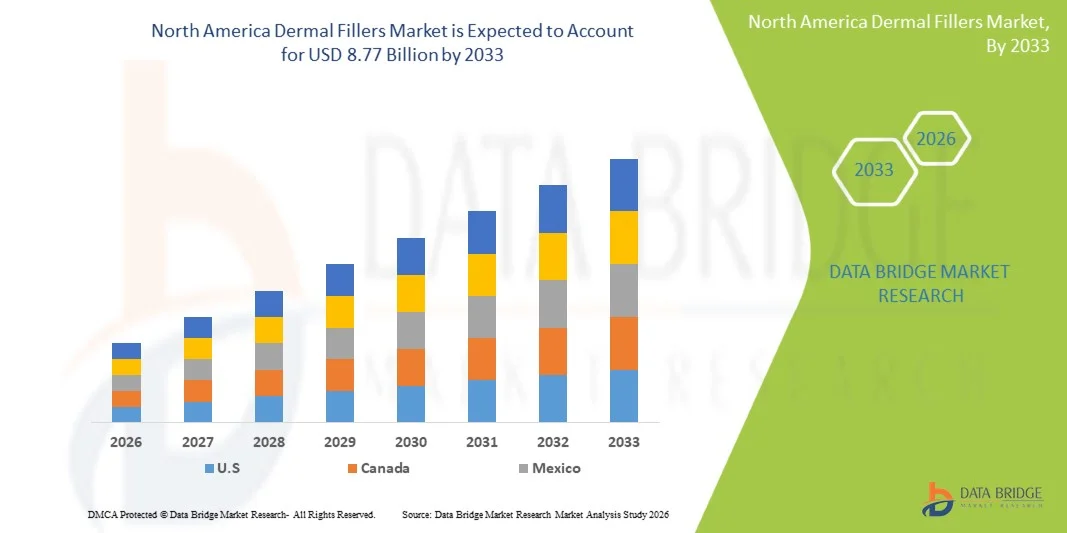

- 北米の皮膚充填剤市場規模は、2025年には37億米ドルと評価され、予測期間中の年平均成長率(CAGR)11.40%で、2033年には87億7000万米ドル に達すると予測されています 。

- 市場の成長は、主に美容整形手術への需要の高まりと、皮膚科クリニックや美容医療センターにおける非外科的顔面若返り治療への認知度の高まりによって促進されています。この傾向は、先進国および新興国の医療市場の両方で、真皮充填剤の普及拡大につながっています。

- さらに、低侵襲美容治療に対する消費者の嗜好の高まり、可処分所得の増加、そして美容医療クリニックの拡大により、ヒアルロン酸注入剤は顔の輪郭形成やしわ軽減のための最も広く用いられている治療法の一つとして定着しつつあります。これらの要因が複合的に作用することで、ヒアルロン酸注入剤の普及が加速し、業界の成長を大きく後押ししています。

北米皮膚充填剤市場分析

- 顔のボリュームを回復させ、しわを軽減し、顔の輪郭を整えるために使用される注射可能な美容製品である真皮充填剤は、低侵襲で回復時間が短い顔の若返り治療を提供できることから、美容クリニック、皮膚科センター、メディカルスパなどにおける現代の美容および皮膚科治療においてますます重要な要素となっています。

- 皮膚充填剤の需要増加の主な要因は、非外科的美容処置の人気上昇、消費者の美容意識の高まり、そして顔面美容やアンチエイジングのための低侵襲性美容治療への嗜好の高まりである。

- 米国は、確立された医療美容産業、美容施術に対する消費者の高い意識、そして大手美容製品メーカーの強力な存在感に支えられ、2025年には北米ダーマルフィラー市場で約39.4%という最大の収益シェアを獲得し、市場を席巻しました。米国では、低侵襲の顔面若返り治療、唇のボリュームアップ、しわ修正施術に対する需要の高まりにより、皮膚科クリニック、美容センター、美容外科施設全体でダーマルフィラー施術が大幅に増加しています。

- カナダは、可処分所得の増加、美容と健康への意識の高まり、美容クリニックの拡大、若年層と高齢者層の両方における非外科的美容処置への需要増加を背景に、予測期間中に北米皮膚充填剤市場で最も急速に成長する地域になると予想されており、年平均成長率(CAGR)は約9.2%となる見込みです。

- ブランドセグメントは、強力なブランド認知度、実証済みの臨床効果、および世界の保健当局からの規制承認に支えられ、2025年には市場収益の約72.3%を占め、最大のシェアを獲得しました。

レポートの範囲と北米皮膚充填剤市場のセグメンテーション

|

属性 |

皮膚充填剤の主要市場インサイト |

|

対象分野 |

|

|

対象国 |

北米

|

|

主要市場プレーヤー |

•ガルデルマ SA (スイス) |

|

市場機会 |

|

|

付加価値データ情報セット |

Data Bridge Market Researchが作成する市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要企業といった市場シナリオに関する洞察に加え、専門家による詳細な分析、患者疫学、パイプライン分析、価格分析、規制枠組みなども含まれています。 |

北米の皮膚充填剤市場の動向

「低侵襲美容施術への需要の高まり」

- 北米の皮膚充填剤市場における重要な、そして加速的なトレンドは、ダウンタイムを最小限に抑え、施術リスクを低減しながら顔の美しさを向上させる低侵襲美容施術への需要の高まりです。消費者は、従来の美容整形手術に伴う複雑さや回復期間を避けつつ、自然な仕上がりを実現する非外科的美容治療をますます好むようになっています。

- 例えば、アラガン・エステティクス社が開発したジュビダームなどのヒアルロン酸注入剤や、ガルデルマ社が開発したレスチレンなどの製品は、世界中のクリニックで皮膚科医や美容医療従事者によって、顔の輪郭形成、しわの軽減、唇のボリュームアップなどの施術に広く使用されています。

- 若年層と高齢者層の両方で美容整形への関心が高まっていることが、顔の若返りのためのヒアルロン酸注入剤の普及拡大につながっています。これらの治療法は、外科手術を必要とせずに、小じわを軽減し、顔のボリュームを回復させ、肌の構造を改善するために広く用いられています。

- In addition, technological advancements in filler formulations, including hyaluronic acid-based fillers and longer-lasting biodegradable materials, are improving treatment safety, longevity, and patient satisfaction. These innovations allow practitioners to achieve more precise aesthetic outcomes while minimizing complications

- The growing influence of social media platforms and beauty trends is also encouraging individuals to seek aesthetic procedures that enhance appearance and boost confidence. Increasing awareness regarding non-invasive cosmetic solutions has significantly expanded the consumer base for dermal filler treatments

- As aesthetic medicine continues to evolve, clinics and medical spas worldwide are expanding their service offerings, further increasing accessibility to dermal filler procedures and supporting sustained market growth

North America Dermal Fillers Market Dynamics

Driver

“Increasing Demand for Aesthetic Enhancements and Aging Population”

- The rising global demand for cosmetic enhancement procedures, combined with the growing aging population seeking anti-aging solutions, is a major driver for the expansion of the North America Dermal Fillers Market. Individuals are increasingly pursuing treatments that help maintain youthful skin and improve facial aesthetics without undergoing invasive surgery

- For instance, companies such as Merz Pharma and Revance Therapeutics are actively expanding their aesthetic product portfolios and launching advanced dermal filler solutions to meet the growing global demand for non-surgical facial rejuvenation treatments

- Increasing disposable incomes and rising consumer spending on aesthetic treatments are also supporting market expansion, particularly in emerging economies where access to cosmetic procedures is becoming more widespread

- Furthermore, the growing presence of specialized dermatology clinics, aesthetic medical centers, and cosmetic surgery facilities is improving access to dermal filler procedures for a larger population

- Continuous advancements in filler materials, injection techniques, and treatment protocols are enhancing safety and effectiveness, encouraging more individuals to consider dermal filler procedures. The expanding acceptance of aesthetic treatments among both men and women is further contributing to the market’s growth trajectory

Restraint/Challenge

“Risk of Side Effects and Regulatory Challenges”

- Despite the growing popularity of dermal fillers, concerns regarding potential side effects and complications remain a significant challenge for the market. Improper injection techniques or the use of low-quality products can result in adverse effects such as swelling, bruising, allergic reactions, and vascular complications

- For instance, regulatory authorities such as the U.S. Food and Drug Administration have issued safety warnings regarding the misuse of dermal fillers and emphasize that these procedures should only be performed by qualified healthcare professionals

- In addition, the presence of counterfeit or unapproved filler products in certain markets can pose serious safety risks and undermine consumer trust in aesthetic procedures. Strict regulatory oversight and quality control measures are therefore essential for ensuring product safety and efficacy

- The relatively high cost of dermal filler treatments may also limit adoption among price-sensitive consumers, particularly in developing regions where cosmetic procedures are considered discretionary expenses

- Moreover, differences in regulatory approval processes across countries can delay product launches and limit the global expansion of certain dermal filler brands. Addressing these challenges through improved practitioner training, stronger regulatory enforcement, and continued product innovation will be essential for sustaining long-term market growth

North America Dermal Fillers Market Scope

The North America Dermal Fillers Market is segmented on the basis of product type, material type, application, drug type, end user, and distribution channel.

• By Product Type

On the basis of product type, the North America Dermal Fillers Market is segmented into Biodegradable Dermal Fillers and Non-Biodegradable Dermal Fillers. The Biodegradable Dermal Fillers segment dominated the largest market revenue share of approximately 68.4% in 2025, driven by their safety profile, temporary nature, and high patient preference for minimally invasive aesthetic treatments. These fillers, primarily composed of hyaluronic acid, collagen, and calcium hydroxylapatite, gradually dissolve in the body, reducing long-term complications. Dermatology clinics and aesthetic centers widely adopt biodegradable fillers for facial contouring, wrinkle reduction, and lip enhancement procedures. The growing demand for non-surgical cosmetic treatments among aging populations significantly supports the segment’s dominance. Technological advancements in filler formulations have improved longevity, smoothness, and injection precision, enhancing patient satisfaction. In addition, biodegradable fillers allow practitioners to adjust treatments over time, making them highly suitable for personalized aesthetic procedures. Increasing awareness regarding aesthetic procedures and rising disposable income in emerging markets also contribute to segment growth. Regulatory approvals and strong product pipelines from leading cosmetic companies further strengthen market penetration. The expansion of medical aesthetic clinics and the rising influence of social media beauty trends are also driving demand for biodegradable dermal fillers globally.

The Non-Biodegradable Dermal Fillers segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, fueled by the growing demand for long-lasting aesthetic results and fewer repeat procedures. Non-biodegradable fillers are designed to provide permanent or semi-permanent facial volume restoration, making them suitable for deep tissue augmentation and structural corrections. These fillers are increasingly used in reconstructive procedures and complex aesthetic treatments requiring durable outcomes. Technological improvements in polymer-based filler materials have enhanced safety and stability, encouraging adoption among aesthetic practitioners. Patients seeking cost-effective long-term results are increasingly opting for non-biodegradable solutions. The segment also benefits from rising demand for facial contouring procedures and advanced cosmetic treatments in developed markets. In addition, increasing research and development activities focused on improving filler biocompatibility and injection techniques support growth. Expanding medical tourism for cosmetic procedures in regions such as North America and Latin America further accelerates adoption. The availability of skilled aesthetic professionals and advanced clinical infrastructure is expected to drive continued growth in this segment.

• By Material Type

On the basis of material type, the North America Dermal Fillers Market is segmented into Natural Dermal Fillers and Synthetic Dermal Fillers. The Natural Dermal Fillers segment dominated the largest market revenue share of approximately 61.5% in 2025, driven by the strong consumer preference for biologically derived and biocompatible materials. Natural fillers such as hyaluronic acid, collagen, and autologous fat are widely used due to their compatibility with human tissue and minimal risk of allergic reactions. These fillers provide natural-looking results and are commonly used in facial wrinkle reduction, lip augmentation, and skin rejuvenation procedures. Dermatologists and cosmetic surgeons frequently recommend natural fillers because of their safety profile and reversible nature. The segment also benefits from increasing demand for minimally invasive aesthetic treatments that deliver subtle yet effective cosmetic improvements. Technological innovations in hyaluronic acid fillers have improved durability and hydration effects, further boosting demand. Growing awareness of aesthetic procedures and increasing acceptance of cosmetic enhancements among younger populations support the segment’s expansion. In addition, strong marketing campaigns by aesthetic product manufacturers and the influence of social media beauty trends contribute to higher adoption.

The Synthetic Dermal Fillers segment is expected to witness the fastest CAGR of 10.2% from 2026 to 2033, driven by advancements in polymer science and the development of durable filler materials. Synthetic fillers such as polymethyl methacrylate (PMMA) and poly-L-lactic acid provide longer-lasting structural support and volume restoration. These fillers are increasingly used for deep tissue augmentation and facial contouring procedures requiring more permanent results. The growing demand for advanced anti-aging treatments among aging populations further supports the segment’s growth. Technological innovations have improved the safety and biocompatibility of synthetic fillers, encouraging their use in specialized cosmetic and reconstructive procedures. Increasing adoption in facial reconstruction, trauma repair, and aesthetic restoration procedures also contributes to rising demand. In addition, growing investments in research and development of next-generation filler materials are expected to accelerate segment expansion globally.

• By Application

On the basis of application, the North America Dermal Fillers Market is segmented into Face Lift, Rhinoplasty, Reconstructive Surgery, Facial Line Correction, Lip Enhancement, Sagging Skin, Cheek Depression, Skin Smoothing, Dentistry, Aesthetic Restoration, Lip Plump, Scar Treatment, Chin Augmentation, Lipoatrophy Treatment, Earlobe Rejuvenation, and Others. The Facial Line Correction segment dominated the largest market revenue share of approximately 34.7% in 2025, driven by the increasing demand for wrinkle reduction and anti-aging treatments. Dermal fillers are widely used to reduce fine lines and deep wrinkles around the eyes, forehead, and mouth. Rising aesthetic consciousness among consumers and the growing aging population are major factors contributing to segment dominance. Dermatology clinics and cosmetic centers frequently offer facial line correction procedures as minimally invasive alternatives to surgical facelifts. Technological improvements in filler formulations have enhanced treatment precision and long-lasting cosmetic outcomes. The increasing influence of social media beauty standards and celebrity endorsements also contributes to higher demand for facial rejuvenation treatments. Furthermore, the growing popularity of lunchtime cosmetic procedures that require minimal recovery time further boosts segment growth. Expanding aesthetic clinics and improved accessibility of cosmetic procedures worldwide reinforce the dominance of this segment.

The Lip Enhancement segment is expected to witness the fastest CAGR of 11.1% from 2026 to 2033, fueled by the increasing popularity of lip augmentation procedures among younger consumers. Social media influence and celebrity beauty trends have significantly increased awareness and demand for fuller lips and facial contouring. Hyaluronic acid fillers are widely used in lip enhancement due to their ability to provide natural-looking volume and reversible results. Dermatology clinics and aesthetic centers are experiencing growing patient demand for minimally invasive lip augmentation treatments. Technological innovations in filler formulations allow precise volume control and improved aesthetic outcomes. In addition, increasing medical tourism for cosmetic procedures and expanding availability of trained aesthetic professionals support segment growth. Rising disposable income and increasing acceptance of cosmetic enhancements among millennials and Generation Z further accelerate the adoption of lip enhancement procedures globally.

• By Drug Type

On the basis of drug type, the North America Dermal Fillers Market is segmented into Branded and Generic. The Branded segment dominated the largest market revenue share of approximately 72.3% in 2025, driven by strong brand recognition, proven clinical efficacy, and regulatory approvals from global health authorities. Leading pharmaceutical and aesthetic companies invest heavily in research and development to introduce innovative filler formulations with improved safety and performance. Dermatology clinics and aesthetic practitioners prefer branded products due to their consistent quality and established clinical evidence. The availability of diverse branded dermal filler products tailored for specific aesthetic procedures further supports segment dominance. Increasing marketing campaigns, physician training programs, and partnerships with cosmetic clinics also contribute to higher adoption. In addition, consumer trust in established brands and the perceived safety of branded products play a critical role in maintaining market leadership.

The Generic segment is expected to witness the fastest CAGR of 9.6% from 2026 to 2033, driven by the increasing demand for cost-effective aesthetic treatment options. Generic dermal fillers provide similar functional benefits at lower prices, making them accessible to a broader patient population. Growing competition among manufacturers and the expiration of patents for several branded filler products have facilitated the entry of generic alternatives into the market. Emerging economies are witnessing higher adoption of generic fillers due to price sensitivity and expanding medical aesthetic markets. Increasing availability of affordable cosmetic treatments is encouraging first-time consumers to undergo aesthetic procedures.

• By End User

On the basis of end user, the North America Dermal Fillers Market is segmented into Dermatology Clinics, Ambulatory Surgical Centers, Hospitals, Academic Research Institutes, and Others. The Dermatology Clinics segment dominated the largest market revenue share of approximately 49.2% in 2025, due to the high volume of cosmetic procedures performed in specialized aesthetic clinics. These clinics offer a wide range of minimally invasive aesthetic treatments, including dermal fillers, botulinum toxin injections, and skin rejuvenation procedures. Dermatologists and cosmetic specialists are highly trained in facial anatomy and injection techniques, ensuring safe and effective treatment outcomes. Increasing patient preference for specialized aesthetic clinics over hospitals further supports segment dominance. The expansion of private dermatology and cosmetic clinics globally also contributes to higher procedure volumes.

The Ambulatory Surgical Centers segment is expected to witness the fastest CAGR of 10.7% from 2026 to 2033, driven by the growing demand for outpatient cosmetic procedures. ASCs offer advanced aesthetic treatments with shorter procedure times and lower operational costs compared to traditional hospital settings. Patients prefer ambulatory centers due to faster recovery times and convenient scheduling of procedures. The increasing number of minimally invasive cosmetic treatments performed in outpatient settings further accelerates segment growth.

• By Distribution Channel

On the basis of distribution channel, the North America Dermal Fillers Market is segmented into Direct Tender, Drug Stores, Retail Pharmacy, Online Pharmacy, and Others. The Direct Tender segment dominated the largest market revenue share of approximately 44.8% in 2025, driven by bulk procurement agreements between manufacturers and hospitals or dermatology clinics. Healthcare institutions often purchase dermal fillers directly from manufacturers to ensure product authenticity and cost efficiency. The direct supply model also enables better inventory management and reliable product availability. Increasing partnerships between cosmetic product manufacturers and aesthetic clinics further support this segment’s dominance.

The Online Pharmacy segment is expected to witness the fastest CAGR of 11.3% from 2026 to 2033, fueled by the rapid expansion of digital healthcare platforms and e-commerce distribution channels. Online platforms offer convenient purchasing options, competitive pricing, and wider product availability for clinics and licensed practitioners. Increasing adoption of digital procurement systems in healthcare institutions further accelerates segment growth. In addition, the rising penetration of e-commerce and telemedicine platforms globally is expected to support the expansion of online distribution channels in the North America Dermal Fillers Market.

North America Dermal Fillers Market Regional Analysis

- 北米の皮膚充填剤市場は、医療美容産業の拡大、可処分所得の増加、米国やカナダなどの国々における美容整形手術に対する消費者の意識の高まりを背景に、予測期間中に著しい成長が見込まれています。

- 急速な都市化、美の基準の変化、そしてソーシャルメディアやセレブリティ文化の影響力の増大は、顔の見た目を改善し自信を高める美容施術を求める人々を後押ししています。さらに、この地域全体で皮膚科クリニック、美容外科センター、専門的な美容医療施設が増加していることも、ヒアルロン酸注入治療へのアクセス向上につながっています。

- 政府や民間医療機関も高度な医療インフラに投資しており、美容医療の成長をさらに後押ししている。その結果、顔の輪郭形成、しわの軽減、肌の若返りのためのヒアルロン酸注入などの低侵襲治療が北米地域全体で急速に普及している。

米国・北米の皮膚充填剤市場に関する洞察

米国北米の皮膚充填剤市場は、2025年には北米地域で約39.4%という最大の収益シェアを占めると予測されています。これは、米国における確立された医療美容産業、美容施術に対する消費者の高い意識、そして大手美容製品メーカーの強力な存在感に支えられています。米国では、低侵襲の顔面若返り治療、唇のボリュームアップ、しわ修正施術への需要の高まりにより、皮膚科クリニック、美容センター、美容外科施設全体で皮膚充填剤施術が大幅に増加しています。さらに、ソーシャルメディアプラットフォームや美容トレンドの影響力の高まりが、若い消費者に非外科的美容施術を求めるよう促しています。民間美容クリニックの拡大、医療美容分野への投資の増加、そして高度な皮膚充填剤製品の入手可能性の向上も、米国市場の成長をさらに促進しています。

カナダ・北米皮膚充填剤市場の概況

カナダの北米ダーマルフィラー市場は、予測期間中に北米地域で最も急速に成長すると予想されており、年平均成長率(CAGR)は約9.2%に達すると見込まれています。この成長は主に、可処分所得の増加、美容と健康に対する意識の高まり、主要都市における皮膚科クリニックや美容治療センターのネットワーク拡大によって牽引されています。デジタルメディア、セレブリティ文化、美容トレンドの影響力の高まりも、若い世代が顔の美しさを向上させる美容治療を求める動機となっています。さらに、迅速な効果と最小限のダウンタイムを提供する低侵襲美容処置への嗜好の高まりも、カナダにおけるダーマルフィラー治療の普及を促進しています。熟練した皮膚科医の存在、民間美容クリニックの拡大、パーソナルケアや美容処置に対する消費者の支出増加も、カナダにおける北米ダーマルフィラー市場の急速な成長に貢献しています。

北米の皮膚充填剤市場シェア

皮膚充填剤業界は主に、以下のような実績のある企業によって牽引されています。

• ガルデルマ SA (スイス)

• メルツ ファーマ GmbH & Co. KGaA (ドイツ)

• レバンス セラピューティクス Inc. (米国)

• シンクレア ファーマ plc (英国)

• テオキサン ラボラトリーズ (スイス)

• ヒューゲル Inc. (韓国)

• LG ケミカル Ltd. (韓国)

• バイオプラス Co., Ltd. (韓国)

• アニカ セラピューティクス Inc. (米国)

• スネバ メディカル Inc. (米国)

• プロレニウム メディカル テクノロジーズ Inc. (カナダ)

• バイオキシス ファーマシューティカルズ (フランス)

• クロマ ファーマ GmbH (オーストリア)

• コントゥラ インターナショナル Ltd. (英国)

• メディトックス Inc. (韓国)

• ブルームエイジ バイオテクノロジー コーポレーション リミテッド (中国)

• ヒューオンズ グローバル Co., Ltd. (韓国)

• ジェテマ Co., Ltd. (韓国)

• サイビジョン バイオテック Inc. (台湾)

北米の皮膚充填剤市場における最新動向

- 2025年2月、世界的な美容医療企業であるEvolus, Inc.は、中等度から重度の鼻唇溝の治療を目的としたヒアルロン酸注入剤「Evolysse Form」と「Evolysse Smooth」について、米国FDAの承認を取得しました。これらの注入剤は、製品の持続性と自然な仕上がりを向上させるためにCold-Xテクノロジーを採用しています。この承認は、Evolusの米国注入剤市場への参入を意味し、多様な美容製品ポートフォリオへの移行を後押しするものです。

- 2025年3月、Laboratoires VIVACYは、Burgeon Biotechnologyとの戦略的提携を発表し、同社のSTYLAGE真皮充填剤とNOVUMAバイオ刺激剤技術を統合しました。この提携により、ヒアルロン酸とハイドロキシアパタイト技術が組み合わされ、肌質の向上と高度な注入型美容ソリューションの提供が実現します。

- 2025年5月、メディトックスは、ニューラミス製品ラインに、ヒアルロン酸をベースとしたプレミアムな皮膚充填剤であるニューラミスハートとニューラミススキンエンハンサーの2種類を追加しました。この発売により、肌の水分量、弾力性、顔のボリューム回復を改善するために設計された、同社の注入型美容ソリューションのポートフォリオが拡大しました。

- 2025年8月、Revance Therapeutics社は米国でメピバカイン配合のTeoxane RHAコレクションを発表しました。これは、フィラー麻酔薬製剤における約20年ぶりの大きな革新となります。この新製剤は、従来のリドカインをメピバカインに置き換えることで、皮膚充填剤施術時の内出血を軽減しつつ、同等の鎮痛効果を実現することを目指しています。

- 2024年10月、Evolus社は、同社の注射用ヒアルロン酸ゲル「Estyme」が、欧州連合医療機器規則(MDR)に基づき、4種類の皮膚充填剤製品として認証を取得したことを発表しました。この認証により、同社は欧州市場における皮膚充填剤のプレゼンスを拡大し、国際的な美容医療製品ポートフォリオを強化することが可能になりました。

- 2024年5月、ガルデルマ社は、先進的なNASHAゲル技術と精密注入システムを搭載した強化版レスチレン皮膚充填剤ポートフォリオをヨーロッパと北米で発売し、美容施術における治療の多様性と患者の快適性を向上させました。

- 2023年4月、アラガン・エステティクス(アッヴィ傘下)は、ハイドロキシアパタイト(CaHA)とヒアルロン酸(HA)を組み合わせた二重作用の皮膚充填剤であるHArmonyCaを発売しました。HArmonyCaは、即効性のあるリフトアップ効果と長期的なコラーゲン生成促進効果の両方を提供し、顔の若返り治療に効果を発揮します。

- 2023年6月、クロマ・ファーマ社は、中顔面ボリューム不足を対象としたヒアルロン酸注入剤「プリンセス・ボリューム・プラス・リドカイン」の第III相臨床試験を中国で開始しました。この多施設共同臨床試験は、複数の病院で実施され、規制当局の承認取得を支援するとともに、北米の美容医療市場における同社のプレゼンス拡大を目指しています。

- 2021年2月、メルツ・エステティクスは米国でリドカイン配合のBELOTERO BALANCE(+)を発売しました。この製品は、注射時の患者の快適性を向上させ、しわやたるみの改善施術において顔面組織へのスムーズな浸透を実現するように設計されています。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。