Europe Infectious Disease Diagnostics Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

12.71 Billion

USD

20.19 Billion

2024

2032

USD

12.71 Billion

USD

20.19 Billion

2024

2032

| 2025 –2032 | |

| USD 12.71 Billion | |

| USD 20.19 Billion | |

| % | |

|

Europe Infectious Disease Diagnostics Market Segmentation, By Product & Service (Assays, Kits, Reagents, Instruments, Service & Software), Technology (Immunodiagnostics, Molecular Diagnostics, Clinical Microbiology, PCR, INAAT, DNA Sequencing & NGS, DNA Microarray, Other Technologies), Disease Type (Hepatitis, HIV, CT/NG, HAIS, HPV, TB, Influenza, Other Infectious Diseases), End User (Hospital/Clinical Laboratories, Reference Laboratories, Physician Offices, Academic/Research Institutes, Other End Users) - Industry Trends and Forecast to 2032

Infectious Disease Diagnostics Market Size

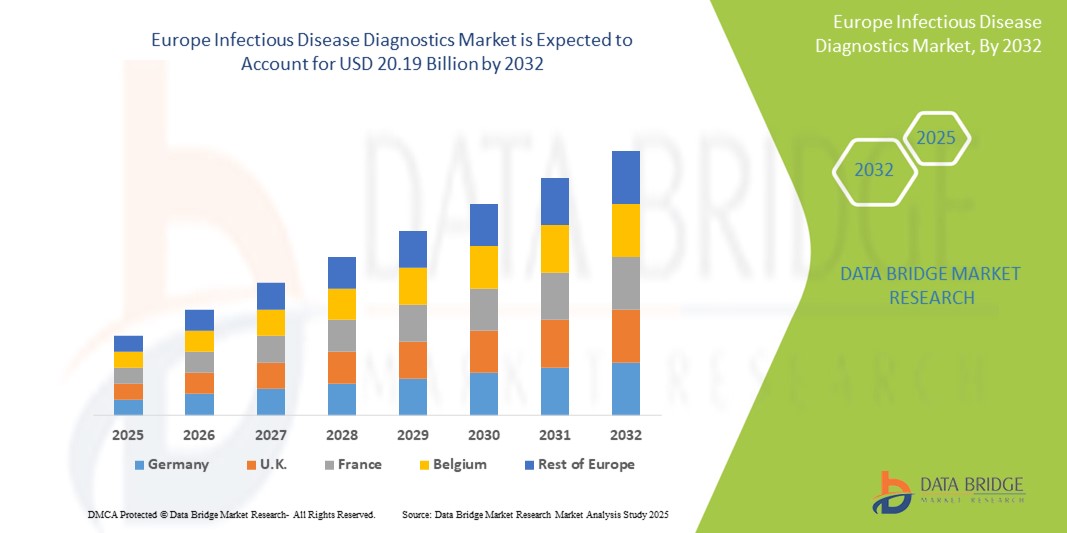

- The Europe Infectious Disease Diagnostics market size was valued at USD 12.71 Billion in 2024 and is expected to reach USD 20.19 Billion by 2032, at a CAGR of 5.9% during the forecast period

- The Europe infectious disease diagnostics market includes a wide array of advanced testing technologies and platforms designed to detect, identify, and monitor infectious pathogens such as bacteria, viruses, fungi, and parasites.

- These diagnostic tools are vital for early and accurate diagnosis, enabling effective treatment and containment of infectious diseases across healthcare settings. Key types of diagnostics include molecular assays (PCR, NAAT), immunoassays, rapid point-of-care tests, culture-based methods, and next-generation sequencing. They are applied in clinical microbiology, hospital laboratories, public health surveillance, and research institutions, targeting diseases like influenza, HIV/AIDS, tuberculosis, hepatitis, and emerging infectious threats.

Infectious Disease Diagnostics Market Analysis

- The Europe infectious disease diagnostics market is driven by the rising prevalence of infectious diseases, increased awareness of early diagnosis benefits, and rapid adoption of molecular and point-of-care technologies. The COVID-19 pandemic significantly accelerated demand for fast, reliable diagnostic solutions and strengthened diagnostic infrastructure. Technological advancements—including multiplex testing, digital diagnostics, AI-based data analysis, and integration with healthcare IT systems—are propelling market growth. Furthermore, government initiatives focused on disease surveillance, antimicrobial resistance, and vaccination campaigns are expanding diagnostic testing requirements.

- The increasing healthcare expenditure, growing elderly population vulnerable to infections, and rising incidence of hospital-acquired infections further support market expansion. Cross-sector collaborations among public health agencies, hospitals, and diagnostic companies are also enhancing the availability and uptake of innovative diagnostics.

- Germany dominates the Infectious Disease Diagnostics market in Europe, holding the largest revenue share of 27.9% in 2025, fueled by its advanced healthcare infrastructure, strong diagnostics industry, and extensive research and development activities. The country’s proactive infectious disease management programs, favorable reimbursement policies, and high adoption of cutting-edge molecular platforms continue to drive market leadership.

- Germany is also projected to be the fastest-growing country in this market during the forecast period, supported by investments in high-throughput testing, digital diagnostic integration, and response readiness for emerging infectious diseases. The country’s focus on antimicrobial resistance monitoring and public health preparedness further stimulates market growth.

- Molecular diagnostics is expected to be the largest segment in Europe’s infectious disease diagnostics market with a significant share of 31.2% in 2025, due to its high sensitivity, specificity, and rapid turnaround. PCR and nucleic acid amplification techniques are widely used for detecting viruses and bacteria, including novel pathogens.

Report Scope and Infectious Disease Diagnostics Market Segmentation

|

Attributes |

Infectious Disease Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

Data Bridge Market Research에서 큐레이팅한 시장 보고서에는 시장 가치, 성장률, 세분화, 지리적 적용 범위, 주요 기업 등 시장 시나리오에 대한 통찰력 외에도 심층적인 전문가 분석, 가격 분석, 브랜드 점유율 분석, 소비자 설문 조사, 인구 통계 분석, 공급망 분석, 가치 사슬 분석, 원자재/소모품 개요, 공급업체 선택 기준, PESTLE 분석, Porter 분석 및 규제 프레임워크가 포함되어 있습니다. |

감염병 진단 시장 동향

“개인화 및 디지털 진단 기술의 발전 ”

- 분자 진단 및 개인 맞춤형 검사의 기술 발전: 유럽 감염병 진단 시장에서 중요하고 빠르게 발전하는 추세는 분자 및 유전체 진단 기술의 지속적인 혁신입니다. 이러한 발전은 정확도를 높이고, 병원균을 신속하게 검출하며, 개인 맞춤형 치료 접근법을 가능하게 하여 환자 치료 결과를 개선하고 있습니다.

- 예를 들어, 차세대 시퀀싱(NGS) 플랫폼은 정확한 병원균 식별 및 항생제 내성 프로파일링에 점점 더 많이 사용되고 있습니다.

- 디지털 헬스 플랫폼 및 웨어러블 기기와의 통합: 시장에서는 지속적인 모니터링 및 실시간 데이터 분석을 위해 디지털 헬스 플랫폼, 웨어러블 기술, 모바일 애플리케이션과 진단 기술의 통합이 증가하고 있습니다. 이러한 통합은 질병의 조기 발견 및 효율적인 관리를 지원합니다.

- 예를 들어, 모바일 앱과 결합된 웨어러블 바이오센서를 사용하면 감염성 질환 증상과 생체 신호를 원격으로 모니터링할 수 있습니다.

- 진료소 검사의 성장: 신속한 진료소 진단 검사가 인기를 얻고 있으며, 전통적인 실험실 환경 밖에서도 빠르고 신뢰할 수 있는 결과를 제공하여 시기적절한 임상적 결정을 내리고 전염병 확산을 통제할 수 있습니다.

- 항생제 내성에 대한 인식이 높아짐에 따라 내성 병원균을 식별할 수 있는 진단법에 대한 수요가 늘어나고 있으며, 이를 통해 표적 항생제 사용이 촉진되고 항생제 관리가 개선되고 있습니다.

- AI와 머신 러닝 기술은 진단 데이터를 분석하여 예측 능력, 진단 정확도, 개인화된 치료 전략을 강화하는 데 점점 더 많이 활용되고 있습니다.

감염병 진단 시장 동향

운전사

“감염성 질환 유병률 증가 및 신속한 진단 필요성”

- 새로운 바이러스 발병 및 약물 내성 감염을 포함한 유럽 전역의 전염병 유병률 증가로 인해 신속하고 정확한 진단 도구에 대한 수요가 증가하고 있습니다.

- 예를 들어, COVID-19 팬데믹은 확산을 통제하고 치료 결과를 개선하기 위해 신속하고 신뢰할 수 있는 감염병 진단의 절실한 필요성을 강조했습니다.

- 조기 진단의 이점에 대한 의료 서비스 제공자와 환자의 인식이 높아짐에 따라 시장 도입이 가속화되고 있습니다.

- 감염병 감시 및 진단 인프라를 강화하기 위한 정부 주도의 계획과 자금 지원은 시장 성장을 더욱 뒷받침합니다.

- 인구 고령화와 면역 저하 환자의 증가로 인해 감염 위험이 커지고, 효과적인 진단에 대한 수요도 증가하고 있습니다.

- 외래환자 서비스 확대 및 재택 검사 솔루션 확대로 휴대가 간편하고 사용이 편리한 진단 장치 개발 촉진

제지/도전

“ 높은 비용과 규제 장벽 ”

- 진보된 감염병 진단 기술과 관련된 높은 비용으로 인해 접근성이 제한되며, 특히 소규모 병원과 실험실에서는 더욱 그렇습니다.

- 예를 들어, 디지털 기능이 통합된 정교한 분자 진단 플랫폼은 비용이 많이 들며 일부 의료 서비스 제공자에게는 부담스러울 수 있습니다.

- 유럽의 엄격한 규제 요건과 긴 승인 절차로 인해 제품 출시가 지연되고 규정 준수 비용이 증가할 수 있습니다.

- 복잡한 진단 장비를 조작할 수 있는 숙련된 의료 전문가가 부족하여 광범위한 도입이 어렵습니다.

- 진단 정확도와 민감도의 변동성에 대한 우려는 임상의의 신뢰를 떨어뜨리고 시장 성장에 영향을 미칠 수 있습니다.

- 특히 GDPR 준수를 포함한 디지털 건강 통합과 관련된 데이터 개인 정보 보호 및 보안 문제는 보다 광범위한 구현에 과제를 제기합니다.

감염성 질환 진단 시장 범위

시장은 제품 및 서비스, 기술, 질병 유형, 최종 사용자를 기준으로 세분화됩니다.

- 제품별

감염성 질환 진단 시장은 제품 기준으로 분석법, 키트, 시약, 기기, 그리고 서비스 및 소프트웨어로 구분됩니다. 분석법 및 키트 부문은 실험실 및 현장 진료 환경에서 신속하고 정확한 병원균 검출을 가능하게 하는 중요한 역할을 하며, 2025년에는 39.2%의 가장 큰 매출 점유율을 기록하며 시장을 장악할 것으로 예상됩니다. 이러한 키트는 다양한 감염성 질환 검사에 있어 편의성과 효율성을 제공합니다.

서비스 및 소프트웨어 부문은 2025년부터 2032년까지 가장 빠른 성장률을 보일 것으로 예상되며, 이는 데이터 관리, 원격 진단, 진단 정확도와 워크플로 효율성을 향상시키는 AI 기반 분석을 위한 통합 디지털 솔루션 도입 증가에 힘입은 것입니다.

- 기술로

감염병 진단 시장은 제품 기준으로 면역진단, 분자진단, 임상미생물학, PCR, INAAT(등온 핵산 증폭 기술), DNA 시퀀싱 및 NGS(차세대 시퀀싱), DNA 마이크로어레이, 그리고 기타 기술로 세분화됩니다. 분자진단 분야는 바이러스와 박테리아를 포함한 다양한 감염원을 검출하는 데 있어 높은 민감도와 특이도를 자랑하며, 가장 큰 매출 점유율을 기록하며 시장을 주도할 것으로 예상됩니다. PCR과 NGS와 같은 분자진단 기술은 빠르고 정확한 진단을 위해 널리 사용되고 있습니다.

The DNA Sequencing & NGS segment is projected to witness the fastest CAGR from 2025 to 2032, driven by advances in genomics and personalized medicine approaches, allowing comprehensive pathogen identification and antimicrobial resistance profiling.

- By Disease Type

On the basis of Disease Type, the Infectious Disease Diagnostics market is segmented into Hepatitis, HIV, CT/NG (Chlamydia trachomatis/Neisseria gonorrhoeae), HAIs (Healthcare-Associated Infections), HPV (Human Papillomavirus), TB (Tuberculosis), Influenza, and Other Infectious Diseases. The HIV held the largest market revenue share in due to the high prevalence and extensive screening programs across Europe.

The TB is expected to witness the fastest CAGR from 2025 to 2032, supported by increased public health efforts for early detection and control, especially with the emergence of drug-resistant strains.

- By End users

On the basis of end users, the Infectious Disease Diagnostics market is segmented into Hospital/Clinical Laboratories, Reference Laboratories, Physician Offices, Academic/Research Institutes, and Other End Users. The Hospital/Clinical Laboratories segment accounted for the largest market revenue share in 2024, accounting for the largest revenue share, as these facilities conduct the majority of infectious disease testing with advanced diagnostic equipment and skilled personnel.

The Reference Laboratories segment is expected to witness the fastest CAGR from 2025 to 2032, during the forecast period, owing to their role in specialized and high-complexity testing, including genomic sequencing and outbreak investigations.

Infectious Disease Diagnostics Market Regional Analysis

- Germany dominates the Europe Infectious Disease Diagnostics Market, accounting for the largest revenue share of 27.9% in 2025, This leadership is driven by the country’s highly advanced healthcare infrastructure, extensive public health programs, and strong presence of specialized diagnostic laboratories. Germany is a pioneer in adopting cutting-edge molecular diagnostics, next-generation sequencing (NGS), and rapid point-of-care testing, particularly for diseases like HIV, tuberculosis, and healthcare-associated infections (HAIs).

- Germany’s dominance is further reinforced by significant investments in digital health platforms and integration of AI-based diagnostics, especially in major cities such as Berlin, Munich, and Hamburg. The presence of leading global and regional diagnostics manufacturers, alongside strong government funding for infectious disease control and research, accelerates market growth. Collaborative networks among academic institutions, biotech startups, and healthcare providers foster continuous innovation and advanced diagnostic solutions.

France Infectious Disease Diagnostics Market Insight

The France Infectious Disease Diagnostics market is expected to register robust growth during the forecast period, supported by national healthcare modernization efforts and increasing focus on infectious disease surveillance and management. France is expanding diagnostic capacities through upgraded clinical laboratories and adoption of rapid molecular tests across hospitals and outpatient settings. The government’s commitment to strengthening infectious disease control, combined with reimbursement reforms and public health initiatives, is encouraging wider use of advanced diagnostics such as PCR, immunodiagnostics, and digital reporting systems. Public and private healthcare facilities in cities like Paris, Lyon, and Marseille are investing in automated and integrated diagnostic platforms, particularly for HIV, hepatitis, and respiratory infections.

U.K. Infectious Disease Diagnostics Market Insight

The U.K. Infectious Disease Diagnostics market is poised for significant growth, driven by increased funding through the NHS for infectious disease control, rising incidence of antibiotic-resistant infections, and expanding use of point-of-care and digital diagnostics. Despite challenges related to regulatory alignment post-Brexit, the U.K. maintains robust import channels and regulatory standards compatible with international norms, facilitating access to advanced diagnostic technologies. Leading hospitals and reference laboratories in London, Manchester, and Edinburgh are rapidly adopting molecular diagnostic tools, rapid antigen tests, and integrated digital health solutions to enhance early detection and treatment of infectious diseases.

Infectious Disease Diagnostics Market Share

The Infectious Disease Diagnostics industry is primarily led by well-established companies, including:

- Abbott Laboratories (U.S.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- bioMérieux SA (France)

- DiaSorin S.p.A (Italy)

- Bio-Rad Laboratories, Inc. (U.S.)

- Danaher Corporation (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- QIAGEN (Netherlands)

- Siemens Healthineers AG (Germany)

- Hologic, Inc. (U.S.)

- Becton, Dickinson and Company (U.S.)

- Trinity Biotech Plc (Ireland)

- Sysmex Corporation (Japan)

Latest Developments in Europe Infectious Disease Diagnostics Market

-

In January 2025, Roche Diagnostics launched the cobas Liat PCR System across several European countries, offering rapid, fully automated molecular testing for infectious diseases such as influenza and COVID-19, reflecting a growing trend toward rapid point-of-care molecular diagnostics.

- In September 2024, Qiagen introduced its QIAstat-Dx Respiratory SARS-CoV-2 Panel in Europe, a multiplex molecular test capable of detecting multiple respiratory pathogens simultaneously, indicating advances in comprehensive syndromic testing.

- 2024년 6월, BioMérieux는 항균제 내성(AMR) 유전자 검출을 위한 새로운 패널을 출시하여 BIOFIRE® FILMARRAY® 시스템 포트폴리오를 확장했으며, 표적 치료를 안내하기 위해 내성 병원균을 신속하게 식별하는 데 중점을 두고 있습니다.

- 2023년 11월, Hologic은 유럽에서 Aptima® Multitest Swab Collection Kit를 출시하여 성병 검체 수집을 개선하고 검사 정확도와 환자 편안함을 높였습니다.

- 2023년 3월, Abbott은 새로운 감염병에 대응하여 빠르고 휴대하기 편리한 진단 솔루션에 대한 지속적인 수요를 강조하며 더 많은 유럽 시장에 ID NOW™ COVID-19 신속 분자 검사 플랫폼을 출시했습니다.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.