Europe Refractories Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

6.43 Billion

USD

9.57 Billion

2024

2032

USD

6.43 Billion

USD

9.57 Billion

2024

2032

| 2025 –2032 | |

| USD 6.43 Billion | |

| USD 9.57 Billion | |

| % | |

|

Europe Refractories Market Segmentation, By Alkalinity (Acidic & Neutral Refractories and Carbon), Form Type (Bricks, Monolithic and Others), Product Type (Clay and Non-Clay), Fusion Temperature (Normal Refractory (1580-1780°C), High Refractory (1780-2000°C) and Super Refractory (2000°C)), Application (Iron and Steel, Cement and Lime, Energy and Chemicals, Glass, Non-Ferrous Metals and Others), Technology (Isostatics and Slide Gates), - Industry Trends and Forecast to 2032

Europe Refractories Market Size

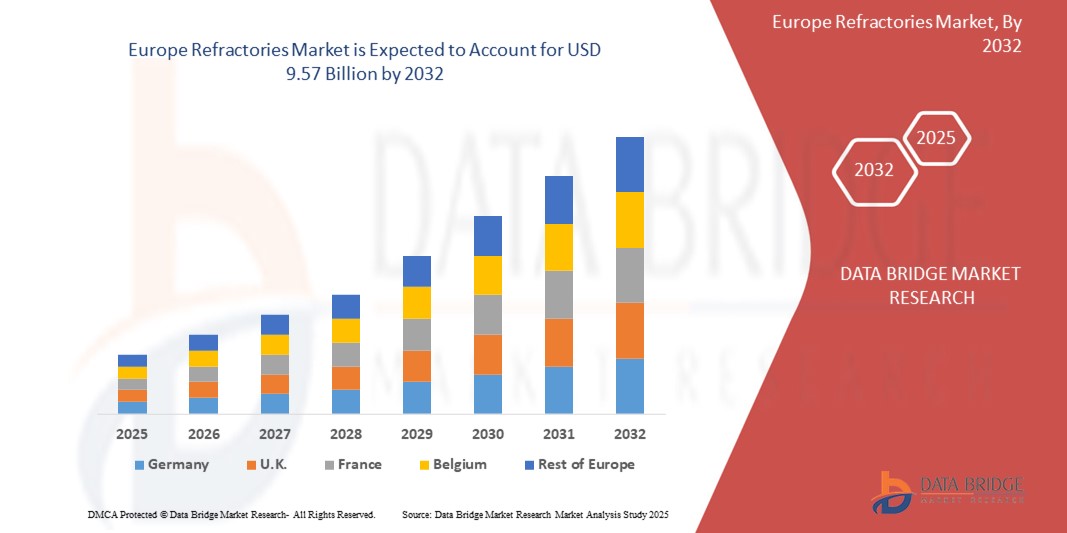

- The refractories market in Europe was valued at approximately USD 6.43 billion in 2024.It is expected to reach USD 9.57 billion by 2032, at a CAGR of 5.1% during the forecast period

- The market growth is largely fueled by the sustained growth and technological advancements within Europe's heavy industries, particularly iron and steel, cement, and glass, coupled with significant investments in infrastructure development

- Furthermore, rising demand for durable and heat-resistant materials in high-temperature industrial processes, driven by a focus on energy efficiency and sustainable practices, is establishing advanced refractories as critical components for modern industrial operations. These converging factors are accelerating the uptake of refractory solutions, thereby significantly boosting the industry's growth

Europe Refractories Market Analysis

- Refractories, offering high-temperature resistance and durability, are vital components in modern industrial processes, including steelmaking, glass manufacturing, and cement production, due to their crucial role in ensuring operational efficiency and prolonging equipment lifespan

- The escalating demand for refractories is primarily fueled by the sustained growth of heavy industries, increasing infrastructure development, and a rising focus on energy efficiency and sustainable manufacturing practices across Europe

- Europe holds a significant market share (approximately 14.2% in 2024). Within Europe, Germany traditionally holds the largest market share, characterized by its robust industrial base, while countries like the UK and Russia are experiencing substantial growth, driven by investments in modernization and infrastructure

- The Iron & Steel segment continues to dominate the refractories market in Europe with a significant market share of around 64.89% in 2024, driven by the extensive use of refractories in various steelmaking processes. The Glass & Ceramics segment is expected to be the fastest-growing during the forecast period due to increasing demand from these industries

Report Scope and Europe Refractories Market Segmentation

|

Attributes |

Smart Lock Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Refractories Market Trends

"Digitalization and Advanced Analytics for Optimized Performance"

- A significant and accelerating trend in the European refractories market is the deepening integration of digitalization, advanced analytics, and AI/Machine Learning (ML) throughout the entire refractory lifecycle. This fusion of technologies is significantly enhancing operational efficiency, extending refractory lifespan, and improving decision-making for end-users

- For instance, leading companies like RHI Magnesita are developing refractory management tools that combine production data with AI technology to predict refractory behavior in real-time, helping clients make fact-based decisions on when to replace linings. Similarly, advanced measurement systems like MINSCAN LSC are being integrated into Electric Arc Furnaces (EAFs) to provide real-time automated refractory maintenance, ensuring safer and more cost-effective operations

- AI and ML integration in refractories enables features such as:

- Predictive Maintenance: Analyzing vast amounts of data (temperature, pressure, gas composition) from sensors embedded in kilns and furnaces to predict wear patterns and potential malfunctions, allowing for proactive maintenance and reducing unplanned downtime

- Process Optimization: AI algorithms can analyze historical data to determine optimal process parameters, significantly enhancing energy efficiency and reducing CO2 emissions

- Improved Quality Control: Data-driven insights and predictive tools can accelerate innovation in materials science, leading to the development of higher-performing refractories

- Enhanced Recycling: Advanced sorting equipment utilizing technologies like laser-induced breakdown spectroscopy and hyperspectral imaging cameras are being developed to improve the yield and quality of recycled refractory materials

- The seamless integration of digital tools and AI in refractory management facilitates centralized control over various aspects of industrial operations. Through a single interface, users can monitor refractory wear, manage maintenance schedules, and optimize energy usage alongside other plant operations, creating a unified and automated production environment

- This trend towards more intelligent, intuitive, and interconnected refractory systems is fundamentally reshaping industry expectations for industrial process management and sustainability. Consequently, companies are investing heavily in research and development to create "smart refractories" that offer enhanced performance and contribute to a more efficient and sustainable industrial landscape

- The demand for refractories that offer seamless digitalization and advanced analytical capabilities is growing rapidly across key industrial sectors, as producers increasingly prioritize operational efficiency, cost reduction, and environmental responsibility

Europe Refractories Market Dynamics

Driver

"Growing Need Due to Industrial Growth, Infrastructure Development, and Sustainability Focus"

- The increasing demand for durable and high-temperature-resistant materials from Europe's core industries, coupled with significant investments in infrastructure and a rising focus on sustainability, is a significant driver for the heightened demand for refractories

- For instance, the European Union's ambitious plans to double its freight rail capacity by 2030 and cut CO2 emissions will drive substantial demand for iron and steel, which are essential for constructing new rail systems. Refractories play a critical role in iron and steel production, lining furnaces to ensure durability and heat resistance during steelmaking processes. Such initiatives by governmental bodies and industrial trends are expected to drive the refractories industry growth in the forecast period

- As industries become more aware of the critical need for efficient high-temperature processes and seek enhanced operational longevity for their equipment, refractories offer advanced features such as improved thermal insulation, resistance to corrosive environments, and extended lifespan, providing a compelling advantage over less specialized materials

- Furthermore, the growing push for energy efficiency and reduced carbon emissions across European industries is making advanced refractories an integral component of sustainable manufacturing. Modern refractories are designed to minimize heat loss, optimize energy consumption, and support cleaner production processes

- The demand for higher-performance refractories that can withstand increasingly extreme conditions in modern industrial furnaces, coupled with the ability to contribute to energy savings and reduced environmental impact, are key factors propelling the adoption of advanced refractory solutions in various industrial sectors. The trend towards optimizing industrial processes for both economic and environmental benefits further contribute to market growth

Restraint/Challenge

"Raw Material Price Volatility, Environmental Regulations, and High Energy Costs"

- Concerns surrounding the volatility of raw material prices, stringent environmental regulations, and high energy costs pose significant challenges to the broader market penetration and profitability of the European refractories industry. As refractories rely heavily on specific minerals and energy-intensive production processes, they are susceptible to fluctuations in global commodity markets and the increasing cost of complying with environmental standards

- For instance, reports indicate that the prices of refractory raw materials like bauxite, magnesite, and graphite have experienced significant surges (over 25% in recent years) due to factors such as supply chain disruptions, geopolitical tensions, and export restrictions from key producing countries (e.g., China). This directly impacts production costs for European manufacturers. Additionally, the energy crisis in Europe has led to substantial increases in energy bills for refractory producers, with some reporting increases of up to 700%, pushing the industry to rethink energy consumption on-site

- Addressing these challenges through strategic sourcing, vertical integration, and investment in sustainable practices is crucial for building market resilience. Companies are exploring diversified supply chains and investing in recycling technologies to mitigate raw material price fluctuations. Furthermore, the European Union's stringent environmental regulations, such as the Carbon Border Adjustment Mechanism (CBAM), compel refractory manufacturers to invest in cleaner production methods and reduce emissions, adding to operational costs. While these regulations drive innovation towards greener refractories, the initial investment required for new technologies and compliance can be a barrier for some manufacturers

- The perceived high initial cost of advanced, high-performance refractories, especially compared to lower-cost alternatives from other regions, can also be a barrier to adoption for price-sensitive industries. While European refractories are often lauded for their superior quality and longer lifespan, the upfront investment can deter some buyers

- Overcoming these challenges through collaborative research and development, government support for sustainable technologies, and a clear demonstration of long-term cost benefits of advanced and sustainable refractories will be vital for sustained market growth

Europe Refractories Market Scope

The market is segmented on the basis of alkalinity, form type, product type, fusion temperature, application, and technology

- By Alkalinity

On the basis of alkalinity, the refractories market is segmented into Acidic & Neutral Refractories and Basic Refractories (Carbon). The Basic Refractories (Carbon) segment is anticipated to hold a significant market share, driven by their superior performance and increasing adoption in high-temperature applications within the steel and cement industries where basic slag conditions prevail. The Acidic & Neutral Refractories segment, while mature, continues to see steady demand, especially for applications requiring specific chemical resistance and high thermal shock resistance

- By Form Type

내화물 시장은 형태에 따라 벽돌, 일체형, 기타 로 구분됩니다 . 벽돌(성형 내화물) 부문은 현재 가장 큰 시장 매출 점유율을 차지하고 있으며, 구조적 무결성, 정밀한 치수, 다양한 산업용 용광로에서의 설치 용이성으로 명성을 얻고 있습니다. 산업 사용자들은 벽돌 내화물의 견고성과 긴 사용 수명을 우선시하는 경우가 많습니다. 또한, 다양한 용광로 설계와의 호환성과 광범위한 적용 범위로 인해 벽돌 유형에 대한 수요가 높습니다. 일체형(비성형) 내화물 부문은 유연성, 빠른 설치 시간, 그리고 이음매 없는 라이닝 형성 능력으로 인해 채택률이 증가함에 따라 가장 빠른 성장률을 보일 것으로 예상되며, 복잡하고 불규칙한 형태의 용광로 구역에 적합합니다. 적용의 용이성과 인건비 절감 또한 인기 증가에 기여합니다.

- 제품 유형별

내화물 시장은 제품 유형에 따라 점토 와 비점토로 구분됩니다 . 마그네시아, 알루미나, 실리카, 지르코니아 등의 소재를 포함하는 비점토 부문은 2024년 시장 매출 점유율이 가장 높았는데, 이는 초고온에서의 탁월한 성능과 다양한 부식 환경에 대한 내성 덕분입니다. 비점토 내화물은 철강 및 유리와 같은 산업의 핵심 응용 분야에 필수적입니다. 점토 부문은 특히 특정 킬른 라이닝 및 단열 내화물과 같이 우수한 단열성과 비용 효율성이 요구되는 분야에서 꾸준한 성장을 보일 것으로 예상됩니다.

- 퓨전 온도에 따라

내화물 시장은 용융 온도 기준으로 일반 내화물(1580~1780°C), 고내화물(1780~2000°C), 초내화물 (2000°C 이상) 로 구분됩니다 . 고내화물(1780~2000°C) 및 초내화물(2000°C 이상) 부문은 현대 산업 공정(예: 첨단 제강, 특수 세라믹)에서 더욱 극한의 작동 온도를 견딜 수 있는 내화물에 대한 수요가 증가함에 따라 상당한 성장을 보일 것으로 예상됩니다. 이러한 추세는 이러한 산업 분야에서 더 높은 효율과 생산량 증가를 추구하는 추세에 힘입은 것입니다. 일반 내화물(1580~1780°C) 부문은 일반 산업 분야에서 꾸준한 수요를 유지하고 있습니다 .

- 응용 프로그램별

내화물 시장은 용도별로 철강, 시멘트 및 석회, 에너지 및 화학, 유리, 비철금속 , 기타 로 구분됩니다 . 철강 부문은 2024년 시장 매출 점유율이 약 64.89% 로 가장 높았으며 , 고로 , 순산소로, 전기로 등 철강 생산의 다양한 단계에서 내화물이 광범위하게 사용됨에 따라 성장세를 보였습니다. 유리 및 비철금속 부문 은 고품질 유리 제품에 대한 수요 증가와 특수하고 내구성 있는 내화물 라이닝을 필요로 하는 비철금속 생산 확대로 인해 가장 빠른 연평균 성장률(CAGR)을 기록할 것으로 예상됩니다.

- 기술로

내화물 시장은 기술 기준으로 등압식과 슬라이드 게이트 로 구분됩니다 . 슬라이드 게이트 부문은 제강 공정에서 레이들과 턴디시에서 용탕의 흐름을 제어하는 데 중요한 역할을 하며, 정밀한 제어와 향상된 안전성을 제공함으로써 상당한 시장 점유율을 기록했습니다. 등압식 기술은 특히 연속 주조 공정 및 우수한 물성을 요구하는 특정 산업 분야에 사용되는 균일한 밀도와 강도를 가진 고성능 내화물 생산 분야에서 높은 성장세를 보일 것으로 예상됩니다.

유럽 내화물 시장 지역 분석

- 유럽은 잘 확립된 산업 기반과 기술 발전 및 지속 가능성에 대한 강력한 강조로 인해 글로벌 내화물 시장에서 상당한 점유율을 차지하고 있습니다(2024년 기준 약 14.2%).

- 이 지역의 산업은 고온 공정에서 장비 수명을 연장하고 에너지 소비와 배출량을 줄이는 데 중요한 역할을 하는 내화물을 높이 평가합니다.

- 이러한 광범위한 채택은 주요 산업 참여자의 존재, 현대화에 대한 지속적인 투자, 고성능 및 환경 친화적인 내화 솔루션에 대한 선호도 증가로 더욱 뒷받침되며 내화재는 지속 가능한 산업 생산을 위한 필수 구성 요소로 자리 잡았습니다.

독일 내화물 시장 통찰력

독일 내화물 시장은 유럽 내에서 상당한 매출 점유율을 차지했으며, 예측 기간 동안 상당한 연평균 성장률(CAGR)로 성장할 것으로 예상됩니다. 이러한 성장은 철강 및 자동차 산업을 중심으로 한 탄탄한 제조업 부문과 첨단 내화물의 이점에 대한 인식 제고에 힘입은 것입니다. 독일의 잘 발달된 산업 인프라는 혁신과 고품질 엔지니어링에 대한 강조와 결합하여, 특히 까다로운 응용 분야에서 정교한 내화물 솔루션 도입을 촉진하고 있습니다. 독일은 기술 선도와 지속 가능한 생산 방식에 중점을 두고 있어 최첨단 내화물에 대한 수요를 더욱 촉진하고 있습니다.

영국 내화물 시장 통찰력

영국 내화재 시장은 예측 기간 동안 주목할 만한 연평균 성장률(CAGR)로 성장할 것으로 예상됩니다. 이는 진행 중인 인프라 프로젝트, 철강 및 유리와 같은 주요 산업 부문에 대한 투자 재개, 그리고 운영 효율성 향상에 대한 요구 때문입니다. 또한, 영국의 변화하는 산업 환경과 첨단 제조 기술 도입에 대한 집중적인 노력은 고성능 내화재 사용을 촉진하고 있습니다. 영국의 기술 혁신 수용과 탄소 배출 감축 노력은 지속 가능한 내화 솔루션 시장 성장을 지속적으로 촉진할 것으로 예상됩니다.

러시아 내화물 시장 통찰력

러시아 내화물 시장은 2025년부터 2030년까지 연평균 성장률 7.5%로 유럽에서 가장 빠르게 성장하는 지역으로 예상되며, 2030년에는 39억 4,550만 달러에 이를 것으로 전망됩니다. 이러한 성장은 대규모 야금 및 중공업의 상당한 국내 수요와 이러한 부문의 지속적인 현대화 노력에 힘입은 것입니다. 러시아의 탄탄한 자원 기반과 세계 최고 수준의 조강 생산을 포함한 산업 개발에 대한 전략적 집중은 내화물 수요 증가에 크게 기여하고 있습니다. 산업 환경 전반의 고로 및 가마에 사용되는 내구성 있고 고성능의 라이닝에 대한 수요 증가는 러시아 시장 성장을 견인하는 핵심 요인입니다.

유럽 내화물 시장 점유율

유럽 내화물 산업은 주로 다음을 포함한 잘 확립된 회사들이 주도하고 있습니다.

- 알마티스 GmbH(독일)

- 이메리스(프랑스)

- RHI Magnesita GmbH(오스트리아)

- 생고뱅 퍼포먼스 세라믹스 & 내화재(PCR)(프랑스)

- 리프라테크닉(독일)

- Allied Mineral Products, Inc.(미국)

- ALTEO(프랑스)

- 쿠어스텍(미국)

- 하비슨워커 인터내셔널(미국)

- IFGL Refractories Ltd.(인도)

- 크로사키 하리마 주식회사(일본)

- 로이스트(벨기에)

- Magnezit 그룹(러시아)

- 미네랄스 테크놀로지스(미국)

- 모건 어드밴스드 머티리얼즈(영국)

- 푸양 내화 그룹 유한회사(중국)

- 시나가와 내화물 주식회사 (일본)

- VENUS Safety & Health Pvt. Ltd(인도)

- 베수비오산(영국)

- Wuxi Nanfang Refractories Co., Ltd. (중국)

글로벌 스마트 잠금 장치 시장의 최신 동향

- In June 2024, MIRECO (a joint venture of RHI Magnesita and Horn & Co. Group) acquired Refrattari Trezzi, an Italian refractory recycling specialist. This acquisition expands MIRECO's production footprint into Italy and represents a significant step towards the decarbonization targets of the European refractories industry by increasing the use of secondary raw materials and promoting the circular economy

- In October 2024, Shinagawa Refractories Co., Ltd. acquired Gouda Refractories Group B.V., a Netherlands-based manufacturer of high-alumina refractories and provider of refractory services. This acquisition strengthens Shinagawa's presence in Europe, providing it with state-of-the-art manufacturing for premium white refractories and high-value service capabilities in the region

- In April 2023, RHI Magnesita, a global leader in refractories, announced the acquisition of the Europe, India, and US operations of Seven Refractories. This strategic move complements RHI Magnesita's existing non-basic refractories portfolio and aims to open new opportunities in the development of low CO2 emitting manufacturing technologies, supporting sustainability goals in key customer industries like steel and cement

- In October 2023, RHI Magnesita also acquired the refractory businesses of the Preiss-Daimler Group ("P-D Refractories") located in Germany, the Czech Republic, and Slovenia. This acquisition enhances RHI Magnesita's capabilities in alumina-based refractories and strengthens its presence in process industries, where the Group is currently under-represented

- In 2022, RHI Magnesita and the Horn & Co. Group combined their recycling activities in Europe to increase the production, use, and supply of secondary raw materials for the European refractory industry, targeting a substantial reduction of CO2 emissions. This initiative underscores the industry's commitment to sustainability and circular economy principles

- The ATHOR and CESAREF projects are ongoing collaborative and interdisciplinary initiatives in Europe, bringing together academic and industrial partners. These projects, funded by programs like Horizon Europe, focus on developing advanced thermomechanical modelling of refractory linings, optimizing the use of mineral resources, recycling, anticipating the use of hydrogen in steelmaking, and improving energy efficiency and durability of refractories. These collaborations aim to shape the future of refractory technology and contribute to the decarbonization of European energy-intensive industries

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.