Europe Wheat Gluten Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

489.63 Million

USD

865.11 Million

2021

2029

USD

489.63 Million

USD

865.11 Million

2021

2029

| 2022 –2029 | |

| USD 489.63 Million | |

| USD 865.11 Million | |

| % | |

Europe Wheat Gluten Market, By Category (Organic and Inorganic), Function (Emulsifier, Solidifier, Binder and Others), Form (Liquid and Dry), Application (Food & Beverages, Animal Feed and Others), Packaging (Bottle/Jar, Pouch & Bags, Boxes and Others), Distribution Channel (Store Based Retailers and Non-Store Based Retailers), End User (Household/Retail and Commercial) -Industry Trends and Forecast to 2029.

Europe Wheat Gluten Market Analysis and Insights

Europe wheat gluten market is growing in the forecast year due to the rise in market players and the availability of various plant-based meat alternatives in the market. Along with this, the number of R&D activities to find out new plant-based proteins has increased in the market which is further boosting the market growth. However, the rising cases of hereditary and chronic disorders due to gluten intolerance might hamper the market growth in the forecast period.

Growing awareness regarding the benefits of plant-based proteins, rising demand for organic products and initiatives by market players are giving opportunities to the market. However, the increased cost of production and manufacturing, gluten sensitivity and autoimmune reactions in people are the key challenges to market growth.

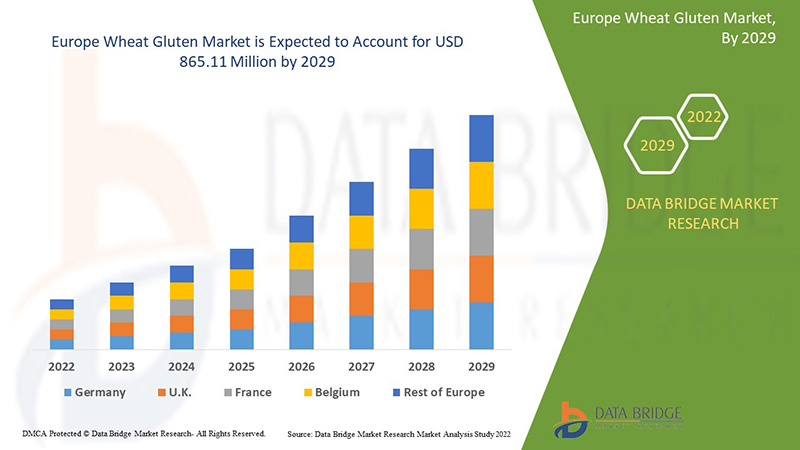

Europe wheat gluten market is expected to gain market growth in the forecast period of 2022 to 2029. Data Bridge Market Research analyzes that the market is growing with a CAGR of 7.6% in the forecast period of 2022 to 2029 and is expected to reach USD 865.11 million by 2029 from USD 489.63 million in 2021.

|

Report Metric |

Details |

|

Forecast Period |

2022 to 2029 |

|

Base Year |

2021 |

|

Historic Year |

2020 (Customisable to 2014-2019) |

|

Quantitative Units |

Revenue in USD Million |

|

Segments Covered |

By Category (Organic and Inorganic), Function (Emulsifier, Solidifier, Binder and Others), Form (Liquid and Dry), Application (Food & Beverages, Animal Feed and Others), Packaging (Bottle/Jar, Pouch & Bags, Boxes and Others), Distribution Channel (Store Based Retailers and Non-Store Based Retailers), End User (Household/Retail and Commercial) |

|

Countries Covered |

Germany, France, U.K., Italy, Spain, Netherlands, Russia, Denmark, Sweden, Poland, Switzerland, Turkey, Sweden and rest of Europe |

|

Market Players Covered |

Cargill, Incorporated, ADM, Crespel & Deiters Group, Glico Nutrition Co., Ltd., Sedamyl, Manildra Group, MGP, Roquette Frères, CropEnergies AG, Anhui Ante Food Co., Ltd., ARDENT MILLS, Bryan W Nash and Sons, Pioneer Industries Private Limited, Henan Tianguan Group Co. Ltd, Permolex, Meelunie B.V., Mühlenchemie GmbH & Co. KG, Royal Ingredients Group, Kröner Stärke and z&f sungold corporation among others |

Market Definition

Wheat gluten is also known as seitan, wheat meat, gluten meat, or gluten. Wheat gluten is a protein that occurs naturally in wheat or wheat flour. It is made by washing wheat flour dough in water until all of the starch granules are removed. Wheat gluten powder is made by hydrating hard wheat flour to activate the gluten. After that, the hydrated mass is processed to remove starch while leaving gluten behind. Finally, the gluten is dried and ground into powder. Some gluten varieties have a stringy or chewy texture similar to meat.

Europe Wheat Gluten Market Dynamics

Drivers

- Rising vegan population and increasing demand for meat alternatives

Gluten is a protein found naturally in some grains like wheat, barley and rye. Wheat glutens are made up of Gliadins and Glutenin protein fractions. Gliadins contain a single polypeptide chain associated with hydrogen bonds, hydrophobic bonds and intra-molecular disulfide interactions whereas Glutenins contain inter-molecular disulfide interactions. Wheat gluten and wheat starch are economically important co-products produced during the wet processing of wheat flour. Wheat gluten is a commodity food ingredient and its applications are predominantly in baked goods and processed meat products. It has unique properties such as, when it is hydrated and mixed, it forms a very extensible, elastic structure that is responsible for the gas-holding ability of bread dough. It can be used in combination with wheat flour and other additives to produce a soy-free texturized product.

The vegan population is increasing worldwide and the demand for meat alternatives is also increasing. People are more aware of the health benefits of plant-based proteins and getting shifted to vegan lifestyles where wheat gluten can act as a meat alternative for them.

- Rising preference of consumers toward high protein-rich diets

Most consumers prefer high-protein-rich diets due to several reasons. A few of them are: protein is the building block of the human body and muscles; it is vital for body and brain activities; it is important for healthy and active living. Gluten is one of the high protein-rich diets which can be extracted from wheat. Gluten has high protein content along with vitamins & minerals such as antioxidants, fiber, vitamin B, vitamin E, magnesium, iron, folic acid and others.

Furthermore, in recent years, high protein diets and products have made a real impression on nutrition and reshaped consumers’ attitudes towards protein in their food intake as adequate nutrition is an important aspect of a healthy lifestyle for all individuals. Various studies have shown the health benefits of plant-based proteins and public awareness has increased to a greater extent. As a result, consumers are preferring high protein-rich diets.

- Rising number of R&D activities to find out new plant-based proteins

The demand for high protein-rich diets is increasing among people and hence, the number of research has increased to find out proteins. As animal-based proteins are causing most health hazards, people are getting shifted to vegan lifestyles gradually, across the globe. Plant-based proteins are rich in vitamins as well as minerals and have great health benefits as per recent studies. Wheat gluten is one of the plant proteins which is used as a meat alternative and a protein-rich diet by most people worldwide.

Most of the human population is preferring high-protein diets from plant sources due to several health benefits and to overcome diseases caused by the intake of animal-based protein diets. So, the number of R&D is increasing to find out new plant-based proteins in various ways to fulfill the demand.

Opportunities

-

Growing awareness regarding the benefits of plant-based proteins

Various plant-based protein products are available in the market due to changing taste preferences of consumers. One of them is wheat gluten and its products which are in high demand. The plant-based protein market such as wheat gluten is having a strong demand and growth in bakeries, functional beverages and other food. The plant-based proteins are easily available due to their wide usage in various industries. Wheat gluten is used in various products such as animal feed products that help to minimize the farmers' dependence on traditional sources of protein. Wheat gluten and plant-based protein products include several nutrients and are infused with protein and flavors. Increasing awareness about healthy lifestyles and weight loss management, along with the demand for plant-based protein bars among consumers.

As a result, the need for wheat gluten in various products will act as an opportunity for market growth. Meanwhile, wheat gluten is used in carbonated products to enhance the added flavors.

-

Rising demand for organic products

The demand for organic products is increasing at a high speed. Organic food ingredients such as plant-based proteins are a perfect protein alternative to meat or other non-vegetarian products that consumers can consume daily. All essential amino acids and high fibers present in organic products make them an ideal substitute for animal proteins.

The demand for organic ingredients in wheat gluten and its products is due to nutritional diet plans as they have various health benefits such as low diabetes risk, easy digestibility, cardiovascular health and others. The increasing awareness among consumers about the health benefits offered by organic ingredients such as plant-based proteins increased the demand for food and beverage products.

Restraints/Challenges

- Increased cost of production and manufacturing

Wheat gluten has opened doors to improve and support health which plays a major role in the food and beverages industry. But on the other hand, it has led to major costs involved in its production and manufacturing

In some countries around the world, wheat gluten is seen as a solution to the problem of maintaining a healthy lifestyle. However, its manufacturing and production are faced with a multitude of challenges such as staff-intensive labor, increasing amount of raw materials and the need for faster production due to increased demand. These demands need to be met effectively and efficiently. Wheat gluten involves a high capital investment to maintain R&D. The new machinery and equipment include a lot of trials to test the functioning which leads to high capital investments for small and medium enterprises.

- Rising cases of hereditary and chronic disorders due to gluten intolerance

Gluten is a type of protein extracted from wheat and other grains. There are so many cases where gluten intolerance has been found. There are several potential causes of gluten intolerance, including celiac disease, non-celiac gluten sensitivity and wheat allergy. All three forms of gluten intolerance can cause widespread symptoms. Celiac disease is the most severe form of gluten intolerance. It is an autoimmune disease that affects about 1% of the population and may lead to damage to the digestive system. It can cause a wide range of symptoms, including skin problems, gastrointestinal issues, mood changes and more. The common symptoms associated with non-celiac disease are bloating, headache, stomach pain, fatigue, diarrhea and constipation among others. Similarly, the symptoms associated with wheat allergy are skin rash, digestive issues, nasal congestion and anaphylaxis among others.

Due to the impact of gluten intolerance, several disorders including celiac, non-celiac and wheat allergies are being caused which are chronic and hereditary in some cases.

Post-COVID-19 Impact on Europe Wheat Gluten Market

COVID-19 had negatively affected the Europe wheat gluten market. Lockdowns and isolation during the pandemic caused the closure of most of the shops and the plant-based protein diet supply was affected to a higher extent. Online purchases of plant-based meat alternatives had increased. Thus, COVID-19 affected the market negatively.

Recent Developments

- In October 2022, Crespel & Deiters Group presented innovative extrudates, wheat starches and functional blends for improved meat products and meat alternatives. Its presence at the show, which is dedicated to the meat and alternative proteins market, presents new, sustainable and economical options for the production of meat products or vegan and vegetarian products based on functional wheat ingredients. These include the innovative texturates of the Lory Tex range for hybrid and plant-based alternatives, as well as hydrolyzed wheat protein. This has helped the company to increase its Europe presence in the market.

- In September 2021, Roquette Freres announced the opening of a center expertise of 2,000 square meters on its site in Vic-Sur-Aisne, France. This center can enlarge the field of possibilities in terms of food innovation, new protein development and new production technologies. Thus, it has helped the company to establish itself globally.

Europe Wheat Gluten Market Scope

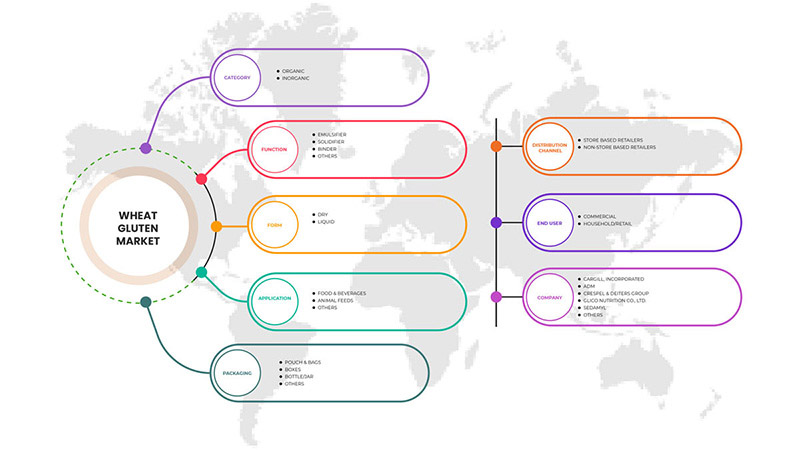

Europe wheat gluten market is segmented into seven notable segments based on category, function, form, application, packaging, distribution channel and end user. The growth amongst these segments will help you analyze meager growth segments in the industries and provide the users with a valuable market overview and market insights to make strategic decisions to identify core market applications.

By Category

- Organic

- Inorganic

Based on category, the market is segmented into organic and inorganic.

By Function

- Emulsifier

- Solidifier

- Binder

- Others

Based on function, the market is segmented into emulsifier, solidifier, binder and others.

By Form

- Liquid

- Dry

Based on form, the market is segmented into liquid and dry.

By Application

- Food & Beverages

- Animal Feed

- Others

Based on application, the market is segmented into food & beverages, animal feed and others.

By Packaging

- Bottle/Jar

- Pouch & Bags

- Boxes

- Others

Based on packaging, the market is segmented into bottle/jar, pouch & bags, boxes and others.

By Distribution Channel

- Store Based Retailers

- Non-Store Based Retailers

Based on distribution channel, the market is segmented into store based retailers and non-store based retailers.

By End User

- Household/Retail

- Commercial

Based on end user, the market is segmented into household/retail and commercial.

Europe Wheat Gluten Market Regional Analysis/Insights

Europe wheat gluten market is analyzed and market size insights and trends are provided by country, category, function, form, application, packaging, distribution channel and end user.

Europe wheat gluten market comprises of the countries Germany, France, U.K., Italy, Spain, Netherlands, Russia, Denmark, Sweden, Poland, Switzerland, Turkey, Sweden and rest of Europe.

France dominates the Europe wheat gluten market in terms of market share and market revenue and will continue to flourish its dominance during the forecast period.

The growing awareness regarding the benefits of plant-based proteins is further fuelling the market growth. Moreover, the rising demand for organic products and initiatives by market players is also boosting market growth.

Competitive Landscape and Europe Wheat Gluten Market Share Analysis

Europe wheat gluten market competitive landscape provides details by the competitors. Details included are company overview, company financials, revenue generated, market potential, investment in R&D, new market initiatives, Europe presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth and application dominance. The above data points provided are only related to the companies’ focus on the market.

Some of the major players operating in the Europe wheat gluten market are Cargill, Incorporated, ADM, Crespel & Deiters Group, Glico Nutrition Co., Ltd., Sedamyl, Manildra Group, MGP, Roquette Frères, CropEnergies AG, Anhui Ante Food Co., Ltd., ARDENT MILLS, Bryan W Nash and Sons, Pioneer Industries Private Limited, Henan Tianguan Group Co. Ltd, Permolex, Meelunie B.V., Mühlenchemie GmbH & Co. KG, Royal Ingredients Group, Kröner Stärke and z&f sungold corporation among others.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The market data is analyzed and estimated using market statistical and coherent models. In addition, market share analysis and key trend analysis are the major success factors in the market report. The key research methodology used by the DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Apart from this, data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Company Market Share Analysis, Standards of Measurement, Europe vs. Regional and Vendor Share Analysis. Please request an analyst call in case of further inquiry.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors as you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

목차

1 서론

1.1 연구 목적

1.2 시장 정의

1.3 유럽 밀 글루텐 시장 개요

1.4 제한 사항

1.5 대상 시장

2 시장 세분화

2.1 대상 시장

2.2 지리적 범위

연구에 2.3년이 고려됨

2.4 통화 및 가격

2.5 DBMR TRIPOD 데이터 검증 모델

2.6 다변량 모델링

2.7 범주 수명선 곡선

2.8 주요 여론 선도자와의 1차 인터뷰

2.9 DBMR 시장 위치 그리드

2.1 시장 적용 범위 그리드

2.11 공급업체 점유율 분석

2.12 2차 소스

2.13 가정

3 요약

4가지 프리미엄 인사이트

4.1 유럽 밀 글루텐 시장의 특허 분석

4.2 소비자 구매 행동

4.3 브랜드 분석

4.4 유럽 밀 글루텐 시장 공급망 분석

4.4.1 원자재 조달

4.4.2 제조

4.4.3 운송 또는 물류

4.4.4 마케팅 및 유통

4.4.5 최종 사용자

4.5 유럽 밀 글루텐 시장 향후 기술 및 동향

4.5.1 밀의 글루텐에 대한 CRISPR/CAS9 유전자 편집

4.5.2 밀 글루텐의 RNA 간섭

4.5.3 콜드 에탄올 기술

5 규제 프레임워크

5.1 식품의약품안전처

5.1.1 알레르겐 표시에 관한 규정

5.2 유럽 연합(EU)

5.3 인도의 규정

5.3.1 FSSAI는 글루텐 및 비글루텐 식품과 관련된 표준을 제안합니다.

5.4 중국의 규정

5.5 미국 규정

5.6 캐나다의 규정

5.7 태국의 규정

6 시장 개요

6.1 드라이버

6.1.1 채식주의 인구 증가 및 육류 대체 식품에 대한 수요 증가

6.1.2 고단백질 식단에 대한 소비자들의 선호도 증가

6.1.3 새로운 식물성 단백질을 찾기 위한 연구 및 개발 활동 증가

6.2 제약

6.2.1 글루텐 불내증으로 인한 유전성 및 만성 질환의 증가

6.2.2 식물성 단백질의 높은 비용

6.3 기회

6.3.1 식물성 단백질의 이점에 대한 인식 증가

6.3.2 유기농 제품에 대한 수요 증가

6.3.3 시장 참여자의 이니셔티브

6.4 과제

6.4.1 생산 및 제조 비용 증가

6.4.2 질병 유병률 증가

6.4.3 사람들의 글루텐 민감성 및 자가면역 반응

7 유럽 밀 글루텐 시장, 카테고리별

7.1 개요

7.2 유기농

7.3 무기물

8 유럽 밀 글루텐 시장, 기능별

8.1 개요

8.2 바인더

8.3 유화제

8.4 솔리디파이어

8.5 기타

9 유럽 밀 글루텐, 형태별

9.1 개요

9.2 건조

9.3 액체

10 유럽 밀 글루텐 시장, 용도별

10.1 개요

10.2 음식 및 음료

10.2.1 제빵 및 제과 제품

10.2.1.1 케이크, 머핀 및 도넛

10.2.1.2 빵

10.2.1.3 쿠키, 크래커

10.2.1.4 파이 크러스트 및 피자 반죽

10.2.1.5 배터리

10.2.1.6 기타

10.2.2 편의식품

10.2.2.1 국수와 파스타

10.2.2.2 수프 & 소스

10.2.2.3 조미료 및 드레싱

10.2.2.4 스낵 및 압출 스낵

10.2.2.5 바로 먹을 수 있는 식사

10.2.2.6 기타

10.2.3 육류 유사품

10.2.4 스포츠 영양

10.2.5 아침 시리얼

10.2.6 육류 및 가금류 제품

10.2.7 영양바

10.2.8 음료

10.2.9 기타

10.3 동물사료

10.3.1 애완동물 사료

10.3.2 반추동물

10.3.3 돼지

10.3.4 가금류

10.3.5 기타

10.4 기타

11 유럽 밀 글루텐 시장, 포장별

11.1 개요

11.2 파우치 & 백

11.3 상자

11.4 병/항아리

11.4.1 플라스틱

11.4.2 유리

11.4.3 금속

11.4.4 종이

11.5 기타

12 유럽 밀 글루텐 시장, 유통 채널별

12.1 개요

12.2 매장 기반 소매업체

12.2.1 하이퍼마켓/슈퍼마켓

12.2.2 편의점

12.2.3 식료품점

12.2.4 특수 매장

12.2.5 기타

12.3 매장 기반이 아닌 소매업체

13 최종 사용자별 유럽 밀 글루텐 시장

13.1 개요

13.2 상업적

13.2.1 제과점

13.2.2 레스토랑 및 카페

13.2.3 호텔

13.2.4 클라우드 키친

13.2.5 기타

13.3 가정/소매

14 유럽 밀 글루텐 시장, 지역별

14.1 유럽

14.1.1 프랑스

14.1.2 영국

14.1.3 독일

14.1.4 네덜란드

14.1.5 벨기에

14.1.6 스페인

14.1.7 이탈리아

14.1.8 덴마크

14.1.9 스웨덴

14.1.10 러시아

14.1.11 스위스

14.1.12 폴란드

14.1.13 터키

14.1.14 유럽의 나머지 지역

15 유럽 밀 글루텐 시장: 회사 환경

15.1 회사 점유율 분석: 유럽

16 SWOT 분석

17 회사 프로필

17.1 카길 주식회사

17.1.1 회사 스냅샷

17.1.2 회사 점유율 분석

17.1.3 제품 포트폴리오

17.1.4 최근 개발

17.2 ADM

17.2.1 회사 스냅샷

17.2.2 수익 분석

17.2.3 회사 점유율 분석

17.2.4 제품 포트폴리오

17.2.5 최근 개발

17.3 크레스펠 & 다이터스 그룹

17.3.1 회사 스냅샷

17.3.2 회사 점유율 분석

17.3.3 제품 포트폴리오

17.3.4 최근 개발

17.4 글리코뉴트리션(주)

17.4.1 회사 스냅샷

17.4.2 회사 점유율 분석

17.4.3 제품 포트폴리오

17.4.4 최근 개발

17.5 세다밀

17.5.1 회사 스냅샷

17.5.2 제품 포트폴리오

17.5.3 최근 개발

17.6 안휘 안터 식품 유한회사

17.6.1 회사 스냅샷

17.6.2 제품 포트폴리오

17.6.3 최근 개발

17.7 아르덴트 밀스

17.7.1 회사 스냅샷

17.7.2 제품 포트폴리오

17.7.3 최근 개발 사항

17.8 브라이언 W 내쉬 앤 선즈

17.8.1 회사 스냅샷

17.8.2 제품 포트폴리오

17.8.3 최근 개발

17.9 크롭너지스 AG

17.9.1 회사 스냅샷

17.9.2 수익 분석

17.9.3 제품 포트폴리오

17.9.4 최근 개발

17.1 허난 티안 관 그룹 유한회사

17.10.1 회사 스냅샷

17.10.2 제품 포트폴리오

17.10.3 최근 개발

17.11 크뢰너-슈테르케 GMBH

17.11.1 회사 스냅샷

17.11.2 제품 포트폴리오

17.11.3 최근 개발

17.12 마닐라 그룹

17.12.1 회사 스냅샷

17.12.2 제품 포트폴리오

17.12.3 최근 개발

17.13 밀루니 BV

17.13.1 회사 스냅샷

17.13.2 제품 포트폴리오

17.13.3 최근 개발

17.14 밀리그램

17.14.1 회사 스냅샷

17.14.2 수익 분석

17.14.3 제품 포트폴리오

17.14.4 최근 개발

17.15 MUHLENCHEMIE GMBH & CO. KG

17.15.1 회사 스냅샷

17.15.2 제품 포트폴리오

17.15.3 최근 개발

17.16 퍼몰렉스

17.16.1 회사 스냅샷

17.16.2 제품 포트폴리오

17.16.3 최근 개발

17.17 파이오니어 인더스트리스 프라이빗 리미티드

17.17.1 회사 스냅샷

17.17.2 제품 포트폴리오

17.17.3 최근 개발

17.18 로케트 프레르

17.18.1 회사 스냅샷

17.18.2 제품 포트폴리오

17.18.3 최근 개발

17.19 로얄 인그리디언트 그룹

17.19.1 회사 스냅샷

17.19.2 제품 포트폴리오

17.19.3 최근 개발

17.2 Z&F SUNGOLD CORPORATION

17.20.1 회사 스냅샷

17.20.2 제품 포트폴리오

17.20.3 최근 개발

18 설문지

19 관련 보고서

표 목록

표 1 유럽 밀 글루텐 시장, 범주별, 2020-2029년(백만 달러)

표 2 유럽 유기농 밀 글루텐 시장, 지역별, 2020-2029 (백만 달러)

표 3 유럽의 밀 글루텐 무기질 시장, 지역별, 2020-2029 (백만 달러)

표 4 기능별 유럽 밀 글루텐 시장, 2020-2029년(백만 달러)

표 5 유럽 밀 글루텐 시장 바인더, 지역별, 2020-2029 (백만 달러)

표 6 유럽 밀 글루텐 시장의 유화제, 지역별, 2020-2029 (백만 달러)

표 7 유럽 지역별 밀 글루텐 시장의 고형화제, 2020-2029년(백만 달러)

표 8 유럽 기타 지역별 밀 글루텐 시장, 2020-2029년(백만 달러)

표 9 유럽 밀 글루텐 시장, 형태별, 2020-2029 (백만 달러)

표 10 유럽의 밀 글루텐 시장(지역별), 2020-2029(백만 달러)

표 11 유럽 지역별 밀 글루텐 시장 액체, 2020-2029년(백만 달러)

표 12 유럽 밀 글루텐 시장, 응용 분야, 2020-2029 (백만 달러)

표 13 지역별 유럽 식품 및 음료 밀 글루텐 시장, 2020-2029 (백만 달러)

표 14 유럽 제빵 및 제과 제품, 밀 글루텐 시장, 응용 분야별, 2020-2029년(백만 달러)

표 15 유럽 편의식품 시장(밀 글루텐, 응용 분야별), 2020-2029(백만 달러)

표 16 유럽 동물 사료 시장(지역별) 밀 글루텐 시장, 2020-2029년(백만 달러)

표 17 유럽 동물 사료 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 18 유럽 기타 지역별 밀 글루텐 시장, 2020-2029년(백만 달러)

표 19 유럽 밀 글루텐 시장, 포장 기준, 2020-2029 (백만 달러)

표 20 유럽 파우치 및 백 밀 글루텐 시장, 지역별, 2020-2029 (백만 달러)

표 21 유럽 상자별 밀 글루텐 시장, 지역별, 2020-2029 (백만 달러)

표 22 유럽 밀 글루텐 시장 병/병, 지역별, 2020-2029 (백만 달러)

표 23 유럽 밀 글루텐 병/병 시장, 포장 기준, 2020-2029 (백만 달러)

표 24 유럽 기타 지역별 밀 글루텐 시장, 2020-2029 (백만 달러)

표 25 유럽 밀 글루텐 시장, 유통 채널 2020-2029 (백만 달러)

표 26 지역별 밀 글루텐 시장의 유럽 매장 기반 소매업체, 2020-2029년(백만 달러)

표 27 유통 채널별 밀 글루텐 시장의 유럽 매장 기반 소매업체, 2020-2029년(백만 달러)

표 28 유럽 비매장 기반 소매업체, 지역별 밀 글루텐 시장, 2020-2029 (백만 달러)

표 29 최종 사용자별 유럽 밀 글루텐 시장, 2020-2029년(백만 달러)

표 30 유럽 밀 글루텐 시장, 지역별, 2020-2029 (백만 달러)

표 31 최종 사용자별 유럽 밀 글루텐 시장 거래량, 2020-2029년(백만 달러)

표 32 지역별 유럽 가정/소매 밀 글루텐 시장, 2020-2029년(백만 달러)

표 33 국가별 유럽 밀 글루텐 시장, 2020-2029년(백만 달러)

표 34 유럽 밀 글루텐 시장, 범주별, 2020-2029 (백만 달러)

표 35 기능별 유럽 밀 글루텐 시장, 2020-2029년(백만 달러)

표 36 유럽 밀 글루텐 시장, 형태별, 2020-2029 (백만 달러)

표 37 유럽 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 38 유럽 식품 및 음료, 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 39 유럽 제빵 및 제과 제품, 밀 글루텐 시장, 응용 분야별, 2020-2029년(백만 달러)

표 40 유럽 편의식품 시장(밀 글루텐 시장, 응용 분야별, 2020-2029년, 백만 달러)

표 41 유럽 동물 사료 시장(밀 글루텐, 용도별), 2020-2029(백만 달러)

표 42 유럽 밀 글루텐 시장, 포장 기준, 2020-2029 (백만 달러)

표 43 유럽 밀 글루텐 병/병 시장, 포장 기준, 2020-2029년(백만 달러)

표 44 유럽 밀 글루텐 시장, 유통 채널별, 2020-2029년(백만 달러)

표 45 유통 채널별 밀 글루텐 시장의 유럽 매장 기반 소매업체, 2020-2029년(백만 달러)

표 46 최종 사용자별 유럽 밀 글루텐 시장, 2020-2029년(백만 달러)

표 47 최종 사용자별 유럽 밀 글루텐 시장 거래량, 2020-2029년(백만 달러)

표 48 프랑스 밀 글루텐 시장, 카테고리별, 2020-2029 (백만 달러)

표 49 프랑스 밀 글루텐 시장, 기능별, 2020-2029 (백만 달러)

표 50 프랑스 밀 글루텐 시장, 형태별, 2020-2029 (백만 달러)

표 51 프랑스 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 52 프랑스 식품 및 음료, 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 53 2020-2029년 응용 분야별 밀 글루텐 시장의 프랑스 제빵 및 제과 제품(백만 달러)

표 54 2020-2029년 응용 분야별 프랑스 편의식품 밀 글루텐 시장(백만 달러)

표 55 프랑스 밀 글루텐 사료 시장, 용도별, 2020-2029 (백만 달러)

표 56 프랑스 밀 글루텐 시장, 포장 기준, 2020-2029 (백만 달러)

표 57 프랑스 밀 글루텐 병/항아리 시장, 포장별, 2020-2029년(백만 달러)

표 58 프랑스 밀 글루텐 시장, 유통 채널별, 2020-2029년(백만 달러)

표 59 유통 채널별 밀 글루텐 시장의 프랑스 매장 기반 소매업체, 2020-2029년(백만 달러)

표 60 최종 사용자별 프랑스 밀 글루텐 시장, 2020-2029년(백만 달러)

표 61 최종 사용자별 프랑스 밀 글루텐 시장 상업적 규모, 2020-2029년(백만 달러)

표 62 영국 밀 글루텐 시장, 범주별, 2020-2029년(백만 달러)

표 63 영국 밀 글루텐 시장, 기능별, 2020-2029 (백만 달러)

표 64 영국 밀 글루텐 시장, 형태별, 2020-2029 (백만 달러)

표 65 영국 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 66 2020-2029년 응용 분야별 밀 글루텐 시장의 영국 식품 및 음료(백만 달러)

표 67 영국 제빵 및 제과 제품, 밀 글루텐 시장, 응용 분야별, 2020-2029년(백만 달러)

표 68 영국 편의식품의 밀 글루텐 시장, 응용 분야별, 2020-2029년(백만 달러)

표 69 2020-2029년 응용 분야별 영국 밀 글루텐 사료 시장(백만 달러)

표 70 영국 밀 글루텐 시장, 포장 기준, 2020-2029 (백만 달러)

표 71 영국 밀 글루텐 병/항아리 시장, 포장 기준, 2020-2029년(백만 달러)

표 72 영국 밀 글루텐 시장, 유통 채널별, 2020-2029년(백만 달러)

표 73 유통 채널별 밀 글루텐 시장의 영국 매장 기반 소매업체, 2020-2029년(백만 달러)

표 74 최종 사용자별 영국 밀 글루텐 시장, 2020-2029년(백만 달러)

표 75 최종 사용자별 영국 밀 글루텐 시장 상업화, 2020-2029년(백만 달러)

표 76 독일 밀 글루텐 시장, 카테고리별, 2020-2029 (백만 달러)

표 77 독일 밀 글루텐 시장, 기능별, 2020-2029 (백만 달러)

표 78 독일 밀 글루텐 시장, 형태별, 2020-2029 (백만 달러)

표 79 독일 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 80 독일 식품 및 음료, 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 81 2020-2029년 응용 분야별 밀 글루텐 시장의 독일 제빵 및 제과 제품(백만 달러)

표 82 독일 편의식품 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 83 독일 밀 글루텐 시장의 동물 사료, 응용 분야별, 2020-2029 (백만 달러)

표 84 독일 밀 글루텐 시장, 포장 기준, 2020-2029 (백만 달러)

표 85 독일 밀 글루텐 시장의 병/항아리, 포장 기준, 2020-2029년(백만 달러)

표 86 독일 밀 글루텐 시장, 유통 채널별, 2020-2029년(백만 달러)

표 87 유통 채널별 밀 글루텐 시장의 독일 매장 기반 소매업체, 2020-2029년(백만 달러)

표 88 최종 사용자별 독일 밀 글루텐 시장, 2020-2029년(백만 달러)

표 89 최종 사용자별 독일 밀 글루텐 시장 상업적 규모, 2020-2029년(백만 달러)

표 90 네덜란드 밀 글루텐 시장, 범주별, 2020-2029년(백만 달러)

표 91 네덜란드 밀 글루텐 시장, 기능별, 2020-2029 (백만 달러)

표 92 네덜란드 밀 글루텐 시장, 형태별, 2020-2029 (백만 달러)

표 93 네덜란드 밀 글루텐 시장, 용도별, 2020-2029년(백만 달러)

표 94 2020-2029년 응용 분야별 밀 글루텐 시장의 네덜란드 식품 및 음료(백만 달러)

표 95 2020-2029년 응용 분야별 밀 글루텐 시장의 네덜란드 제빵 및 제과 제품(백만 달러)

표 96 2020-2029년 응용 분야별 네덜란드 편의 식품 밀 글루텐 시장(백만 달러)

표 97 2020-2029년 응용 분야별 네덜란드 밀 글루텐 사료 시장(백만 달러)

표 98 네덜란드 밀 글루텐 시장, 포장 기준, 2020-2029 (백만 달러)

표 99 네덜란드 밀 글루텐 병/항아리 시장, 포장 기준, 2020-2029년(백만 달러)

표 100 네덜란드 밀 글루텐 시장, 유통 채널별, 2020-2029년(백만 달러)

표 101 유통 채널별 밀 글루텐 시장의 네덜란드 매장 기반 소매업체, 2020-2029년(백만 달러)

표 102 최종 사용자별 네덜란드 밀 글루텐 시장, 2020-2029년(백만 달러)

표 103 최종 사용자별 네덜란드 밀 글루텐 시장 상업적 규모, 2020-2029년(백만 달러)

표 104 벨기에 밀 글루텐 시장, 범주별, 2020-2029년(백만 달러)

표 105 벨기에 밀 글루텐 시장, 기능별, 2020-2029 (백만 달러)

표 106 벨기에 밀 글루텐 시장, 형태별, 2020-2029 (백만 달러)

표 107 벨기에 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 108 벨기에 밀 글루텐 시장의 식품 및 음료, 응용 분야별, 2020-2029 (백만 달러)

표 109 벨기에 제빵 및 제과 제품, 밀 글루텐 시장, 응용 분야별, 2020-2029년(백만 달러)

표 110 벨기에 편의식품의 밀 글루텐 시장, 응용 분야별, 2020-2029년(백만 달러)

표 111 벨기에의 밀 글루텐 시장 내 동물 사료, 응용 분야별, 2020-2029년(백만 달러)

표 112 벨기에 밀 글루텐 시장, 포장 기준, 2020-2029 (백만 달러)

표 113 벨기에 밀 글루텐 시장 병/항아리, 포장 기준, 2020-2029년(백만 달러)

표 114 벨기에 밀 글루텐 시장, 유통 채널별, 2020-2029년(백만 달러)

표 115 유통 채널별 밀 글루텐 시장의 벨기에 매장 기반 소매업체, 2020-2029년(백만 달러)

표 116 최종 사용자별 벨기에 밀 글루텐 시장, 2020-2029년(백만 달러)

표 117 벨기에의 밀 글루텐 시장 상업적 규모, 최종 사용자별, 2020-2029년(백만 달러)

표 118 스페인 밀 글루텐 시장, 카테고리별, 2020-2029 (백만 달러)

표 119 스페인 밀 글루텐 시장, 기능별, 2020-2029 (백만 달러)

표 120 스페인 밀 글루텐 시장, 형태별, 2020-2029 (백만 달러)

표 121 스페인 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 122 스페인 밀 글루텐 시장의 식품 및 음료, 응용 분야별, 2020-2029 (백만 달러)

표 123 스페인 제빵 및 제과 제품, 밀 글루텐 시장, 응용 분야별, 2020-2029년(백만 달러)

표 124 스페인 편의식품 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 125 스페인 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 126 스페인 밀 글루텐 시장, 포장 기준, 2020-2029 (백만 달러)

표 127 스페인 병/항아리 밀 글루텐 시장, 포장 기준, 2020-2029년(백만 달러)

표 128 스페인 밀 글루텐 시장, 유통 채널별, 2020-2029년(백만 달러)

표 129 유통 채널별 밀 글루텐 시장의 스페인 매장 기반 소매업체, 2020-2029년(백만 달러)

표 130 스페인 밀 글루텐 시장, 최종 사용자별, 2020-2029(백만 달러)

표 131 스페인의 밀 글루텐 시장 상업적 규모, 최종 사용자별, 2020-2029년(백만 달러)

표 132 이탈리아 밀 글루텐 시장, 카테고리별, 2020-2029 (백만 달러)

표 133 이탈리아 밀 글루텐 시장, 기능별, 2020-2029 (백만 달러)

표 134 이탈리아 밀 글루텐 시장, 형태별, 2020-2029 (백만 달러)

표 135 이탈리아 밀 글루텐 시장, 용도별, 2020-2029 (백만 달러)

표 136 2020-2029년 응용 분야별 밀 글루텐 시장의 이탈리아 식품 및 음료(백만 달러)

표 137 2020-2029년 응용 분야별 밀 글루텐 시장의 이탈리아 제빵 및 제과 제품(백만 달러)

표 138 2020-2029년 응용 분야별 이탈리아 편의 식품 밀 글루텐 시장(백만 달러)

표 139 2020-2029년 용도별 이탈리아 밀 글루텐 사료 시장(백만 달러)

표 140 이탈리아 밀 글루텐 시장, 포장 기준, 2020-2029 (백만 달러)

표 141 이탈리아 밀 글루텐 시장 병/항아리, 포장별, 2020-2029년(백만 달러)

표 142 이탈리아 밀 글루텐 시장, 유통 채널별, 2020-2029년(백만 달러)

표 143 유통 채널별 밀 글루텐 시장의 이탈리아 매장 기반 소매업체, 2020-2029년(백만 달러)

표 144 이탈리아 밀 글루텐 시장, 최종 사용자별, 2020-2029년(백만 달러)

표 145 최종 사용자별 이탈리아 밀 글루텐 시장 상업적 규모, 2020-2029년(백만 달러)

표 146 덴마크 밀 글루텐 시장, 범주별, 2020-2029 (백만 달러)

표 147 덴마크 밀 글루텐 시장, 기능별, 2020-2029 (백만 달러)

표 148 덴마크 밀 글루텐 시장, 형태별, 2020-2029 (백만 달러)

표 149 덴마크 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 150 덴마크 밀 글루텐 시장의 식품 및 음료, 응용 분야별, 2020-2029 (백만 달러)

표 151 덴마크 제빵 및 제과 제품, 밀 글루텐 시장, 응용 분야별, 2020-2029년(백만 달러)

표 152 덴마크의 밀 글루텐 시장에서의 편의 식품, 응용 분야별, 2020-2029년 (백만 달러)

표 153 덴마크의 밀 글루텐 시장 내 동물 사료, 용도별, 2020-2029년(백만 달러)

표 154 덴마크 밀 글루텐 시장, 포장 기준, 2020-2029 (백만 달러)

표 155 덴마크 밀 글루텐 병/항아리 시장, 포장 기준, 2020-2029 (백만 달러)

표 156 덴마크 밀 글루텐 시장, 유통 채널별, 2020-2029년(백만 달러)

표 157 유통 채널별 밀 글루텐 시장의 덴마크 매장 기반 소매업체, 2020-2029년(백만 달러)

표 158 덴마크 밀 글루텐 시장, 최종 사용자별, 2020-2029 (백만 달러)

표 159 덴마크의 밀 글루텐 시장 거래, 최종 사용자별, 2020-2029년(백만 달러)

표 160 스웨덴 밀 글루텐 시장, 범주별, 2020-2029 (백만 달러)

표 161 스웨덴 밀 글루텐 시장, 기능별, 2020-2029 (백만 달러)

표 162 스웨덴 밀 글루텐 시장, 형태별, 2020-2029 (백만 달러)

표 163 스웨덴 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 164 스웨덴 식품 및 음료, 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 165 스웨덴 제빵 및 제과 제품, 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 166 스웨덴 편의식품, 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 167 2020-2029년 용도별 스웨덴 밀 글루텐 사료 시장(백만 달러)

표 168 스웨덴 밀 글루텐 시장, 포장 기준, 2020-2029 (백만 달러)

표 169 스웨덴 병/항아리 밀 글루텐 시장, 포장 기준, 2020-2029 (백만 달러)

표 170 스웨덴 밀 글루텐 시장, 유통 채널별, 2020-2029년(백만 달러)

표 171 유통 채널별 밀 글루텐 시장의 스웨덴 매장 기반 소매업체, 2020-2029년(백만 달러)

표 172 최종 사용자별 스웨덴 밀 글루텐 시장, 2020-2029년(백만 달러)

표 173 최종 사용자별 스웨덴 밀 글루텐 시장 상업적 규모, 2020-2029년(백만 달러)

표 174 러시아 밀 글루텐 시장, 범주별, 2020-2029 (백만 달러)

표 175 러시아 밀 글루텐 시장, 기능별, 2020-2029 (백만 달러)

표 176 러시아 밀 글루텐 시장, 형태별, 2020-2029 (백만 달러)

표 177 러시아 밀 글루텐 시장, 용도별, 2020-2029 (백만 달러)

표 178 러시아 밀 글루텐 시장의 식품 및 음료, 응용 분야별, 2020-2029 (백만 달러)

표 179 러시아 제빵 및 제과 제품, 밀 글루텐 시장, 응용 분야별, 2020-2029년(백만 달러)

표 180 러시아 편의식품, 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 181 러시아 동물 사료 시장(밀 글루텐, 용도별), 2020-2029(백만 달러)

표 182 러시아 밀 글루텐 시장, 포장 기준, 2020-2029 (백만 달러)

표 183 러시아 밀 글루텐 시장 병/항아리, 포장별, 2020-2029년(백만 달러)

표 184 러시아 밀 글루텐 시장, 유통 채널별, 2020-2029년(백만 달러)

표 185 러시아 밀 글루텐 시장의 유통 채널별 매장 기반 소매업체, 2020-2029년(백만 달러)

표 186 최종 사용자별 러시아 밀 글루텐 시장, 2020-2029년(백만 달러)

표 187 최종 사용자별 러시아 밀 글루텐 시장 상업적 규모, 2020-2029년(백만 달러)

표 188 스위스 밀 글루텐 시장, 범주별, 2020-2029년(백만 달러)

표 189 스위스 밀 글루텐 시장, 기능별, 2020-2029 (백만 달러)

표 190 스위스 밀 글루텐 시장, 형태별, 2020-2029 (백만 달러)

표 191 스위스 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 192 2020-2029년 응용 분야별 밀 글루텐 시장의 스위스 식품 및 음료(백만 달러)

표 193 2020-2029년 응용 분야별 밀 글루텐 시장의 스위스 제빵 및 제과 제품(백만 달러)

표 194 스위스 편의식품, 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 195 스위스의 밀 글루텐 시장 동물 사료, 용도별, 2020-2029 (백만 달러)

표 196 스위스 밀 글루텐 시장, 포장 기준, 2020-2029 (백만 달러)

표 197 스위스 밀 글루텐 병/항아리 시장, 포장 기준, 2020-2029년(백만 달러)

표 198 스위스 밀 글루텐 시장, 유통 채널별, 2020-2029년(백만 달러)

표 199 유통 채널별 밀 글루텐 시장의 스위스 매장 기반 소매업체, 2020-2029년(백만 달러)

표 200 스위스 밀 글루텐 시장, 최종 사용자별, 2020-2029(백만 달러)

표 201 최종 사용자별 스위스 밀 글루텐 시장 상업적 규모, 2020-2029 (백만 달러)

표 202 폴란드 밀 글루텐 시장, 카테고리별, 2020-2029 (백만 달러)

표 203 폴란드 밀 글루텐 시장, 기능별, 2020-2029 (백만 달러)

표 204 폴란드 밀 글루텐 시장, 형태별, 2020-2029 (백만 달러)

표 205 폴란드 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 206 폴란드 밀 글루텐 시장의 식품 및 음료, 응용 분야별, 2020-2029 (백만 달러)

표 207 폴란드 제빵 및 제과 제품, 밀 글루텐 시장, 응용 분야별, 2020-2029년(백만 달러)

표 208 폴란드 편의식품 밀 글루텐 시장, 응용 분야별, 2020-2029 (백만 달러)

표 209 폴란드 밀 글루텐 사료 시장, 응용 분야별, 2020-2029 (백만 달러)

표 210 폴란드 밀 글루텐 시장, 포장 기준, 2020-2029 (백만 달러)

표 211 폴란드 밀 글루텐 시장 병/항아리, 포장별, 2020-2029 (백만 달러)

표 212 폴란드 밀 글루텐 시장, 유통 채널별, 2020-2029년(백만 달러)

표 213 유통 채널별 밀 글루텐 시장의 폴란드 매장 기반 소매업체, 2020-2029년(백만 달러)

표 214 폴란드 밀 글루텐 시장, 최종 사용자별, 2020-2029(백만 달러)

표 215 폴란드의 밀 글루텐 시장, 최종 사용자별, 2020-2029년 (백만 달러)

표 216 칠면조 밀 글루텐 시장, 범주별, 2020-2029년(백만 달러)

표 217 칠면조 밀 글루텐 시장, 기능별, 2020-2029년(백만 달러)

표 218 칠면조 밀 글루텐 시장, 형태별, 2020-2029 (백만 달러)

표 219 칠면조 밀 글루텐 시장, 응용 분야별, 2020-2029년(백만 달러)

표 220 밀 글루텐 시장의 칠면조 식품 및 음료, 응용 분야별, 2020-2029년(백만 달러)

표 221 밀 글루텐 시장의 터키 제빵 및 제과 제품, 응용 분야별, 2020-2029년(백만 달러)

표 222 밀 글루텐 시장에서의 터키 편의 식품, 응용 분야별, 2020-2029 (백만 달러)

표 223 밀 글루텐 시장에서의 칠면조 동물 사료, 응용 분야별, 2020-2029년(백만 달러)

표 224 칠면조 밀 글루텐 시장, 포장별, 2020-2029년(백만 달러)

표 225 밀 글루텐 시장에서의 칠면조 병/항아리, 포장별, 2020-2029년(백만 달러)

표 226 유통 채널별 칠면조 밀 글루텐 시장, 2020-2029년(백만 달러)

표 227 유통 채널별 밀 글루텐 시장의 터키 매장 기반 소매업체, 2020-2029년(백만 달러)

표 228 최종 사용자별 칠면조 밀 글루텐 시장, 2020-2029년(백만 달러)

표 229 밀 글루텐 시장에서의 터키 상업적 거래, 최종 사용자별, 2020-2029 (백만 달러)

표 230 유럽 기타 지역 밀 글루텐 시장, 범주별, 2020-2029년(백만 달러)

그림 목록

그림 1 유럽 밀 글루텐 시장: 세분화

그림 2 유럽 밀 글루텐 시장: 데이터 삼각 측량

그림 3 유럽 밀 글루텐 시장: DROC 분석

그림 4 유럽 밀 글루텐 시장: 유럽 대 지역 시장 분석

그림 5 유럽 밀 글루텐 시장: 회사 연구 분석

그림 6 유럽 밀 글루텐 시장: 인터뷰 인구 통계

그림 7 유럽 밀 글루텐 시장: DBMR 시장 위치 그리드

그림 8 유럽 밀 글루텐 시장: 시장 적용 범위 그리드

그림 9 유럽 밀 글루텐 시장: 공급업체 점유율 분석

그림 10 유럽 밀 글루텐 시장: 세분화

그림 11 밀 글루텐 기술에 대한 지출 증가는 2022년에서 2029년 예측 기간 동안 유럽 밀 글루텐 시장을 주도할 것으로 예상됩니다.

그림 12 유기농 세그먼트는 2022년 및 2029년 유럽 밀 글루텐 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다.

그림 13 유럽 밀 글루텐 시장의 동인, 제약, 기회 및 과제

그림 14 유럽 밀 글루텐 시장: 범주별, 2021

그림 15 유럽 밀 글루텐 시장: 범주별, 2022-2029(백만 달러)

그림 16 유럽 밀 글루텐 시장: 범주별, CAGR(2022-2029)

그림 17 유럽 밀 글루텐 시장: 범주별, 수명선 곡선

그림 18 유럽 밀 글루텐 시장: 기능별, 2021

그림 19 유럽 밀 글루텐 시장: 기능별, 2022-2029년(백만 달러)

그림 20 유럽 밀 글루텐 시장: 기능별, CAGR(2022-2029)

그림 21 유럽 밀 글루텐 시장: 기능별, 수명선 곡선

그림 22 유럽 밀 글루텐 시장: 형태별, 2021

그림 23 유럽 밀 글루텐 시장: 형태별, 2022-2029(백만 달러)

그림 24 유럽 밀 글루텐 시장: 형태별, CAGR별(2022-2029)

그림 25 유럽 밀 글루텐 시장: 형태별, 수명선 곡선

그림 26 유럽 밀 글루텐 시장: 응용, 2021

그림 27 유럽 밀 글루텐 시장: 응용, 2022-2029(백만 달러)

그림 28 유럽 밀 글루텐 시장: 응용, CAGR(2022-2029)

그림 29 유럽 밀 글루텐 시장: 형태별, 수명선 곡선별

그림 30 유럽 밀 글루텐 시장: 포장별, 2021

그림 31 유럽 밀 글루텐 시장: 포장별, 2022-2029(백만 달러)

그림 32 유럽 밀 글루텐 시장: 포장별, CAGR(2022-2029)

그림 33 유럽 밀 글루텐 시장: 포장별, 수명선 곡선

그림 34 유럽 밀 글루텐 시장: 유통 채널, 2021

그림 35 유럽 밀 글루텐 시장: 유통 채널, 2022-2029(백만 달러)

그림 36 유럽 밀 글루텐 시장: 유통 채널, CAGR(2022-2029)

그림 37 유럽 밀 글루텐 시장: 유통 채널, 라이프라인 곡선

그림 38 유럽 밀 글루텐 시장: 최종 사용자별, 2021

그림 39 유럽 밀 글루텐 시장: 최종 사용자별, 2022-2029(백만 달러)

그림 40 유럽 밀 글루텐 시장: 최종 사용자별, CAGR(2022-2029)

그림 41 유럽 밀 글루텐 시장: 최종 사용자별, 수명선 곡선

그림 42 유럽 밀 글루텐 시장: 스냅샷(2021)

그림 43 유럽 밀 글루텐 시장: 국가별(2021)

그림 44 유럽 밀 글루텐 시장: 국가별(2022년 및 2029년)

그림 45 유럽 밀 글루텐 시장: 국가별(2021년 및 2029년)

그림 46 유럽 밀 글루텐 시장: 범주(2022-2029)

그림 47 유럽 밀 글루텐 시장: 회사 점유율 2021(%)

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.