Global Adhesives Sealants Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

121.27 Billion

USD

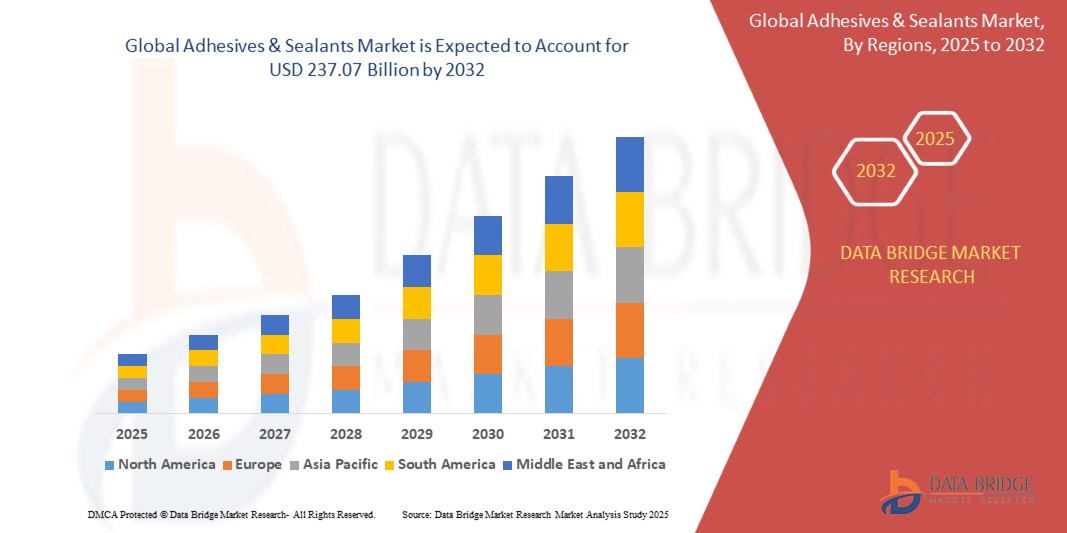

237.07 Billion

2024

2032

USD

121.27 Billion

USD

237.07 Billion

2024

2032

| 2025 –2032 | |

| USD 121.27 Billion | |

| USD 237.07 Billion | |

| % | |

|

글로벌 접착제 및 실란트 시장 세분화, 기술(수성, 용제 기반, 핫멜트, 반응성 및 기타), 제품(아크릴, 폴리비닐 아세테이트(PVA), 폴리우레탄, 스티렌 블록 공중합체, 에폭시, 에틸렌-비닐 아세테이트(EVA), 기타), 응용 분야(종이 및 포장, 소비자 및 DIY, 건축 및 건설, 가구 및 목공, 신발 및 가죽, 자동차 및 운송, 의료, 기타) - 산업 동향 및 2032년까지의 전망

접착제 및 실란트 시장 규모

- 글로벌 접착제 및 실란트 시장 규모는 2023년에 1,212억 7천만 달러로 평가되었으며, 2030년까지 2,370억 7천만 달러에 이를 것으로 예상되며, 예측 기간 동안 연평균 성장률 10.1%로 성장할 것으로 전망됩니다.

- 이 부문의 성장은 자동차, 건설, 전자, 재생 에너지 부문 전반에 걸쳐 고성능 접합 솔루션에 대한 수요 증가에 힘입어 이루어지고 있습니다.

접착제 및 실란트 시장 분석

- 시장 성장은 자동차 제조 및 건설 프로젝트에서 유리, 금속, 고무와 같은 재료를 조립하는 데 광범위하게 사용되면서 촉진되었습니다.

- 경량 차량 생산에서 고성능 실런트에 대한 수요가 증가함에 따라 경제적 효율성이 향상되고 금속, 플라스틱과 같은 기존 소재에 대한 의존도가 낮아졌습니다.

- 아시아 태평양 지역은 2023년 기준 글로벌 시장 점유율 41.3%를 차지하며 주요 소비 지역으로 자리매김했으며, 이는 중국, 인도, 인도네시아 등의 국가에서 건설 및 건축에 대한 소비가 증가한 데 따른 것입니다.

- 북미와 유럽은 각각 건설 활동과 자동차 생산의 증가로 인해 꾸준한 성장을 경험하고 있습니다.

- 수성 접착제는 2023년에 31.7%의 시장 점유율로 시장을 장악했습니다. 수성 접착제는 다재다능하고 환경적 이점이 있어 다양한 산업 분야에 적합합니다.

- 반응형 및 기타 기술은 첨단 접합 기능에 힘입어 연평균 성장률 8.9%로 성장할 것으로 예상됩니다.

보고서 범위 및 접착제 및 실란트 시장 세분화

|

속성 |

접착제 및 실란트 시장 통찰력 |

|

다루는 세그먼트 |

|

|

포함 국가 |

북아메리카

유럽

아시아 태평양

중동 및 아프리카

남아메리카

|

|

주요 시장 참여자 |

|

|

시장 기회 |

|

|

부가가치 데이터 정보 세트 |

Data Bridge Market Research에서 큐레이팅한 시장 보고서에는 시장 가치, 성장률, 세분화, 지리적 적용 범위, 주요 기업 등 시장 시나리오에 대한 통찰력 외에도 심층적인 전문가 분석, 가격 분석, 브랜드 점유율 분석, 소비자 설문 조사, 인구 통계 분석, 공급망 분석, 가치 사슬 분석, 원자재/소모품 개요, 공급업체 선택 기준, PESTLE 분석, Porter 분석 및 규제 프레임워크가 포함되어 있습니다. |

접착제 및 실란트 시장 동향

“ 지속 가능하고 VOC가 낮은 접착제 및 실란트에 대한 선호도 증가 ”

- 글로벌 접착제 및 실란트 시장을 형성하는 두드러진 추세 중 하나는 지속 가능하고 VOC가 낮은 제형에 대한 선호도가 높아지는 것입니다.

- 이러한 추세는 주로 배출량을 줄이려는 규제 압력이 증가하고, 건강과 환경에 미치는 영향에 대한 소비자의 인식이 높아지고, 자동차, 포장, 건설 등 주요 최종 사용자 산업이 지속 가능성에 대한 약속을 채택한 데서 비롯되었습니다.

예를 들어, Henkel AG와 HB Fuller Company와 같은 회사는 글로벌 친환경 건축 규정과 환경 규정 준수 기준을 충족하는 생물 기반 접착제와 수성 실란트 솔루션을 개발했습니다.

- 이러한 저VOC 및 무용제 제품을 채택하면 제조업체는 높은 접합 성능을 유지하는 동시에 환경 인증을 충족할 수 있습니다.

- 산업계가 강도나 내구성을 떨어뜨리지 않으면서도 보다 친환경적인 화학 물질을 우선시함에 따라, 지속 가능한 접착제 및 실란트 기술의 혁신이 가속화되어 향후 몇 년 안에 경쟁 우위를 확보할 것으로 예상됩니다.

접착제 및 실란트 시장 동향

운전사

“경량 고성능 접합 솔루션에 대한 수요 증가”

- 가볍고 고성능의 접합 솔루션에 대한 수요가 증가함에 따라 접착제 및 실런트 시장이 크게 성장하고 있습니다.

- 이러한 변화는 특히 자동차, 항공우주, 전자, 건설과 같은 분야에서 두드러지는데, 이러한 분야에서는 성능 저하 없이 무게를 줄이는 것이 효율성, 내구성, 에너지 보존에 필수적입니다.

- 접착제와 실런트는 전통적인 기계적 패스너에 비해 응력 분포가 균일하고, 열 팽창에 대한 저항성이 뛰어나며, 미학적으로 우수한 등의 장점을 제공합니다.

For example, Sika AG has developed advanced polyurethane and epoxy adhesives designed for structural bonding in lightweight vehicle assemblies. Similarly, 3M Company provides acrylic and silicone-based sealants tailored for electronics and construction applications where high thermal stability and moisture resistance are critical.

- As industries increasingly focus on design flexibility, fuel efficiency, and enhanced mechanical properties, the demand for specialized adhesive and sealant solutions is expected to remain strong, driving both volume and value growth in the global market.

Restraint/Challenge

“Volatility in Raw Material Prices and Supply Chain Disruptions”

- A major restraint impacting the adhesives & sealants market is the volatility in raw material prices, particularly those derived from petrochemicals, such as resins, solvents, and isocyanates.

- Fluctuations in crude oil prices, coupled with geopolitical tensions and supply chain bottlenecks, have led to increased uncertainty in material costs and availability. This volatility puts pressure on manufacturers’ margins and limits pricing flexibility in highly competitive end-use industries.

For instance, producers of polyurethane and epoxy adhesives face periodic cost surges due to disrupted feedstock supply, especially in regions heavily reliant on imports. Additionally, the push toward bio-based raw materials often entails higher input costs and longer development cycles, further constraining affordability.

- These challenges can impede the adoption of advanced adhesives and sealants, particularly in cost-sensitive sectors such as furniture, footwear, and construction. Addressing raw material cost volatility and ensuring reliable supply chains will remain critical for sustaining growth in the adhesives & sealants market.

Adhesives & Sealants Market Scope

The market is segmented on the basis of technology, product, and application.

- By Technology

On the basis of technology, the adhesives & sealants market is segmented into Water-Based, Solvent-Based, Hot-Melt, Reactive, and Others. The Water-Based segment holds the largest market revenue share of 38.5% in 2025, attributed to its widespread adoption across packaging, construction, and labeling applications, driven by regulatory pressure to reduce VOC emissions and growing end-user preference for non-toxic, environmentally friendly formulations. Water-based adhesives offer easy application, cost-effectiveness, and excellent performance across porous substrates, supporting their dominance.

However, the Reactive segment is expected to grow at the highest CAGR of 7.86% during the forecast period of 2025–2032. This growth is driven by increasing demand for high-strength, durable bonding in automotive, electronics, and aerospace sectors, where reactive technologies such as polyurethane and epoxy-based adhesives offer superior resistance to heat, chemicals, and moisture.

- By Product

On the basis of product, the market is segmented into Acrylic, Polyvinyl Acetate (PVA), Polyurethanes, Styrenic Block Copolymers, Epoxy, Ethylene-Vinyl Acetate (EVA), and Others. The Acrylic segment dominates with the largest revenue share of 30.7% in 2025, owing to its versatility, fast curing times, and strong adhesion to a variety of substrates. Acrylic adhesives are widely used in construction, electronics, and packaging industries due to their excellent UV resistance and durability.

Meanwhile, the Polyurethanes segment is projected to exhibit the highest CAGR of 8.14% over the forecast period. This is driven by growing applications in automotive, footwear, and construction sectors where flexibility, weather resistance, and superior bonding on varied surfaces are critical performance parameters. The development of moisture-curing and two-component polyurethane systems is further propelling segment growth.

- By End-Use Industry

On the basis of end-use industry, the market is categorized into Biomedical, Electronics, Paints & Coatings, and Others. The Biomedical segment is anticipated to dominate the market by 2025 owing to the growing use of Adhesives & Sealants in drug delivery systems, implants, and anti-fouling medical devices. Their superior biocompatibility, non-toxicity, and customizable surface functionality are critical for advanced healthcare applications.

The Electronics segment is expected to grow with the highest CAGR through 2032, attributed to increasing demand for nanoscale surface modification in electronic components, semiconductors, and wearable devices where Adhesives & Sealants enhance performance, insulation, and durability.

- By Application

Based on application, the adhesives & sealants market is segmented into Paper & Packaging, Consumer & DIY, Building & Construction, Furniture & Woodworking, Footwear & Leather, Automotive & Transportation, Medical, and Others. The Paper & Packaging segment is expected to account for the largest share of 23.9% in 2025, primarily due to the surge in e-commerce and FMCG sectors, where fast-setting and food-safe adhesive solutions are essential for corrugated boxes, labels, and cartons.

In contrast, the Automotive & Transportation segment is projected to witness the highest CAGR of 8.32% during the forecast period. Increasing emphasis on vehicle light-weighting, structural integrity, and NVH (noise, vibration, and harshness) performance is driving the use of structural adhesives and advanced sealants in electric vehicles, interiors, and under-the-hood applications.

Global Adhesives & Sealants Market Regional Analysis

North America Adhesives & Sealants Market Insight

North America holds a prominent position in the global adhesives & sealants market, accounting for 32.1% of the total market revenue in 2025. The market is driven by well-established end-use industries such as construction, automotive, packaging, and electronics.

이 지역의 지속가능성, 저VOC 및 무용제 기술 혁신, 그리고 주요 글로벌 제조업체들의 입지가 수요 증가에 기여하고 있습니다. 또한, 인프라 개보수 활동 증가와 내구성이 뛰어나고 가벼운 접착 솔루션에 대한 소비자들의 선호도가 성장을 지속적으로 촉진하고 있습니다.

- 미국 접착제 및 실란트 시장 통찰력

미국은 포장, 건설, 자동차 부문의 높은 소비에 힘입어 북미 시장에서 가장 큰 매출 점유율을 기록하며 시장을 선도하고 있습니다. 친환경 건축 솔루션과 에너지 효율 기술에 대한 수요 증가로 반응성 및 수성 접착제의 도입이 빠르게 증가하고 있습니다. 바이오 기반 제품에 대한 R&D 투자와 탄탄한 OEM 파트너십은 성장을 더욱 촉진하고 있습니다.

- 캐나다 접착제 및 실란트 시장 통찰력

캐나다 시장은 주택 및 사회 기반 시설에 대한 지속적인 투자에 힘입어 꾸준한 성장을 보일 것으로 예상됩니다. 모듈러 건축 분야에서 고성능 접착제에 대한 수요 증가와 목재 가구 제조 산업의 성장이 주요 원인입니다. 또한, 캐나다의 강력한 환경 규제 체계는 친환경적이고 무독성 접착제 기술의 사용을 장려하고 있습니다.

유럽 접착제 및 실란트 시장 통찰력

유럽은 엄격한 환경 기준, 에너지 효율적인 건축 법규, 그리고 친환경 화학 분야의 혁신을 바탕으로 성숙하면서도 역동적인 접착제 및 실란트 시장을 선도하고 있습니다. 2025년 유럽은 전 세계 시장 매출의 약 28.7%를 차지했습니다. 자동차, 의료 및 포장 산업 전반에 걸쳐 고성능, 규정 준수형 접착제 시스템에 대한 수요가 지속적으로 증가하고 있습니다.

- 독일 접착제 및 실란트 시장 통찰력

독일은 자동차 및 엔지니어링 분야의 선진화 덕분에 유럽 최대 시장으로 자리매김했습니다. 차량 조립 및 경량 구조물 분야에서 반응성 및 폴리우레탄 접착제의 높은 채택률이 시장 확대를 견인하고 있습니다. 제품 품질, VOC 준수, 재활용성 강화는 OEM 및 애프터마켓 채널 모두에서 차세대 실란트 시스템 사용을 더욱 촉진합니다.

- 프랑스 접착제 및 실란트 시장 통찰력

프랑스는 정부의 지속 가능한 도시 개발 및 에너지 개량 프로그램 강화에 힘입어 접착제 및 실란트 시장이 눈에 띄게 성장하고 있습니다. 친환경 건축 자재의 증가와 태양광 모듈 및 풍력 터빈을 포함한 재생 에너지의 활용 증가는 구조용 접착제 및 내후성 실란트 사용량 증가를 뒷받침하고 있습니다.

아시아 태평양 접착제 및 실란트 시장 통찰력

아시아 태평양 지역은 예측 기간(2025~2032년) 동안 8.74%의 가장 높은 연평균 성장률(CAGR)을 기록하며 가장 빠르게 성장하는 지역 시장이 될 것으로 예상됩니다. 이러한 성장은 중국, 인도, 동남아시아 등 신흥 경제권의 대규모 산업화, 증가하는 소비자 수요, 그리고 인프라 개발에 힘입어 가능합니다. 이 지역의 전자, 포장, 운송 산업의 성장은 다양한 접착 기술의 소비를 촉진하고 있습니다.

- 중국 접착제 및 실란트 시장 통찰력

중국은 대규모 건설 활동, 자동차 생산의 급속한 성장, 그리고 가전제품 제조 분야의 선도적 지위를 바탕으로 아시아 태평양 시장을 장악하고 있습니다. 지속 가능한 도시 기반 시설에 대한 관심 증가와 에너지 효율 기술에 대한 정부 지원은 주요 산업 분야에서 첨단 무용제 접착제 시스템 도입을 촉진하고 있습니다.

- 인도 접착제 및 실란트 시장 통찰력

인도는 건설 호황, 제조 능력 확대, 그리고 포장 및 FMCG 산업의 자동화 도입 증가에 힘입어 이 지역에서 가장 빠른 연평균 성장률(CAGR)을 기록할 것으로 예상됩니다. 정부의 "메이크 인 인디아(Make in India)" 정책과 운송 및 재생 에너지 투자는 시장 수요를 뒷받침하고 있습니다. 친환경 화학 및 국제 품질 기준에 대한 인식이 높아짐에 따라 수성 및 하이브리드 접착제 기술의 사용이 가속화되고 있습니다.

접착제 및 실란트 시장 참여자

접착제 및 실런트 산업은 주로 다음을 포함한 잘 확립된 회사들이 주도하고 있습니다.

- 헨켈 AG(독일)

- 3M 회사(미국)

- HB 풀러 컴퍼니(미국)

- Sika AG(스위스)

- Pidilite Industries Ltd.(인도)

- 다우(Dow Inc.) (미국)

- RPM International Inc.(미국)

- 쿠라레 주식회사(일본)

- Wacker Chemie AG(독일)

- 애슐랜드 주식회사(미국)

- Mapei SpA(이탈리아)

- 보스틱(프랑스)

- 프랭클린 인터내셔널(미국)

- Jowat SE(독일)

- Permabond LLC(영국)

- 헌츠먼 코퍼레이션(미국)

글로벌 접착제 및 실란트 시장의 최신 동향

- 2025년 4월, 헨켈은 자동차 내장재 및 전자 부품 조립 분야에 특화된 테크노멜트 PUR 시리즈의 새로운 폴리우레탄 기반 반응성 핫멜트 접착제 제품군을 출시했습니다. 이 접착제는 향상된 내열성과 장기적인 내구성을 제공하는 동시에 저배출 기준을 충족합니다. 이 제품군은 고성능 접착 분야에서 헨켈의 경쟁력을 강화하고, 환경 프로파일 개선을 통해 지속가능성 목표 달성에 기여할 것으로 기대됩니다.

- 2025년 2월, 3M은 항공우주 및 방위 산업에서 사용되는 경량 복합재용으로 설계된 고급 구조용 접착제인 스카치-웰드 EC-9300을 출시했습니다. 이 새로운 접착제는 탁월한 강도 대 중량비와 높은 피로 저항성을 제공하여 연비 및 소재 최적화를 중시하는 업계 추세에 부합합니다. 이번 개발은 핵심 응용 분야를 위한 고급 구조용 접착제 기술 분야에서 3M의 선도적 입지를 더욱 강화합니다.

- In August 2024, Arkema expanded its Bostik smart adhesives portfolio by acquiring a specialty adhesives plant in Vietnam. This strategic move is intended to increase its production capabilities in Southeast Asia and respond to rising regional demand from the packaging and construction sectors. The expansion supports Bostik’s regional footprint and enhances supply chain responsiveness for fast-growing Asian markets.

- In June 2024, Sika AG unveiled a new-generation silane-modified polymer (SMP)-based sealant, Sikaflex®-521 Evolution, formulated for transportation and industrial assembly. Offering improved elasticity, UV resistance, and green chemistry credentials, this innovation meets tightening regulatory requirements and end-user expectations for sustainable sealant technologies.

- In January 2024, H.B. Fuller introduced TEC® CleanBond™, a next-gen water-based adhesive designed for use in hygiene and medical applications. It provides strong adhesion to low-energy surfaces, improved skin compatibility, and minimal residue, making it ideal for wound care, wearable devices, and medical tapes. This launch is expected to boost H.B. Fuller’s presence in the fast-growing medical adhesives segment.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.