Global Ambient Food Packaging Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

5.08 Billion

USD

9.77 Billion

2025

2033

USD

5.08 Billion

USD

9.77 Billion

2025

2033

| 2026 –2033 | |

| USD 5.08 Billion | |

| USD 9.77 Billion | |

| % | |

|

세계 상온 식품 포장 시장 세분화: 포장 유형(경질 포장 및 연질 포장), 재질 유형(금속, 유리 및 플라스틱), 적용 분야(과일 및 채소, 육류, 생선 및 가금류) - 산업 동향 및 2033년까지의 전망

상온 식품 포장 시장 규모

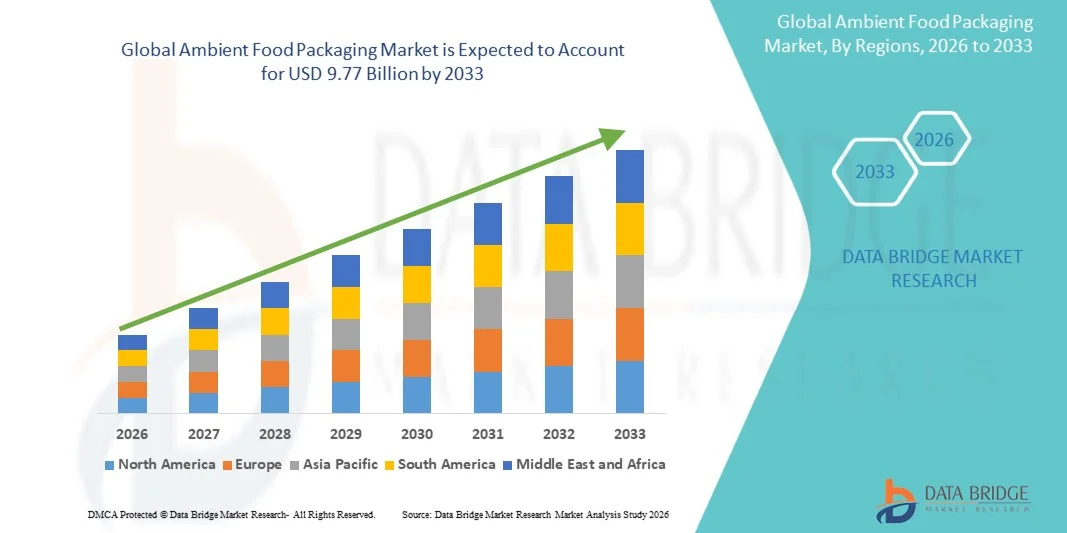

- 세계 상온 식품 포장 시장 규모는 2025년 50억 8천만 달러 였으며, 예측 기간 동안 연평균 8.50%의 성장률을 기록하여 2033년에는 97억 7천만 달러 에 이를 것으로 예상됩니다 .

- 시장 성장은 주로 포장 및 즉석식품에 대한 수요 증가, 편의성에 대한 소비자 선호도 상승, 그리고 조직화된 소매 채널의 확장에 힘입어 이루어지고 있습니다.

- 식품 안전 및 위생에 대한 인식이 높아지고 포장재 기술이 발전함에 따라 상온 식품 포장재의 도입이 촉진되고 있습니다.

상온 식품 포장 시장 분석

- 도시화, 생활 방식의 변화, 가공 및 포장 식품의 보급 확대로 인해 시장은 견조한 성장세를 보이고 있습니다.

- 제조업체들은 식품 품질을 유지하면서 유통기한을 연장하는 포장재를 개발하기 위한 연구 개발에 투자하고 있습니다.

- 북미는 포장 및 즉석식품에 대한 수요 증가와 편의성 및 긴 유통기한을 선호하는 소비자 심리에 힘입어 2025년까지 상온 식품 포장 시장에서 38.75%의 최대 매출 점유율을 기록하며 시장을 주도할 것으로 예상됩니다.

- 아시아 태평양 지역은 인구 증가, 포장 식품 수요 증가, 식품 안전 및 위생에 대한 인식 제고, 그리고 현대적인 포장 기술 도입에 힘입어 전 세계 상온 식품 포장 시장 에서 가장 높은 성장률을 보일 것으로 예상됩니다 .

- 견고한 포장재 부문은 내구성, 물리적 손상 방지 기능, 그리고 유통기한 연장에 힘입어 2025년까지 가장 큰 시장 매출 점유율을 차지할 것으로 예상됩니다. 캔, 병, 상자 등의 견고한 포장재는 음료, 유제품, 가공식품에 널리 사용되며, 높은 구조적 안정성과 대량 생산 및 운송에 적합한 장점을 제공합니다.

보고서 범위 및 상온 식품 포장 시장 세분화

|

속성 |

상온 식품 포장 주요 시장 분석 |

|

포함되는 부문 |

|

|

대상 국가 |

북아메리카

유럽

아시아태평양

중동 및 아프리카

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Ambient Food Packaging Market Trends

“Rising Demand for Convenient and Shelf-Stable Food Products”

• The growing preference for ready-to-eat and long-shelf-life food products is significantly shaping the ambient food packaging market, as consumers increasingly seek convenience, portability, and minimal preparation requirements. Ambient packaging solutions, such as aseptic cartons, pouches, and cans, are gaining traction due to their ability to maintain product freshness without refrigeration. This trend is driving adoption across food and beverage sectors, encouraging manufacturers to innovate with packaging that balances functionality, cost, and sustainability

• Increasing awareness about food safety, hygiene, and waste reduction has accelerated the demand for ambient food packaging. Consumers and retailers are actively seeking packaging that protects products from contamination, extends shelf life, and reduces spoilage. This has prompted collaborations between packaging material suppliers and food manufacturers to develop solutions that ensure product quality while meeting evolving regulatory and consumer standards

• Convenience, sustainability, and safety trends are influencing purchasing decisions, with manufacturers emphasizing recyclable materials, minimal packaging, and eco-friendly production processes. These factors are helping brands differentiate products in a competitive market and build consumer trust, while also driving the adoption of certification labels and environmental claims. Companies are increasingly using marketing campaigns to highlight these benefits and reinforce brand positioning

• For instance, in 2024, Tetra Pak in Sweden and Amcor in Australia expanded their packaging portfolios by introducing innovative ambient packaging formats for beverages and processed foods. These launches were in response to growing consumer preference for convenient, hygienic, and eco-conscious products, with distribution across retail, e-commerce, and foodservice channels

• While demand for ambient food packaging is growing, sustained market expansion depends on continuous innovation, cost-effective production, and maintaining packaging performance comparable to refrigerated alternatives. Manufacturers are also focusing on enhancing supply chain efficiency, improving scalability, and developing sustainable solutions to support broader adoption

Ambient Food Packaging Market Dynamics

Driver

“Growing Preference for Convenience and Long-Shelf-Life Products”

• Rising consumer demand for ready-to-eat and shelf-stable foods is a major driver for the ambient food packaging market. Manufacturers are increasingly adopting packaging that ensures product freshness without refrigeration, improves convenience, and reduces waste. This trend is also encouraging research into novel packaging materials and formats that enhance product appeal and functionality

• Expanding applications across beverages, dairy alternatives, snacks, and processed foods are influencing market growth. Ambient food packaging helps maintain product quality, protect against contamination, and improve transportability, enabling manufacturers to meet consumer expectations for safe, convenient, and durable products. Increasing urbanization and busy lifestyles further reinforce this trend

• Food and beverage manufacturers are actively promoting ambient packaging through product innovation, marketing campaigns, and sustainability initiatives. These efforts are supported by growing consumer preference for eco-friendly and hygienic products, and they also encourage partnerships between packaging suppliers and brands to enhance product protection and reduce environmental footprint

• For instance, in 2023, Nestlé in Switzerland and PepsiCo in the U.S. reported increased use of ambient packaging for dairy beverages and ready-to-drink products. This expansion followed higher consumer demand for convenient, safe, and recyclable packaging solutions, driving repeat purchases and product differentiation. Both companies highlighted sustainability and safety in marketing campaigns to strengthen consumer trust and brand loyalty

• Although rising convenience and safety trends support growth, wider adoption depends on cost optimization, material availability, and scalable production processes. Investment in supply chain efficiency, sustainable sourcing, and advanced packaging technologies will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

“Higher Cost And Limited Awareness Compared To Conventional Packaging”

• The relatively higher cost of advanced ambient packaging compared to traditional packaging remains a key challenge, limiting adoption among price-sensitive manufacturers. Higher raw material costs and complex production processes contribute to elevated pricing. In addition, fluctuating supply of sustainable packaging materials can affect cost stability and market penetration

• Consumer and manufacturer awareness remains uneven, particularly in developing markets where demand for ambient and sustainable packaging is still emerging. Limited understanding of functional and environmental benefits restricts adoption across certain product categories. This also leads to slower uptake in emerging economies where educational initiatives on ambient packaging are minimal

• Supply chain and distribution challenges also impact market growth, as ambient packaging requires sourcing from certified suppliers and adherence to stringent quality standards. Logistical complexities, specialized storage, and transportation requirements increase operational costs. Companies must invest in efficient handling and distribution networks to maintain product integrity

• For instance, in 2024, distributors in Singapore and Thailand supplying packaged beverages and ready-to-eat foods reported slower uptake due to higher prices and limited awareness of functional and environmental advantages compared to conventional packaging. Storage requirements and certification compliance were additional barriers, prompting some retailers to limit shelf space for premium ambient packaging products

• Overcoming these challenges will require cost-efficient production, expanded distribution networks, and focused educational initiatives for manufacturers and consumers. Collaboration with retailers, foodservice operators, and certification bodies can help unlock the long-term growth potential of the global ambient food packaging market. Furthermore, developing cost-competitive and sustainable packaging solutions, while emphasizing product safety and convenience, will be essential for widespread adoption

Ambient Food Packaging Market Scope

The market is segmented on the basis of packaging type, material type, and application.

• By Packaging Type

On the basis of packaging type, the ambient food packaging market is segmented into rigid packaging and flexible packaging. The rigid packaging segment held the largest market revenue share in 2025 driven by its durability, ability to protect food from physical damage, and extended shelf life. Rigid packaging solutions such as cans, jars, and cartons are widely used for beverages, dairy, and processed foods, offering high structural integrity and suitability for mass production and transport.

The flexible packaging segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its lightweight nature, cost-effectiveness, and adaptability for a variety of food products. Flexible packaging formats, such as pouches, bags, and films, are particularly popular for snacks, ready-to-eat meals, and liquid products, providing convenience, easy storage, and enhanced barrier properties to maintain product freshness.

• By Material Type

On the basis of material type, the market is segmented into metal, glass, and plastic. The metal segment held the largest market revenue share in 2025 due to its robustness, recyclability, and ability to provide an airtight seal, which preserves food quality and prevents contamination. Metal cans are widely used in processed foods, beverages, and ready-to-eat meals.

The plastic segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its lightweight properties, versatility, and suitability for innovative packaging designs. Plastic materials are increasingly used in pouches, trays, and bottles, offering convenience, cost efficiency, and compatibility with various food types.

• By Application

On the basis of application, the ambient food packaging market is segmented into fruits and vegetables, meat, fish, and poultry. The fruits and vegetables segment held the largest market revenue share in 2025 driven by the growing demand for fresh, packaged produce with extended shelf life and reduced spoilage. Ambient packaging solutions such as cartons, films, and pouches are widely used to maintain freshness and quality during transportation and retail.

The meat, fish, and poultry segment is expected to witness the fastest growth from 2026 to 2033, fueled by the rising consumption of packaged protein products and increasing preference for hygiene, convenience, and ready-to-cook options. Packaging solutions for these products are designed to prevent contamination, maintain freshness, and extend shelf life without refrigeration.

Ambient Food Packaging Market Regional Analysis

• North America dominated the ambient food packaging market with the largest revenue share of 38.75% in 2025, driven by increasing demand for packaged and ready-to-eat food products, as well as rising consumer preference for convenience and long shelf-life solutions

• Consumers in the region highly value the safety, freshness preservation, and sustainability offered by ambient food packaging across snacks, beverages, dairy, and processed foods

• This widespread adoption is further supported by high disposable incomes, a technologically inclined population, and the growth of organized retail and e-commerce channels, establishing ambient food packaging as a preferred solution for both household and commercial consumption

U.S. Ambient Food Packaging Market Insight

The U.S. ambient food packaging market captured the largest revenue share in 2025 within North America, fueled by the increasing consumption of ready-to-eat and packaged food products. Consumers are prioritizing convenience, extended shelf life, and hygiene, encouraging manufacturers to adopt innovative packaging solutions. The growth of e-commerce, retail expansion, and demand for sustainable materials further drives market adoption. Moreover, marketing campaigns emphasizing food safety and eco-friendly packaging are contributing to the market’s expansion.

Europe Ambient Food Packaging Market Insight

The Europe ambient food packaging market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing demand for sustainable, hygienic, and shelf-stable food solutions. Urbanization, busy lifestyles, and regulatory standards promoting food safety are fostering adoption. European consumers are also drawn to packaging that reduces food waste while offering convenience. Growth spans across beverages, dairy, snacks, and processed foods, with both new product launches and reformulations leveraging ambient packaging.

U.K. Ambient Food Packaging Market Insight

The U.K. ambient food packaging market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising consumer preference for convenient, ready-to-eat, and eco-friendly packaged foods. Concerns regarding food safety, waste reduction, and sustainability are encouraging manufacturers and retailers to adopt ambient packaging solutions. The country’s well-developed retail infrastructure, combined with high consumer awareness of sustainable packaging, is expected to continue supporting market growth.

Germany Ambient Food Packaging Market Insight

The Germany ambient food packaging market is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing focus on food safety, hygiene, and environmentally responsible packaging. Germany’s strong manufacturing and technological capabilities, along with consumer demand for innovative and sustainable packaging formats, support adoption in both commercial and household applications. The integration of eco-friendly packaging into product portfolios aligns with local consumer preferences for safe, high-quality, and sustainable food products.

Asia-Pacific Ambient Food Packaging Market Insight

The Asia-Pacific ambient food packaging market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising urbanization, growing disposable incomes, and increasing demand for packaged and ready-to-eat foods in countries such as China, Japan, and India. The region’s expanding retail sector, rising food safety awareness, and adoption of modern packaging technologies are fueling growth. Furthermore, the availability of cost-effective packaging materials and local manufacturing capabilities is making ambient packaging more accessible to a wider consumer base.

Japan Ambient Food Packaging Market Insight

The Japan ambient food packaging market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s busy urban lifestyle, high disposable income, and demand for convenience. Consumers prioritize packaged foods with extended shelf life, hygiene, and quality preservation. The growing adoption of ready-to-eat meals, processed beverages, and retail innovations, coupled with sustainable packaging initiatives, is driving market growth.

China Ambient Food Packaging Market Insight

The China ambient food packaging market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding middle class, rapid urbanization, and increasing demand for packaged and shelf-stable foods. China represents one of the largest markets for processed and ready-to-eat foods, with ambient packaging widely adopted in household, commercial, and foodservice sectors. Government initiatives promoting food safety, modern retail expansion, and the presence of strong domestic packaging manufacturers are key factors propelling the market in China.

Ambient Food Packaging Market Share

The Ambient Food Packaging industry is primarily led by well-established companies, including:

- FFP Packaging Solutions Ltd (U.K.)

- Berry Global Inc. (U.S.)

- Amcor Limited (Australia)

- SIG Combibloc Obeikan (Switzerland)

- Tetra Pak (Sweden)

- Rexam (U.K.)

- Bemis (U.S.)

- Mondi (Austria)

- Ampac (U.S.)

- Dupont (U.S.)

- Excelsior Technologies (U.K.)

- KM Packaging Services Ltd. (U.K.)

- Marsden Holding LLC (U.S.)

Latest Developments in Global Ambient Food Packaging Market

- In August 2023, Amcor (Australia) announced a partnership with a leading food manufacturer to develop a new line of fully recyclable ambient food packaging. The initiative focuses on creating sustainable solutions that reduce environmental impact while maintaining food quality and shelf life. By leveraging Amcor’s packaging expertise, the partnership aims to deliver high-performance, eco-friendly options for a growing demand for responsible packaging. This move strengthens Amcor’s position as a leader in sustainable packaging and supports brands in meeting consumer expectations for environmentally conscious products. The collaboration is expected to drive adoption of recyclable packaging across the ambient food sector

- In September 2023, Sealed Air (U.S.) launched an innovative smart packaging technology integrating IoT capabilities to monitor product freshness in real-time. This technology allows manufacturers and retailers to track food quality throughout the supply chain, reducing spoilage and waste. By providing real-time data on product conditions, the solution enhances consumer safety and confidence in packaged foods. The adoption of smart packaging positions Sealed Air as a leader in tech-driven ambient food solutions and supports the broader trend of digitalization in food supply chains. The innovation also offers competitive differentiation in a market increasingly focused on sustainability and convenience

- In July 2023, Mondi Group (U.K.) expanded its operations in Southeast Asia by acquiring a local packaging firm specializing in ambient food solutions. The acquisition allows Mondi to broaden its product portfolio and offer innovative, high-quality packaging tailored to regional market needs. Leveraging the local company’s distribution networks and market knowledge, Mondi strengthens its competitive presence in a rapidly growing region. The move also enhances its ability to serve both multinational and local food brands with sustainable packaging solutions. This strategic expansion aligns with increasing demand for hygienic, convenient, and eco-friendly packaging in Asia-Pacific markets

- In August 2023, Amcor (North America) launched AmFiber™ high-barrier performance paper packaging designed for ambient food products. The packaging provides optimal barrier properties, extended shelf life, and efficient machine performance while being fully curbside-recyclable. This innovation addresses both environmental concerns and operational needs, offering brands a sustainable alternative to conventional packaging. By combining high performance with eco-friendliness, AmFiber™ supports the growing consumer preference for recyclable packaging. The launch is expected to influence market adoption of paper-based solutions in ambient food packaging, particularly for brands emphasizing sustainability and product quality

- In July 2023, Melodea introduced MelOx NGen, a high-performance barrier product designed for recyclable plastic food packaging. The product enables recyclability without compromising barrier properties, ensuring product freshness and extending shelf life. By facilitating sustainable packaging solutions, MelOx NGen helps food manufacturers meet regulatory requirements and consumer expectations for eco-friendly products. The innovation also supports circular economy initiatives by allowing post-consumer recycling of packaging materials. This launch strengthens Melodea’s position as a provider of sustainable packaging solutions and drives broader adoption of recyclable plastics in the ambient food market

- 2023년 7월, 캐나다의 캐스케이드(Cascades)는 농산물 포장용으로 재활용 및 재활용 가능한 골판지로 만든 밀폐형 바구니를 출시했습니다. 이 포장재는 과일과 채소를 위한 친환경적인 대안을 제공하며, 제품 보호는 물론 재활용성까지 향상시킵니다. 재활용 불가능한 소재 사용을 줄임으로써 식품 산업의 지속가능성 트렌드에 부합하는 솔루션입니다. 이 혁신은 소매업체와 브랜드가 환경 목표를 달성하는 데 도움을 주는 동시에 신선 농산물을 위한 편리하고 고품질의 포장재를 제공합니다. 이번 출시를 계기로 농산물 및 신선식품 분야에서 순환형 포장 솔루션의 도입이 가속화될 것으로 기대됩니다.

- 2023년 2월, 팩티브 에버그린(Pactiv Evergreen)과 미국 기업 암스티(AmSty)는 사용 후 재활용 소재를 사용한 순환형 폴리스티렌 식품 포장 제품을 출시했습니다. 이 제품을 통해 주요 식품 브랜드는 성능이나 안전성을 희생하지 않고도 지속가능성 목표를 달성할 수 있습니다. 이번 협력은 첨단 재활용 기술을 통합하여 폐기물을 줄이고 순환 경제를 촉진합니다. 내구성이 뛰어나면서도 재활용 가능한 옵션을 제공함으로써, 이 솔루션은 식품의 품질과 유통기한을 보장하는 동시에 환경 문제에도 대응합니다. 이 이니셔티브는 지속가능한 포장 분야의 혁신 기업으로서 팩티브 에버그린과 암스티의 입지를 강화하고, 상온 식품 포장 시장에서 재활용 소재의 활용 확대를 촉진합니다.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.