Global Ambient Food Packaging Market

Market Size in USD Billion

USD

5.08 Billion

USD

9.77 Billion

2025

2033

USD

5.08 Billion

USD

9.77 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.08 Billion | |

| USD 9.77 Billion | |

| % | |

|

Ambient Food Packaging Market Size

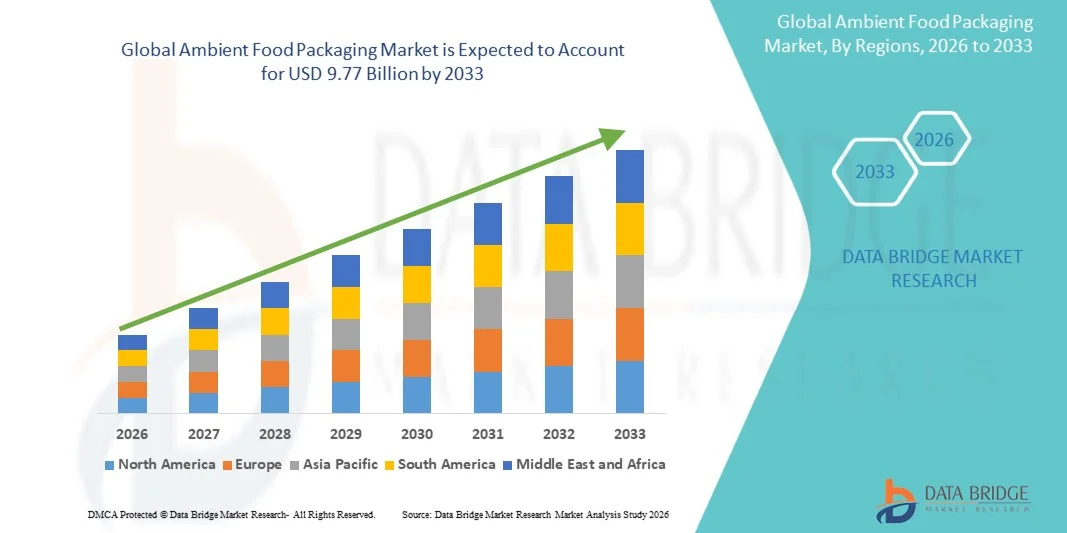

- The global ambient food packaging market size was valued at USD 5.08 billion in 2025 and is expected to reach USD 9.77 billion by 2033, at a CAGR of 8.50% during the forecast period

- The market growth is largely fuelled by the rising demand for packaged and ready-to-eat food products, increasing consumer preference for convenience, and the expansion of organized retail channels

- Growing awareness about food safety and hygiene, coupled with technological advancements in packaging materials, is driving the adoption of ambient food packaging

Ambient Food Packaging Market Analysis

- The market is witnessing robust growth due to urbanization, changing lifestyles, and the increasing penetration of processed and packaged foods

- Manufacturers are investing in research and development to create packaging that extends shelf life while maintaining food quality

- North America dominated the ambient food packaging market with the largest revenue share of 38.75% in 2025, driven by increasing demand for packaged and ready-to-eat food products, as well as rising consumer preference for convenience and long shelf-life solutions

- Asia-Pacific region is expected to witness the highest growth rate in the global ambient food packaging market, driven by growing population, increasing demand for packaged foods, rising awareness of food safety and hygiene, and adoption of modern packaging technologies

- The rigid packaging segment held the largest market revenue share in 2025 driven by its durability, ability to protect food from physical damage, and extended shelf life. Rigid packaging solutions such as cans, jars, and cartons are widely used for beverages, dairy, and processed foods, offering high structural integrity and suitability for mass production and transport

Report Scope and Ambient Food Packaging Market Segmentation

|

Attributes |

Ambient Food Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Ambient Food Packaging Market Trends

“Rising Demand for Convenient and Shelf-Stable Food Products”

• The growing preference for ready-to-eat and long-shelf-life food products is significantly shaping the ambient food packaging market, as consumers increasingly seek convenience, portability, and minimal preparation requirements. Ambient packaging solutions, such as aseptic cartons, pouches, and cans, are gaining traction due to their ability to maintain product freshness without refrigeration. This trend is driving adoption across food and beverage sectors, encouraging manufacturers to innovate with packaging that balances functionality, cost, and sustainability

• Increasing awareness about food safety, hygiene, and waste reduction has accelerated the demand for ambient food packaging. Consumers and retailers are actively seeking packaging that protects products from contamination, extends shelf life, and reduces spoilage. This has prompted collaborations between packaging material suppliers and food manufacturers to develop solutions that ensure product quality while meeting evolving regulatory and consumer standards

• Convenience, sustainability, and safety trends are influencing purchasing decisions, with manufacturers emphasizing recyclable materials, minimal packaging, and eco-friendly production processes. These factors are helping brands differentiate products in a competitive market and build consumer trust, while also driving the adoption of certification labels and environmental claims. Companies are increasingly using marketing campaigns to highlight these benefits and reinforce brand positioning

• For instance, in 2024, Tetra Pak in Sweden and Amcor in Australia expanded their packaging portfolios by introducing innovative ambient packaging formats for beverages and processed foods. These launches were in response to growing consumer preference for convenient, hygienic, and eco-conscious products, with distribution across retail, e-commerce, and foodservice channels

• While demand for ambient food packaging is growing, sustained market expansion depends on continuous innovation, cost-effective production, and maintaining packaging performance comparable to refrigerated alternatives. Manufacturers are also focusing on enhancing supply chain efficiency, improving scalability, and developing sustainable solutions to support broader adoption

Ambient Food Packaging Market Dynamics

Driver

“Growing Preference for Convenience and Long-Shelf-Life Products”

• Rising consumer demand for ready-to-eat and shelf-stable foods is a major driver for the ambient food packaging market. Manufacturers are increasingly adopting packaging that ensures product freshness without refrigeration, improves convenience, and reduces waste. This trend is also encouraging research into novel packaging materials and formats that enhance product appeal and functionality

• Expanding applications across beverages, dairy alternatives, snacks, and processed foods are influencing market growth. Ambient food packaging helps maintain product quality, protect against contamination, and improve transportability, enabling manufacturers to meet consumer expectations for safe, convenient, and durable products. Increasing urbanization and busy lifestyles further reinforce this trend

• Food and beverage manufacturers are actively promoting ambient packaging through product innovation, marketing campaigns, and sustainability initiatives. These efforts are supported by growing consumer preference for eco-friendly and hygienic products, and they also encourage partnerships between packaging suppliers and brands to enhance product protection and reduce environmental footprint

• For instance, in 2023, Nestlé in Switzerland and PepsiCo in the U.S. reported increased use of ambient packaging for dairy beverages and ready-to-drink products. This expansion followed higher consumer demand for convenient, safe, and recyclable packaging solutions, driving repeat purchases and product differentiation. Both companies highlighted sustainability and safety in marketing campaigns to strengthen consumer trust and brand loyalty

• Although rising convenience and safety trends support growth, wider adoption depends on cost optimization, material availability, and scalable production processes. Investment in supply chain efficiency, sustainable sourcing, and advanced packaging technologies will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

“Higher Cost And Limited Awareness Compared To Conventional Packaging”

• The relatively higher cost of advanced ambient packaging compared to traditional packaging remains a key challenge, limiting adoption among price-sensitive manufacturers. Higher raw material costs and complex production processes contribute to elevated pricing. In addition, fluctuating supply of sustainable packaging materials can affect cost stability and market penetration

• Consumer and manufacturer awareness remains uneven, particularly in developing markets where demand for ambient and sustainable packaging is still emerging. Limited understanding of functional and environmental benefits restricts adoption across certain product categories. This also leads to slower uptake in emerging economies where educational initiatives on ambient packaging are minimal

• Supply chain and distribution challenges also impact market growth, as ambient packaging requires sourcing from certified suppliers and adherence to stringent quality standards. Logistical complexities, specialized storage, and transportation requirements increase operational costs. Companies must invest in efficient handling and distribution networks to maintain product integrity

• For instance, in 2024, distributors in Singapore and Thailand supplying packaged beverages and ready-to-eat foods reported slower uptake due to higher prices and limited awareness of functional and environmental advantages compared to conventional packaging. Storage requirements and certification compliance were additional barriers, prompting some retailers to limit shelf space for premium ambient packaging products

• Overcoming these challenges will require cost-efficient production, expanded distribution networks, and focused educational initiatives for manufacturers and consumers. Collaboration with retailers, foodservice operators, and certification bodies can help unlock the long-term growth potential of the global ambient food packaging market. Furthermore, developing cost-competitive and sustainable packaging solutions, while emphasizing product safety and convenience, will be essential for widespread adoption

Ambient Food Packaging Market Scope

The market is segmented on the basis of packaging type, material type, and application.

• By Packaging Type

On the basis of packaging type, the ambient food packaging market is segmented into rigid packaging and flexible packaging. The rigid packaging segment held the largest market revenue share in 2025 driven by its durability, ability to protect food from physical damage, and extended shelf life. Rigid packaging solutions such as cans, jars, and cartons are widely used for beverages, dairy, and processed foods, offering high structural integrity and suitability for mass production and transport.

The flexible packaging segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its lightweight nature, cost-effectiveness, and adaptability for a variety of food products. Flexible packaging formats, such as pouches, bags, and films, are particularly popular for snacks, ready-to-eat meals, and liquid products, providing convenience, easy storage, and enhanced barrier properties to maintain product freshness.

• By Material Type

On the basis of material type, the market is segmented into metal, glass, and plastic. The metal segment held the largest market revenue share in 2025 due to its robustness, recyclability, and ability to provide an airtight seal, which preserves food quality and prevents contamination. Metal cans are widely used in processed foods, beverages, and ready-to-eat meals.

The plastic segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its lightweight properties, versatility, and suitability for innovative packaging designs. Plastic materials are increasingly used in pouches, trays, and bottles, offering convenience, cost efficiency, and compatibility with various food types.

• By Application

On the basis of application, the ambient food packaging market is segmented into fruits and vegetables, meat, fish, and poultry. The fruits and vegetables segment held the largest market revenue share in 2025 driven by the growing demand for fresh, packaged produce with extended shelf life and reduced spoilage. Ambient packaging solutions such as cartons, films, and pouches are widely used to maintain freshness and quality during transportation and retail.

The meat, fish, and poultry segment is expected to witness the fastest growth from 2026 to 2033, fueled by the rising consumption of packaged protein products and increasing preference for hygiene, convenience, and ready-to-cook options. Packaging solutions for these products are designed to prevent contamination, maintain freshness, and extend shelf life without refrigeration.

Ambient Food Packaging Market Regional Analysis

• North America dominated the ambient food packaging market with the largest revenue share of 38.75% in 2025, driven by increasing demand for packaged and ready-to-eat food products, as well as rising consumer preference for convenience and long shelf-life solutions

• Consumers in the region highly value the safety, freshness preservation, and sustainability offered by ambient food packaging across snacks, beverages, dairy, and processed foods

• This widespread adoption is further supported by high disposable incomes, a technologically inclined population, and the growth of organized retail and e-commerce channels, establishing ambient food packaging as a preferred solution for both household and commercial consumption

U.S. Ambient Food Packaging Market Insight

The U.S. ambient food packaging market captured the largest revenue share in 2025 within North America, fueled by the increasing consumption of ready-to-eat and packaged food products. Consumers are prioritizing convenience, extended shelf life, and hygiene, encouraging manufacturers to adopt innovative packaging solutions. The growth of e-commerce, retail expansion, and demand for sustainable materials further drives market adoption. Moreover, marketing campaigns emphasizing food safety and eco-friendly packaging are contributing to the market’s expansion.

Europe Ambient Food Packaging Market Insight

The Europe ambient food packaging market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing demand for sustainable, hygienic, and shelf-stable food solutions. Urbanization, busy lifestyles, and regulatory standards promoting food safety are fostering adoption. European consumers are also drawn to packaging that reduces food waste while offering convenience. Growth spans across beverages, dairy, snacks, and processed foods, with both new product launches and reformulations leveraging ambient packaging.

U.K. Ambient Food Packaging Market Insight

The U.K. ambient food packaging market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising consumer preference for convenient, ready-to-eat, and eco-friendly packaged foods. Concerns regarding food safety, waste reduction, and sustainability are encouraging manufacturers and retailers to adopt ambient packaging solutions. The country’s well-developed retail infrastructure, combined with high consumer awareness of sustainable packaging, is expected to continue supporting market growth.

Germany Ambient Food Packaging Market Insight

The Germany ambient food packaging market is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing focus on food safety, hygiene, and environmentally responsible packaging. Germany’s strong manufacturing and technological capabilities, along with consumer demand for innovative and sustainable packaging formats, support adoption in both commercial and household applications. The integration of eco-friendly packaging into product portfolios aligns with local consumer preferences for safe, high-quality, and sustainable food products.

Asia-Pacific Ambient Food Packaging Market Insight

The Asia-Pacific ambient food packaging market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising urbanization, growing disposable incomes, and increasing demand for packaged and ready-to-eat foods in countries such as China, Japan, and India. The region’s expanding retail sector, rising food safety awareness, and adoption of modern packaging technologies are fueling growth. Furthermore, the availability of cost-effective packaging materials and local manufacturing capabilities is making ambient packaging more accessible to a wider consumer base.

Japan Ambient Food Packaging Market Insight

The Japan ambient food packaging market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s busy urban lifestyle, high disposable income, and demand for convenience. Consumers prioritize packaged foods with extended shelf life, hygiene, and quality preservation. The growing adoption of ready-to-eat meals, processed beverages, and retail innovations, coupled with sustainable packaging initiatives, is driving market growth.

China Ambient Food Packaging Market Insight

The China ambient food packaging market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding middle class, rapid urbanization, and increasing demand for packaged and shelf-stable foods. China represents one of the largest markets for processed and ready-to-eat foods, with ambient packaging widely adopted in household, commercial, and foodservice sectors. Government initiatives promoting food safety, modern retail expansion, and the presence of strong domestic packaging manufacturers are key factors propelling the market in China.

Ambient Food Packaging Market Share

The Ambient Food Packaging industry is primarily led by well-established companies, including:

- FFP Packaging Solutions Ltd (U.K.)

- Berry Global Inc. (U.S.)

- Amcor Limited (Australia)

- SIG Combibloc Obeikan (Switzerland)

- Tetra Pak (Sweden)

- Rexam (U.K.)

- Bemis (U.S.)

- Mondi (Austria)

- Ampac (U.S.)

- Dupont (U.S.)

- Excelsior Technologies (U.K.)

- KM Packaging Services Ltd. (U.K.)

- Marsden Holding LLC (U.S.)

Latest Developments in Global Ambient Food Packaging Market

- In August 2023, Amcor (Australia) announced a partnership with a leading food manufacturer to develop a new line of fully recyclable ambient food packaging. The initiative focuses on creating sustainable solutions that reduce environmental impact while maintaining food quality and shelf life. By leveraging Amcor’s packaging expertise, the partnership aims to deliver high-performance, eco-friendly options for a growing demand for responsible packaging. This move strengthens Amcor’s position as a leader in sustainable packaging and supports brands in meeting consumer expectations for environmentally conscious products. The collaboration is expected to drive adoption of recyclable packaging across the ambient food sector

- In September 2023, Sealed Air (U.S.) launched an innovative smart packaging technology integrating IoT capabilities to monitor product freshness in real-time. This technology allows manufacturers and retailers to track food quality throughout the supply chain, reducing spoilage and waste. By providing real-time data on product conditions, the solution enhances consumer safety and confidence in packaged foods. The adoption of smart packaging positions Sealed Air as a leader in tech-driven ambient food solutions and supports the broader trend of digitalization in food supply chains. The innovation also offers competitive differentiation in a market increasingly focused on sustainability and convenience

- In July 2023, Mondi Group (U.K.) expanded its operations in Southeast Asia by acquiring a local packaging firm specializing in ambient food solutions. The acquisition allows Mondi to broaden its product portfolio and offer innovative, high-quality packaging tailored to regional market needs. Leveraging the local company’s distribution networks and market knowledge, Mondi strengthens its competitive presence in a rapidly growing region. The move also enhances its ability to serve both multinational and local food brands with sustainable packaging solutions. This strategic expansion aligns with increasing demand for hygienic, convenient, and eco-friendly packaging in Asia-Pacific markets

- In August 2023, Amcor (North America) launched AmFiber™ high-barrier performance paper packaging designed for ambient food products. The packaging provides optimal barrier properties, extended shelf life, and efficient machine performance while being fully curbside-recyclable. This innovation addresses both environmental concerns and operational needs, offering brands a sustainable alternative to conventional packaging. By combining high performance with eco-friendliness, AmFiber™ supports the growing consumer preference for recyclable packaging. The launch is expected to influence market adoption of paper-based solutions in ambient food packaging, particularly for brands emphasizing sustainability and product quality

- In July 2023, Melodea introduced MelOx NGen, a high-performance barrier product designed for recyclable plastic food packaging. The product enables recyclability without compromising barrier properties, ensuring product freshness and extending shelf life. By facilitating sustainable packaging solutions, MelOx NGen helps food manufacturers meet regulatory requirements and consumer expectations for eco-friendly products. The innovation also supports circular economy initiatives by allowing post-consumer recycling of packaging materials. This launch strengthens Melodea’s position as a provider of sustainable packaging solutions and drives broader adoption of recyclable plastics in the ambient food market

- In July 2023, Cascades (Canada) launched a closed basket made of recycled and recyclable corrugated cardboard for the produce sector. The packaging provides an eco-friendly alternative for fruits and vegetables, promoting recyclability while maintaining product protection. By reducing reliance on non-recyclable materials, the solution aligns with growing sustainability trends in the food industry. The innovation supports retailers and brands in meeting environmental targets while offering convenient, high-quality packaging for fresh produce. This launch is expected to accelerate the adoption of circular packaging solutions in the produce and fresh food sectors

- In February 2023, Pactiv Evergreen and AmSty (U.S.) launched circular polystyrene food packaging products using post-consumer recycled content. These products allow major food brands to achieve sustainability goals without sacrificing performance or safety. The collaboration integrates advanced recycling technologies, reducing waste and promoting a circular economy. By offering durable and recyclable options, the solution addresses environmental concerns while supporting food quality and shelf life. This initiative enhances Pactiv Evergreen and AmSty’s positions as innovators in sustainable packaging, encouraging broader adoption of recycled-content materials in the ambient food packaging market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Ambient Food Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Ambient Food Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Ambient Food Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.