Global Chemical Surface Treatments Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

16.09 Billion

USD

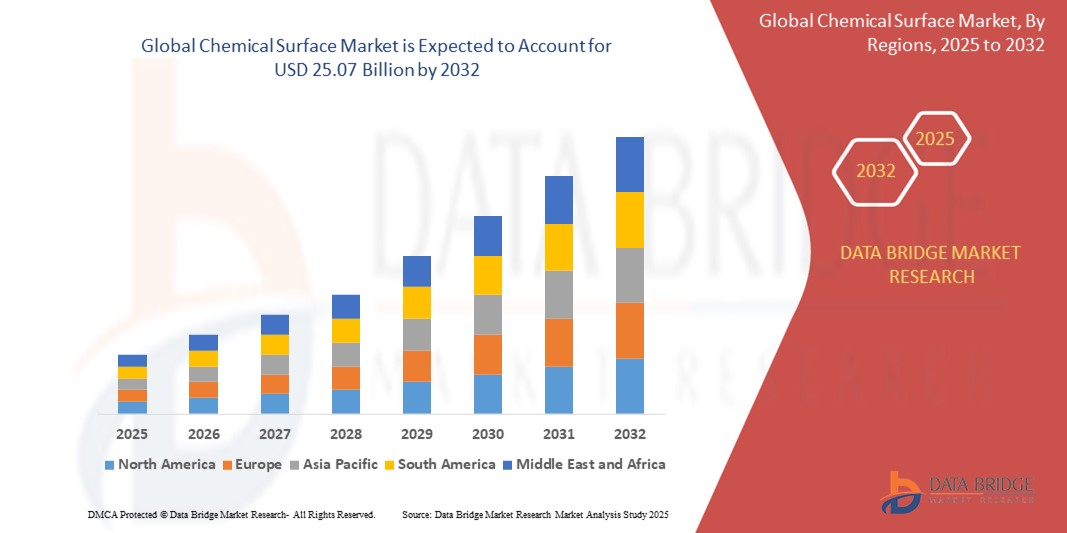

25.07 Billion

2024

2032

USD

16.09 Billion

USD

25.07 Billion

2024

2032

| 2025 –2032 | |

| USD 16.09 Billion | |

| USD 25.07 Billion | |

| % | |

|

글로벌 화학 표면 시장 세분화, 제품별(도금 화학 물질, 전환 코팅, 활성화제, 페인트 제거제, 세정제, 금속 가공액 등), 기본(금속, 플라스틱, 목재 등), 응용 분야(금속 착색제, 부식 방지제, 후처리, 전처리 세정제, 전처리 컨디셔너, 장식, 식재 등), 최종 사용자(건축 및 건설, 운송, 항공우주 및 방위, 비철 금속, 가전제품, 일반 산업, 산업 기계, 전자, 페인트 및 코팅 등) - 산업 동향 및 2032년까지의 전망

화학 표면 시장 규모

- 글로벌 화학 표면 시장 규모는 2024년에 160억 9천만 달러 로 평가되었으며 예측 기간 동안 5.70%의 CAGR 로 2032년까지 250억 7천만 달러에 도달할 것으로 예상됩니다 .

- 이러한 성장은 자동차 및 항공우주 산업의 수요 증가, 표면 처리 기술의 발전, 전자 및 건설 부문의 응용 프로그램 증가와 같은 요인에 의해 촉진됩니다.

화학 표면 시장 분석

- 화학 표면 처리 시장은 자동차, 건설, 전자 등 다양한 산업 분야에서 수요가 증가함에 따라 꾸준한 성장을 경험하고 있습니다.

- 현재 추세는 제품 내구성과 표면 성능을 개선하는 친환경적이고 고급 처리 솔루션으로의 강력한 전환을 보여줍니다.

- 북미는 잘 확립된 제조 부문, 자동차 및 항공우주 산업의 강력한 수요, 혁신과 생산 능력을 주도하는 주요 시장 참여자의 존재로 인해 화학 표면 시장을 지배할 것으로 예상됩니다.

- 아시아 태평양 지역은 급속한 산업화, 자동차 및 전자 산업의 확장, 인프라 및 지속 가능한 표면 처리 기술에 대한 투자 증가로 인해 예측 기간 동안 화학 표면 시장에서 가장 빠르게 성장하는 지역이 될 것으로 예상됩니다.

- 도금 화학 분야는 금속 부품의 내식성, 내구성, 그리고 미적 감각을 향상시키는 데 광범위하게 사용되어 2025년 화학 표면 처리 시장에서 42.36%의 가장 큰 점유율을 차지하며 시장을 장악할 것으로 예상됩니다 . 도금 화학 분야는 자동차, 전자, 항공우주 등 고성능 표면 마감이 필수적인 주요 산업에 광범위하게 적용됩니다. 제조업에서 금속 마감 솔루션에 대한 수요 증가는 도금 화학 분야의 시장 지배력을 더욱 강화하고 있습니다.

보고서 범위 및 화학 표면 시장 세분화

|

속성 |

화학 표면 주요 시장 통찰력 |

|

다루는 세그먼트 |

|

|

포함 국가 |

북아메리카

유럽

아시아 태평양

중동 및 아프리카

남아메리카

|

|

주요 시장 참여자 |

|

|

시장 기회 |

|

|

부가가치 데이터 정보 세트 |

Data Bridge Market Research에서 큐레이팅한 시장 보고서에는 시장 가치, 성장률, 세분화, 지리적 적용 범위, 주요 업체 등 시장 시나리오에 대한 통찰력 외에도 수입 수출 분석, 생산 능력 개요, 생산 소비 분석, 가격 추세 분석, 기후 변화 시나리오, 공급망 분석, 가치 사슬 분석, 원자재/소모품 개요, 공급업체 선택 기준, PESTLE 분석, Porter 분석 및 규제 프레임워크가 포함됩니다. |

화학 표면 시장 동향

"친환경 표면 처리 솔루션 채택 증가"

- 제조업체들은 글로벌 지속 가능성 표준을 준수하고 환경 영향을 줄이기 위해 점점 더 환경 친화적인 화학 표면 처리로 전환하고 있습니다.

- 수성 및 크롬 무첨가 표면 처리가 특히 자동차 및 항공우주 분야에서 기존 방법에 비해 안전한 대안으로 주목을 받고 있습니다.

- 주요 산업계가 친환경 기술에 투자를 시작했습니다.

- 예를 들어, Henkel은 자동차 제조에 사용되는 금속 표면에 대한 지속 가능한 전처리 공정을 도입했습니다.

- 정부와 규제 기관은 환경 규정을 강화하고 있으며, 이로 인해 기업들은 덜 위험한 제형으로 혁신을 추진하고 있습니다.

- For instance, the European Union’s REACH regulation has led many firms to eliminate toxic substances from their processes

Chemical Surface Market Dynamics

Driver

“Rising Demand from The Automotive and Aerospace Industries”

- The automotive and aerospace industries are major consumers of chemical surface treatments, using them to improve durability, appearance, and resistance to corrosion in components

- In automotive manufacturing, treatments such as anodizing and phosphating are essential for ensuring paint adhesion and extending the life of parts under harsh conditions

- For instance, BMW uses advanced pretreatment methods to improve corrosion resistance in electric vehicles

- Aerospace components are exposed to high altitudes and extreme temperatures, requiring treatments that maintain structural integrity and safety

- For instance, Boeing employs passivation and anodizing to protect critical aircraft parts

- The increasing production of electric vehicles and the growing demand for air travel are driving consistent growth in these sectors, fueling the need for reliable surface treatment solutions

- This sustained demand encourages manufacturers to invest in innovation, focusing on more efficient, high-performance, and sustainable chemical surface treatment technologies to meet evolving industry needs

Opportunity

“Growth in Emerging Economies Due to Industrialization”

- Rapid industrialization in emerging economies like India and Indonesia is creating a surge in demand for chemical surface treatments, especially in automotive, construction, and electronics manufacturing

- For instance, India’s automotive sector is projected to become the world’s third-largest by 2030, driving demand for corrosion-resistant surface coatings

- Infrastructure development and urbanization are pushing the need for durable and treated materials, especially in public works and housing

- For instance, Indonesia’s $35 billion infrastructure roadmap includes new highways, airports, and ports, all requiring treated metal and concrete surfaces

- Government initiatives like “Make in India” and China’s “Made in China 2025” promote local manufacturing and quality standards, encouraging industries to adopt advanced surface treatments to meet global requirements

- Low penetration of advanced technologies offers a first-mover advantage for companies that can provide cost-effective, scalable, and environmentally compliant surface treatment solutions

- Rising consumer and industrial awareness of product lifespan, appearance, and performance is increasing the adoption of quality surface treatments in everyday manufacturing

Restraint/Challenge

“High Cost and Complexity Associated with Adopting Advanced Technologies”

- Adopting advanced and environmentally compliant chemical surface treatments involves high costs and technical complexity, making it a major challenge for the industry

- Transitioning to sustainable methods requires significant investment in R&D, equipment, and workforce training; for instance, smaller firms often struggle to afford new treatment systems that meet green standards

- Eco-friendly alternatives may not always match the performance of traditional treatments in sectors such as aerospace and defense, limiting their immediate application

- Global companies face difficulties complying with different regulatory standards across countries, requiring customized solutions and increasing operational complexity

- For instance, AkzoNobel faced delays in launching a chromium-free coating line due to the need to meet differing environmental compliance requirements in both the U.S. and Europe, highlighting the complexity of international regulation in sustainable innovation

Chemical Surface Market Scope

The market is segmented on the basis of product, base, application, and end-user.

|

Segmentation |

Sub-Segmentation |

|

By Product |

|

|

By Base |

|

|

By Application |

|

|

By End-User |

|

In 2025, the plating chemicals is projected to dominate the market with a largest share in product segment

The plating chemicals segment is expected to dominate the chemical surface market with the largest share of 42.36% in 2025 due to its extensive use in enhancing corrosion resistance, durability, and aesthetic appeal of metal components. Its applications span key industries such as automotive, electronics, and aerospace, where high-performance surface finishes are essential. The growing demand for metal finishing solutions in manufacturing is further fuelling this segment’s dominance.

The conversion coating is expected to account for the largest share during the forecast period in product segment

In 2025, the conversion coating segment is expected to dominate the market with the largest market share of 31.84% due to its critical role in improving paint adhesion and protecting surfaces from corrosion. Widely used in pre-treatment processes, especially in automotive and industrial applications, these coatings enhance surface performance and longevity. Their compatibility with eco-friendly formulations also supports their expanding use across regulated industries.

Chemical Surface Market Regional Analysis

“North America Holds the Largest Share in the Chemical Surface Market”

- North America holds the largest share of the global chemical surface treatment market, accounting for approximately 38.5%.

- The U.S. leads the North American market, driven by a robust automotive and aerospace industry demanding advanced surface treatment solutions

- General Motors와 같은 회사가 EV 포트폴리오를 확장하면서 이 지역은 전기 자동차 (EV) 생산에 중점을 두고 표면 처리에 대한 수요가 증가합니다.

- 미국의 기술 발전과 전략적 파트너십은 화학 표면 처리 분야의 혁신을 촉진하고 있습니다.

- 주요 시장 참여자의 존재와 강력한 제조 기반은 북미의 시장 지배력에 기여합니다.

“아시아 태평양 지역은 화학 표면 시장에서 가장 높은 CAGR을 기록할 것으로 예상됩니다.”

- 아시아 태평양 지역은 화학 표면 시장에서 가장 빠르게 성장하는 지역입니다.

- 중국, 인도 등 국가의 급속한 산업화로 인해 다양한 분야에서 화학 표면 처리에 대한 수요가 증가하고 있습니다.

- 자동차 제조 분야에서 중국의 우위는 2,600만 대 이상의 차량을 생산하여 표면 처리 화학 시장 규모를 크게 확대하고 있습니다.

- 아시아 태평양 지역 전역의 인프라 개발에 대한 정부 이니셔티브와 투자가 시장 성장을 촉진하고 있습니다.

- 지속 가능하고 친환경적인 표면 처리 솔루션에 대한 이 지역의 관심이 점차 커지면서 글로벌 환경 표준에 부합합니다.

화학 표면 시장 점유율

시장 경쟁 구도는 경쟁사별 세부 정보를 제공합니다. 여기에는 회사 개요, 회사 재무 상태, 매출 창출, 시장 잠재력, 연구 개발 투자, 신규 시장 진출, 글로벌 입지, 생산 시설 및 설비, 생산 능력, 회사의 강점과 약점, 제품 출시, 제품 종류 및 범위, 응용 분야별 우위 등이 포함됩니다. 위에 제공된 데이터는 해당 회사의 시장 집중도와 관련된 데이터입니다.

시장에서 활동하는 주요 시장 리더는 다음과 같습니다.

- 엘리먼트 솔루션즈 주식회사 (미국)

- NOF 주식회사 (일본)

- 아토텍 (독일)

- Henkel AG & Co. KGaA (독일)

- 케메탈 주식회사 (독일)

- 니혼 파커라이징 주식회사(일본)

- PPG Industries, Inc.(미국)

- 닛폰 페인트 홀딩스 주식회사(일본)

- 솔베이(벨기에)

- OC Oerlikon Management AG (스위스)

- McGean-Rohco Inc.(미국)

- JCU CORPORATION(일본)

- 플랫폼 스페셜티 프로덕츠 코퍼레이션(미국)

- 퀘이커 케미컬 코퍼레이션(미국)

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.