Global Orthopedic Joint Reconstruction Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

19.92 Billion

USD

27.06 Billion

2024

2032

USD

19.92 Billion

USD

27.06 Billion

2024

2032

| 2025 –2032 | |

| USD 19.92 Billion | |

| USD 27.06 Billion | |

| % | |

|

Global Orthopedic Joint Reconstruction Market Segmentation, By Product Type (Demineralized Bone Matrix, Allograft, Bone Morphogenetic Protein, Visco supplementation Products, Synthetic Bone Substitutes, and Others), Joint Type (Knee, Hip, Shoulder, Ankle, and Other), Procedure (Total, Partial, and Others), Technique (Joint Replacement, Implants, Bone Graft, Osteotomy, Arthroscopy, Resurfacing, and Arthrodesis), Biomaterial (Metallic, Polymeric, Ceramic, and Natural), End-User (Hospitals and Ambulatory Centers, Research, and Academic Institute)- Industry Trends and Forecast to 2032

Orthopedic Joint Reconstruction Market Size

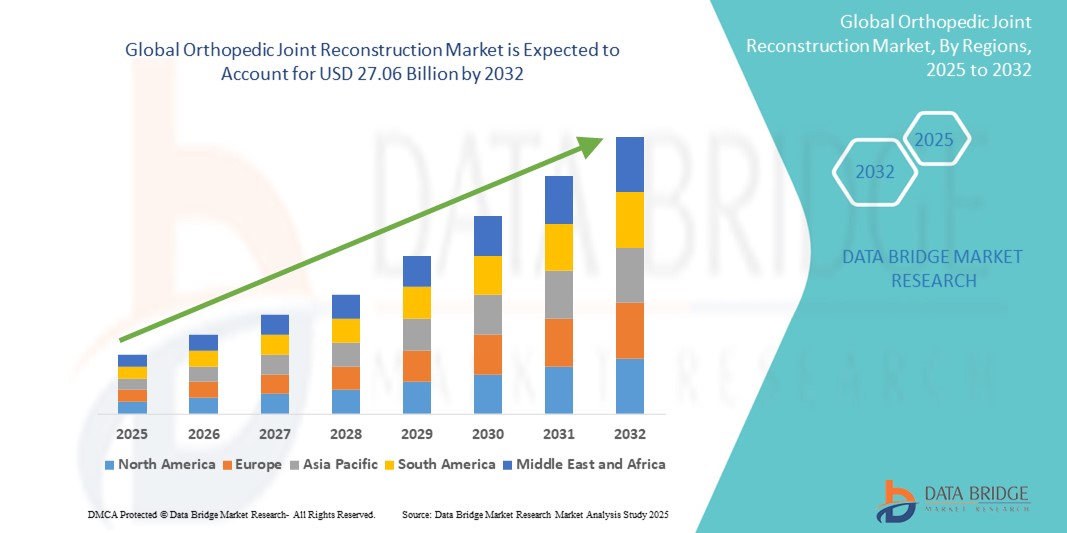

- The global orthopedic joint reconstruction market size was valued atUSD 19.92 billion in 2024and is expected to reachUSD 27.06 billion by 2032, at aCAGR of 3.90 %during the forecast period

- This growth is driven by factors such as the increasing aging population, rising prevalence of joint disorders, advancements in surgical techniques and implants, and growing demand for minimally invasive procedures

Orthopedic Joint Reconstruction Market Analysis

- The orthopedic joint reconstruction market is experiencing steady growth due to the increasing number of joint replacement surgeries globally, driven by aging populations and a rise in orthopedic conditions. This growth reflects a higher demand for advanced surgical procedures and innovative products

- Technological advancements in joint reconstruction implants and surgical techniques are significantly improving outcomes and recovery times. These innovations are expanding the market potential by enhancing patient satisfaction and surgical precision

- North America is expected to dominate the orthopedic joint reconstructions market due to its advanced healthcare infrastructure, high adoption of innovative medical technologies, and a large aging population requiring joint replacement surgeries.

- Asia-Pacific is expected to be the fastest growing region in the Orthopedic Joint Reconstruction market during the forecast period due to increasing healthcare access, a rising aging population, and growing awareness of orthopedic treatments.

- Allografts segment is expected to dominate the global orthopedic joint reconstruction market holding a major market share 60.7% in 2025, due to the osteoconductivity, reduced surgical time, and wide availability through tissue banks.

Report Scope and Orthopedic Joint Reconstruction Market Segmentation

|

Attributes |

Orthopedic Joint Reconstruction Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Orthopedic Joint Reconstruction Market Trends

“Increasing Adoption of Robotic andAIIntegration in Joint Reconstruction”

- Robotic-assisted systems enable sub-millimeter accuracy in joint replacement surgeries, significantly reducing variability in implant placement

- For instance, The Mako SmartRobotics system by Stryker uses CT-based planning and robotic arm assistance to enhance accuracy in total knee arthroplasty

- Personalized surgical plans are created using preoperative imaging (such as 3D CT scans), tailored to each patient's unique anatomy and biomechanics

- AI analyzes large datasets from previous cases to guide surgeons in selecting optimal surgical approaches and implant types based on specific patient profiles

- Precise alignment and balancing of soft tissues reduce complications such as implant loosening, malalignment, and abnormal wear

- Enhanced accuracy leads to quicker recovery times, reduced postoperative pain, and improved long-term outcomes for patients

- Hospitals adopting these technologies report higher patient satisfaction scores and lower revision rates over time

- For instance, A 2023 study in the Journal of Arthroplasty showed that robotic-assisted knee replacements had a 37% lower revision rate compared to manual procedures over a 2-year follow-up

Orthopedic Joint Reconstruction Market Dynamics

Driver

“Rising Geriatric Population and Associated Joint Disorders”

- The global elderly population is growing rapidly, with the WHO estimating 2.1 billion people aged 60+ by 2050, directly increasing cases of osteoarthritis and other joint-related disorders

- Older adults frequently suffer from reduced joint mobility and chronic pain, making them prime candidates for hip, knee, and shoulder replacements

- Technological improvements in surgical techniques and implants are leading to quicker recovery and higher success rates among elderly patients

- For instance, A 2023 report in The Journal of Arthroplasty highlighted a 30% improvement in mobility post-surgery among patients over 70 when robotic assistance was used

- In high-income countries, strong healthcare infrastructure and insurance coverage make joint replacement surgeries more accessible to aging populations

- For instance, Medicare in the US covers most costs for total joint replacements, making them one of the most common elective surgeries among seniors

- Medical device companies are developing implants specifically for geriatric patients, designed for lower bone density and minimal surgical trauma, ensuring safer procedures and better outcomes

Opportunity

“Rising Demand for Minimally Invasive Joint Reconstruction”

- The growing preference for minimally invasive surgery (MIS) is a key opportunity in the orthopedic joint reconstruction market, as it offers reduced pain, faster recovery, and smaller incisions compared to traditional open surgery

- For instance, the adoption of minimally invasive knee and hip replacement surgeries has significantly increased in recent years, with MIS techniques now accounting for nearly 30% of total joint replacement procedures in the U.S.

- MIS procedures often result in shorter hospital stays and quicker return to normal activities, which is appealing to both patients and healthcare providers looking to optimize surgical throughput and minimize costs

- For instance, A 2023 study in the Journal of Orthopaedic Surgery found that patients undergoing minimally invasive hip replacement reported a 25% faster recovery time and 40% less post-surgery pain compared to traditional open surgery

- The rise in outpatient facilities and ASCs, which focus on faster recovery times and fewer complications, is driving the demand for these types of procedures, expanding market opportunities for orthopedic companies focusing on these innovations

- Increased patient demand for less invasive procedures, along with advancements in tools and techniques, is encouraging hospitals to adopt MIS technology, expanding the reach of joint reconstruction to a broader population

- These technologies also lower the risk of infection, which is a significant concern in joint replacement surgeries, further motivating their growth in the global market

Restraint/Challenge

“Limited Access to Advanced Technologies”

- High upfront costs of robotic surgical systems and AI-based platforms restrict adoption to large urban hospitals, leaving rural and underfunded healthcare facilities behind

- For instance, Robotic systems such as Stryker’s Mako or Zimmer Biomet’s ROSA can cost upwards of USD 1 million, not including maintenance and disposable components

- Many healthcare systems in low- and middle-income countries lack the infrastructure and funding required to adopt high-tech orthopedic solutions

- Limited insurance reimbursement for robotic or AI-assisted surgeries in some regions discourages hospitals from investing in these technologies

- For instance, in many parts of Asia and Latin America, robotic joint replacements are often considered elective and are not fully covered by public or private insurers

- A steep learning curve and lack of widespread training programs make it difficult for surgeons, especially in remote areas, to gain the expertise needed to safely use advanced systems

- Disparities in access to cutting-edge technologies result in unequal surgical outcomes, with urban patients benefitting from precision tools while others rely on conventional, less accurate techniques

Orthopedic Joint Reconstruction Market Scope

The market is segmented on the basis of product type, joint type, procedure, technique, biomaterial, and end-user.

|

Segmentation |

Sub-Segmentation |

|

By Product Type |

|

|

By Joint Type |

|

|

By Procedure |

|

|

By Technique |

|

|

By Biomaterial |

|

|

By End-User |

|

In 2025, the allografts is projected to dominate the market with a largest share in product type segment

The allografts segment is expected to dominate the orthopedic joint reconstruction market with the largest share of 60.7% in 2025 due to its osteoconductivity, reduced surgical time, and wide availability through tissue banks.

The synthetic bone substitutes is expected to account for the largest share during the forecast period in Product Type market

In 2025, the synthetic bone substitutes segment is expected to dominate the market with the largest market share of 35.5% due to its better biocompatibility, lower risk of disease transmission, and continuous innovation in bioactive materials.

Orthopedic Joint Reconstruction Market Regional Analysis

“North America Holds the Largest Share in the orthopedic joint reconstruction Market”

- North America dominates the orthopedic joint reconstruction Market holding 35.5% share of the market

- The high prevalence of orthopedic disorders, with around 21.2% of U.S. adults diagnosed with arthritis, driving demand for joint surgeries

- Advanced healthcare infrastructure, with over 790,000 knee and 544,000 hip replacements performed annually in the U.S.

- Technological innovations such as AI integration and robotic surgery enhancing surgical precision and treatment outcomes

- An aging population in North America, which is increasing the need for joint replacement surgeries

“Asia-Pacific is Projected to Register the Highest CAGR in the orthopedic joint reconstruction Market”

- The Asia-Pacific region is the fastest-growing market for orthopedic joint reconstruction, driven by increasing healthcare access, aging populations, and rising demand for advanced surgical solutions.

- Arthroscopy is the fastest-growing technique segment in the region, reflecting a shift towards minimally invasive procedures

- Japan is expected to register the highest CAGR from 2024 to 2030, indicating a strong demand for joint reconstruction solutions

- The increasing prevalence of osteoporosis and arthritis in countries such as China and India is driving the need for effective orthopedic interventions

Orthopedic Joint Reconstruction Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Zimmer Biomet(U.S.)

- Stryker(U.S.)

- Johnson & Johnson Private Limited(U.S.)

- Smith+Nephew(U.K.)

- Arthrex, Inc(U.S.)

- Exactech, Inc (U.S.)

- Corin Group (U.K.)

- DJO LLC (U.S.)

- Beijing Chunlizhengda Medical Instruments Co.,Ltd (China)

- B. Braun Melsungen AG (Germany)

- GROUP FH ORTHO communication (U.S.)

- Limacorporate S.p.a. (Italy)

- Japan MDM, Inc (Japan)

- PETER BREHM GmbH (Germany)

- Exactech, Inc (U.S.)

- United Orthopedic Corporation (Taiwan)

Latest Developments in Global Orthopedic Joint Reconstruction Market

- In July 2022, Enovis Corporation launched ARVIS, the first FDA-cleared augmented reality (AR) surgical guidance system for total hip and knee replacement surgeries. This hands-free, wearable device provides real-time, in-surgical-field guidance to orthopedic surgeons, enhancing precision. ARVIS aims to improve patient outcomes, reduce costs, and expand access to advanced surgical technology, especially in ambulatory surgical centers. Its compact design also reduces the need for disposable instruments, promoting a more sustainable and efficient operating room environment

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.