Global Polyoxin Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

1.57 Billion

USD

2.12 Billion

2025

2033

USD

1.57 Billion

USD

2.12 Billion

2025

2033

| 2026 –2033 | |

| USD 1.57 Billion | |

| USD 2.12 Billion | |

| % | |

|

Global Polyoxin Market Segmentation, By Product Type (Polyoxin B and Polyoxin D), Crop Type (Polyoxin B by Crop Type and Polyoxin D by Crop Type), Formulation (Wettable Powder (WP), Emulsifiable Concentrate (EC), and Dustable Powder (DP)) - Industry Trends and Forecast to 2033

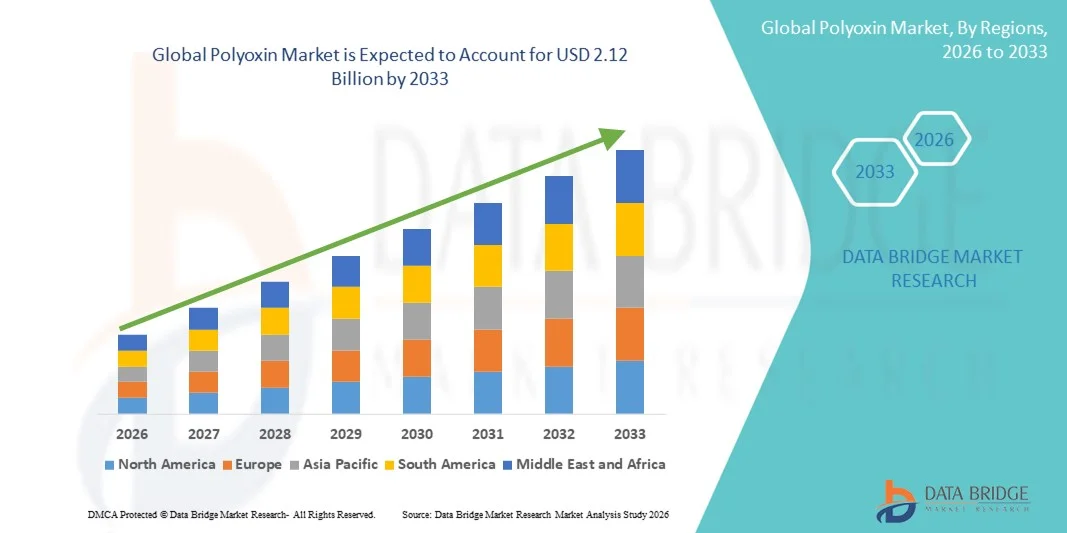

What is the Global Polyoxin Market Size and Growth Rate?

- The global polyoxin market size was valued at USD 1.57 billion in 2025 and is expected to reach USD 2.12 billion by 2033, at a CAGR of3.80% during the forecast period

- Growing awareness about the benefits of polyoxin such as minimal toxicity will emerge as the major factor fostering the growth of polyoxin market

- Also, rising environmental concerns in regards to soil quality conservation and increased crop production especially in the developing economies are other factors fostering the growth of polyoxin market

What are the Major Takeaways of Polyoxin Market?

- Growth in the expenditure for research and development proficiencies in regards to new product launches, rising food safety concerns and increasing personal disposable income will further create lucrative and remunerative growth opportunities for the polyoxin market

- Growth and expansion of agrochemicals industry in the developing economies, surging globalization and growing initiatives by the government to promote industrialization will also carve the way for the growth of the polyoxin market

- North America dominated the polyoxin market with a 42.26% revenue share in 2025, driven by strong growth in agrochemical adoption, advanced crop protection programs, and extensive R&D investments across the U.S. and Canada. Increasing demand for biofungicides, high-efficiency formulations, and sustainable agriculture practices continues to fuel Polyoxin adoption across rice, vegetable, and horticultural crops

- Asia-Pacific is projected to register the fastest CAGR of 8.19% from 2026 to 2033, driven by rising adoption of modern crop protection techniques, government incentives for sustainable agriculture, and rapid growth in rice, vegetable, and fruit cultivation across China, India, Japan, South Korea, and Southeast Asia

- The Polyoxin B segment dominated the market with a 52.3% share in 2025, owing to its broad-spectrum antifungal activity, high efficacy against major crop diseases such as rice blast and cucumber powdery mildew, and widespread adoption across both conventional and organic farming practices

Report Scope and Polyoxin Market Segmentation

|

Attributes |

Polyoxin Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Polyoxin Market?

Increasing Shift Toward High-Efficiency, Sustainable, and Targeted Polyoxins

- The polyoxin market is witnessing strong adoption of innovative, environmentally friendly, and highly targeted formulations designed to improve crop protection, minimize chemical residues, and ensure sustainable agriculture practices

- Manufacturers are introducing multi-component, high-purity, and biocontrol-integrated Polyoxin products that offer enhanced stability, broad-spectrum efficacy, and compatibility with modern integrated pest management (IPM) systems

- Growing demand for cost-effective, scalable, and field-deployable Polyoxin solutions is driving usage across large-scale farms, greenhouse operations, and organic cultivation projects

- For instance, companies such as UPL, BASF SE, Bayer AG, Syngenta, and FMC Corporation have upgraded their Polyoxin portfolios with higher potency, extended shelf-life, and formulation innovations to support improved crop yields and reduced environmental impact

- Increasing need for precision agriculture, sustainable disease control, and reduced chemical dependency is accelerating the shift toward bio-based and hybrid Polyoxin solutions

- As crop protection strategies become more complex and regulatory pressures increase, Polyoxins will remain vital for effective fungal disease management and sustainable farming practices

What are the Key Drivers of Polyoxin Market?

- Rising demand for efficient, selective, and eco-friendly fungicides to support disease management in crops such as fruits, vegetables, and cereals is fueling polyoxin adoption

- For instance, in 2025, leading companies including UPL, BASF SE, and Bayer AG launched advanced Polyoxin formulations with improved solubility, broader crop compatibility, and enhanced antifungal activity

- Growing adoption of integrated pest management (IPM), organic farming, and precision agriculture practices is boosting demand for Polyoxins across the U.S., Europe, and Asia-Pacific

- Advancements in formulation technologies, controlled-release mechanisms, and field-applicable delivery systems have strengthened efficacy, safety, and convenience for end-users

- Increasing regulatory focus on reducing chemical residues and promoting sustainable agriculture is creating demand for highly targeted and biodegradable Polyoxin products

- Supported by steady investments in agricultural R&D, crop protection innovation, and sustainable farming programs, the polyoxin market is expected to witness strong long-term growth

Which Factor is Challenging the Growth of the Polyoxin Market?

- High costs associated with premium, bio-based, and multi-component Polyoxins restrict adoption among smallholder farmers and emerging markets

- For instance, during 2024–2025, fluctuations in raw material prices, manufacturing lead times, and global supply chain constraints increased production costs for several Polyoxin manufacturers

- Complexity in developing stable, field-ready, and environmentally safe Polyoxin formulations increases the need for specialized expertise, testing, and regulatory compliance

- Limited awareness in certain emerging markets regarding Polyoxin efficacy, application methods, and disease-targeting advantages slows adoption

- Competition from conventional fungicides, alternative biopesticides, and multi-mode chemical formulations creates pricing pressure and reduces differentiation

- To address these challenges, companies are focusing on cost-optimized, high-efficacy formulations, farmer training programs, digital crop monitoring support, and regulatory-compliant innovations to increase global adoption of Polyoxins

How is the Polyoxin Market Segmented?

The market is segmented on the basis of product type, crop type, and formulation.

- By Product Type

On the basis of product type, the polyoxin market is segmented into Polyoxin B and Polyoxin D. The Polyoxin B segment dominated the market with a 52.3% share in 2025, owing to its broad-spectrum antifungal activity, high efficacy against major crop diseases such as rice blast and cucumber powdery mildew, and widespread adoption across both conventional and organic farming practices. Polyoxin B is preferred by large-scale farms and greenhouse operations due to its proven reliability, ease of application, and compatibility with integrated pest management (IPM) programs.

The Polyoxin D segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for targeted disease management, development of improved formulations with enhanced stability, and rising cultivation of high-value crops requiring precise fungal control. Ongoing R&D, farmer awareness programs, and regulatory support for bio-based fungicides are expected to accelerate the adoption of Polyoxin D globally.

- By Crop Type

On the basis of crop type, the polyoxin market is segmented into Polyoxin B by Crop Type and Polyoxin D by Crop Type. The Polyoxin B by Crop Type segment dominated the market in 2025 with a 49.6% share, largely due to its extensive use in staple crops such as rice, wheat, and vegetables, which face high susceptibility to fungal pathogens. Farmers and agribusinesses rely on Polyoxin B for its proven efficacy, safety profile, and cost-effectiveness in large-scale applications.

The Polyoxin D by Crop Type segment is expected to grow at the fastest CAGR from 2026 to 2033, fueled by increasing cultivation of high-value fruits, vegetables, and horticultural crops that require precise fungal control and minimal residue. Enhanced formulations, compatibility with organic and IPM systems, and rising awareness of sustainable disease management practices are driving the global uptake of crop-specific Polyoxin D applications.

- By Formulation

On the basis of formulation, the polyoxin market is segmented into Wettable Powder (WP), Emulsifiable Concentrate (EC), and Dustable Powder (DP). The Wettable Powder (WP) segment dominated the market with a 46.8% share in 2025, driven by its ease of handling, water dispersibility, broad-spectrum effectiveness, and suitability for large-scale agricultural spraying systems. WP formulations remain widely preferred among farmers and agrochemical distributors due to their stability, affordability, and compatibility with most spraying equipment.

The Emulsifiable Concentrate (EC) segment is projected to grow at the fastest CAGR from 2026 to 2033, propelled by increasing demand for concentrated, highly soluble formulations suitable for high-value crops and greenhouse applications. Innovations in formulation technology, improved solubility, and reduced application frequency are enhancing efficiency and boosting adoption across emerging and developed markets.

Which Region Holds the Largest Share of the Polyoxin Market?

- North America dominated the polyoxin market with a 42.26% revenue share in 2025, driven by strong growth in agrochemical adoption, advanced crop protection programs, and extensive R&D investments across the U.S. and Canada. Increasing demand for biofungicides, high-efficiency formulations, and sustainable agriculture practices continues to fuel Polyoxin adoption across rice, vegetable, and horticultural crops

- Leading companies in North America are introducing advanced Polyoxin formulations, including high-stability powders, emulsifiable concentrates, and wettable powders, strengthening the region’s technological advantage. Continuous investment in sustainable agriculture, digital crop monitoring, and precision farming supports long-term market expansion

- High farmer awareness, strong distribution networks, and government-backed agricultural innovation programs further reinforce regional market leadership

U.S. Polyoxin Market Insight

The U.S. is the largest contributor in North America, supported by growing adoption of integrated pest management (IPM) practices, organic farming, and high-value crop cultivation. Rising demand for Polyoxin B and D in rice, vegetables, and greenhouse crops drives market growth. Increasing investments by leading agrochemical companies in formulation optimization, field trials, and farmer training further accelerate Polyoxin adoption across the country.

Canada Polyoxin Market Insight

Canada contributes significantly to regional growth, driven by strong demand in cereal, potato, and horticultural crops. Farmers increasingly rely on Polyoxin for effective fungal disease control and yield improvement. Government-supported programs promoting sustainable crop protection, skilled agronomists, and growing awareness of biofungicides strengthen market penetration across the country.

Asia-Pacific Polyoxin Market

Asia-Pacific is projected to register the fastest CAGR of 8.19% from 2026 to 2033, driven by rising adoption of modern crop protection techniques, government incentives for sustainable agriculture, and rapid growth in rice, vegetable, and fruit cultivation across China, India, Japan, South Korea, and Southeast Asia. Increasing investments in Polyoxin B and D production, advanced formulations, and precision farming solutions continue to accelerate adoption across smallholder and commercial farms.

China Polyoxin Market Insight

China is the largest contributor to Asia-Pacific due to massive agricultural production, strong government support for crop protection programs, and growing demand for high-yield, disease-resistant crops. Expansion of Polyoxin manufacturing facilities, competitive pricing, and extensive farmer awareness campaigns further boost domestic and export market adoption.

Japan Polyoxin Market Insight

Japan shows steady growth supported by advanced agricultural infrastructure, greenhouse farming, and focus on premium crop quality. Rising use of Polyoxin formulations for fruits, vegetables, and ornamental plants drives market adoption. The demand for low-residue, environmentally friendly fungicides strengthens long-term market expansion.

India Polyoxin Market Insight

India is emerging as a key growth hub, driven by increasing rice, vegetable, and horticultural production, rising awareness of biofungicides, and government initiatives promoting sustainable crop protection. Polyoxin adoption is accelerating in commercial farms and greenhouse operations due to enhanced yield protection and resistance management.

South Korea Polyoxin Market Insight

South Korea contributes significantly due to high-value vegetable, rice, and fruit cultivation. Rapid adoption of modern agricultural techniques, greenhouses, and precision farming supports increasing Polyoxin demand. Strong R&D, advanced manufacturing capabilities, and growing awareness of bio-based crop protection solutions reinforce sustained market growth.

Which are the Top Companies in Polyoxin Market?

The polyoxin industry is primarily led by well-established companies, including:

- Jiangsu Fengyuan Bioengineering Co., Ltd. (China)

- Beijing Green Crop Science and Technology Co., Ltd. (China)

- Kaken Pharmaceutical Co., Ltd. (Japan)

- Nufarm Canada (Canada)

- Arysta LifeScience Corporation (U.S.)

- Certis (U.S.)

- OHP, Inc. (U.S.)

- Cleary Chemical Corp. (U.S.)

- DAYANG CHEM (HANGZHOU) CO., LTD. (China)

- Shanxi Lvhai Agrochemicals (China)

- MITSUI & CO., LTD. (Japan)

- UPL (India)

- BASF SE (Germany)

- Bayer AG (Germany)

- Syngenta Crop Protection AG (Switzerland)

- FMC Corporation (U.S.)

- DuPont (U.S.)

- Dow (U.S.)

- LANXESS (Germany)

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.