Global Venous Blood Collection Devices Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

6.84 Billion

USD

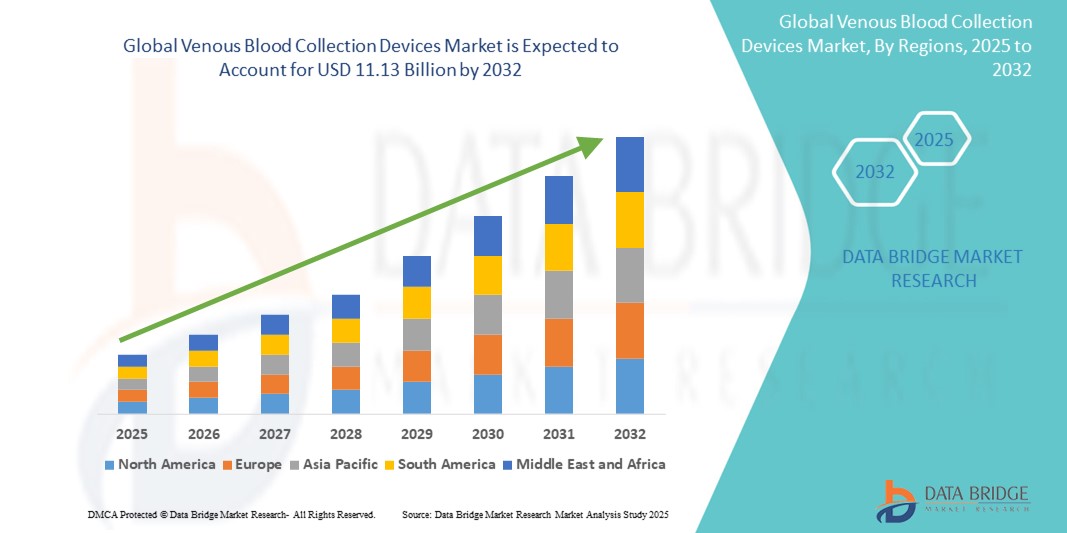

11.13 Billion

2024

2032

USD

6.84 Billion

USD

11.13 Billion

2024

2032

| 2025 –2032 | |

| USD 6.84 Billion | |

| USD 11.13 Billion | |

| % | |

|

글로벌 정맥 채혈 장치 시장 세분화(유형별: 채혈관, 바늘, 진공 채혈 시스템, 미세유체 시스템 등), 소재별(플라스틱, 유리, 스테인리스 스틸 등), 응용 분야별(정맥 혈액 가스 샘플링, 수술 중 혈액 회수), 최종 사용자별(병원 및 진료소, 현장 진료, 헌혈 센터, 진단 센터 등) - 2032년까지 산업 동향 및 전망

정맥혈 채취 장치 시장 규모

- 글로벌 정맥혈액 수집 장치 시장 규모는 2024년에 68억 4천만 달러 로 평가되었으며 예측 기간 동안 6.27%의 CAGR 로 2032년까지 111억 3천만 달러 에 도달할 것으로 예상됩니다 .

- 이러한 성장은 진단 검사에 대한 수요 증가, 만성 질환 수 증가, 의료 기술의 발전, 조기 질병 감지의 중요성에 대한 인식 증가와 같은 요인에 의해 촉진됩니다.

정맥혈 채취 장치 시장 분석

- 정맥 채혈 장치는 임상 및 진단 환경에서 다양한 검사와 치료를 위한 혈액 샘플을 채취하는 데 사용되는 필수 도구입니다. 바늘, 주사기, 채혈관을 포함한 이러한 장치는 정기적인 혈액 검사, 수혈, 만성 질환 진단 등의 시술에 필수적입니다.

- 당뇨병, 심혈관 질환, 암 등 만성 질환의 유병률 증가와 예방 건강 관리 및 조기 질병 탐지에 대한 강조가 증가함에 따라 정맥혈 수집 장치에 대한 수요가 크게 증가하고 있습니다.

- 북미 지역은 선진 의료 인프라, 높은 의료비 지출, 그리고 증가하는 진단 검사 수요 덕분에 정맥 채혈 장치 시장을 약 75.5%의 가장 큰 시장 점유율로 장악할 것으로 예상됩니다. 또한, 이 지역은 수많은 의료 시설과 잘 구축된 의료보험 상환 시스템을 갖추고 있어 유리한 위치를 점하고 있습니다.

- 아시아 태평양 지역은 의료 접근성 향상, 혈액 관련 진단 검사에 대한 인식 증가, 중국 및 인도와 같은 국가의 의료 인프라 확장으로 인해 예측 기간 동안 정맥 혈액 수집 장치 시장에서 가장 빠르게 성장하는 지역으로 예상됩니다.

- 플라스틱 부문은 약 88.5%의 시장 점유율로 시장을 장악할 것으로 예상됩니다. 플라스틱은 비용 효율성이 뛰어나 유리 소재에 비해 생산 및 구매 비용이 저렴하기 때문입니다. 플라스틱 채혈 장치는 파손 위험이 적기 때문에 더 안전하고 내구성이 뛰어나 취급 및 운송 중 부상 위험을 줄여줍니다.

보고서 범위 및 정맥혈 채취 장치 시장 세분화

|

속성 |

정맥혈 채취 장치 주요 시장 통찰력 |

|

다루는 세그먼트 |

|

|

포함 국가 |

북아메리카

유럽

아시아 태평양

중동 및 아프리카

남아메리카

|

|

주요 시장 참여자 |

|

|

시장 기회 |

|

|

부가가치 데이터 정보 세트 |

Data Bridge Market Research에서 큐레이팅한 시장 보고서에는 시장 가치, 성장률, 세분화, 지리적 적용 범위, 주요 업체 등 시장 시나리오에 대한 통찰력 외에도 심층적인 전문가 분석, 환자 역학, 파이프라인 분석, 가격 분석, 규제 프레임워크가 포함되어 있습니다. |

정맥 채혈 장치 시장 동향

“정맥혈 채취 장치의 기술적 발전”

- 정맥혈 채취 장치 시장의 두드러진 추세 중 하나는 혈액 채취 시술 중 효율성, 안전성 및 환자 편의성을 향상시키기 위한 첨단 기술의 통합입니다.

- 이러한 혁신에는 바늘 찔림 부상 위험을 최소화하는 수납식 바늘과 같은 안전 공학 장치 개발, 환자의 불편함을 줄이고 전반적인 수집 프로세스를 개선하는 혈류 제어를 개선하는 장치가 포함됩니다.

- For instance, advancements in needle design and the introduction of smart blood collection tubes with digital tracking systems enable real-time data collection and improve sample integrity, streamlining the diagnostic process

- These advancements are transforming blood collection practices, improving patient safety and comfort, and driving the demand for next-generation blood collection devices with enhanced features

Venous Blood Collection Devices Market Dynamics

Driver

“Growing Demand Due to Increasing Chronic Diseases”

- The rising prevalence of chronic diseases such as diabetes, cardiovascular conditions, and obesity is significantly contributing to the increased demand for venous blood collection devices

- As the global population ages and lifestyle diseases continue to rise, there is an increasing need for regular diagnostic testing, which in turn drives the demand for efficient and reliable blood collection methods

- As more individuals undergo routine blood tests for monitoring and managing these chronic conditions, the need for advanced blood collection devices grows, ensuring better diagnosis, treatment, and monitoring

For instance,

- In 2022, the World Health Organization (WHO) reported that the global prevalence of diabetes is expected to rise significantly, with an estimated 700 million people living with the disease by 2045. This increase is directly contributing to the growing need for blood collection devices to monitor diabetes and other chronic diseases

- As a result of the rising incidence of chronic diseases, there is a significant increase in the demand for venous blood collection devices, driving market growth and the adoption of advanced technologies for improved healthcare outcomes

Opportunity

“Expanding Role of Digital Health and AI in Blood Collection”

- The integration of digital health technologies and artificial intelligence (AI) into venous blood collection systems presents a significant market opportunity by enhancing the accuracy, traceability, and efficiency of blood sample management

- AI-driven tools can assist in optimizing vein detection, reducing errors in collection, and improving the overall patient experience, particularly in difficult venous access cases or pediatric and elderly patients

- Smart blood collection devices with connectivity features can automatically log and track samples, integrate with electronic health records (EHRs), and support remote patient monitoring and data analytics

For instance,

- In 2023, multiple healthcare innovators began piloting AI-powered vein visualization and digital labeling systems to reduce human error and streamline pre-analytical processes, contributing to faster diagnostics and improved clinical outcomes

- The integration of AI and digital tools in venous blood collection can lead to increased operational efficiency, reduced sample misidentification, and enhanced diagnostic accuracy—creating new growth avenues in both hospital and home-care settings

Restraint/Challenge

“Risk of Contamination and Needlestick Injuries Hindering Market Growth”

- The risk of bloodborne pathogen transmission and needlestick injuries remains a significant challenge in the venous blood collection devices market, particularly impacting healthcare worker safety and regulatory compliance

- Despite advancements in safety-engineered devices, improper handling, lack of training, and insufficient use of protective technologies in certain regions increase the likelihood of accidents and infections

- These safety concerns can lead to higher liability for healthcare institutions, increased operational costs, and hesitance in adopting new blood collection systems without proven safety records

For instance,

- According to a 2023 report by the World Health Organization (WHO), over 2 million healthcare workers globally experience needlestick injuries annually, with a considerable percentage related to blood collection procedures. This has heightened the demand for strict safety protocols and advanced protective equipment

- Consequently, safety risks and infection concerns act as barriers to wider adoption, particularly in under-resourced healthcare systems, hindering the growth of the global venous blood collection devices market

Venous Blood Collection Devices Market Scope

The market is segmented on the basis of type, material, application, and end users

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Material |

|

|

By Application |

|

|

By End users |

|

In 2025, the plastic is projected to dominate the market with a largest share in material segment

The plastic segment is expected to dominate the venous blood collection devices market with the largest share of approximately 88.5%, due to the cost-effectiveness of plastic, which makes it more affordable to produce and purchase compared to glass alternatives. Plastic blood collection devices are also safer and more durable, as they are less prone to breakage, reducing the risk of injury during handling and transportation

The hospitals and clinics is expected to account for the largest share during the forecast period in end users segment

In 2025, the hospitals and clinics segment is expected to dominate the market with the largest market share of approximately 34.2%, due to the high volume of diagnostic tests and increased blood transfusion needs associated with surgeries and chronic conditions. Hospitals and clinics serve as primary centers for patient care, encompassing a wide range of services from routine check-ups to complex surgical procedures, thereby driving the demand for venous blood collection devices

Venous Blood Collection Devices Market Regional Analysis

“North America Holds the Largest Share in the Venous Blood Collection Devices Market”

- North America dominates the venous blood collection devices market with largest market share of approximately 75.5%, driven by a well-established healthcare infrastructure, high healthcare spending, and early adoption of advanced diagnostic technologies

- The U.S. holds a significant share of 28.7%, due to the increasing number of diagnostic tests, strong presence of key players such as Becton, Dickinson and Company, and favorable reimbursement policies that support the widespread use of modern blood collection devices

- The growing burden of chronic diseases such as diabetes, cardiovascular conditions, and cancer continues to drive demand for frequent blood tests, further boosting the market in the region

- The presence of regulatory bodies like the FDA that enforce safety and quality standards also encourages innovation and deployment of advanced, safety-engineered blood collection devices

“Asia-Pacific is Projected to Register the Highest CAGR in the Venous Blood Collection Devices Market”

- The Asia-Pacific region is expected to witness the highest growth rate in the venous blood collection devices market, fueled by the rapid expansion of healthcare infrastructure and increasing investments in healthcare modernization

- Countries such as China, India, and Japan are emerging as key contributors, supported by large patient populations, rising prevalence of lifestyle diseases, and growing demand for improved diagnostic services

- Japan leads in technology adoption, while China and India are seeing rising public and private sector investments to expand diagnostic capabilities, particularly in rural and underserved areas

- Government initiatives promoting early disease detection, coupled with improving access to healthcare services, are accelerating the adoption of venous blood collection devices across the region

Venous Blood Collection Devices Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- BD (US)

- Haematonics (US)

- Terumo BCT (US)

- Fresenius Kabi AG (Germany)

- Grifols, S.A. (Spain)

- Nipro Medical Corporation (Japan)

- Greiner Holding (Austria)

- Quest Diagnostics (US)

- SARSTEDT AG & Co. (Germany)

- Macopharma (France)

- Smiths Medical (US)

- Cardinal Health (US)

- Retractable Technologies (US)

- Liuyang Sanli Medical Technology Development (China)

- F.L. Medical S.R.L (Italy)

- AB Medical (South Korea)

- APTCA SPA (Italy)

- Jiangsu Micsafe Medical Technology CO., LTD. (China)

- Disera Tibbi Malzeme Lojistik Sanayi Ve Ticaret A.Þ(터키)

- Ajosha Bio Teknik Pvt. Ltd.(인도)

- Preq Systems(인도)

- CML Biotech(인도)

- Lmb Technologie GmbH(독일)

- Mitra Industries Private Limited(인도)

- 네오메딕 리미티드(영국)

글로벌 정맥 채혈 장치 시장의 최신 동향

- 2020년 8월, Greiner Bio-One과 Haematologic Technologies는 체외진단(IVD) 및 임상 진단 기기 개발자의 요구에 맞춘 혈액 채혈 튜브에 대한 포괄적인 엔드 투 엔드 개발 및 맞춤형 제조 서비스를 제공하기 위한 전략적 협력을 발표했습니다. 이 협력은 혈액 채혈 튜브 제조의 혁신과 맞춤형 제작을 강화하여 정밀 진단에 대한 증가하는 수요에 대응합니다. 시장이 더욱 전문화되고 고성능의 진단 솔루션으로 전환됨에 따라, 이러한 전략적 제휴는 제품 품질 향상 및 출시 기간 단축에 중요한 역할을 하며, 궁극적으로 정맥 채혈 기기의 글로벌 확장 및 기술 발전을 지원합니다.

- 2020년 7월, Magnolia Medical은 Steripath Gen2 초기 검체 전환 장치를 출시했습니다. 이 장치는 특히 혈관계가 손상된 환자의 혈액 검체 채취 정확도를 향상시키도록 설계된 주사기가 내장되어 있습니다. Steripath Gen2의 출시는 더욱 정확하고 환자 중심적인 혈액 채취 솔루션으로의 시장 변화를 반영합니다. 특히 취약 계층을 중심으로 진단 신뢰성에 대한 수요가 증가함에 따라, 이와 같이 기술적으로 진보된 장치는 임상 결과 개선에 기여하고 전 세계 시장 성장을 견인하는 혁신의 중요성을 다시 한번 강조합니다.

- 2022년 3월, 비바슈어 메디컬(Vivasure Medical)은 차세대 PerQseal+ 기기를 평가하는 미국 조기 타당성 연구에 첫 환자가 등록되었다고 발표했습니다. PerQseal+는 경피적 경피적 대동맥판막 치환술(TAVR)에 사용하도록 설계되었으며, 혈관 폐쇄 기술의 중요한 발전을 보여줍니다. 이러한 발전은 정맥 접근 및 채혈의 광범위한 생태계를 보완하여 안전성, 사용 편의성, 그리고 환자 치료 결과 향상을 강조하며, 이러한 요소들은 정맥 채혈 기기 시장의 성장을 촉진하고 있습니다.

- 2022년 2월, 로슈의 파운데이션 메디슨(Foundation Medicine)은 혈장 내 순환 종양 DNA(ctDNA)를 검출하도록 설계된 검사법에 대한 규제 승인을 받았습니다. FDA로부터 혁신적 치료제로 지정된 이 검사법은 완치적 치료 후 암 환자의 분자적 잔류 질환(MRD)을 검출하기 위한 것입니다. ctDNA 검사법 승인은 개인 맞춤 의료에서 비침습적 혈액 기반 진단 기술의 중요성이 커지고 있음을 보여줍니다. 이러한 추세는 정확한 검체 채취 및 처리가 신뢰할 수 있는 진단 결과를 보장하는 데 필수적이기 때문에 첨단 혈액 채취 장비에 대한 수요 증가와 일치합니다.

- 2024년 2월, Tasso, Inc.는 사전 검사 프로그램의 효율성을 향상시키도록 설계된 포괄적인 엔드 투 엔드 서비스 솔루션인 Tasso Care for Prescreening을 출시했습니다. Tasso Care for Prescreening의 출시는 임상 시험에서 혁신적인 채혈 솔루션에 대한 수요가 증가하고 있음을 보여줍니다. Tasso는 원격 채혈 기능을 통합함으로써 더욱 접근성이 높고 효율적인 의료 서비스로의 전환에 기여하고 있으며, 이는 고급 정맥 채혈 장비의 필요성을 증가시키고 있습니다.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.