Middle East And Africa Healthcare 3d Printing Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

1.53 Billion

USD

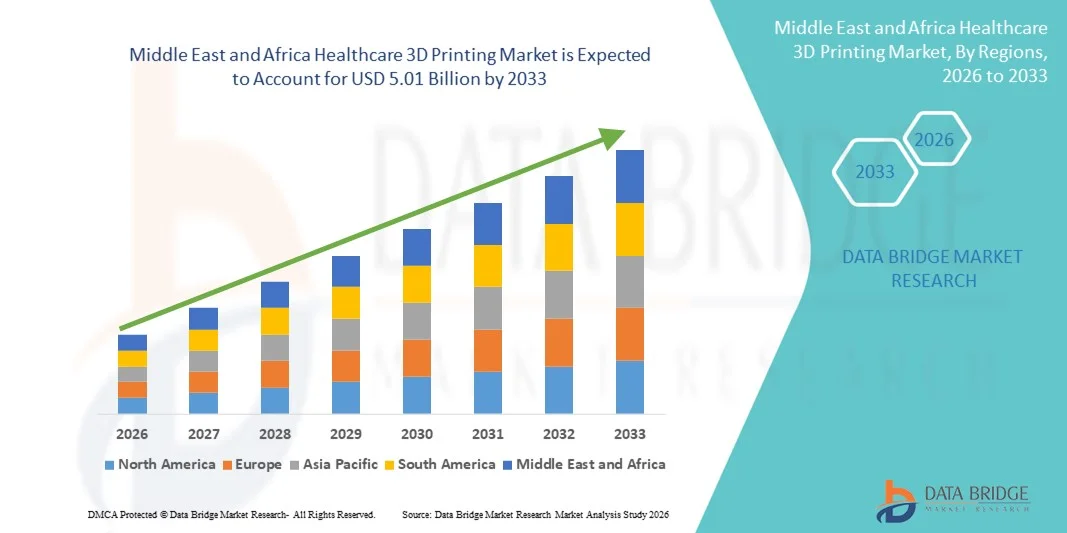

5.01 Billion

2025

2033

USD

1.53 Billion

USD

5.01 Billion

2025

2033

| 2026 –2033 | |

| USD 1.53 Billion | |

| USD 5.01 Billion | |

| % | |

|

중동 및 아프리카 의료용 3D 프린팅 시장 세분화: 방식별(독립형 및 통합형), 구성 요소별(재료, 하드웨어, 소프트웨어 및 서비스), 기술별(바이오프린팅, 액적 증착/압출 기반 기술, 광중합, 레이저 빔 용융, 전자빔 용융(EBM), 3D 프린팅/접착 결합/바인더 제팅 및 기타), 응용 분야별(의료, 외과, 제약 및 기타), 의료 전문 분야별(정형외과, 치과, 심혈관, 두개악안면(CMF), 신경외과, 종양학 및 기타), 최종 사용자별(의료 및 외과 센터, 연구 센터 및 학술 기관, 제약 및 생명공학 회사 및 기타) - 산업 동향 및 2033년까지의 전망

중동 및 아프리카 의료용 3D 프린팅 시장 규모

- 중동 및 아프리카 의료용 3D 프린팅 시장 규모는 2025년 15억 3천만 달러 였으며, 예측 기간 동안 연평균 성장률(CAGR) 16.00% 로 성장하여 2033년에는 50억 1천만 달러 에 이를 것으로 예상됩니다 .

- 시장 성장은 의료 분야에서 첨단 적층 제조 기술의 도입이 증가함에 따라 환자 맞춤형 임플란트, 보철물, 수술 가이드 및 해부학적 모델 생산이 가능해지면서 크게 촉진되고 있습니다. 3D 프린팅 소재, 소프트웨어 및 프린팅 기술의 빠른 발전은 임상 및 연구 분야 전반에 걸쳐 정밀도, 맞춤화 및 효율성을 향상시키고 있습니다.

- 더욱이, 의료 서비스 제공자들이 비용 효율적이고 시간 효율적이며 개인 맞춤형 의료 솔루션에 대한 수요가 증가함에 따라 의료용 3D 프린팅은 현대 의료 현장에서 혁신적인 접근 방식으로 자리매김하고 있습니다. 이러한 여러 요인이 복합적으로 작용하여 의료용 3D 프린팅 솔루션의 도입을 가속화하고 있으며, 결과적으로 전체 시장 성장을 크게 촉진하고 있습니다.

중동 및 아프리카 의료용 3D 프린팅 시장 분석

- 환자 맞춤형 임플란트, 보철물, 수술 가이드 및 해부학적 모델 제작을 가능하게 하는 의료용 3D 프린팅은 치료 정확도 향상, 시술 시간 단축 및 환자 결과 개선에 기여하여 현대 의료 서비스 제공에 필수적인 요소로 자리 잡고 있습니다. 병원, 연구 기관 및 의료 기기 제조 분야 전반에 걸쳐 3D 프린팅의 활용이 증가함에 따라 임상 워크플로우가 크게 변화하고 있습니다.

- 개인 맞춤형 의료에 대한 수요 증가, 첨단 적층 제조 기술의 도입 확대, 그리고 생체 적합성 소재의 지속적인 혁신은 의료용 3D 프린팅 시장 성장을 이끄는 주요 요인입니다. 이러한 발전은 비용 효율성 향상, 생산 주기 단축, 그리고 임상 정확도 개선을 지원하여 시장 확대를 가속화하고 있습니다.

- Saudi Arabia dominated the healthcare 3D printing market with the largest revenue share of 34.7% in 2025. This dominance is supported by significant government investments under Vision 2030, rapid modernization of healthcare infrastructure, growing adoption of advanced medical technologies, and increasing use of 3D printing for implants, prosthetics, and surgical planning in major hospitals and research centers

- The U.A.E. is expected to be the fastest-growing region in the healthcare 3D printing market during the forecast period, with a projected CAGR of 22.4%. Growth is driven by strong healthcare spending, government-backed innovation initiatives, expanding medical tourism, rising adoption of precision medicine, and increasing collaboration between hospitals, research institutes, and technology providers

- The standalone segment dominated the market with the largest revenue share of 55.4% in 2024, driven by its high flexibility, ease of deployment, and compatibility with various hospital workflows. Standalone systems are preferred by medical facilities due to their lower cost of ownership, minimal setup requirements, and ability to be used across multiple departments

Report Scope and Healthcare 3D Printing Market Segmentation

|

Attributes |

Healthcare 3D Printing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Middle East and Africa Healthcare 3D Printing Market Trends

Accelerated Adoption of Patient-Specific and Point-of-Care 3D Printing Solutions

- A significant and accelerating trend in the Middle East and Africa Healthcare 3D Printing market is the growing adoption of patient-specific, customized medical devices and point-of-care 3D printing within hospitals and academic medical centers. Healthcare providers across the region are increasingly leveraging 3D printing to produce anatomical models, surgical guides, prosthetics, and implants tailored to individual patient anatomy, improving surgical precision and clinical outcomes

- For instance, in June 2023, King Faisal Specialist Hospital & Research Centre (Saudi Arabia) expanded its in-house medical 3D printing laboratory to support personalized surgical planning and implant prototyping, enabling surgeons to practice complex procedures using patient-specific anatomical models prior to surgery. Similar initiatives have been observed in the UAE, where academic hospitals have incorporated 3D-printed anatomical models for orthopedic and cardiovascular interventions

- The increasing availability of advanced biocompatible materials and medical-grade polymers is further strengthening this trend, allowing healthcare facilities to move beyond prototyping toward functional applications such as customized implants, dental restorations, and hearing aids. These innovations are particularly valuable in regions facing high trauma incidence and congenital disorders, where customized solutions can significantly improve patient outcomes

- In addition, collaborations between hospitals, universities, and technology providers are supporting the localization of medical 3D printing capabilities. Training programs and innovation hubs are being established to build regional expertise, reducing reliance on imported medical devices and shortening lead times for critical surgical components

- This shift toward decentralized, hospital-based 3D printing is transforming healthcare delivery in the region by enabling faster treatment decisions, reducing surgical risks, and supporting personalized medicine approaches. As a result, healthcare providers across the Middle East and Africa are increasingly viewing 3D printing as a strategic clinical tool rather than a purely experimental technology

- The growing emphasis on customized care, surgical accuracy, and cost-effective production of medical components is expected to further accelerate the adoption of healthcare 3D printing solutions across both public and private healthcare institutions in the region

Middle East and Africa Healthcare 3D Printing Market Dynamics

Driver

Rising Burden of Chronic Diseases, Trauma Cases, and Surgical Demand

- The rising prevalence of chronic diseases, road traffic accidents, and complex surgical cases across the Middle East and Africa is a major driver for the adoption of healthcare 3D printing solutions. Increasing incidences of cardiovascular diseases, orthopedic conditions, and dental disorders are driving demand for customized implants, prosthetics, and surgical planning tools that can improve treatment accuracy and patient recover

- For instance, in September 2022, Dubai Health Authority reported the expanded use of 3D-printed anatomical models in complex orthopedic and spinal surgeries within government hospitals, supporting surgeons in preoperative planning and reducing intraoperative risks. Such initiatives highlight how healthcare systems are integrating 3D printing to manage rising surgical volumes more efficiently

- Healthcare providers are increasingly recognizing the value of 3D printing in reducing operating room time, minimizing surgical errors, and improving procedural outcomes. Customized surgical guides and patient-specific implants help clinicians achieve better alignment and fit, which is particularly important in trauma and reconstructive surgeries

- Furthermore, growing investments in healthcare infrastructure and modernization initiatives across Gulf Cooperation Council (GCC) countries are encouraging the adoption of advanced manufacturing technologies, including medical 3D printing. Government-backed healthcare transformation programs are supporting innovation and digitalization in clinical workflows

- The ability of 3D printing to reduce dependency on imported medical devices, lower long-term costs, and support rapid prototyping is further strengthening its appeal among hospitals and specialty clinics. As surgical demand continues to rise, healthcare 3D printing is becoming a key enabler of efficient and high-quality patient care

- These factors collectively position healthcare 3D printing as a critical solution to address growing clinical demands, thereby driving sustained market growth across the Middle East and Africa

Restraint/Challenge

High Capital Investment, Regulatory Complexity, and Limited Skilled Workforce

- High initial capital investment associated with medical-grade 3D printers, certified materials, and post-processing equipment remains a significant challenge to widespread adoption, particularly in resource-constrained healthcare systems across parts of Africa. Smaller hospitals and clinics often face budget limitations that restrict investment in advanced 3D printing infrastructure

- For instance, in November 2021, several public hospitals in Sub-Saharan Africa highlighted budgetary constraints and regulatory uncertainties as barriers to adopting in-house medical 3D printing, despite recognizing its clinical benefits, reflecting the uneven pace of adoption across the region

- In addition to cost barriers, the lack of harmonized regulatory frameworks for 3D-printed medical devices poses challenges for commercialization and clinical use. Regulatory approval processes for patient-specific implants and surgical guides can be complex and time-consuming, discouraging rapid adoption by healthcare providers

- The limited availability of skilled professionals trained in medical design software, additive manufacturing processes, and clinical validation further restricts market growth. Many healthcare facilities rely on external service providers due to the shortage of in-house expertise, which can increase operational costs and turnaround times

- Concerns related to quality assurance, material standardization, and long-term performance of 3D-printed medical products also contribute to cautious adoption among clinicians and hospital administrators. Ensuring consistent product quality and compliance with international medical standards remains a critical requirement

- Addressing these challenges through targeted investments, workforce training programs, clearer regulatory guidelines, and cost-effective technology solutions will be essential for unlocking the full potential of healthcare 3D printing across the Middle East and Africa

Middle East and Africa Healthcare 3D Printing Market Scope

The market is segmented on the basis of modality, components, technology, application, medical specialty, and end user.

- By Modality

On the basis of modality, the Healthcare 3D Printing market is segmented into standalone and integrated. The standalone segment dominated the market with the largest revenue share of 55.4% in 2024, driven by its high flexibility, ease of deployment, and compatibility with various hospital workflows. Standalone systems are preferred by medical facilities due to their lower cost of ownership, minimal setup requirements, and ability to be used across multiple departments. The segment also benefits from rising adoption in small and medium-sized hospitals and dental clinics that prefer dedicated 3D printers for specific applications such as prosthetics and dental models. In addition, standalone systems often provide better customization options for specific medical specialties, making them ideal for orthopedic and dental applications. Strong demand for rapid prototyping and patient-specific solutions further supports the dominance of standalone systems in the market.

The integrated segment is expected to register the fastest CAGR of 18.2% from 2025 to 2032, owing to growing demand for end-to-end printing solutions that combine hardware, software, and workflow integration. Integrated systems provide enhanced automation, reduced manual intervention, and improved accuracy, making them suitable for high-volume hospital environments. The increasing adoption of integrated systems is also driven by the need for standardized workflows, regulatory compliance, and improved traceability in medical device manufacturing. As healthcare providers move toward digitalization, integrated solutions are gaining traction for streamlined operations and reduced time-to-treatment. Rising investments in hospital infrastructure and digital transformation initiatives are expected to accelerate growth in this segment during the forecast period.

- By Components

On the basis of components, the Healthcare 3D Printing market is segmented into material, hardware, software, and services. The material segment dominated the market with the largest revenue share of 39.7% in 2024, driven by increasing demand for biocompatible materials and customized medical-grade polymers. Materials such as medical-grade resins, metals, and ceramics are widely used for implants, prosthetics, surgical guides, and dental applications. Rising R&D activities in material science and increasing approval of new biomaterials by regulatory authorities further strengthen this segment. Additionally, the need for patient-specific implants and personalized medicine is driving material consumption across healthcare settings. Growing demand for high-performance materials that ensure safety, durability, and precision is also supporting market dominance.

The services segment is expected to witness the fastest CAGR of 19.3% from 2025 to 2032, driven by increasing outsourcing of 3D printing services by hospitals and clinics. Service providers offer end-to-end solutions including design, printing, post-processing, and quality validation. Many healthcare providers prefer outsourcing due to high capital investment and technical expertise required for in-house printing. Rising demand for rapid prototyping, patient-specific implants, and surgical planning models is fueling growth in service-based offerings. In addition, the growing adoption of centralized printing hubs and shared services models is expected to boost the services segment during the forecast period.

- By Technology

On the basis of technology, the Healthcare 3D Printing market is segmented into bioprinting, droplet deposition/extrusion-based technologies, photopolymerization, laser beam melting, electron beam melting (EBM), 3DP/adhesion bonding/binder jetting, and others. The droplet deposition/extrusion-based technology segment dominated the market with the largest revenue share of 31.8% in 2024, driven by its wide use in creating surgical models, dental prosthetics, and orthopedic implants. This technology offers high accuracy, cost-efficiency, and compatibility with a wide range of biomaterials, which supports its adoption across hospitals and dental clinics. The segment also benefits from continuous innovation and development of multi-material printing capabilities.

The bioprinting segment is expected to register the fastest CAGR of 21.1% from 2025 to 2032, driven by growing R&D in tissue engineering, regenerative medicine, and organ-on-chip applications. Bioprinting enables the fabrication of complex tissues and organs using living cells and biomaterials, making it a key technology for future medical breakthroughs. Increasing funding for bioprinting research, rising collaborations between academic institutions and biotech companies, and growing demand for personalized medicine are accelerating market growth.

- By Application

On the basis of application, the Healthcare 3D Printing market is segmented into medical, surgical, pharmaceutical, and others. The medical segment dominated the market with the largest revenue share of 42.5% in 2024, supported by high demand for patient-specific implants, anatomical models, and prosthetics. 3D printing is widely used in orthopedics and dentistry to produce customized implants and surgical guides. Rising prevalence of chronic diseases and increasing need for personalized healthcare solutions further drive adoption. The segment also benefits from regulatory approvals for medical-grade printing materials and devices. Continuous innovation in biocompatible materials and improved printing accuracy further strengthen its leadership. Medical applications also receive strong investments from hospitals and healthcare systems to improve patient outcomes. The growing demand for rapid prototyping in medical research is also boosting this segment. As healthcare providers increasingly focus on precision medicine, the medical segment is expected to retain dominance in the near future.

The surgical segment is expected to witness the fastest CAGR of 20.4% from 2025 to 2032, driven by rising use of 3D printed surgical guides, pre-operative planning models, and custom implants. Surgeons increasingly rely on 3D printed models to improve surgical accuracy, reduce operation time, and enhance patient outcomes. Growing adoption in complex surgeries such as spinal, craniofacial, and orthopedic procedures is supporting this growth. The segment benefits from advancements in multi-material printing and better imaging-to-print workflows. Increasing use of patient-specific implants and surgical planning tools further accelerates adoption. Collaboration between hospitals and 3D printing solution providers is strengthening market expansion. Rising investments in healthcare infrastructure in emerging markets also contribute to faster growth. The growing trend of minimally invasive surgeries is also boosting the need for 3D printed surgical models.

- By Medical Specialty

On the basis of medical specialty, the Healthcare 3D Printing market is segmented into orthopedics, dental, cardiovascular, craniomaxillofacial (CMF), neurosurgery, oncology, and others. The dental segment dominated the market with the largest revenue share of 37.9% in 2024, driven by widespread use of 3D printing in dental implants, aligners, crowns, and bridges. Dental clinics and labs are adopting 3D printing due to its precision, cost-efficiency, and fast turnaround time. The availability of advanced dental materials and increasing demand for customized dental solutions further support market dominance. The segment also benefits from increasing patient awareness and rising demand for cosmetic dentistry. Rapidly evolving dental CAD/CAM systems and scanners are further boosting adoption. Dental 3D printing reduces production time and improves treatment accuracy, making it a preferred choice for dentists.

The orthopedics segment is expected to register the fastest CAGR of 18.9% from 2025 to 2032, driven by increasing use of 3D printed implants, prosthetics, and surgical models. Orthopedic applications require highly customized and patient-specific devices, which is driving adoption of 3D printing technology. Growing incidence of bone disorders and trauma cases, along with rising demand for personalized implants, is expected to boost segment growth. Innovations in metal 3D printing and biocompatible polymers are also supporting this trend. Rising geriatric population and increased orthopedic surgeries are further increasing demand. Hospitals are investing heavily in 3D printed surgical models for better treatment outcomes. The growing adoption of 3D printed joint implants is also strengthening the segment’s growth.

- By End User

On the basis of end user, the Healthcare 3D Printing market is segmented into medical & surgical centers, research centers and academic institutions, pharmaceutical & biotechnology companies, and others. The medical & surgical centers segment dominated the market with the largest revenue share of 45.2% in 2024, driven by high adoption of 3D printing for surgical planning, patient-specific implants, and prosthetics. Hospitals and surgical centers increasingly use 3D printing to reduce operation time, improve patient outcomes, and enhance preoperative planning. The presence of advanced healthcare infrastructure and increasing investments in digital health are further supporting this segment. Increasing number of hospital-based 3D printing labs and partnerships with technology providers is strengthening market dominance.

The research centers and academic institutions segment is expected to witness the fastest CAGR of 19.8% from 2025 to 2032, driven by growing research in bioprinting, regenerative medicine, and medical device innovation. Academic institutions and research labs are investing in 3D printing technologies for experimental studies, prototyping, and tissue engineering. Increasing collaborations between universities and biotech companies are accelerating innovation and driving market growth. The segment also benefits from government grants and funding for advanced research. Rising interest in personalized medicine and tissue engineering is further boosting adoption. Research centers are focusing on developing new biomaterials and printing methods to improve clinical applications.

Middle East and Africa Healthcare 3D Printing Market Regional Analysis

- The Europe healthcare 3D printing market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing demand for personalized medical devices and rising adoption of advanced healthcare technologies. The region benefits from strong healthcare infrastructure, high R&D spending, and supportive regulatory frameworks for medical device innovation. European hospitals and clinics are increasingly adopting 3D printing for implants, surgical planning models, and prosthetics

- Rising geriatric population and chronic disease prevalence are further supporting demand for customized healthcare solutions. Continuous advancements in biocompatible materials and printing technologies also contribute to market growth

- Key European countries such as Germany, the U.K., France, and Italy are investing heavily in 3D printing research and clinical applications. Collaboration between healthcare providers and technology companies is accelerating product development and commercialization. The presence of leading medical device manufacturers in Europe further strengthens market expansion

U.K. Healthcare 3D Printing Market Insight

The U.K. healthcare 3D printing market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing adoption of 3D printing in clinical and surgical applications. The U.K. has strong medical research capabilities and a well-established healthcare system, supporting innovation in 3D printing for implants, prosthetics, and surgical models. Rising demand for patient-specific solutions and growing investments in healthcare digitalization further accelerate growth. The U.K. also benefits from strong collaboration between academic institutions, hospitals, and technology providers. Increasing focus on reducing surgical time and improving patient outcomes is encouraging the use of 3D printed models for preoperative planning.

Germany Healthcare 3D Printing Market Insight

The Germany healthcare 3D printing market is expected to expand at a considerable CAGR during the forecast period, driven by rising demand for advanced medical devices and increasing adoption of 3D printing in hospitals and research centers. Germany’s well-developed healthcare infrastructure, strong manufacturing base, and high investment in medical technology support market growth. The country is witnessing rising use of 3D printing in orthopedic implants, dental applications, and surgical models. The emphasis on innovation and quality standards also encourages adoption of medical-grade 3D printing materials. Increasing healthcare spending and the growing need for customized healthcare solutions further drive demand. Germany’s strong focus on sustainability and precision manufacturing also supports the use of 3D printing technology.

Middle East and Africa Healthcare 3D Printing Market Share

The Healthcare 3D Printing industry is primarily led by well-established companies, including:

• GE HealthCare (U.S.)

• Renishaw (U.K.)

• EnvisionTEC (Germany)

• EOS GmbH (Germany)

• Stryker (U.S.)

• Zimmer Biomet (U.S.)

• Johnson & Johnson (U.S.)

• HP Inc. (U.S.)

• Carbon, Inc. (U.S.)

• Formlabs (U.S.)

• CELLINK (Sweden)

• Organovo (U.S.)

• Bio3D Technologies (Japan)

• Aspect Biosystems (Canada)

• Nano Dimension (Israel)

• Prodways Group (France)

• Ultimaker (Netherlands)

Latest Developments in Middle East and Africa Healthcare 3D Printing Market

- In March 2021, Stratasys Ltd. partnered with Canwell Medical to introduce the J5 DentaJet 3D PolyJet printer for dental laboratories, enabling high-precision, multi-material 3D printing of dental parts such as crowns, bridges, and surgical guides. This development helped accelerate the use of 3D printing technology for customized dental and minor surgical applications, supporting broader adoption of 3D printing in clinical workflows

- 2024년 6월, 스트라타시스는 RAPID + TCT 컨퍼런스에서 수술 계획 및 임상 교육을 위한 매우 정확한 해부학적 모델을 제작하도록 설계된 J5 디지털 해부학 3D 프린터를 출시한다고 발표했습니다. 이 프린터는 수술 전 시각화를 개선하고 임상 의사의 의사 결정을 향상시킵니다.

- 2025년 6월, 3D Systems와 프랑스 의료기기 파트너사인 TISSIUM은 말초신경 복구를 위한 최초의 3D 프린팅 기반 생분해성 솔루션인 COAPTIUM CONNECT with TISSIUM Light에 대해 FDA로부터 신규 승인(De Novo authorization)을 획득했습니다. 이러한 규제 승인은 첨단 재생의학 분야 및 맞춤형 임플란트에 있어 적층 제조 기술의 잠재력을 보여주는 중요한 이정표입니다.

- 2025년 4월, 3D Systems는 바젤 대학 병원과 협력하여 자사의 EXT 220 MED 시스템을 활용해 의료기기 규정(MDR)을 준수하는 최초의 3D 프린팅 PEEK 안면 임플란트를 현장에서 생산했습니다. 이를 통해 엄격한 유럽 의료기기 규정을 충족하는 맞춤형 악안면 임플란트를 현장에서 제작할 수 있게 되었습니다.

- 2025년 2월, 스트라타시스 다이렉트의 애리조나주 투손 공장은 의료기기 제조 분야의 핵심 품질 관리 표준인 ISO 13485 인증을 획득했습니다. 이 표준은 3D 프린팅 부품 및 임플란트의 광범위한 임상 적용과 확장 가능한 생산을 지원합니다.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.