Middle East And Africa Heart Valve Repair And Replacement Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

1.50 Billion

USD

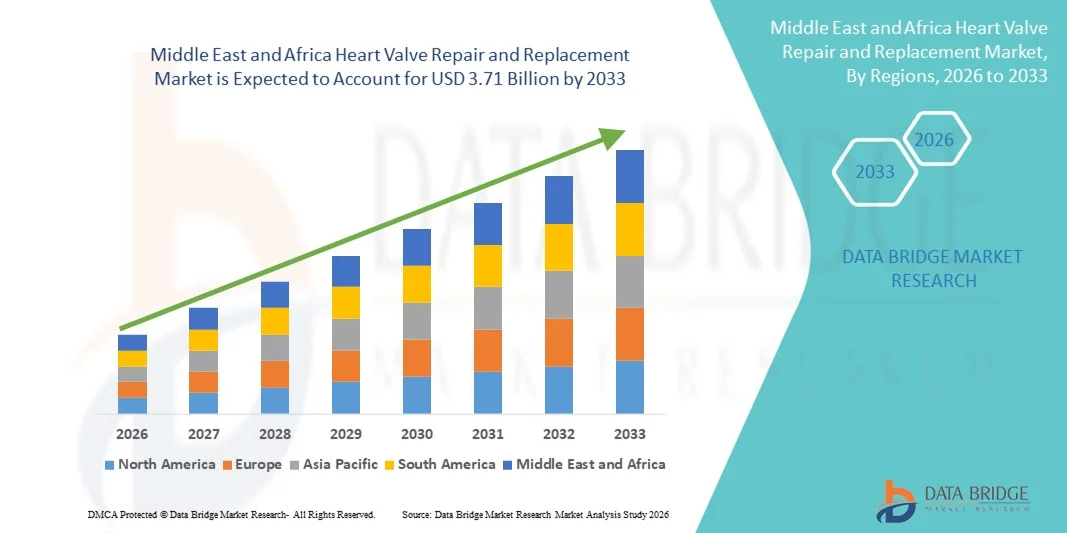

3.71 Billion

2025

2033

USD

1.50 Billion

USD

3.71 Billion

2025

2033

| 2026 –2033 | |

| USD 1.50 Billion | |

| USD 3.71 Billion | |

| % | |

|

Middle East and Africa Heart Valve Repair and Replacement Market Segmentation, By Product (Surgical Heart Valves Replacement, Surgical Heart Valves Repair, TAVI / TAVR Valves, Grafts, Patches, Medication and Others), Procedure (Surgical Procedure and Non-Surgical Procedure), Indication (Valvular Stenosis, Valvular Insufficiency, Mitral Valve Prolapse and Others), End User (Hospital, Specialty Centers, Cardiac Catheterization Lab, Ambulatory Surgical Centers and Others), Distribution Channel (Direct Tender, Retail Sales and Others)- Industry Trends and Forecast to 2033

Middle East and Africa Heart Valve Repair and Replacement Market Size

- The Middle East and Africa heart valve repair and replacement market size was valued at USD 1.50 billion in 2025 and is expected to reach USD 3.71 billion by 2033, at a CAGR of 12.0% during the forecast period

- This regional growth is primarily driven by increasing prevalence of cardiovascular diseases, demographic shifts toward an aging population, and wider adoption of innovative and minimally invasive techniques such as transcatheter procedures, which improve outcomes and reduce recovery times

- Furthermore, rising healthcare expenditures and investments in medical infrastructure across key MEA countries along with greater patient awareness of heart valve disorders are strengthening the uptake of repair and replacement solutions in both public and private care settings

Middle East and Africa Heart Valve Repair and Replacement Market Analysis

- Heart valve repair and replacement procedures, encompassing surgical and transcatheter approaches, are increasingly essential in managing valvular heart diseases across the Middle East and Africa due to rising cardiovascular disease prevalence, aging populations, and growing awareness of minimally invasive treatment options

- The escalating demand for heart valve repair and replacement is primarily driven by increasing incidence of heart valve disorders, improvements in procedural outcomes, and wider availability of advanced technologies such as transcatheter aortic valve replacement (TAVR) and minimally invasive mitral valve repair

- Saudi Arabia dominated the MEA market with the largest revenue share of 38.3% in 2025, supported by well-established healthcare infrastructure, higher healthcare expenditure, and early adoption of advanced cardiac procedures, particularly in urban hospitals and specialized cardiac centers

- South Africa is expected to be the fastest-growing country in the MEA heart valve repair and replacement market during the forecast period due to expanding healthcare access, increasing investment in medical facilities, and rising patient awareness of cardiac conditions

- Surgical heart valves replacement segment dominated the market with a market share of 55.7% in 2025, driven by its established clinical outcomes, long-term durability, and broad availability in major hospitals across the region

Report Scope and Middle East and Africa Heart Valve Repair and Replacement Market Segmentation

|

Attributes |

Middle East and Africa Heart Valve Repair and Replacement Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Heart Valve Repair and Replacement Market Trends

Minimally Invasive and Transcatheter Procedures Gaining Traction

- A significant and accelerating trend in the MEA heart valve repair and replacement market is the increasing adoption of minimally invasive and transcatheter procedures such as TAVR and MitraClip, which reduce recovery time and procedural risk

- For instance, hospitals in Saudi Arabia and UAE are implementing transcatheter aortic valve replacement programs in major cardiac centers, improving patient outcomes and attracting referrals from neighboring countries

- These procedures are supported by advanced imaging and catheterization technologies that enable precise valve placement and reduced surgical trauma, enhancing both patient safety and satisfaction

- The growing expertise among interventional cardiologists and cardiac surgeons in MEA countries facilitates wider adoption of these procedures across urban hospitals and specialized cardiac centers

- This trend toward less invasive solutions is fundamentally reshaping patient expectations for heart valve therapy, prompting hospitals and manufacturers to expand offerings in transcatheter and hybrid repair options

- The demand for minimally invasive and transcatheter procedures is rising across both private and public healthcare sectors, as patients increasingly prioritize shorter hospital stays and faster recovery

- Increasing collaborations between local hospitals and global medical device companies are enabling faster introduction of innovative valve technologies in the region

- Telemedicine and remote monitoring integration are emerging trends, allowing post-procedure follow-ups and patient monitoring that enhance clinical outcomes and convenience

Middle East and Africa Heart Valve Repair and Replacement Market Dynamics

Driver

Rising Cardiovascular Disease Burden and Aging Population

- The increasing prevalence of cardiovascular diseases and an aging population in MEA countries is a significant driver for the heightened demand for heart valve repair and replacement procedures

- For instance, Saudi Arabia reported a substantial rise in valvular heart disease cases in 2025, prompting hospitals to expand advanced cardiac care programs and procedural capacities

- As awareness of heart valve disorders grows, patients are seeking interventions that improve survival and quality of life, creating demand for both surgical and transcatheter solutions

- Furthermore, increasing healthcare expenditure and investment in specialized cardiac centers support the expansion of procedural capabilities in the region

- Enhanced access to advanced diagnostic and imaging technologies facilitates early detection and timely intervention, further propelling market growth

- The growing patient preference for minimally invasive options and improved procedural outcomes is encouraging adoption across both public and private healthcare sectors

- Government initiatives promoting cardiovascular health awareness and screening programs are driving early diagnosis and increasing patient pool for interventions

- Rising medical tourism in UAE and Saudi Arabia for advanced cardiac procedures is attracting regional and international patients, boosting market demand

Restraint/Challenge

High Procedural Costs and Limited Specialist Availability

- The relatively high cost of surgical and transcatheter valve procedures, coupled with limited availability of trained interventional cardiologists and cardiac surgeons in certain MEA countries, poses a significant market challenge

- For instance, in some Sub-Saharan African nations, access to advanced valve replacement programs is restricted due to shortage of specialized staff and infrastructure, limiting market penetration

- Procedural costs, including device prices and hospitalization, can make therapies unaffordable for price-sensitive patients, particularly in regions with limited insurance coverage

- In addition, maintaining procedural quality and managing post-operative complications require highly skilled teams and well-equipped facilities, which are not uniformly available across all MEA countries

- Addressing these challenges through government initiatives, medical training programs, and partnerships with device manufacturers is essential for broader adoption

- Without these measures, disparities in access to advanced heart valve therapies may persist, constraining the growth potential of the MEA market

- Limited awareness and delayed diagnosis of valvular heart diseases in rural areas further restrict market growth potential

- Supply chain challenges for imported valves and devices can cause procedural delays and increase costs, especially in less-developed MEA countries

Middle East and Africa Heart Valve Repair and Replacement Market Scope

The market is segmented on the basis of product, procedure, indication, end user, and distribution channel.

- By Product

On the basis of product, the MEA heart valve repair and replacement market is segmented into surgical heart valves replacement, surgical heart valves repair, TAVI/TAVR Valves, grafts, patches, medication, and others. The Surgical Heart Valves Replacement segment dominated the market with the largest revenue share of 55.7% in 2025, driven by its long-established clinical outcomes, wide availability across major hospitals, and familiarity among cardiac surgeons. Hospitals in Saudi Arabia and UAE particularly prefer surgical valve replacements for high-risk patients due to the procedure’s proven durability and long-term effectiveness. The segment benefits from strong insurance coverage in GCC countries, contributing to its continued adoption. Surgeons and cardiologists also favor surgical valves for complex multi-valve cases where minimally invasive approaches may not be feasible. The segment’s dominance is further reinforced by ongoing training programs in tertiary cardiac centers and the availability of multiple valve types from global manufacturers.

The TAVI/TAVR Valves segment is anticipated to witness the fastest growth rate of 15% CAGR from 2026 to 2033, fueled by increasing preference for minimally invasive procedures in urban hospitals across MEA. For instance, Saudi Arabia and UAE have rapidly expanded TAVI programs due to shorter hospital stays, reduced surgical trauma, and improved recovery times. The segment is particularly popular among elderly patients or those with high surgical risk who are unsuitable for traditional surgery. Advancements in valve design and catheter delivery systems are enhancing procedural safety and broadening the eligible patient population. Growing awareness of these less invasive options and increasing collaborations between local hospitals and international device manufacturers further accelerate adoption.

- By Procedure

On the basis of procedure, the market is segmented into surgical procedure and non-surgical procedure. The Surgical Procedure segment dominated the market with the largest revenue share of 60% in 2025, as traditional open-heart surgeries remain the standard for complex valvular repairs and multi-valve cases in MEA. Hospitals in Saudi Arabia and UAE continue to prefer surgical procedures for patients requiring high precision and long-term durability. Surgical procedures are supported by extensive infrastructure in tertiary care hospitals and experienced cardiac surgery teams. The segment also benefits from established insurance reimbursement policies that cover major cardiac surgeries. Continuous training and clinical workshops in cardiac centers reinforce adoption of surgical procedures.

The Non-Surgical Procedure segment, comprising TAVI/TAVR and catheter-based valve repair, is expected to witness the fastest growth rate of 15% CAGR from 2026 to 2033 due to rising demand for minimally invasive treatment. For instance, South Africa and UAE are expanding cardiac catheterization programs to perform non-surgical valve procedures with reduced recovery times. Patient preference for shorter hospital stays and lower procedural risk drives adoption. Technological advancements in catheter delivery and imaging guidance enhance procedural success rates. Increasing awareness campaigns and early diagnosis programs also contribute to the rapid uptake of non-surgical procedures.

- By Indication

On the basis of indication, the market is segmented into valvular stenosis, valvular insufficiency, mitral valve prolapse, and others. The Valvular Stenosis segment dominated the market with the largest revenue share of 45% in 2025, driven by the high prevalence of aortic stenosis and mitral stenosis in aging populations. Hospitals in GCC countries prioritize treatment of severe stenosis due to the high risk of heart failure and mortality. Advanced diagnostic imaging, including echocardiography and CT, enables early detection and timely intervention. Availability of both surgical and transcatheter options strengthens the segment’s market position. The segment also benefits from government-sponsored cardiovascular health initiatives that screen high-risk populations.

The Mitral Valve Prolapse segment is expected to witness the fastest growth rate of 14% CAGR from 2026 to 2033 due to increasing awareness and early diagnosis programs. For instance, UAE and South Africa are introducing screening programs that detect MVP at earlier stages, allowing intervention before complications arise. Minimally invasive repairs and catheter-based options increase patient willingness for treatment. Growing investment in cardiac centers and interventional cardiology programs further accelerates adoption.

- By End User

On the basis of end user, the market is segmented into hospital, specialty centers, cardiac catheterization lab, ambulatory surgical centers, and others. The Hospital segment dominated the market with the largest revenue share of 65% in 2025, owing to comprehensive infrastructure, availability of specialized cardiac teams, and capacity to handle complex surgical procedures. Hospitals in Saudi Arabia and UAE act as referral centers for patients across the region. High patient trust and insurance coverage make hospitals the primary choice for valve repair and replacement. Hospitals also offer advanced ICU care and post-operative rehabilitation services, reinforcing their dominance. Continuous government support and private investment in hospital infrastructure further strengthen market share.

The Cardiac Catheterization Lab segment is expected to witness the fastest growth rate of 16% CAGR from 2026 to 2033, driven by increasing adoption of minimally invasive procedures such as TAVI/TAVR and MitraClip. For instance, UAE and South Africa are expanding catheterization labs to meet rising patient demand for non-surgical interventions. Labs provide high procedural efficiency and shorter recovery times. Investment in advanced imaging and catheter technologies facilitates accurate interventions. Growing expertise among interventional cardiologists and partnerships with global device manufacturers support rapid expansion.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, retail sales, and others. The Direct Tender segment dominated the market with the largest revenue share of 70% in 2025, as hospitals and specialty centers procure devices directly from manufacturers or authorized distributors through government or private tenders. This ensures cost-effectiveness, timely delivery, and authenticity of heart valves and related devices. GCC countries rely heavily on direct tenders for advanced medical devices due to centralized procurement systems. Long-term contracts and bulk purchasing agreements also reinforce dominance.

The Retail Sales segment is expected to witness the fastest growth rate of 13% CAGR from 2026 to 2033, driven by increasing availability of valve-related medications, patches, and small devices through pharmacies and medical suppliers. For instance, UAE and South Africa are witnessing growing retail access to post-operative medications and supportive devices for home-based care. Retail channels improve convenience for patients and caregivers and enhance adherence to treatment regimens. Expansion of private clinics and specialty pharmacies further boosts retail distribution.

Middle East and Africa Heart Valve Repair and Replacement Market Regional Analysis

- Saudi Arabia dominated the MEA market with the largest revenue share of 38.3% in 2025, supported by well-established healthcare infrastructure, higher healthcare expenditure, and early adoption of advanced cardiac procedures, particularly in urban hospitals and specialized cardiac centers

- Patients and healthcare providers in the region increasingly prefer minimally invasive and transcatheter procedures due to reduced recovery times, improved safety, and better clinical outcomes compared to traditional open-heart surgeries

- The widespread adoption is further supported by government initiatives promoting cardiovascular health awareness, high patient inflow in tertiary care hospitals, and the presence of experienced cardiac surgeons, establishing Saudi Arabia as a key hub for both public and private cardiac interventions

The Saudi Arabia Heart Valve Repair and Replacement Market Insight

The Saudi Arabia heart valve repair and replacement market captured the largest revenue share of 38.3% in 2025, driven by advanced healthcare infrastructure, rising healthcare expenditure, and early adoption of minimally invasive and surgical valve procedures. Patients increasingly prioritize safer, faster recovery options, while tertiary hospitals offer specialized cardiac programs that attract both local and regional patients. Government initiatives promoting cardiovascular health and widespread insurance coverage further support market expansion. The presence of experienced cardiac surgeons and advanced catheterization labs ensures high procedural success rates and strengthens patient confidence in both public and private hospitals.

UAE Heart Valve Repair and Replacement Market Insight

The UAE heart valve repair and replacement market is anticipated to grow at a substantial CAGR during the forecast period, fueled by growing investments in healthcare infrastructure, advanced cardiac centers, and medical tourism. Increasing patient awareness of heart valve disorders, coupled with demand for minimally invasive and transcatheter procedures, is driving adoption. The UAE’s focus on specialized care, along with partnerships with international medical device companies, facilitates access to state-of-the-art heart valve technologies. Both local and regional patients are opting for advanced valve procedures, positioning the UAE as a key hub for high-quality cardiac interventions.

South Africa Heart Valve Repair and Replacement Market Insight

The South Africa heart valve repair and replacement market is expected to expand at a considerable CAGR during the forecast period, driven by rising prevalence of valvular heart diseases and expansion of cardiac care infrastructure. Growing expertise among interventional cardiologists and cardiac surgeons, combined with government and private investment in modern catheterization labs, is enabling increased procedural volumes. Awareness campaigns for early detection of valvular disorders and improved access to diagnostic imaging further contribute to market growth. Patients increasingly seek minimally invasive solutions to reduce hospital stays and enhance recovery.

Egypt Heart Valve Repair and Replacement Market Insight

The Egypt heart valve repair and replacement market is poised for steady growth due to increasing incidence of cardiovascular diseases and expansion of specialized cardiac centers in urban areas. Hospitals are adopting advanced surgical and transcatheter valve procedures to meet growing patient demand. Public health initiatives and screening programs for heart valve disorders improve early diagnosis rates, enhancing procedural uptake. Rising healthcare expenditure and partnerships with international device manufacturers are facilitating access to cutting-edge valve replacement and repair technologies.

Middle East and Africa Heart Valve Repair and Replacement Market Share

The Middle East and Africa Heart Valve Repair and Replacement industry is primarily led by well-established companies, including:

- Edwards Lifesciences Corporation (U.S.)

- Abbott (U.S.)

- Boston Scientific Corporation (U.S.)

- Biotronik (Germany)

- Meril Life Sciences (India)

- Artivion, Inc (U.S.)

- Corcym Group (U.K.)

- Peijia Medical Limited (China)

- Micro Interventional Devices, Inc. (U.S.)

- TTK Healthcare Limited (India)

- Colibri Heart Valve (U.S.)

- Neovasc Inc (Canada)

- LivaNova PLC (U.K.)

- Cardiac Science Corporation (U.S.)

- St. Jude Medical (U.S.)

- C.R. Bard (U.S.)

- Medtronic (Ireland)

- Sorin Group (Italy)

- AbioMed, Inc. (U.S.)

- Endovalve Inc. (U.S.)

What are the Recent Developments in Middle East and Africa Heart Valve Repair and Replacement Market?

- In October 2025, Sheikh Khalifa Medical City (SKMC) in Abu Dhabi performed a groundbreaking paediatric tricuspid valve replacement surgery on a 14‑year‑old using minimally invasive techniques, marking a major advancement in complex valve care for younger patients in the region

- In March 2025, Egypt’s National Heart Institute announced a pioneering valve implantation program (pulmonary valve via catheter) that enables patients to be discharged within a day, significantly shortening recovery and demonstrating progress in less invasive valve replacement in Egypt

- In October 2024, Cleveland Clinic Abu Dhabi celebrated its 500th TAVI (Transcatheter Aortic Valve Implantation) procedure, underscoring the rapid adoption of minimally invasive valve replacement in the UAE and reflecting expanding procedural capacity and expertise

- In August 2024, the King Faisal Specialist Hospital & Research Centre (KFSHRC) in Jeddah successfully performed a breakthrough catheter‑based heart surgery on a patient with multiple severe valve abnormalities, showcasing advanced interventional valve care in Saudi Arabia

- In April 2021, the Saudi Ministry of Health, with Jameel Health, introduced the AVNeo™ heart valve reconstruction procedure an innovative surgical technique using a patient’s tissue for valve reconstruction, making Saudi Arabia the first Gulf country to adopt this advanced method

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.