North America Gastric Cancer Diagnostics Market, By Product Type (Instruments, Reagents & Consumables, Services), Diagnostics Type (Confirmatory Test, Gastric Cancer Screening Tests/Physical Exam), Age Group (Adult, Pediatric, and Geriatrics), Disease Type (Intestinal Or Diffuse Adenocarcinoma, Carcinoid Tumor, Gastrointestinal Stromal Tumor (GIST), Gastric Lymphoma and Others), Stage (Stage 0, Stage I, Stage II, Stage III), Gender (Male and Female), Sample Type (Blood, Tissue, Urine, and Stool), End Users (Diagnostic Laboratories, Hospitals, Cancer Research Institutes, Oncology Specialty Clinics, and Others), Distribution Channel (Direct Tenders and Retail Sales) - Industry Trends and Forecast to 2030.

North America Gastric Cancer Diagnostics Market Analysis and Insights

The increase in the North America geriatric population is driving the growth of the gastric cancer diagnostics industry. The prevalence of gastrointestinal tumors and lymphomas has also fueled the demand for gastric cancer diagnostics. The key market constraint is the need to lower the high prices associated with cancer diagnostic testing so that even developing countries may benefit from it.

Large numbers of market players are offering gastric cancer diagnostics products with innovations that pave the way for the growth of the North America gastric cancer diagnostics market.

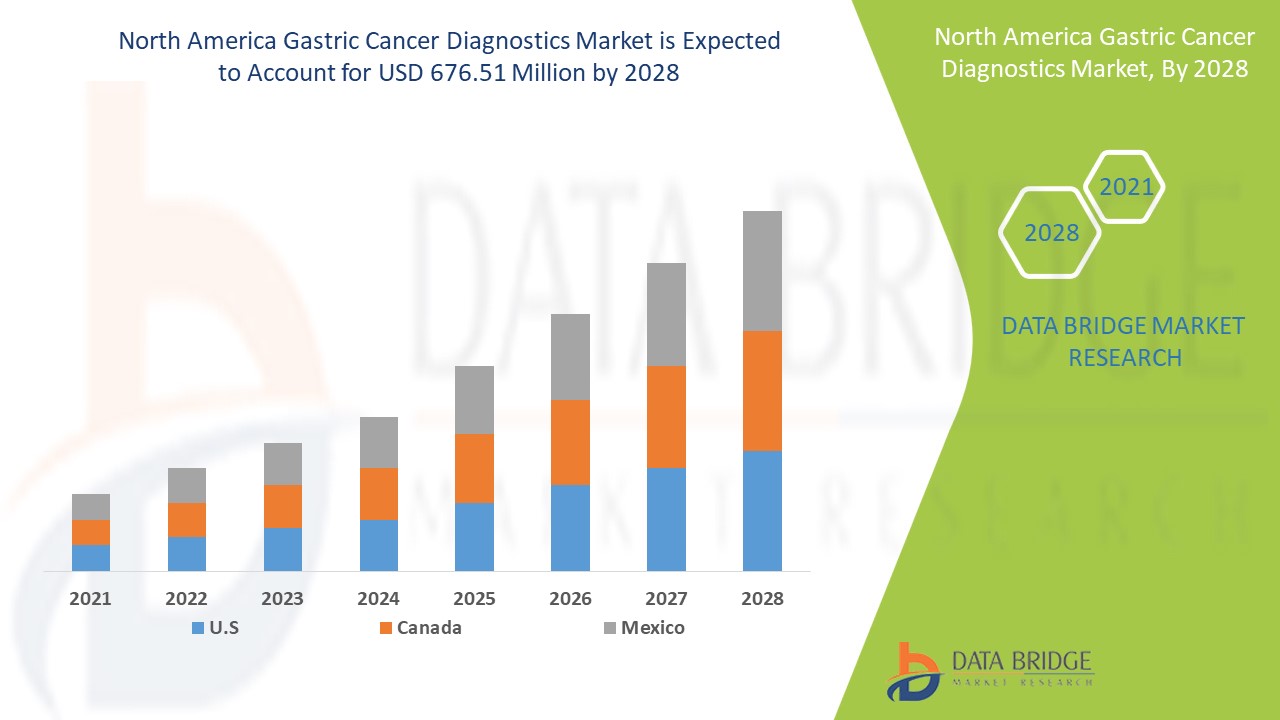

Data Bridge Market Research analyzes that the North America Gastric cancer diagnostics market is expected to reach the value of USD 843.49 million by 2030, at a CAGR of 8.5% during the forecast period. Reagents and consumables account for the largest product type segment in the market due to rising demand for kits and reagents, and increasing health expenditures have accelerated the demand for smart medical devices.

|

Report Metric |

Details |

|

Forecast Period |

2023 to 2030 |

|

Base Year |

2022 |

|

Historic Years |

2021 (Customisable to 2015-2020) |

|

Quantitative Units |

Revenue in USD Million, Volumes in Units, Pricing in USD |

|

Segments Covered |

By Product Type (Instruments, Reagents & Consumables, Services), Diagnostics Type (Confirmatory Test, Gastric Cancer Screening Tests/Physical Exam), Age Group (Adult, Pediatric, and Geriatrics), Disease Type (Intestinal Or Diffuse Adenocarcinoma, Carcinoid Tumor, Gastrointestinal Stromal Tumor (GIST), Gastric Lymphoma and Others), Stage (Stage 0, Stage I, Stage II, Stage III), Gender (Male and Female), Sample Type (Blood, Tissue, Urine, and Stool), End Users (Diagnostic Laboratories, Hospitals, Cancer Research Institutes, Oncology Specialty Clinics, and Others), Distribution Channel (Direct Tenders and Retail Sales) |

|

Countries Covered |

U.S., Canada, and Mexico |

|

Market Players Covered |

BIOMÉRIEUX, Myriad Genetics, Inc., ACON Laboratories, Inc., Teco Diagnostics, Vela Diagnostics, Abbott, AdvaCare Pharma, MiRXES Pte Ltd., Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd, General Electric, Agilent Technologies, Inc., Biohit Oyj, BIOCEPT, INC., FOUNDATION MEDICINE, INC., DiaSorin S.p.A, Paragon Genomics, Inc., QIAGEN, and among others |

Market Definition

Stomach cancer is a type of cancer that starts in the stomach and spreads throughout the body. The stomach is a muscular pouch that lies immediately below the ribs in the upper part of the abdomen. The stomach takes in and holds the food we eat before breaking it down and digesting it. Stomach cancer, commonly referred to as gastric cancer, can occur in any section of the stomach. Stomach cancers develop in the major section of the stomach in most parts of the world (stomach body). Various diagnostic tests used for the diagnosis of cancer include prescreening tests, biopsy, biomarkers, imaging tests, PET/CT scans, and ultrasound among others.

Cancer is caused by uncontrolled, abnormal cell proliferation that has the ability to spread and invade other sections of the body. Changes in the gene cause a single cell or a few cells to expand and replicate, which is when cancer begins. This could lead to the growth of a tumor, which is an abnormal mass of tissue. The creation of cancer cells in the stomach lining is known as gastric cancer or stomach cancer. Diet and stomach disorders are both risk factors for gastric cancer.

North America Gastric Cancer Diagnostics Market Dynamics

This section deals with understanding the market drivers, advantages, opportunities, restraints, and challenges. All of this is discussed in detail below:

Drivers

- Increase in incidence of gastrointestinal tumors, lymphoma, and adenocarcinoma

According to a report published in Clinical Medicine, gastric cancer is the fifth most common cancer and the fourth leading cause of cancer death worldwide in 2020. In 2020, an estimated 1.1 million cases (720,000 males and 370,000 females) of gastric cancer were diagnosed worldwide. Gastric cancer is responsible for about 1 in every 12 oncological fatalities. Every year, about a million new instances of stomach cancer are diagnosed around the world.

It is projected that the incidence of gastric cancer will rise, due to to aging and increasing population, lifestyle, and socioeconomic change. Striking variations in race, sociocultural norms, behaviors, and dietary trends are reflected in the burden and distribution of cancer in different regions across the globe.

Thus, the rising incidence of cancers across the globe is expected to accelerate the demand for gastric cancer diagnostics. Thus the increased incidence rates of gastrointestinal tumors, lymphoma, and adenocarcinoma are expected to drive the growth of the North America gastric cancer diagnostics market.

- Rise in alcohol consumption and surge in smoking

Epidemiological, clinical, and laboratory evidence point to a behavioral relationship between cigarette smoking and alcohol consumption. The combined use of cigarettes and alcohol poses health concerns in addition to those posed by smoking alone and so represents a severe public health issue that warrants further investigation.

A chemical chain reaction occurs every time a smoker inhales a lit cigarette, producing dozens of hazardous chemicals. Cigarette smoke contains substances that are inhaled through the lips, through the tongue and mouth, down the throat, and into the lungs, producing inflammation and exposing those bodily parts to cancer-causing chemicals.

Thus, the rise in alcohol consumption and surge in smoking is expected to drive the North America gastric cancer market growth.

Opportunity

-

Rise in adoption of automated systems

Cancer is a system and network illness. This indicates that in a cancer cell, certain network-related genes stop working properly. Complex interactions in such gene networks should be addressed in cancer treatment. Artificial intelligence (AI) algorithms, in particular, have been rapidly evolving, which is reflected in oncology's progress.

Machine learning and neural networks are becoming increasingly significant in precision oncology and system medicine. The combination of imaging data with clinical and molecular data opens up a world of possibilities. Radiogenomics, for instance, is a new field focused on multidimensional data processing. It can also benefit from AI advancements.

Thus, the increased adoption of automated systems acts as an opportunity for the growth of this market.

Restraint/Challenge

- Lack of sufficient financial support from health insurance policies

To achieve their objectives, health systems require financial resources. Human resources, hospital care, and medications are the most expensive aspects of most healthcare systems. In most tropical countries, health care is funded through a combination of government, private (mainly out-of-pocket) spending, and international help.

Healthcare finance remains a key concern for low- and lower-middle-income countries. Many upper-middle-income countries in Latin America, Africa, and Asia have been able to establish health finance arrangements that cover large segments of their populations. These measures enable access to health care while also protecting individuals from catastrophic debt incurred as a result of that access. Finance, on the other hand, is a major obstacle to health care delivery in low-income countries (the bulk of which are in Sub-Saharan Africa).

Thus, the lack of sufficient financial support from health insurance policies acts as a restraint to market's growth.

Recent Developments

- In October 2022, General Electric Company collaborated with several research institutes such as the University of Cambridge Hospitals, Sophia Genetics, and earlier with Optellum to use imaging data in collaboration with Artificial intelligence. This will help to reduce the diagnosing time of several cancers and help to provide personalized care to patients. This has helped the company to widen its horizons in cancer diagnostics

- In March 2020, Thermo Fisher Scientific Inc. announced that it would be acquiring QIAGEN, a Netherland-based molecular diagnostics and healthcare company. This acquisition by the company will increase its product portfolio in the market, leading to increased revenue in future

North America Gastric Cancer Diagnostics Market Scope

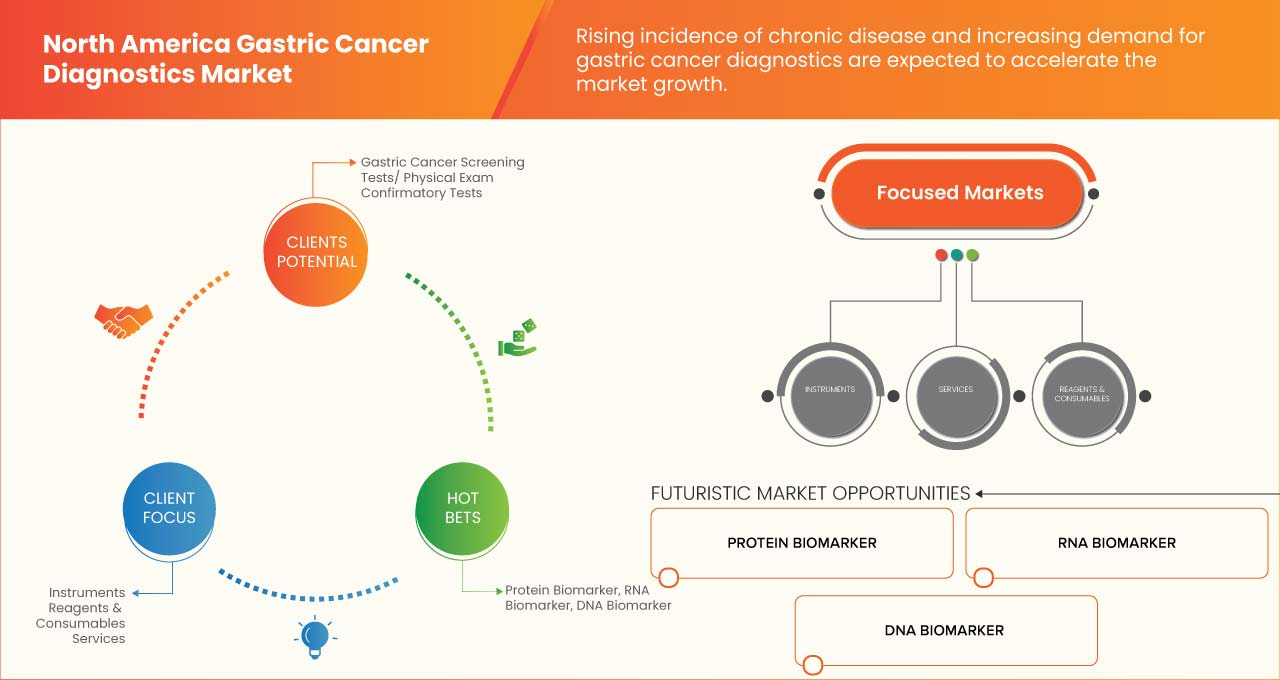

The North America gastric cancer diagnostics market is segmented into nine notable segments based on product type, diagnostic type, age group, type, stage, gender, sample, end user, and distribution channel. The growth among segments helps you analyze niche pockets of growth and strategies to approach the market and determine your core application areas and the difference in your target markets.

PRODUCT TYPE

- Instruments

- Reagents & Consumables

- Services

On the basis of product type, the market is segmented into instruments, reagents & consumables, and services.

DIAGNOSTIC TYPE

- Confirmatory Test

- Gastric Cancer Screening Tests/Physical Exam

On the basis of diagnostics type, the market is segmented into gastric cancer screening tests/physical exam and confirmatory tests.

AGE GROUP

- Adult

- Pediatric

- Geriatrics

On the basis of age group, the market is segmented into adult, pediatric, and geriatrics.

TYPE

- Intestinal Or Diffuse Adenocarcinoma

- Carcinoid Tumor

- Gastrointestinal Stromal Tumor (GIST)

- Gastric Lymphoma

- Others

On the basis of type, the market is segmented into intestinal or diffuse adenocarcinoma, carcinoid tumor, gastrointestinal stromal tumor (GIST), gastric lymphoma, and others.

STAGE

- Stage 0

- Stage I

- Stage II

- Stage III

On the basis of stage, the market is segmented into stage 0, stage I, stage II, and stage III.

GENDER

- Male

- Female

On the basis of gender, the market is segmented into male and female.

SAMPLE TYPE

- Blood

- Tissue

- Urine

- Stool

On the basis of sample type, the market is segmented into blood, tissue, urine, and stool.

END USER

- Diagnostic Laboratories

- Hospitals

- Cancer Research Institutes

- Oncology Specialty Clinics

- Others

On the basis of end users, the market is segmented into diagnostic laboratories, hospitals, cancer research institutes, oncology specialty clinics, and others.

DISTRIBUTION CHANNEL

- Direct Tenders

- Retail Sales

On the basis of distribution channel, the market is segmented into direct tender and retail sales.

North America Gastric Cancer Diagnostics Market Regional Analysis/Insights

The North America gastric cancer diagnostics market is segmented into nine notable segments based on product type, diagnostic type, age group, disease type, stage, gender, sample, end user, and distribution channel.

The countries covered in this market report U.S., Canada, and Mexico.

U.S. is expected to dominate due to rise in technological advancement in the healthcare industry.

The country section of the report also provides individual market impacting factors and changes in regulation in the market domestically that impact the current and future trends of the market. Data points such as new sales, replacement sales, country demographics, regulatory acts, and import-export tariffs are some of the major pointers used to forecast the market scenario for individual countries. Also, the presence and availability of North American brands and their challenges faced due to large or scarce competition from local and domestic brands, and impact of sales channels are considered while providing forecast analysis of the country data.

Competitive Landscape and Gastric Cancer Diagnostics Market Share Analysis

The North America gastric cancer diagnostics market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in R&D, new market initiatives, production sites and facilities, company strengths and weaknesses, product launch, product approvals, product width and breadth, application dominance, and product type lifeline curve. The above data points provided are only related to the company's focus on the North America gastric cancer diagnostics market.

Some of the major players operating in the North America gastric cancer diagnostics market are BIOMÉRIEUX, Myriad Genetics, Inc., ACON Laboratories, Inc., Teco Diagnostics, Vela Diagnostics, Abbott, AdvaCare Pharma, MiRXES Pte Ltd., Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd, General Electric, Agilent Technologies, Inc., Biohit Oyj, BIOCEPT, INC., FOUNDATION MEDICINE, INC., DiaSorin S.p.A, Paragon Genomics, Inc., QIAGEN, and among others.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

목차

1 서론

1.1 연구 목적

1.2 시장 정의

1.3 북미 위암 진단 시장 개요

1.4 제한 사항

1.5 대상 시장

2 시장 세분화

2.1 대상 시장

2.2 지리적 범위

연구에 2.3년이 고려됨

2.4 통화 및 가격

2.5 DBMR TRIPOD 데이터 검증 모델

2.6 다변량 모델링

2.7 제품 유형 수명선 곡선

2.8 주요 여론 선도자와의 1차 인터뷰

2.9 DBMR 시장 위치 그리드

2.1 공급업체 점유율 분석

2.11 시장 최종 커버리지 그리드

2.12 2차 소스

2.13 가정

3 요약

4 프리미엄 인사이트

4.1 페스텔 모델

4.2 포터의 5가지 힘

4.3 역학

4.4 브랜드 분석

4.5 인공 지능(AI) 및 머신 러닝(ML)의 역할: 북미 위암 진단 시장

4.6 산업 통찰력:

5 북미 위암 진단 시장, 규제

5.1 북미

5.1.1 미국 규제 시나리오

6 시장 개요

6.1 드라이버

6.1.1 위장관 종양, 림프종 및 선암의 발생 증가

6.1.2 알코올 소비 증가 및 흡연 급증

6.1.3 노령 인구의 증가

6.1.4 위암 진단 제품의 최근 발전

6.2 제약

6.2.1 위암 진단 검사 비용이 높음

6.2.2 건강 보험 정책으로부터의 충분한 재정 지원 부족

6.3 기회

6.3.1 자동화 시스템 도입 증가

6.3.2 암 진단 제품에 대한 연구 및 개발 증가

6.3.3 신흥 플레이어의 전략적 이니셔티브

6.4 과제

6.4.1 방사선 장치의 복잡한 특성을 승인하기 위한 엄격한 규정 및 정책

6.4.2 방사선 검사의 한계

7 북미 위암 진단 시장, 제품 유형별

7.1 개요

7.2 시약 및 소모품

7.2.1 키트

7.2.1.1 DNA 중합효소 키트

7.2.1.2 PCR 키트

7.2.1.3 핵산 분리 키트

7.2.1.4 기타

7.2.2 시약

7.2.2.1 분석

7.2.2.2 버퍼

7.2.2.3 프라이머

7.2.2.4 기타

7.3 도구

7.4 서비스

8 북미 위암 진단 시장, 진단 유형별

8.1 개요

8.2 확인 테스트

8.2.1 영상 테스트

8.2.1.1 PET 스캔/CT 스캔

8.2.1.2 CT 스캔

8.2.1.3 초음파

8.2.1.4 자기공명영상(MRI)

8.2.1.5 엑스레이

8.2.2 바이오마커

8.2.2.1 DNA 바이오마커

8.2.2.2 RNA 바이오마커

8.2.2.3 단백질 바이오마커

8.2.3 생검

8.3 위암 검진 검사/신체 검사

9 북미 위암 진단 시장, 연령대별

9.1 개요

9.2 노인의학

9.3 성인

9.4 소아과

10 북미 위암 진단 시장, 질병 유형별

10.1 개요

10.2 장 또는 확산성 선암

10.3 카르시노이드 종양

10.4 위장관 기질종양

10.5 위 림프종

10.6 기타

11 북미 위암 진단 시장, 단계별

11.1 개요

11.2 1단계

11.2.1 단계 IA

11.2.2 IB 단계

11.3 2단계

11.3.1 2A기

11.3.2 단계 IIB

11.4 3단계

11.4.1 단계 IIIA

11.4.2 단계 IIIB

11.4.3 단계 IIIC

11.5 스테이지 0

12 북미 위암 진단 시장, 성별별

12.1 개요

12.2 남자

12.3 여성

13 북미 위암 진단 시장, 샘플 유형별

13.1 개요

13.2 의자

13.3 조직

13.4 혈액

13.5 소변

14 북미 위암 진단 시장, 최종 사용자별

14.1 개요

14.2 병원

14.3 진단 실험실

14.4 암 연구 기관

14.5 종양학 전문 클리닉

14.6 기타

15 북미 위암 진단 시장, 유통 채널별

15.1 개요

15.2 직접 입찰

15.3 소매 판매

16 북미 위암 진단 시장, 지역별

16.1 북미

16.1.1 미국

16.1.2 캐나다

16.1.3 멕시코

17 북미 위암 진단 시장, 회사 환경

17.1 회사 점유율 분석: 북미

18 SWOT 분석

19 회사 프로필

19.1 F. 호프만-라 로슈 유한회사

19.1.1 회사 스냅샷

19.1.2 수익 분석

19.1.3 회사 점유율 분석

19.1.4 제품 포트폴리오

19.1.5 최근 개발

19.2 일반 전기

19.2.1 회사 스냅샷

19.2.2 수익 분석

19.2.3 회사 점유율 분석

19.2.4 제품 포트폴리오

19.2.5 최근 개발

19.3 애벗

19.3.1 회사 스냅샷

19.3.2 수익 분석

19.3.3 회사 점유율 분석

19.3.4 제품 포트폴리오

19.3.5 최근 개발

19.4 퀴아젠

19.4.1 회사 스냅샷

19.4.2 수익 분석

19.4.3 회사 점유율 분석

19.4.4 제품 포트폴리오

19.4.5 최근 개발

19.5 미리드 제네틱스 주식회사

19.5.1 회사 스냅샷

19.5.2 수익 분석

19.5.3 회사 점유율 분석

19.5.4 제품 포트폴리오

19.5.5 최근 개발

19.6 에이콘 연구소 주식회사

19.6.1 회사 스냅샷

19.6.2 제품 포트폴리오

19.6.3 최근 개발

19.7 아드바케어파마

19.7.1 회사 스냅샷

19.7.2 제품 포트폴리오

19.7.3 최근 개발

19.8 애질런트 테크놀로지스 주식회사

19.8.1 회사 스냅샷

19.8.2 수익 분석

19.8.3 제품 포트폴리오

19.8.4 최근 개발 사항

19.9 비오메리유

19.9.1 회사 스냅샷

19.9.2 수익 분석

19.9.3 제품 포트폴리오

19.9.4 최근 개발

19.1 바이오셉트 주식회사

19.10.1 회사 스냅샷

19.10.2 수익 분석

19.10.3 제품 포트폴리오

19.10.4 최근 개발

19.11 비오히트 오이제이

19.11.1 회사 스냅샷

19.11.2 수익 분석

19.11.3 제품 포트폴리오

19.11.4 최근 개발

19.12 디아소린 스파

19.12.1 회사 스냅샷

19.12.2 수익 분석

19.12.3 제품 포트폴리오

19.12.4 최근 개발

19.13 엔도포토닉스 주식회사

19.13.1 회사 스냅샷

19.13.2 제품 포트폴리오

19.13.3 최근 개발

19.14 파운데이션 메디신 주식회사

19.14.1 회사 스냅샷

19.14.2 제품 포트폴리오

19.14.3 최근 개발 사항

19.15 후지레바이오(AN HU 그룹 회사)

19.15.1 회사 스냅샷

19.15.2 수익 분석

19.15.3 제품 포트폴리오

19.15.4 최근 개발

19.16 미르크세스 주식회사

19.16.1 회사 스냅샷

19.16.2 제품 포트폴리오

19.16.3 최근 개발

19.17 파라곤 제노믹스 주식회사

19.17.1 회사 스냅샷

19.17.2 제품 포트폴리오

19.17.3 최근 개발 사항

19.18 테코 진단

19.18.1 회사 스냅샷

19.18.2 제품 포트폴리오

19.18.3 최근 개발

19.19 써모 피셔 사이언티픽 주식회사

19.19.1 회사 스냅샷

19.19.2 수익 분석

19.19.3 제품 포트폴리오

19.19.4 최근 개발 사항

19.2 VELA 진단

19.20.1 회사 스냅샷

19.20.2 제품 포트폴리오

19.20.3 최근 개발 사항

20 설문지

21 관련 보고서

표 목록

표 1 승인된 동반 진단 장치

표 2 아래 언급된 목록은 전 세계 여러 지역의 암 진단을 위한 PET 스캔 비용을 보여줍니다.

표 3 북미 위암 진단 시장, 제품 유형별, 2021-2030년(백만 달러)

표 4 북미 위암 진단 시장의 시약 및 소모품, 지역별, 2021-2030 (백만 달러)

표 5 북미 위암 진단 시장의 시약 및 소모품, 제품 유형별, 2021-2030년(백만 달러)

표 6 북미 위암 진단 키트 시장, 제품 유형별, 2021-2030년(백만 달러)

표 7 북미 위암 진단 시장의 시약, 제품 유형별, 2021-2030년(백만 달러)

표 8 북미 위암 진단 시장 기기, 지역별, 2021-2030 (백만 달러)

표 9 북미 위암 진단 시장 서비스, 지역별, 2021-2030 (백만 달러)

표 10 북미 위암 진단 시장, 진단 유형별, 2021-2030년(백만 달러)

표 11 북미 위암 진단 시장의 확인 테스트, 지역별, 2021-2030 (백만 달러)

표 12 북미 위암 진단 시장에서의 확인 테스트, 진단 유형별, 2021-2030년(백만 달러)

표 13 북미 위암 진단 시장에서의 영상 검사, 진단 유형별, 2021-2030년(백만 달러)

표 14 북미 위암 진단 시장의 바이오마커, 진단 유형별, 2021-2030년(백만 달러)

표 15 북미 위암 검진 검사/위암 진단 시장에서의 신체 검사, 지역별, 2021-2030년 (백만 달러)

표 16 북미 위암 진단 시장, 연령대별, 2021-2030년(백만 달러)

표 17 북미 노인의학 위암 진단 시장, 지역별, 2021-2030 (백만 달러)

표 18 북미 성인 위암 진단 시장, 지역별, 2021-2030 (백만 달러)

표 19 북미 소아 위암 진단 시장, 지역별, 2021-2030 (백만 달러)

표 20 북미 위암 진단 시장, 질병 유형별, 2021-2030년(백만 달러)

표 21 북미 장 또는 확산성 선암종 위암 진단 시장, 지역별, 2021-2030 (백만 달러)

표 22 북미 지역별 위암 진단 카르시노이드 종양 시장, 2021-2030년 지역별 (백만 달러)

표 23 북미 위장관 기질종양 위암 진단 시장, 지역별, 2021-2030 (백만 달러)

표 24 북미 위암 진단 시장, 지역별 위암 림프종, 2021-2030년(백만 달러)

표 25 북미 기타 위암 진단 시장, 지역별, 2021-2030 (백만 달러)

표 26 북미 위암 진단 시장, 단계별, 2021-2030 (백만 달러)

표 27 북미 위암 진단 시장 1단계, 지역별, 2021-2030년(백만 달러)

표 28 북미 위암 진단 시장 1단계, 단계별, 2021-2030년(백만 달러)

표 29 북미 2단계 위암 진단 시장, 지역별, 2021-2030년(백만 달러)

표 30 북미 위암 진단 시장 2단계, 단계별, 2021-2030 (백만 달러)

표 31 북미 위암 진단 시장 3단계, 지역별, 2021-2030년(백만 달러)

표 32 북미 위암 진단 시장 3단계, 단계별, 2021-2030년(백만 달러)

표 33 북미 위암 진단 시장 0단계, 지역별, 2021-2030년(백만 달러)

표 34 북미 위암 진단 시장, 성별별, 2021-2030년(백만 달러)

표 35 북미 남성 위암 진단 시장, 지역별, 2021-2030 (백만 달러)

표 36 북미 여성 위암 진단 시장, 지역별, 2021-2030 (백만 달러)

표 37 북미 위암 진단 시장, 샘플 유형별, 2021-2030년(백만 달러)

표 38 북미 지역별 위암 진단 시장(2021-2030년, 백만 달러)

표 39 북미 위암 진단 시장, 지역별, 2021-2030 (백만 달러)

표 40 북미 혈액 위암 진단 시장, 지역별, 2021-2030 (백만 달러)

표 41 북미 소변 위암 진단 시장, 지역별, 2021-2030 (백만 달러)

표 42 북미 위암 진단 시장, 최종 사용자별, 2021-2030년(백만 달러)

표 43 북미 병원의 위암 진단 시장, 지역별, 2021-2030 (백만 달러)

표 44 북미 위암 진단 시장의 진단 실험실, 지역별, 2021-2030 (백만 달러)

표 45 북미 암 연구 기관의 위암 진단 시장, 지역별, 2021-2030 (백만 달러)

표 46 북미 종양학 전문 클리닉 위암 진단 시장, 지역별, 2021-2030 (백만 달러)

표 47 북미 기타 위암 진단 시장, 지역별, 2021-2030 (백만 달러)

표 48 북미 위암 진단 시장, 유통 채널별, 2021-2030년(백만 달러)

표 49 2021-2030년 지역별 위암 진단 시장의 북미 직접 입찰(백만 달러)

표 50 북미 위암 진단 시장의 소매 판매, 지역별, 2021-2030 (백만 달러)

표 51 북미 위암 진단 시장, 국가별, 2021-2030년(백만 달러)

표 52 북미 위암 진단 시장, 제품 유형별, 2021-2030년(백만 달러)

표 53 북미 위암 진단 시장의 시약 및 소모품, 제품 유형별, 2021-2030년(백만 달러)

표 54 북미 위암 진단 키트 시장, 제품 유형별, 2021-2030년(백만 달러)

표 55 북미 위암 진단 시약 시장, 제품 유형별, 2021-2030년(백만 달러)

표 56 북미 위암 진단 시장, 진단 유형별, 2021-2030년(백만 달러)

표 57 북미 위암 진단 시장에서의 확인 테스트, 진단 유형별, 2021-2030년(백만 달러)

표 58 북미 위암 진단 시장에서의 영상 검사, 진단 유형별, 2021-2030년(백만 달러)

표 59 북미 위암 진단 바이오마커 시장, 진단 유형별, 2021-2030년(백만 달러)

표 60 북미 위암 진단 시장, 연령대별, 2021-2030 (백만 달러)

표 61 북미 위암 진단 시장, 질병 유형별, 2021-2030년(백만 달러)

표 62 북미 위암 진단 시장, 단계별, 2021-2030 (백만 달러)

표 63 북미 위암 진단 시장 1단계, 단계별, 2021-2030년(백만 달러)

표 64 북미 위암 진단 시장 2단계, 단계별, 2021-2030년(백만 달러)

표 65 북미 위암 진단 시장 3단계, 단계별, 2021-2030년(백만 달러)

표 66 북미 위암 진단 시장, 성별별, 2021-2030년(백만 달러)

표 67 북미 위암 진단 시장, 샘플 유형별, 2021-2030년(백만 달러)

표 68 북미 위암 진단 시장, 최종 사용자별, 2021-2030년(백만 달러)

표 69 북미 위암 진단 시장, 유통 채널별, 2021-2030년(백만 달러)

표 70 미국 위암 진단 시장, 제품 유형별, 2021-2030년(백만 달러)

표 71 미국 위암 진단 시장의 시약 및 소모품, 제품 유형별, 2021-2030년(백만 달러)

표 72 미국 위암 진단 키트 시장, 제품 유형별, 2021-2030년(백만 달러)

표 73 미국 위암 진단 시장의 시약, 제품 유형별, 2021-2030년(백만 달러)

표 74 미국 위암 진단 시장, 진단 유형별, 2021-2030년(백만 달러)

표 75 미국 위암 진단 시장에서의 확인 테스트, 진단 유형별, 2021-2030 (백만 달러)

표 76 미국 위암 진단 시장에서의 영상 검사, 진단 유형별, 2021-2030년(백만 달러)

표 77 미국 위암 진단 시장의 바이오마커, 진단 유형별, 2021-2030년(백만 달러)

표 78 미국 위암 진단 시장, 연령대별, 2021-2030년(백만 달러)

표 79 미국 위암 진단 시장, 질병 유형별, 2021-2030년(백만 달러)

표 80 미국 위암 진단 시장, 단계별, 2021-2030 (백만 달러)

표 81 미국 위암 진단 시장 1단계, 2021-2030년 단계별(백만 달러)

표 82 미국 위암 진단 시장 2단계, 단계별, 2021-2030년(백만 달러)

표 83 미국 위암 진단 시장 3단계, 2021-2030년 단계별(백만 달러)

표 84 미국 위암 진단 시장, 성별별, 2021-2030년(백만 달러)

표 85 미국 위암 진단 시장, 샘플 유형별, 2021-2030년(백만 달러)

표 86 미국 위암 진단 시장, 최종 사용자별, 2021-2030년(백만 달러)

표 87 미국 위암 진단 시장, 유통 채널별, 2021-2030년(백만 달러)

표 88 캐나다 위암 진단 시장, 제품 유형별, 2021-2030년(백만 달러)

표 89 캐나다 위암 진단 시장에서의 시약 및 소모품, 제품 유형별, 2021-2030년(백만 달러)

표 90 캐나다 위암 진단 키트 시장, 제품 유형별, 2021-2030 (백만 달러)

표 91 캐나다 위암 진단 시장의 시약, 제품 유형별, 2021-2030년(백만 달러)

표 92 캐나다 위암 진단 시장, 진단 유형별, 2021-2030년(백만 달러)

표 93 캐나다 위암 진단 시장에서의 확인 테스트, 진단 유형별, 2021-2030 (백만 달러)

표 94 캐나다 위암 진단 시장에서의 영상 검사, 진단 유형별, 2021-2030년(백만 달러)

표 95 캐나다 위암 진단 시장의 바이오마커, 진단 유형별, 2021-2030년(백만 달러)

표 96 캐나다 위암 진단 시장, 연령대별, 2021-2030 (백만 달러)

표 97 캐나다 위암 진단 시장, 질병 유형별, 2021-2030 (백만 달러)

표 98 캐나다 위암 진단 시장, 단계별, 2021-2030 (백만 달러)

표 99 캐나다 위암 진단 시장의 1단계, 2021-2030년 단계별(백만 달러)

표 100 캐나다 위암 진단 시장 2단계, 단계별, 2021-2030(백만 달러)

표 101 캐나다 위암 진단 시장의 3단계, 2021-2030년 단계별(백만 달러)

표 102 캐나다 위암 진단 시장, 성별별, 2021-2030 (백만 달러)

표 103 캐나다 위암 진단 시장, 샘플 유형별, 2021-2030년(백만 달러)

표 104 캐나다 위암 진단 시장, 최종 사용자별, 2021-2030년(백만 달러)

표 105 캐나다 위암 진단 시장, 유통 채널별, 2021-2030 (백만 달러)

표 106 멕시코 위암 진단 시장, 제품 유형별, 2021-2030년(백만 달러)

표 107 멕시코 위암 진단 시장의 시약 및 소모품, 제품 유형별, 2021-2030년(백만 달러)

표 108 멕시코 위암 진단 키트 시장, 제품 유형별, 2021-2030 (백만 달러)

표 109 멕시코 위암 진단 시장의 시약, 제품 유형별, 2021-2030년(백만 달러)

표 110 멕시코 위암 진단 시장, 진단 유형별, 2021-2030년(백만 달러)

표 111 멕시코 위암 진단 시장에서의 확인 테스트, 진단 유형별, 2021-2030년(백만 달러)

표 112 멕시코 위암 진단 시장에서의 영상 검사, 진단 유형별, 2021-2030년(백만 달러)

표 113 멕시코 위암 진단 시장의 바이오마커, 진단 유형별, 2021-2030년(백만 달러)

표 114 멕시코 위암 진단 시장, 연령대별, 2021-2030 (백만 달러)

표 115 멕시코 위암 진단 시장, 질병 유형별, 2021-2030년(백만 달러)

표 116 멕시코 위암 진단 시장, 단계별, 2021-2030 (백만 달러)

표 117 멕시코 위암 진단 시장 1단계, 2021-2030년 단계별(백만 달러)

표 118 멕시코 위암 진단 시장 2단계, 단계별, 2021-2030(백만 달러)

표 119 멕시코 위암 진단 시장 3단계, 2021-2030년 단계별(백만 달러)

표 120 멕시코 위암 진단 시장, 성별별, 2021-2030 (백만 달러)

표 121 멕시코 위암 진단 시장, 샘플 유형별, 2021-2030년(백만 달러)

표 122 멕시코 위암 진단 시장, 최종 사용자별, 2021-2030년(백만 달러)

표 123 멕시코 위암 진단 시장, 유통 채널별, 2021-2030년(백만 달러)

그림 목록

그림 1 북미 위암 진단 시장: 세분화

그림 2 북미 위암 진단 시장: 데이터 삼각 측량

그림 3 북미 위암 진단 시장: DROC 분석

그림 4 북미 위암 진단 시장: 북미 대 지역 시장 분석

그림 5 북미 위암 진단 시장: 회사 연구 분석

그림 6 북미 위암 진단 시장: 다변량 모델링

그림 7 북미 위암 진단 시장: 인터뷰 인구 통계

그림 8 북미 위암 진단 시장: DBMR 시장 위치 그리드

그림 9 북미 위암 진단 시장: 공급업체 점유율 분석

그림 10 북미 위암 진단 시장: 시장 최종 범위 그리드

그림 11 북미 위암 진단 시장: 세분화

그림 12 위장관 종양, 림프종 및 선암의 발생률 증가는 2023년에서 2030년 예측 기간 동안 북미 위암 진단 시장 성장을 견인할 것으로 예상됩니다.

그림 13 시약 및 소모품 부문은 2023년 및 2030년 북미 위암 진단 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다.

그림 14 북미 위암 진단 시장의 동인, 제약, 기회 및 과제

그림 15 북미 위암 진단 시장: 제품 유형별, 2022년

그림 16 북미 위암 진단 시장: 제품 유형별, 2023-2030년(백만 달러)

그림 17 북미 위암 진단 시장: 제품 유형별, CAGR(2023-2030)

그림 18 북미 위암 진단 시장: 제품 유형별, 수명 곡선

그림 19 북미 위암 진단 시장: 진단 유형별, 2022

그림 20 북미 위암 진단 시장: 진단 유형별, 2023-2030년(백만 달러)

그림 21 북미 위암 진단 시장: 진단 유형별, CAGR(2023-2030)

그림 22 북미 위암 진단 시장: 진단 유형별, 수명선 곡선

그림 23 북미 위암 진단 시장: 연령대별, 2022

그림 24 북미 위암 진단 시장: 연령대별, 2023-2030년(백만 달러)

그림 25 북미 위암 진단 시장: 연령대별, CAGR(2023-2030)

그림 26 북미 위암 진단 시장: 연령대별, 수명선 곡선

그림 27 북미 위암 진단 시장: 질병 유형별, 2022

그림 28 북미 위암 진단 시장: 질병 유형별, 2023-2030년(백만 달러)

그림 29 북미 위암 진단 시장: 질병 유형별, CAGR(2023-2030)

그림 30 북미 위암 진단 시장: 질병 유형별, 수명선 곡선

그림 31 북미 위암 진단 시장: 단계별, 2022

그림 32 북미 위암 진단 시장: 단계별, 2023-2030년(백만 달러)

그림 33 북미 위암 진단 시장: 단계별, CAGR(2023-2030)

그림 34 북미 위암 진단 시장: 단계별, 수명선 곡선

그림 35 북미 위암 진단 시장: 성별별, 2022

그림 36 북미 위암 진단 시장: 성별별, 2023-2030년(백만 달러)

그림 37 북미 위암 진단 시장: 성별, CAGR별(2023-2030)

그림 38 북미 위암 진단 시장: 성별, 수명선 곡선별

그림 39 북미 위암 진단 시장: 샘플 유형별, 2022

그림 40 북미 위암 진단 시장: 샘플 유형별, 2023-2030년(백만 달러)

그림 41 북미 위암 진단 시장: 샘플 유형별, CAGR(2023-2030)

그림 42 북미 위암 진단 시장: 샘플 유형별, 수명선 곡선

그림 43 북미 위암 진단 시장: 최종 사용자별, 2022

그림 44 북미 위암 진단 시장: 최종 사용자별, 2023-2030년(백만 달러)

그림 45 북미 위암 진단 시장: 최종 사용자별, CAGR(2023-2030)

그림 46 북미 위암 진단 시장: 최종 사용자별, 수명선 곡선

그림 47 북미 위암 진단 시장: 유통 채널별, 2022년

그림 48 북미 위암 진단 시장: 유통 채널별, 2023-2030년(백만 달러)

그림 49 북미 위암 진단 시장: 유통 채널별, CAGR(2023-2030)

그림 50 북미 위암 진단 시장: 유통 채널별, 수명선 곡선

그림 51 북미 위암 진단 시장: 스냅샷(2022)

그림 52 북미 위암 진단 시장: 국가별(2022년)

그림 53 북미 위암 진단 시장: 국가별(2023년 및 2030년)

그림 54 북미 위암 진단 시장: 국가별(2022년 및 2030년)

그림 55 북미 위암 진단 시장: 제품 유형별(2023-2030)

그림 56 북미 위암 진단 시장: 회사 점유율 2022(%)

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.