Asia Pacific Glyoxal Market

Размер рынка в млрд долларов США

CAGR :

%

USD

274.18 Million

USD

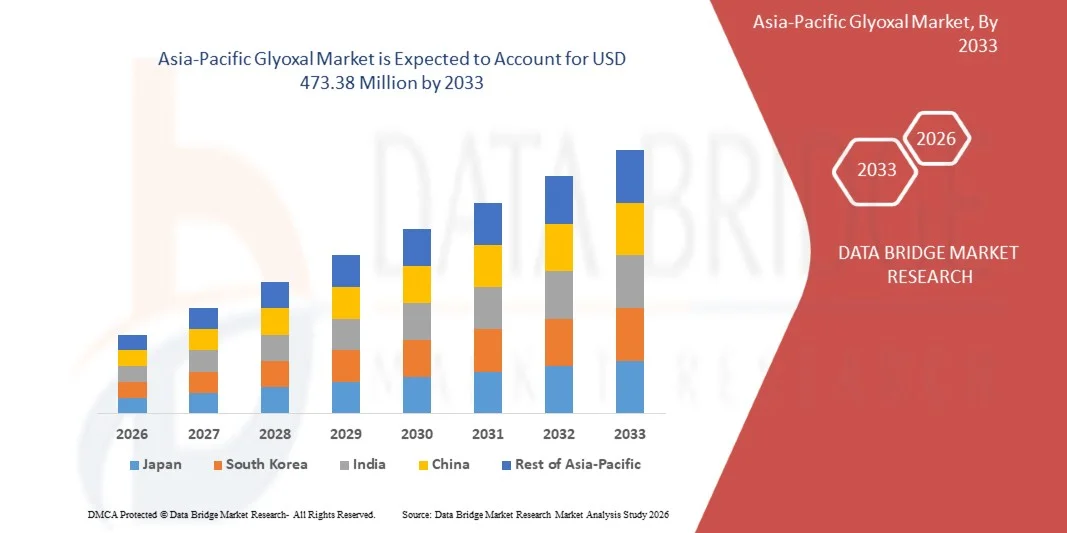

473.38 Million

2025

2033

USD

274.18 Million

USD

473.38 Million

2025

2033

| 2026 –2033 | |

| USD 274.18 Million | |

| USD 473.38 Million | |

| % | |

|

Азиатско-Тихоокеанский регионGlyoxal Market Segmentation, By Grade (Industrial Grade, Pharmaceutical Grade), Purity (90%-99%, 40%-60%, Others), Production Process (Catalytic Oxidation of Ethylene Glycol, 40%-60%, Others), Production Process (Catalytic Oxidation of Ethylene Glycol, Oxidation of Acetylene and Others), Packaging (Cross-Linking, Chemical Intermediates, Bulk), Application (Cross-Linking, Chemical Intermediates and others), Enduseuse Chemicals (Dihydroxyethylene Urea (DHEU), 2-Imidazolidinone, Glyoxalated Polyacrylamide (GPAM), Glyoxal Acid, Glyoxal Phenol Resin, Glyoxal Glycol Resin, Glyoxal Erea Diformate, Ethylene Glycol Conformate, Urea-Glyoxal Derivate, Urea-Glyox

Каков размер и обзор рынка глиоксаля в Азиатско-Тихоокеанском регионе

- Согласно анализу Data Bridge Market Research, размер рынка глиоксаля в Азиатско-Тихоокеанском регионе был оценен как274,18 млн долларов США в 2025 годуОжидается, что он достигнет473,38 млн долларов к 2033 году, вCAGR 6,1%в течение прогнозируемого периода

- Растущее использование глиоксаля в качестве связующего агента в текстильной отделке является основным фактором, стимулирующим спрос во всем регионе.

- Растущее внедрение в бумагу и упаковку для применения во влажной силе и поверхностной обработке еще больше усиливает охват рынка.

Размер рынка и прогноз

- Рыночная стоимость Азиатско-Тихоокеанского региона (2025):$274,18 млн.

- Ожидаемая рыночная стоимость (2033):473,38 млн долларов

- Прогноз CAGR (2026–2033): 6.1%

Азиатско-Тихоокеанский анализ рынка глиоксаля

- Азиатско-Тихоокеанский рынок глиоксаля обслуживает различные отрасли промышленности, включая текстиль, бумагу, смолы, фармацевтические препараты, косметику и обработку воды. Спрос обусловлен его сильными сшивающими свойствами и ролью в качестве ключевого промежуточного звена в специализированных и эксплуатационных химических составах.

- Растущая деятельность по отделке текстиля, увеличение потребления бумажной упаковки и растущее использование экологически чистых смол являются основными факторами спроса. Расширение фармацевтического производства и ужесточение правил очистки сточных вод способствуют устойчивому потреблению глиоксаля во всем мире.

- Рынок представляет собой смесь многонациональных химических производителей и региональных производителей. Конкуренция основана на чистоте продукции, конкретных марках приложений, ценообразовании, надежности поставок и соблюдении правил охраны окружающей среды и безопасности в ключевых отраслях конечного использования.

- Китай доминирует на Азиатско-Тихоокеанском рынке глиоксаля, занимая 43,69% рынка, что обусловлено крупномасштабными производственными мощностями, низкими производственными затратами и обильной доступностью сырья. Сильный спрос со стороны текстильной, смоловой, бумажной и кожевенной промышленности в сочетании с хорошо налаженной цепочкой поставок химических веществ еще больше укрепляет ее лидерство на рынке.

- Ожидается, что в 2025 году сегмент промышленного класса будет доминировать на Азиатско-Тихоокеанском рынке глиоксаля с долей 81,39% из-за его широкого использования в производстве смол, клеев и химикатов для обработки бумаги. Сегмент выигрывает от высокого спроса в крупномасштабных промышленных применениях и экономической эффективности для массового производства, что делает его предпочтительным выбором по сравнению с другими сортами.

Сфера охвата и сегментация рынка глиоксаля в Азиатско-Тихоокеанском регионе

|

Атрибуты |

Азиатско-Тихоокеанский глиоксальный ключевой рынок |

|

Сегменты покрыты |

|

|

Страны, охваченные |

Азиатско-Тихоокеанский регион

|

|

Ключевые игроки рынка |

|

|

Рыночные возможности |

|

|

Информационные наборы данных с добавленной стоимостью |

В дополнение к информации о рыночных сценариях, таких как рыночная стоимость, темпы роста, сегментация, географическое покрытие и основные игроки, рыночные отчеты, курируемые Data Bridge Market Research, также включают анализ экспорта импорта, обзор производственных мощностей, анализ потребления продукции, анализ ценового тренда, сценарий изменения климата, анализ цепочки поставок, анализ цепочки создания стоимости, обзор сырья / расходных материалов, критерии выбора поставщиков, анализ PESTLE, анализ Porter и нормативную базу. |

Каковы основные тенденции на Азиатско-Тихоокеанском рынке глиоксаля

Растущее использование глиоксаля в качестве сшивающего агента в текстильной отделке.

- Глиоксал все чаще используется в качестве сшивающего агента в текстильной отделке из-за его способности улучшать производительность ткани, не влияя на текстуру или комфорт.

- Он улучшает устойчивость к морщинам, стабильность размеров, восстановление складок и свойства легкого ухода, особенно в тканях на основе хлопка и целлюлозы.

- Glyoxal совместим с существующими процессами отделки и экономически эффективен, что делает его предпочтительным выбором в крупном текстильном производстве.

- Отраслевые отчеты (nbinno.com, Silver Fern Chemical, AlphaChem.biz, Ataman Chemicals, 2025) подчеркивают его роль в повышении прочности ткани, влагостойкости и долговечности в текстиле и коже.

- Его принятие отражает спрос швейной промышленности на прочные, морщинистые и легкие ткани, поддерживающие добавленную стоимость и неизменное качество продукции.

- Ожидается, что Glyoxal останется важным компонентом в текстильной отделке, поддерживая спрос на рынке глиоксаля в Азиатско-Тихоокеанском регионе.

Азиатско-Тихоокеанская динамика рынка глиоксаля

водитель

Растущий спрос со стороны сектора продуктов питания и напитков

- Внедрение глиоксаля в бумагу и упаковку растет благодаря его способности повышать влажную прочность, долговечность поверхности и общую производительность бумажных продуктов.

- Он улучшает влагостойкость, стабильность размеров, печатаемость и структурную целостность, что делает его ценным для упаковочных бумаг, картона и специализированных бумажных изделий.

- Отраслевые отчеты (ChemCeed, NBINNO.com, ivySCI, 2025) подчеркивают роль глиоксаля в повышении влажной и сухой прочности, уменьшении поглощения воды и повышении прочности на растяжение в бумажной и крахмальной формах.

- Его совместимость с различными марками бумаги и обработками поверхности позволяет производителям производить высококачественные, долговечные и функциональные упаковочные бумаги, которые выдерживают влажные или влажные условия.

- С ростом спроса на надежную упаковку в пищевых продуктах, потребительских товарах и промышленных секторах, глиоксаль, как ожидается, останется ключевым агентом для повышения влажности и обработки поверхностей на мировом рынке бумаги и упаковки.

Сдержанность/вызов

Сложность обработки из-за высокой реактивности и чувствительности к стабильности

- Обработка глиоксаля создает значительные проблемы из-за его высокой химической реактивности и чувствительности к условиям хранения и окружающей среды. Неправильное хранение, колебания температуры или длительное воздействие воздуха и света могут привести к полимеризации или деградации, что требует строгих протоколов безопасности, специализированных решений для хранения и контролируемых методов транспортировки. Эти требования увеличивают эксплуатационные расходы и требуют квалифицированного персонала, особенно на малых и средних производственных предприятиях.

- Например, как сообщает Amzole India Pvt. Ltd. в июле 2025 года, в отчете о безопасности глиоксаля 40% подчеркивается его высокореактивный характер и критическая потребность в специализированной обработке для предотвращения полимеризации, воздействия раздражителей и реакций с несовместимыми веществами, такими как сильные окислители и основания. Аналогичным образом, документация ChemSpider в апреле 2025 года подчеркивает, что глиоксал может бурно реагировать с воздухом, водой и химическими агентами, такими как гидроксид натрия, что делает контролируемое хранение, тщательную транспортировку и строгие меры безопасности необходимыми во время обработки.

- Эти сложности непосредственно влияют на хранение, транспортировку и эксплуатационные расходы, создавая особые проблемы для небольших производителей. Несмотря на эти ограничения, глиоксаль по-прежнему широко используется в текстиле, бумаге, клеях и химических промежуточных продуктах из-за его универсального применения и функциональных преимуществ.

- Следовательно, тщательное управление реактивными свойствами глиоксаля имеет важное значение для безопасного и эффективного использования, гарантируя, что отрасли могут использовать его преимущества при одновременном снижении рисков на мировом рынке.

Азиатско-Тихоокеанский рынок глиоксаля

Рынок сегментирован на основе класса, чистоты, производственного процесса, применения упаковки, химикатов конечного использования и промышленности конечного использования.

По степени

Исходя из сорта, Азиатско-Тихоокеанский рынок глиоксаля в основном сегментирован на промышленный и фармацевтический классы.

По прогнозам, к 2026 году сегмент промышленного класса будет доминировать на рынке, составляя 81,30% от общей доли. Это доминирование объясняется его широким применением в различных отраслях промышленности, включая текстиль, обработку бумаги, смолы, обработку кожи и обработку воды. Высокое потребление глиоксала промышленного класса также поддерживается его экономичностью и эффективностью в крупномасштабных операциях. Кроме того, быстрое расширение промышленного и производственного секторов в Азиатско-Тихоокеанском регионе стимулирует сильный и устойчивый спрос. В результате ожидается, что глиоксал промышленного класса останется ключевым драйвером роста на региональном рынке.

Ожидается, что сегмент фармацевтического класса на Азиатско-Тихоокеанском рынке глиоксаля будет расти быстрее всего с 2026 по 2033 год, что обусловлено растущим спросом на фармацевтический синтез, строгими нормативными требованиями к химическим веществам высокой чистоты и расширением передового производства лекарств и специализированных приложений. Эти факторы способствуют принятию высококачественного глиоксала в API и инновационных лекарственных препаратах.

По чистоте

Исходя из чистоты, Азиатско-Тихоокеанский рынок глиоксаля подразделяется на 90%-99%, 40%-60% и другие.

Ожидается, что к 2026 году сегмент чистоты 40%-60% будет доминировать на рынке, что составит 72,34% от общей доли. Выдающееся положение этого сегмента объясняется его превосходной производительностью, более высокой реактивностью и пригодностью для передовых применений в фармацевтике, специальных смолах, текстиле и косметике. Его неизменное качество, наряду с соблюдением строгих отраслевых стандартов, еще больше стимулирует сильный и устойчивый спрос. Кроме того, баланс между эффективностью и экономичностью делает этот диапазон чистоты очень предпочтительным для производителей. В результате, по прогнозам, сегмент чистоты 40-60% останется основным фактором роста на Азиатско-Тихоокеанском рынке глиоксаля.

Сегмент чистоты 90%-99% на Азиатско-Тихоокеанском рынке глиоксаля, как ожидается, станет свидетелем самого быстрого роста с 2026 по 2033 год.фармацевтическийи специальное химическое применение, которое требует глиоксаля высокой чистоты, наряду с растущим спросом на передовые лекарственные препараты и соответствующие нормативным требованиям производственные процессы.

Производственный процесс

На основе производственного процесса Азиатско-Тихоокеанский рынок глиоксаля подразделяется на каталитическое окисление этиленгликоля, окисление ацетилена и другие.

Ожидается, что к 2026 году сегмент каталитического окисления этиленгликоля будет доминировать на рынке, что составит 89,61% от общей доли. Доминирование этого сегмента обусловлено его более высокой эффективностью производства, лучшим контролем урожайности и более низким уровнем примесей по сравнению с процессами на основе ацетилена. Кроме того, он обеспечивает повышенную безопасность и более экологичен, что делает его очень подходящим для крупномасштабного производства. Экономическая эффективность и масштабируемость этого метода еще больше усиливают его предпочтение среди производителей. В результате маршрут каталитического окисления останется основным драйвером роста на Азиатско-Тихоокеанском рынке глиоксаля.

Сегмент производственных процессов «Окисление ацетилена» на Азиатско-Тихоокеанском рынке глиоксаля, как ожидается, продемонстрирует самый быстрый рост с 2026 по 2033 год, обусловленный его способностью производить глиоксал высокой чистоты, подходящий для фармацевтических и специализированных химических применений, а также растущим спросом на передовые лекарственные препараты и соблюдением строгих стандартов качества и нормативных требований.

Упаковка

На основе упаковки азиатско-тихоокеанский рынок глиоксаля подразделяется на барабаны, композитный IBC, навал, джерриканы и бутылки.

Ожидается, что к 2026 году сегмент Bottles будет доминировать на рынке, составляя 38,28% от общей доли. Это доминирование объясняется его универсальностью, простотой обработки и безопасным хранением, особенно для приложений с небольшим количеством. Бутылки особенно подходят для фармацевтических препаратов, косметики и специальных химических применений, где точность и безопасность имеют решающее значение. Кроме того, их широкая доступность и экономически эффективное производство способствуют активному внедрению в различных отраслях. Удобство и надежность упаковки для бутылок делают ее предпочтительным выбором как для производителей, так и для конечных пользователей.

Ожидается, что сегмент упаковки «Composite IBC» на Азиатско-Тихоокеанском рынке глиоксаля продемонстрирует самый быстрый рост с 2026 по 2033 год, обусловленный его эффективностью в хранении и транспортировке сыпучих химических веществ, повышенной безопасностью и химической устойчивостью, а также растущим спросом со стороны фармацевтических, специализированных химических и промышленных пользователей, которым требуются надежные решения для упаковки большой емкости.

С помощью приложения

На основе упаковки азиатско-тихоокеанский рынок глиоксаля подразделяется на барабаны, композитный IBC, навал, джерриканы и бутылки.

Ожидается, что к 2026 году сегмент Bottles будет доминировать на рынке, составляя 64,31% от общей доли. Это доминирование объясняется его универсальностью, простотой обработки и безопасным хранением, особенно для приложений с небольшим количеством. Бутылки особенно подходят для фармацевтических препаратов, косметики и специальных химических применений, где точность и безопасность имеют решающее значение. Кроме того, их широкая доступность и экономически эффективное производство способствуют активному внедрению в различных отраслях. Удобство и надежность упаковки для бутылок делают ее предпочтительным выбором как для производителей, так и для конечных пользователей.

Сегмент применения химических посредников на Азиатско-Тихоокеанском рынке глиоксаля, как ожидается, будет самым быстрорастущим сегментом с 2026 по 2033 год, что обусловлено растущим спросом на смолы, полимеры и специальные химические вещества, расширением химической обрабатывающей промышленности и использованием глиоксаля в качестве универсального перекрестного связывания и реактивного промежуточного продукта в промышленных и специализированных приложениях.

Конечные химикаты

На основе химических веществ конечного использования Азиатско-Тихоокеанский рынок глиоксаля сегментируется в дигидроксиэтиленовую мочевину (DHEU), 2-имидазолидинон, глиоксалированный полиакриламид (GPAM), глиоксалированную крахмальную кислоту, глиоксалированную фенольную смолу, глиоксаловую смолу мочевины, этиленгликолевую диформацию, концентрат уреа-глиоксалина, производные квиноксалина, метилолглиоксал, глиоксал-бис (2-гидроксианил), глиоксальский бисульфит натрия, квиноксалин, 2-метилимидазол, имидазол, гликолурил, аллантоин и тетраметилол ацетилендиуреа.

Ожидается, что к 2026 году сегмент Dihydroxyethylene Urea (DHEU) будет доминировать на рынке, составляя 17,79% от общей доли. Его доминирование обусловлено его широкой применимостью в текстильной отделке, обработке бумаги и производстве смолы. Сегмент выигрывает от высокой реактивности, стабильной производительности и совместимости с различными промышленными процессами. Кроме того, растущий спрос на высококачественные текстильные изделия и специализированные химические продукты в Азиатско-Тихоокеанском регионе поддерживает его сильные позиции на рынке. Эффективность и экономичность DHEU еще больше усиливают его предпочтения среди производителей и конечных пользователей.

Сегмент химикатов конечного использования 2-Имидазолидинона на Азиатско-Тихоокеанском рынке глиоксаля, как ожидается, будет самым быстрорастущим с 2026 по 2033 год, что обусловлено его растущим использованием в фармацевтических препаратах, агрохимикатах и специальных химических приложениях. Его рост подпитывается растущим спросом на глиоксаль высокой чистоты в качестве ключевого промежуточного соединения в синтезе 2-имидазолидинона для передовых составов и соответствующего нормативным требованиям химического производства.

конечным пользователем

На базе конечного пользователя Азиатско-Тихоокеанский рынок глиоксаля сегментирован на текстиль, целлюлозу и бумагу, кожу, краски и покрытия, водоочистку, фармацевтику, бытовую продукцию,косметикаи личной гигиены, упаковки, электротехники и электроники, нефти и газа и других.

Ожидается, что к 2026 году текстильный сегмент будет доминировать на рынке, составляя 33,55% от общей доли. Этот рост обусловлен его широким использованием в отделке тканей, устойчивости к морщинам и резистентности к складкам. Растущий спрос на прочный и высококачественный текстиль в сочетании с быстрым расширением в швейной и мебельной промышленности еще больше поддерживает рост рынка. Кроме того, рост потребительских предпочтений в отношении премиальных и долговечных тканей стимулирует принятие решений на основе глиоксаля. В результате текстильный сегмент останется ключевым участником Азиатско-Тихоокеанского рынка глиоксаля.

Ожидается, что сегмент конечных пользователей целлюлозы и бумаги на Азиатско-Тихоокеанском рынке глиоксаля будет самым быстрорастущим с 2026 по 2033 год, что обусловлено растущим спросом на смолы с влажной прочностью и химические добавки, которые повышают долговечность и качество бумаги. Рост поддерживается расширением бумажной и упаковочной промышленности и переходом к высокоэффективным, устойчивым бумажным продуктам.

Азиатско-Тихоокеанский региональный анализ рынка глиоксаля

- В 2026 году Китай, по прогнозам, будет доминировать на Азиатско-Тихоокеанском рынке глиоксаля, что составит 43,88% от общей выручки. Это лидерство обусловлено быстрой индустриализацией, высоким спросом со стороны текстильной и бумажной промышленности и хорошо развитой инфраструктурой химического производства в стране.

- Индия переживает быстрый рост благодаря увеличению производства текстиля и бумаги, расширению промышленного применения и увеличению инвестиций в химическое производство и процессы отделки с добавленной стоимостью.

- В Японии наблюдается рост благодаря передовым технологиям химического производства, высокому спросу на специализированные химические вещества и внедрению глиоксаля в текстильной, бумажной и лакокрасочной промышленности.

- Южная Корея переживает рост, обусловленный ее сильной промышленной базой, увеличением использования глиоксаля в текстиле, бумаге и клеях, а также акцентом на высокоэффективные и добавленные в стоимость химические приложения.

Индия Азиатско-Тихоокеанский глиоксальный рынок

Индия переживает быстрый рост на Азиатско-Тихоокеанском рынке глиоксаля из-за расширения производства текстиля и бумаги и роста промышленного применения. Растущие инвестиции в химическое производство и процессы отделки с добавленной стоимостью способствуют более широкому внедрению. Спрос на прочные ткани и высокопроизводительные бумажные изделия стимулирует расширение рынка. Ожидается, что по мере того, как отрасли сосредоточатся на эффективности и качестве, индийский рынок глиоксаля в Азиатско-Тихоокеанском регионе продолжит свою восходящую траекторию.

Япония Азиатско-Тихоокеанский глиоксальный рынок

Японский рынок глиоксаля в Азиатско-Тихоокеанском регионе демонстрирует рост, обусловленный передовыми технологиями химического производства и высоким спросом на специализированные химические вещества. Принятие глиоксаля в текстиле, бумаге, покрытиях и клеях поддерживает различные промышленные применения. Ориентация на высокопроизводительные химические продукты с добавленной стоимостью способствует дальнейшему развитию рынка. Ожидается, что постоянные инновации и технологический прогресс будут поддерживать рост рынка Японии.

Основными лидерами рынка, работающими на рынке, являются:

- Asis Scientific Pty Ltd (Австралия)

- Ataman Chemicals (Индия)

- BASF SE (Германия)

- Bidvest Chemical (Южная Африка)

- Bisley Asia (M) Sdn Bhd (Малайзия)

- Eastman Chemical Company (США)

- Fluorochem Limited (Великобритания)

- Fujifilm Wako Pure Chemical Corporation (Япония)

- Glentham Life Sciences Limited (Великобритания)

- GetChem Co., Ltd. (Китай)

- Hanna Instruments Ltd (США)

- Himedia Laboratories (Индия)

- Канто Кагаку (Япония)

- Кемира Ойдж (Финляндия)

- Merck KGaA (Германия)

- Meru Chem Pvt. Ltd (Индия)

- Muby Chemicals (Индия)

- Multichem Specialities Private Limited (Индия)

- Oakwood Products Inc. (США)

- Otto Chemie Pvt. Ltd (Индия)

- Oxford Lab Fine Chem LLP (Индия)

- Santa Cruz Biotechnology Inc. (США)

- Сасол (Южная Африка)

- Silver Fern Chemical, Inc. (США)

- Thermo Fisher Scientific Inc. (США)

- Univar Solutions LLC (США)

- Weylchem International GmbH (Германия)

- Zhishang Chemical (Китай)

Последние события на Азиатско-Тихоокеанском рынке глиоксаля

- В июне 2022 года Univar Solutions была назначена эксклюзивным дистрибьютором BASF Chemical Intermediates’ Glyoxal в США и Канаде. Это партнерство направлено на то, чтобы предоставить клиентам в текстильной, дезинфекционной, бумажной, кожевенной, косметической и эпоксидной промышленности надежный доступ к Glyoxal BASF, биоразлагаемому сшивающему агенту, который повышает гибкость, вязкость, антиморщинные свойства, размягчение и влагостойкость в различных составах. Это сотрудничество поможет BASF укрепить свое присутствие на рынке в Северной Америке, используя обширную дистрибьюторскую сеть Univar Solutions и возможности цепочки поставок, обеспечивая более широкий охват и надежную доставку Glyoxal клиентам.

- В январе Merck KGaA объявила о завершении сделки по приобретению химического бизнеса Mecaro, в настоящее время работающего под названием M Chemicals Inc. Это приобретение расширило возможности Merck в области исследований и разработок, а также производственные мощности, укрепив портфель полупроводниковых материалов-прекурсоров и химических веществ электроники. Хотя это стратегический рост в химическом бизнесе Merck, приобретение не связано с продуктами из глиоксаля, поскольку основное внимание уделяется передовым материалам для полупроводниковой и электронной промышленности, а не специальной химии альдегидов.

- В декабре 2025 года Thermo Fisher Scientific Inc. объявила о запуске двух новых продуктов Gibco Bacto CD Supreme FPM Plus и Gibco Bacto CD Supreme Feed (2X), которые расширяют линейку химически определенных носителей Gibco Bacto CD для улучшения и упрощения рабочих процессов биопроизводства Escherichia coli (E. coli). Эти химически определенные составы следующего поколения предназначены для поддержки более высоких урожаев, последовательной производительности и масштабируемого производства плазмидной ДНК и рекомбинантных белков, особенно для применения в генной терапии и разработке мРНК-вакцины.

- В мае 2025 года Alpha Chemika расширила свой портфель лабораторных реагентов и тонких химических веществ, внедрив дополнительные продукты класса AR / GR / LR и диверсифицированные специализированные лабораторные химические вещества для поддержки аналитических, фармацевтических и научно-исследовательских приложений, усиливая свою приверженность удовлетворению меняющегося глобального исследовательского и промышленного спроса.

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Содержание

1 Введение

1.1 Цели исследования

1.2 Маркетологическое определение

1.3 ОБЗОР АСИА-ПАЦИФИЧЕСКОГО ГЛИОКСАЛЬНОГО МАРКЕТА

1.4 Ограничения

1.5 МАРКЕТЫ

2 МАРКЕТНАЯ СЕГМЕНТАЦИЯ

2.1 Приняты меры

2.2 ГЕОГРАФИЧЕСКАЯ СКОПА

2,3 года, присланные на обучение

2.4 КУРРЕНСИЯ И ПРИЧИНА

2.5 DBMR TRIPOD DATA VALIDATION

2.6 МУЛЬТИВАРИАТНОЕ МОДЕЛЛирование

2.7 ПРОДУКТНЫЙ ТИП ЛИФЕЛИНА

2.8 Первичное Интервью с ключевыми лидерами

2.9 DBMR MARKET POSITION GRID

2.1 ПОЛЬЗОВАТЕЛЬ ПОЛЬЗОВАТЕЛЬНЫЙ КОВЕРАГ

2.11 Вторичные источники

2.12 Предложения

3 ИСПОЛНИТЕЛЬНАЯ РЕЗЮМЕ

4 Премиум Впечатления

4.1 ASIA-PACIFIC GLYOXAL MARKET: VALUE CHAIN ANALYSIS

4.1.1 RAW MATERIAL & FEEDSTOCK SUPPLY (5%-10%)

4.1.2 Мануфактурирование и обработка (15%-25%)

4.1.3 ДИСТРИБУЦИЯ И ЛОГИСТИКА (30%–40% ДОЛЖНОСТЬ)

4.1.4 Индустрии конечного использования и каналы продаж (10% - 20%)

4.2 Вспомогательный анализ цепи

4.2.1 Сырьевое сырье и производство

4.2.2 ПРОЦЕССИРОВАНИЕ И ПРОИЗВОДСТВО (ПРОДУКЦИЯ)

4.2.3 Логистика снабжения и распределения (Передача)

4.2.4 СТОИТЕЛЬНЫЕ И КОММЕРЧЕСКИЕ ШАНСЫ ПОКУПАТЕЛЯ (ДИСТРИБУЦИЯ И ПРОДАЖА)

4.3 АНАЛИЗ ПЯТИ СИЛ ПОРТЕРА

4.3.1 СОСТОЯТЕЛЬНАЯ ВЛАСТЬ ПОКУПАТЕЛЕЙ / ПОКУПАТЕЛЕЙ - ВЫСОКО

4.3.2 Угроза новых арендаторов - СМЕРТЬ

4.3.3 Угроза субститутных продуктов - СОДЕРЖАНИЕ ВЫСОКОМУ

4.3.4 СОГЛАШАЮЩАЯСЯ ВЛАСТЬ ПОСТОЯТЕЛЕЙ - СОВРЕМЕННО

4.3.5 ИНТЕНСИТНОСТЬ КОМПЕТИВНОЙ РИВАЛЬНОСТИ - ВЫСОКО

5 МАРКЕТНЫЙ ОБЗОР

5.1 Водители

5.1.1 УТИЛИЗАЦИЯ ГЛИОКСАЛА как КРОССЛИНГНУЮ АГЕНТУ В ТЕКСТИЛЬНОМ РЕШЕНИИ.

5.1.2 Растущее принятие в Папуа-Новой Гвинее и ПАККАГИРОВАНИЕ для ПРИМЕНЕНИЙ НА ПРИМЕЧАНИЯ СВЯЗИ И СУФРАЦИИ.

5.1.3 ИСКЛЮЧЕНИЕ МЕЖДУНАРОДНОГО ХИМИЧЕСКОГО ТРАНСПОРТА В ФАРМАЦЕВТИКАХ И АГРОХИМИКАХ.

5.1.4 Повышение эффективности низкомолекулярных альдегидов в осадочных и адгезивных системах.

5.2 УВЕДОМЛЕНИЯ

5.2.1 ОБЯЗАТЕЛЬНОСТЬ РЕАКТИВНОСТИ И СТОЯТЕЛЬНОСТИ

5.2.2 ДОСТУПНОСТЬ ПРИМЕНЕНИЯ-СПЕЦИФИЧЕСКИХ ХИМИЧЕСКИХ ПОСТУТОВ.

5.3 Возможность

5.3.1 ВОЛАТИТЕЛЬНОСТЬ В СТРОИТЕЛЬНОЙ СТРОИТЕЛЬНОСТИ ПРЕДОСТАВЛЕНИЯ СТРОИТЕЛЬНОСТИ

5.3.2 СТРОИТЕЛЬНЫЕ ОБЩИЕ И ОККУПАЦИОННЫЕ ПРАВИЛА БЕЗОПАСНОСТИ.

5.3.3 Ограниченная производственная дифференциация в ценовом рынке

5.4 Вызовы

5.4.1 РАЗВИТИЕ МОДИФИРОВАННЫХ И ПРИМЕНИТЕЛЬНЫХ ГЛИОКСАЛЬНЫХ ГРАДОВ.

5.4.2 ОБЯЗАТЕЛЬНОЕ ЗАЯВЛЕНИЕ ОТ ЭМЕРГИРОВАНИЯ ИНДУСТРИАЛЬНЫХ ЭКОНОМИКИ

6 ASIA-PACIFIC GLYOXAL MARKET, BY GRADE

6.1 Проверка

6.2 Промышленная лестница

6.3 Фармацевтическая лестница

6.4 ASIA-PACIFIC GLYOXAL MARKET, BY GRADE, 2018-2033

6.4.1 Промышленная лестница

6.4.2 Фармацевтическая лестница

6.5 ASIA-PACIFIC INDUSTRIAL GRADE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

6.5.1 ASIA-PACIFIC

6.5.2 Северная Америка

6.5.3 Европа

6.5.4 Средний Восток и Африка

6.5.5 Южная Америка

6.6 ASIA-PACIFIC PHARMACEUTICAL GRADE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

6.6.1 ASIA-PACIFIC

6.6.2 Северная Америка

6.6.3 Евро

6.6.4 Средний Восток и Африка

6.6.5 Южная Америка

7 ASIA-PACIFIC GLYOXAL MARKET, BY PURITY

7.1 Проверка

7.1.1 40%-60%

7.1.2 90%-99%

7.1.3 Другие

7.2 ASIA-PACIFIC 40%-60% в ГЛЫОКСАЛЬНОМ РЫНКЕ, РЕГИОН, 2018-2033 (USD THOUSAND)

7.2.1 ASIA-PACIFIC

7.2.2 Северная Америка

7.2.3 Европа

7.2.4 Средний Восток и Африка

7.2.5 Южная Америка

7.3 ASIA-PACIFIC 90%-99% в ГЛЫОКСАЛЬНОМ РЫНКЕ, ПО РЕГИОНУ, 2018-2033 (USD THOUSAND)

7.3.1 ASIA-PACIFIC

7.3.2 Северная Америка

7.3.3 Евро

7.3.4 Средний Восток и Африка

7.3.5 Южная Америка

7.4 АСИА-ПАЦИФИЧЕСКИЕ ДРУГИ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ПО РЕГИОНУ, 2018-2033 (USD THOUSAND)

7.4.1 ASIA-PACIFIC

7.4.2 Северная Америка

7.4.3 Европа

7.4.4 Средний Восток и Африка

7.4.5 Южная Америка

8 ASIA-PACIFIC GLYOXAL MARKET, BY ПРОДУКЦИОННЫЙ ПРОЦЕСС

8.1 Проверка

8.1.1 Каталитическое окисление этиленгликоля

8.1.2 Окисление ацетилена

8.1.3 Другие

8.2 ASIA-PACIFIC CATALYTIC OXIDATION OF ETHYLENE GLYCOL IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.2.1 ASIA-PACIFIC

8.2.2 Северная Америка

8.2.3 Европа

8.2.4 Средний Восток и Африка

8.2.5 Южная Америка

8.3 ASIA-PACIFIC OXIDATION ACETYLENE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.3.1 ASIA-PACIFIC

8.3.2 Северная Америка

8.3.3 Евро

8.3.4 Средний Восток и Африка

8.3.5 Южная Америка

8.4 АСИА-ПАЦИФИЧЕСКИЕ ДРУГИ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ПО РЕГИОНУ, 2018-2033 (USD THOUSAND)

8.4.1 ASIA-PACIFIC

8.4.2 Северная Америка

8.4.3 Европа

8.4.4 Средний Восток и Африка

8.4.5 Южная Америка

9 ASIA-PACIFIC GLYOXAL MARKET, BY PACKAGING

9.1 Проверка

9.2 ПРАВИЛА

9.3 Состав КСГМГ

9,4 балка

9.5 Джерриканс

9.6 Ботлеты

9.7 ASIA-PACIFIC DRUMS IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

9.7.1 ПЛАСТИЧЕСКИЕ ДРУМЫ (ПЭВП)

9.7.2 ДРУМЫ ТИГТ-ХИД

9.7.3 ЛИНЕРЫ В СТРАНАХ

9.7.4 ПРАВИЛА С КОТОРЫМИ ХИМИЧЕСКОЙ СОБСТВЕННОСТЬЮ

9.7.5 ДРУМЫ ОТКРЫТЫХ ТОПОВ

9.8 ASIA-PACIFIC DRUMS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.8.1 ASIA-PACIFIC

9.8.2 Северная Америка

9.8.3 Европа

9.8.4 Средний Восток и Африка

9.8.5 Южная Америка

9.9 ASIA-PACIFIC COMPOSITE IBC IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

9.9.1 Составные КСГМГ

9.9.2 ПРАВОВЫЕ КСГМГ

9.9.3 КСГМГ с изоляцией

9.9.4 Другие

9.1 ASIA-PACIFIC COMPOSITE IBC in GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.10.1 ASIA-PACIFIC

9.10.2 Северная Америка

9.10.3 Евро

9.10.4 Среднее Восток и Африка

9.10.5 Южная Америка

9.11 ASIA-PACIFIC BULK IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.11.1 ASIA-PACIFIC

9.11.2 Северная Америка

9.11.3 Евро

9.11.4 Средний Восток и Африка

9.11.5 Южная Америка

9.12 ASIA-PACIFIC JERRYCANS IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

9.12.1 Пластические иерриканы

9.12.2 Замкнутые иерриканы

9.12.3 МЕТАЛЬНЫЕ ДЖЕРРИКАНСЫ

9.12.4 Другие Иерриканы

9.13 ASIA-PACIFIC JERRYCANS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.13.1 ASIA-PACIFIC

9.13.2 Северная Америка

9.13.3 Евро

9.13.4 Среднее Восток и Африка

9.13.5 Южная Америка

9.14 ASIA-PACIFIC BOTTLES IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

9.14.1 БОТТЛЫ МОЛЬШЕЙ ЛАБОРАТОРИИ

9.14.2 КОСМЕТИЧЕСКИЕ / ПЕРСОНАЛЬНЫЕ КРЕДИТНЫЕ ИСПОЛЬЗОВАНИЯ БОТТЛЕЙ

9.14.3 Ботлеты со специальными материалами

9.14.4 Другие буклеты

9.15 ASIA-PACIFIC BOTTLES IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.15.1 ASIA-PACIFIC

9.15.2 Северная Америка

9.15.3 Евро

9.15.4 Среднее Восток и Африка

9.15.5 Южная Америка

10 ASIA-PACIFIC GLYOXAL MARKET

10.1 Проверка

10.2 Кросс-лизинг

10.3 Химические интермедии

10.4 Другие

10.5 ASIA-PACIFIC CROSS-LINKING IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

10.5.1 ГЛЯКСАЛАТНЫЙ ПОЛИАКРИЛАМИД (ГПАМ)

10.5.2 ГЛИОКСАЛЬНЫЙ СТАРТ

10.6 ASIA-PACIFIC CROSS-LINKING IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.6.1 ASIA-PACIFIC

10.6.2 Северная Америка

10.6.3 Европа

10.6.4 Средний Восток и Африка

10.6.5 Южная Америка

10.7 ASIA-PACIFIC CHEMICAL INTERMEDIATES, IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

10.7.1 ПИЛЬНЫЕ ХИМИЧЕСКИЕ ПРОИЗВОДЫ

10.7.2 Процедура ПОЛИМЕР

10.8 ASIA-PACIFIC BULK CHEMICALS MANUFACTURING IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

10.8.1 2-Имидазолидинон

10.8.2 Диформат этиленгликоля

10.8.3 Квиноксалиновые испытания

10.9 АСИА-ПАЦИФИЧЕСКИЙ ПОЛИМЕР, ОБРАЩАЮЩИЙСЯ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ТИП, 2018-2033 (USD THOUSAND)

10.9.1 GLYOXAL REA RESIN

10.9.2 GLYOXAL PHENOL RESIN

10.9.3 GLYOXAL-BIS(2-HYDROXYANIL)

10.1 ASIA-PACIFIC CHEMICAL INTERMEDIATES IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.10.1 АСИА-ПАСИФИК

10.10.2 Северная Америка

10.10.3 Европа

10.10.4 Среднее Восток и Африка

10.10.5 Южная Америка

10.11 АСИА-ПАЦИФИЧЕСКИЕ ДРУГИЕ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

10.11.1 Дигидроксиэтиленовая мочевина (ДГЭУ)

10.11.2 МЕТИЛОЛ ГЛИОКСАЛ

10.12 АСИА-ПАЦИФИЧЕСКИЕ ДРУГИ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ПО РЕГИОНУ, 2018-2033 (USD THOUSAND)

10.12.1 ASIA-PACIFIC

10.12.2 Северная Америка

10.12.3 Европа

10.12.4 Среднее Восток и Африка

10.12.5 Южная Америка

11 ASIA-PACIFIC GLYOXAL MARKET, BY END-USE CHEMICALS

11.1 Проверка

11.2 DIHYDROXYETHYLENE UREA (DHEU)

11.3 2-Имидазолидинон

11.4 GLYOXALATED POLYACRYLAMIDE (GPAM)

11.5 ГЛИОКСИЛЬНЫЙ ДОК

11.6 ГЛИОКСАЛЬНЫЙ ЗВЕЗД

11.7 ГЛЁКСАЛЬНЫЙ ФЕНОЛ РЕЗИН

11.8 ГЛЁКСАЛЬНЫЙ РЕЗИН

11.9 Диформат этиленгликоля

11.1 УРЕА-ГЛИОКСАЛЬНЫЙ КОНЦЕНТРАТ

11.11 Квиноксалинские испытания

11.12 МЕТИЛЛ ГЛИОКСАЛ

11.13 GLYOXAL-BIS (2-HYDROXYANIL)

11.14 GLYOXAL SODIUM BISULFITE

11.15 Квиноксалин

11.16 2-метилимидазол

11.17 Имидазол

11.18 ГЛИКОЛУРИЛ

11.19 Аллантоин

11.2 ТЕТРАМЕТИЛОЛЬНАЯ АЦЕТИЛЕНЕДИУРА

11.21 ASIA-PACIFIC DIHYDROXYETHYLENE UREA (DHEU) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.21.1 ASIA-PACIFIC

11.21.2 Северная Америка

11.21.3 Евро

11.21.4 Среднее Восток и Африка

11.21.5 Южная Америка

11.22 ASIA-PACIFIC 2-IMIDAZOLIDINONE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.22.1 ASIA-PACIFIC

11.22.2 Северная Америка

11.22.3 Евро

11.22.4 Среднее Восток и Африка

11.22.5 Южная Америка

11.23 ASIA-PACIFIC GLYOXALATED POLYACRYLAMIDE (GPAM) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.23.1 ASIA-PACIFIC

11.23.2 Северная Америка

11.23.3 Европа

11.23.4 Средний Восток и Африка

11.23.5 Южная Америка

11.24 ASIA-PACIFIC GLYOXYLIC ACID IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.24.1 ASIA-PACIFIC

11.24.2 Северная Америка

11.24.3 Евро

11.24.4 Среднее Восток и Африка

11.24.5 Южная Америка

11.25 ASIA-PACIFIC GLYOXALATED STARCH IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.25.1 ASIA-PACIFIC

11.25.2 Северная Америка

11.25.3 Евро

11.25.4 Среднее Восток и Африка

11.25.5 Южная Америка

11.26 ASIA-PACIFIC GLYOXAL PHENOL RESIN IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.26.1 ASIA-PACIFIC

11.26.2 Северная Америка

11.26.3 Евро

11.26.4 Среднее Восток и Африка

11.26.5 Южная Америка

11.27 ASIA-PACIFIC GLYOXAL UREA RESIN IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.27.1 ASIA-PACIFIC

11.27.2 Северная Америка

11.27.3 Евро

11.27.4 Среднее Восток и Африка

11.27.5 Южная Америка

11.28 ASIA-PACIFIC ETHYLENE GLYCOL DIFORMATE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.28.1 АСИА-ПАСИФИК

11.28.2 Северная Америка

11.28.3 Евро

11.28.4 Среднее Восток и Африка

11.28.5 Южная Америка

11.29 ASIA-PACIFIC UREA-GLYOXAL CONCENTRATE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.29.1 ASIA-PACIFIC

11.29.2 Северная Америка

11.29.3 Евро

11.29.4 Среднее Восток и Африка

11.29.5 Южная Америка

11.3 ASIA-PACIFIC QUINOXALINE DERIVATIVES IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.30.1 ASIA-PACIFIC

11.30.2 Северная Америка

11.30.3 Евро

11.30.4 Среднее Восток и Африка

11.30.5 Южная Америка

11.31 ASIA-PACIFIC METHYLOL GLYOXAL IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.31.1 ASIA-PACIFIC

11.31.2 Северная Америка

11.31.3 Евро

11.31.4 Среднее Восток и Африка

11.31.5 Южная Америка

11.32 ASIA-PACIFIC GLYOXAL-BIS(2-HYDROXYANIL) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.32.1 ASIA-PACIFIC

11.32.2 Северная Америка

11.32.3 Евро

11.32.4 Среднее Восток и Африка

11.32.5 Южная Америка

11.33 ASIA-PACIFIC GLYOXAL SODIUM BISULFITE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.33.1 ASIA-PACIFIC

11.33.2 Северная Америка

11.33.3 Европа

11.33.4 Среднее Восток и Африка

11.33.5 Южная Америка

11.34 ASIA-PACIFIC QUINOXALINE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.34.1 ASIA-PACIFIC

11.34.2 Северная Америка

11.34.3 Евро

11.34.4 Среднее Восток и Африка

11.34.5 Южная Америка

11.35 ASIA-PACIFIC 2-METHYLIMIDAZOLE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.35.1 ASIA-PACIFIC

11.35.2 Северная Америка

11.35.3 Евро

11.35.4 Среднее Восток и Африка

11.35.5 Южная Америка

11.36 ASIA-PACIFIC IMIDAZOLE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.36.1 ASIA-PACIFIC

11.36.2 Северная Америка

11.36.3 Евро

11.36.4 Среднее Восток и Африка

11.36.5 Южная Америка

11.37 ASIA-PACIFIC GLYCOLURIL IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.37.1 ASIA-PACIFIC

11.37.2 Северная Америка

11.37.3 Европа

11.37.4 Среднее Восток и Африка

11.37.5 Южная Америка

11.38 ASIA-PACIFIC ALLANTOIN IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.38.1 ASIA-PACIFIC

11.38.2 Северная Америка

11.38.3 Евро

11.38.4 Среднее Восток и Африка

11.38.5 Южная Америка

11.39 ASIA-PACIFIC TETRAMETHYLOL ACETYLENEDIUREA IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.39.1 ASIA-PACIFIC

11.39.2 Северная Америка

11.39.3 Евро

11.39.4 Среднее Восток и Африка

11.39.5 Южная Америка

12 ASIA-PACIFIC GLYOXAL MARKET

12.1 Проверка

12.2 Текс.

12.3 PULP и PAPER

12.4 Учитель

12,5 боли и покрытия

12.6 Водоснабжение

12.7 Фармацевтические

12.8 Производство домов

12.9 Косметика и личная забота

12.1 Упаковка

12.11 ЭЛЕКТРИКА И ЭЛЕКТРОНИКА

12.12 Нефть и газ

12.13 Другие

12.14 ASIA-PACIFIC TEXTILE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.14.1 ASIA-PACIFIC

12.14.2 Северная Америка

12.14.3 Евро

12.14.4 Среднее Восток и Африка

12.14.5 Южная Америка

12.15 ASIA-PACIFIC PULP and PAPER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.15.1 ASIA-PACIFIC

12.15.2 Северная Америка

12.15.3 Евро

12.15.4 Среднее Восток и Африка

12.15.5 Южная Америка

12.16 ASIA-PACIFIC LEATHER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.16.1 ASIA-PACIFIC

12.16.2 Северная Америка

12.16.3 Евро

12.16.4 Среднее Восток и Африка

12.16.5 Южная Америка

12.17 АСИА-ПАЦИФИЧЕСКИЕ ПАРИНЫ И КОТОРЫЕ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ПРИ РЕГИОНЕ, 2018-2033 (USD THOUSAND)

12.17.1 ASIA-PACIFIC

12.17.2 Северная Америка

12.17.3 Европа

12.17.4 Среднее Восток и Африка

12.17.5 Южная Америка

12.18 ASIA-PACIFIC WATER TREATMENT IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.18.1 ASIA-PACIFIC

12.18.2 Северная Америка

12.18.3 Евро

12.18.4 Среднее Восток и Африка

12.18.5 Южная Америка

12.19 АСИА-ПАЦИФИЧЕСКИЕ ФАРМАЦЕВТИКИ В ГЛИОКСАЛЬНОМ МАРКЕ, РЕГИОН, 2018-2033 (USD THOUSAND)

12.19.1 АСИА-ПАЦИФИК

12.19.2 Северная Америка

12.19.3 Европа

12.19.4 Средний Восток и Африка

12.19.5 Южная Америка

12.2 ASIA-PACIFIC HOUSEHOLD PRODUCTS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.20.1 ASIA-PACIFIC

12.20.2 Северная Америка

12.20.3 Европа

12.20.4 Средний Восток и Африка

12.20.5 Южная Америка

12.21 ASIA-PACIFIC COSMETICS and PERSONAL CARE IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

12.21.1 Лекции и крики

12.21.2 Перфумы и дезодоранты

12.21.3 Другие

12.22 ASIA-PACIFIC COSMETICS and PERSONAL CARE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.22.1 ASIA-PACIFIC

12.22.2 Северная Америка

12.22.3 Евро

12.22.4 Средний Восток и Африка

12.22.5 Южная Америка

12.23 АСИА-ПАЦИФИЧЕСКИЙ ПАККАГИНГ В ГЛИОКСАЛЬНОМ МАРКЕ, РЕГИОН, 2018-2033 (USD THOUSAND)

12.23.1 ASIA-PACIFIC

12.23.2 Северная Америка

12.23.3 Европа

12.23.4 Средний Восток и Африка

12.23.5 Южная Америка

12.24 ASIA-PACIFIC ELECTRICAL AND ELECTRONICS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.24.1 ASIA-PACIFIC

12.24.2 Северная Америка

12.24.3 Евро

12.24.4 Среднее Восток и Африка

12.24.5 Южная Америка

12.25 ASIA-PACIFIC OIL AND GAS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.25.1 ASIA-PACIFIC

12.25.2 Северная Америка

12.25.3 Евро

12.25.4 Среднее Восток и Африка

12.25.5 Южная Америка

12.26 АСИА-ПАЦИФИЧЕСКИЕ ДРУГИ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ПО РЕГИОНУ, 2018-2033 (USD THOUSAND)

12.26.1 ASIA-PACIFIC

12.26.2 Северная Америка

12.26.3 Евро

12.26.4 Среднее Восток и Африка

12.26.5 Южная Америка

13 ASIA-PACIFIC GLYOXAL MARKET, BY REGION

13.1 Азия Пацифик

13.1.1 Китай

13.1.2 ИНДИЯ

13.1.3 Япония

13.1.4 Южная Корея

13.1.5 Тайвань

13.1.6 Вьетнам

13.1.7 Индонезия

13.1.8 Таиланд

13.1.9 Австралия

13.1.10 Малайзия

13.1.11 СИНГАПУР

13.1.12 Филиппины

13.1.13 ПЕСТ АСИА-ПАЦИФИКА

14 ASIA-PACIFIC GLYOXAL MARKET, COMPANY LANDSCAPE

14.1 КОМПАНИЯ ДЛЯ АНАЛИЗА: ГЛОБАЛ

15 СВОТ АНАЛИЗ

16 КОМПАНИЯ ПРОФИЛЬНОЕ

16.1 BASF

16.1.1 КОМПАНИЯ СНАПШОТ

16.1.2 РЕВЕНУАЛЬНЫЙ АНАЛИЗ

16.1.3 ПРОДУКТ ПОРТФОЛИО

16.1.4 ПРОЕКТ РАЗВИТИЯ

16.2 МЕРКК КГАА

16.2.1 КОМПАНИЯ СНАПШОТ

16.2.2 РЕВЕННЫЙ АНАЛИЗ

16.2.3 ПРОДУКТ ПОРТФОЛИО

16.2.4 ПРОЕКТ РАЗВИТИЯ

16.3 НАУЧНЫЙ ИНЦ THERMO FISHER.

16.3.1 КОМПАНИЯ СНАПШОТ

16.3.2 РЕВЕННЫЙ АНАЛИЗ

16.3.3 ПРОДУКТ ПОРТФОЛИО

16.3.4 ПРОЕКТ РАЗВИТИЯ

16.4 МЕЖДУНАРОДНЫЙ ГМБХ ВЕЙЛХИМ

16.4.1 КОМПАНИЯ СНАПШОТ

16.4.2 ПРОДУКТ ПОРТФОЛИО

16.4.3 ПРОЕКТ РАЗВИТИЯ

16.5 Алфа Хемика.

16.5.1 КОМПАНИЯ СНАПШОТ

16.5.2 ПРОДУКТ ПОРТФОЛИО

16.5.3 ПРОЕКТ РАЗВИТИЯ

16.6 AMZOLE INDIA PVT. LTD

16.6.1 КОМПАНИЯ СНАПШОТ

16.6.2 ПРОДУКТ ПОРТФОЛИО

16.6.3 ПРОЕКТ РАЗВИТИЯ

16.7 EMCO DYESTUFF

16.7.1 КОМПАНИЯ СНАПШОТ

16.7.2 ПРОДУКТ ПОРТФОЛИО

16.7.3 ПРОЕКТ РАЗВИТИЯ

16.8 Ограничение флуорохимии

16.8.1 КОМПАНИЯ СНАПШОТ

16.8.2 ПРОДУКТ ПОРТФОЛИО

16.8.3 ПРОЕКТ РАЗВИТИЯ

16.9 FUJIFILM WAKO PURE CHEMICAL CORPORATION

16.9.1 КОМПАНИЯ СНАПШОТ

16.9.2 ПРОДУКТ ПОРТФОЛИО

16.9.3 ПРОЕКТ РАЗВИТИЯ

16.1 GETCHEM CO., LTD.

16.10.1 КОМПАНИЯ СНАПШОТ

16.10.2 ПРОДУКТ ПОРТФОЛИО

16.10.3 ПРОЕКТ РАЗВИТИЯ

16.11 ГЛЕНТАМ ОГРАНИЧЕННЫЕ НАУКИ ЖИЗНИ

16.11.1 КОМПАНИЯ СНАПШОТ

16.11.2 ПРОДУКТ ПОРТФОЛИО

16.11.3 ПРОЕКТ РАЗВИТИЯ

16.12 HANNA EQUIPMENTS (INDIA) PVT. ЛТД.

16.12.1 КОМПАНИЯ СНАПШОТ

16.12.2 ПРОДУКТ ПОРТФОЛИО

16.12.3 ПРОЕКТ РАЗВИТИЯ

16.13 HEZE RUNQUAN CHEMICAL CO., Ltd.

16.13.1 КОМПАНИЯ СНАПШОТ

16.13.2 ПРОДУКТ ПОРТФОЛИО

16.13.3 РАЗВИТИЕ ПРИЛОЖЕНИЯ

16.14 Химедия Лаборатории

16.14.1 КОМПАНИЯ СНАПШОТ

16.14.2 ПРОДУКТ ПОРТФОЛИО

16.14.3 ПРОЕКТ РАЗВИТИЯ

16.15 HUBEI SHUNHUI BIO-TECHNOLOGY CO., Ltd.

16.15.1 КОМПАНИЯ СНАПШОТ

16.15.2 ПРОДУКТ ПОРТФОЛИО

16.15.3 ПРОЕКТ РАЗВИТИЯ

16.16 Канто Кагаку

16.16.1 КОМПАНИЯ СНАПШОТ

16.16.2 ПРОДУКТ ПОРТФОЛИО

16.16.3 ПРОЕКТ РАЗВИТИЯ

16.17 КЕМИРА

16.17.1 КОМПАНИЯ СНАПШОТ

16.17.2 АНАЛИЗ РЕВЕНУА

16.17.3 ПРОДУКТ ПОРТФОЛИО

16.17.4 ПРОЕКТ РАЗВИТИЯ

16.18 LOBACHEMIE PVT. LTD.

16.18.1 КОМПАНИЯ СНАПШОТ

16.18.2 ПРОДУКТ ПОРТФОЛИО

16.18.3 ПРОЕКТ РАЗВИТИЯ

16.19 MERU CHEM PVT.LTD.

16.19.1 КОМПАНИЯ СНАПШОТ

16.19.2 ПРОДУКТ ПОРТФОЛИО

16.19.3 ПРОЕКТ РАЗВИТИЯ

16.2 МУЛТИХИМНЫЕ СПЕЦИАЛИТИКИ ОГРАНИЧЕННЫЕ

16.20.1 КОМПАНИЯ СНАПШОТ

16.20.2 ПРОДУКТ ПОРТФОЛИО

16.20.3 ПРОЕКТ РАЗВИТИЯ

16.21 OTTO CHEMIE PVT. LTD

16.21.1 КОМПАНИЯ СНАПШОТ

16.21.2 ПРОДУКТ ПОРТФОЛИО

16.21.3 ПРОЕКТ РАЗВИТИЯ

16.22 ТОО OXFORD LAB FINE CHEM.

16.22.1 КОМПАНИЯ СНАПШОТ

16.22.2 ПРОДУКТ ПОРТФОЛИО

16.22.3 ПРОЕКТ РАЗВИТИЯ

16.23 САНТА КРУЗ БИОТЕХНОЛОГИЯ ИНК.

16.23.1 КОМПАНИЯ СНАПШОТ

16.23.2 ПРОДУКТ ПОРТФОЛИО

16.23.3 РАЗВИТИЕ ПРИЛОЖЕНИЯ

16.24 SHANDONG ZHISHANG CHEMICAL CO.LTD,

16.24.1 КОМПАНИЯ СНАПШОТ

16.24.2 ПРОДУКТ ПОРТФОЛИО

16.24.3 ПРОЕКТ РАЗВИТИЯ

16.25 СИХАУЛЬСКИЕ ХИМИКАЛЫ ОГРАНИЧЕННЫ

16.25.1 КОМПАНИЯ СНАПШОТ

16.25.2 ПРОДУКТ ПОРТФОЛИО

16.25.3 ПРОЕКТ РАЗВИТИЯ

16.26 ООО "Сильвер Ферн Хемикал"

16.26.1 КОМПАНИЯ СНАПШОТ

16.26.2 ПРОДУКТ ПОРТФОЛИО

16.26.3 ПРОЕКТ РАЗВИТИЯ

16.27 Симсон Фарма ограничен

16.27.1 КОМПАНИЯ СНАПШОТ

16.27.2 ПРОДУКТ ПОРТФОЛИО

16.27.3 ПРОЕКТ РАЗВИТИЯ

16.28 TOKYO CHEMICAL INDUSTRY UK LTD.

16.28.1 КОМПАНИЯ СНАПШОТ

16.28.2 ПРОДУКТ ПОРТФОЛИО

16.28.3 ПРОЕКТ РАЗВИТИЯ

16.29 ООО УНИВАР РЕШЕНИЯ

16.29.1 КОМПАНИЯ СНАПШОТ

16.29.2 ПРОДУКТ ПОРТФОЛИО

16.29.3 ПРОЕКТ РАЗВИТИЯ

16.3 WUXI LANSEN CHEMICALS CO., LTD.

16.30.1 КОМПАНИЯ СНАПШОТ

16.30.2 ПРОДУКТ ПОРТФОЛИО

16.30.3 ПРОЕКТ РАЗВИТИЯ

17 Вопросник

18 Связанные поправки

Список таблиц

СТАТЬЯ 1 ОСНОВНЫЙ ИСПОЛЬЗОВАНИЕ ПРОДУКТОВ ДЛЯ ГЛИОКСАЛА

Таблица 2 ASIA-PACIFIC GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND)

Таблица 3 ASIA-PACIFIC GLYOXAL MARKET, BY GRADE, 2018-2033

СТАТЬЯ 4 АСИА-ПАЦИФИЧЕСКАЯ ИНДУСТРИАЛЬНАЯ ГРАДА В ГЛИОКСАЛЬНОМ МАРКЕ, РЕГИОН, 2018-2033 (USD THOUSAND)

Таблица 5 ASIA-PACIFIC PHARMACEUTICAL GRADE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

Таблица 6 ASIA-PACIFIC GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

СТАТЬЯ 7 АСИА-ПАЦИФИЧЕСКИЕ 40%-60% В ГЛИОКСАЛЬНОМ РЫНКЕ, ПО РЕГИОНУ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 8 АСИА-ПАЦИФИКА 90%-99% В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ПО РЕГИОНУ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 9 АСИА-ПАЦИФИЧЕСКИЕ ДРУГИ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ПО РЕГИОНУ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 10 ASIA-PACIFIC GLYOXAL MARKET, BY PRODUCTION PROCESS, 2018-2033 (USD THOUSAND)

СТАТЬЯ 11 АСИА-ПАЦИФИЧЕСКАЯ КАТАЛИТИЧЕСКАЯ ОКСИДАЦИЯ ЭТИЛЕННОГО ГЛИКОЛЯ В ГЛИОКСАЛЬНОМ МАРКЕ, ПРИ РЕГИОНЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 12 АСИА-ПАЦИФИЧЕСКОЕ ОКСИДОВАНИЕ АЦЕТИЛЕНА В ГЛИОКСАЛЬНОМ МАРКЕ, ПРИ РЕГИОНЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 13 АСИА-ПАЦИФИЧЕСКИЕ ДРУГИЕ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ПО РЕГИОНУ, 2018-2033 (USD THOUSAND)

Таблица 14 ASIA-PACIFIC GLYOXAL MARKET, BY PACKAGING, 2018-2033 (USD THOUSAND)

СТАТЬЯ 15 АСИА-ПАЦИФИЧЕСКИХ ПРАВИЛ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 16 АСИА-ПАЦИФИЧЕСКИЕ ПРАВИЛА В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ПРИ РЕГИОНЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 17 ASIA-PACIFIC COMPOSITE IBC IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

СТАТЬЯ 18 ASIA-PACIFIC COMPOSITE IBC IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

Таблица 19 ASIA-PACIFIC BULK IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

СТАТЬЯ 20 АСИА-ПАЦИФИЧЕСКИХ ИЕРРИКАНСОВ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 21 АСИА-ПАЦИФИЧЕСКИЕ ИЕРРИКАНСЫ В ГЛИОКСАЛЬНОМ МАРКЕ, ПО РЕГИОНУ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 22 АСИА-ПАЦИФИЧЕСКИЕ БОТТЛЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 23 АСИА-ПАЦИФИЧЕСКИЕ БОТТЛЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ПО РЕГИОНУ, 2018-2033 (USD THOUSAND)

Таблица 24 ASIA-PACIFIC GLYOXAL MARKET, ПРИМЕЧАНИЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 25 АСИА-ПАЦИФИЧЕСКИЙ КРОСС-ЛИНКИНГ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 26 АСИА-ПАЦИФИЧЕСКИЙ КРОСС-ЛИНКИНГ В ГЛИОКСАЛЬНОМ МАРКЕ, ПО РЕГИОНУ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 27 ASIA-PACIFIC CHEMICAL INTERMEDIATES, IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

СТАТЬЯ 28 ASIA-PACIFIC BULK CHEMICALS MANUFACTURING IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

СТАТЬЯ 29 АСИА-ПАЦИФИЧЕСКИЙ ПОЛИМЕР, ОБРАЩАЮЩИЙСЯ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

Таблица 30 ASIA-PACIFIC CHEMICAL INTERMEDIATES IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

СТАТЬЯ 31 АСИА-ПАЦИФИЧЕСКИЕ ДРУГИЕ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 32 АСИА-ПАЦИФИЧЕСКИЕ ДРУГИ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ПРИ РЕГИОНЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 33 ASIA-PACIFIC GLYOXAL MARKET, BY END-USE CHEMICALS, 2018-2033 (USD THOUSAND)

Таблица 34 ASIA-PACIFIC DIHYDROXYETHYLENE UREA (DHEU) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

СТАТЬЯ 35 АСИА-ПАЦИФИЧЕСКИЙ 2-ИМИДАЗОЛИДИНОН В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ПО РЕГИОНУ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 36 ASIA-PACIFIC GLYOXALATED POLYACRYLAMIDE (GPAM) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

Таблица 37 ASIA-PACIFIC GLYOXYLIC ACID IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

СТАТЬЯ 38 ASIA-PACIFIC GLYOXALATED STARCH IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

Таблица 39 ASIA-PACIFIC GLYOXAL PHENOL RESIN IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

Таблица 40 ASIA-PACIFIC GLYOXAL UREA RESIN IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

СТАТЬЯ 41 АСИА-ПАЦИФИЧЕСКАЯ ЭТИЛЕННАЯ ГЛИКОЛЬНАЯ ДИФОРМАЦИЯ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ПРИ РЕГИОНЕ, 2018-2033 (USD THOUSAND)

Таблица 42 ASIA-PACIFIC UREA-GLYOXAL CONCENTRATE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

СТАТЬЯ 43 АСИА-ПАЦИФИЧЕСКИЕ КВИНОКСАЛИНЫ ДЕРИВАТИВЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ПРИ РЕГИОНЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 44 ASIA-PACIFIC METHYLOL GLYOXAL IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

Таблица 45 ASIA-PACIFIC GLYOXAL-BIS(2-HYDROXYANIL) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

Таблица 46 ASIA-PACIFIC GLYOXAL SODIUM BISULFITE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

СТАТЬЯ 47 ASIA-PACIFIC QUINOXALINE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

Таблица 48 ASIA-PACIFIC 2-METHYLIMIDAZOLE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

СТАТЬЯ 49 АСИА-ПАЦИФИЧЕСКАЯ ИМИДАЗОЛЬ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, РЕГИОН, 2018-2033 (USD THOUSAND)

Таблица 50 ASIA-PACIFIC GLYCOLURIL IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

СТАТЬЯ 51 АСИА-ПАЦИФИЧЕСКИЙ АЛЛАНТОИН В ГЛИОКСАЛЬСКОМ МАРКЕТЕ, ПРИ РЕГИОНЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 52 АСИА-ПАЦИФИЧЕСКАЯ ТЕТРАМЕТИЛОЛЬНАЯ АЦЕТИЛЕНЕДИУРА В ГЛИОКСАЛЬНОМ МАРКЕ, ПРИ РЕГИОНЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 53 ASIA-PACIFIC GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

СТАТЬЯ 54 ASIA-PACIFIC TEXTILE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

Таблица 55 ASIA-PACIFIC PULP and PAPER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

СТАТЬЯ 56 ASIA-PACIFIC LEATHER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

СТАТЬЯ 57 АСИА-ПАЦИФИЧЕСКИЕ ПАИНТЫ И КОТОРЫЕ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, РЕГИОН, 2018-2033 (USD THOUSAND)

СТАТЬЯ 58 ASIA-PACIFIC WATER TREATMENT IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

СТАТЬЯ 59 АСИА-ПАЦИФИЧЕСКИЕ ФАРМАЦЕВТИКИ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ПО РЕГИОНУ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 60 ПРОДУКТЫ АСИА-ПАЦИФИЧЕСКИХ ДОМОВ В ГЛИОКСАЛЬНОМ МАРКЕ, ПРИ РЕГИОНЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 61 ASIA-PACIFIC COSMETICS and PERSONAL CARE IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

СТАТЬЯ 62 ASIA-PACIFIC COSMETICS and PERSONAL CARE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

СТАТЬЯ 63 АСИА-ПАЦИФИЧЕСКИЙ ПАККАГИНГ В ГЛИОКСАЛЬНОМ МАРКЕ, ПРИ РЕГИОНЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 64 АСИА-ПАЦИФИЧЕСКАЯ ЭЛЕКТРИКА И ЭЛЕКТРОНИКА В ГЛИОКСАЛЬНОМ МАРКЕ, РЕГИОН, 2018-2033 (USD THOUSAND)

СТАТЬЯ 65 АСИА-ПАЦИФИЧЕСКОЕ НЕФТЬ И ГАЗ В ГЛИОКСАЛЬНОМ МАРКЕ, ПРИ РЕГИОНЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 66 АСИА-ПАЦИФИЧЕСКИЕ ДРУГИЕ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ПО РЕГИОНУ, 2018-2033 (USD THOUSAND)

Таблица 67 ASIA-PACIFIC GLYOXAL MARKET, BY COUNTRY, 2018-2033 (USD THOUSAND)

СТАТЬЯ 68 ASIA-PACIFIC GLYOXAL MARKET, BY COUNTRY, 2018-2033

СТАТЬЯ 69 USD TUSAND

Таблица 70 ASIA-PACIFIC GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND)

Таблица 71 ASIA-PACIFIC GLYOXAL MARKET, BY GRADE, 2018-2033

Таблица 72 ASIA-PACIFIC GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

СТАТЬЯ 73 ASIA-PACIFIC GLYOXAL MARKET, BY PRODUCTION PROCESS, 2018-2033 (USD THOUSAND)

Таблица 74 ASIA-PACIFIC GLYOXAL MARKET, BY PACKAGING, 2018-2033 (USD THOUSAND)

СТАТЬЯ 75 АСИА-ПАЦИФИЧЕСКИЕ ПРАВИЛА В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 76 ASIA-PACIFIC COMPOSITE IBC IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

СТАТЬЯ 77 АСИА-ПАЦИФИЧЕСКИЕ ИЕРРИКАНСЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 78 АСИА-ПАЦИФИЧЕСКИХ БОТТЛЕЙ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

Таблица 79 ASIA-PACIFIC GLYOXAL MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

СТАТЬЯ 80 АСИА-ПАЦИФИЧЕСКИЙ КРОСС-ЛИНКИНГ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 81 ASIA-PACIFIC CHEMICAL INTERMEDIATES, IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

СТАТЬЯ 82 ASIA-PACIFIC BULK CHEMICALS MANUFACTURING IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

СТАТЬЯ 83 АСИА-ПАЦИФИЧЕСКИЙ ПОЛИМЕР, ОБРАЩАЮЩИЙСЯ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 84 АСИА-ПАЦИФИЧЕСКИЕ ДРУГИЕ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 85 ASIA-PACIFIC GLYOXAL MARKET, BY END-USE CHEMICALS, 2018-2033 (USD THOUSAND)

Таблица 86 ASIA-PACIFIC GLYOXAL MARKET, К концу использования, 2018-2033 (USD THOUSAND)

СТАТЬЯ 87 ASIA-PACIFIC COSMETICS and PERSONAL CARE IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

Таблица 88 Китайский Глиоксальский Маркет, КРАЙДЫ, 2018-2033 (USD THOUSAND)

89 CHINA GLYOXAL MARKET, BY GRADE, 2018-2033

Таблица 90 Китайский Глиоксальский Маркет, Чистота, 2018-2033 (USD THOUSAND)

СТАТЬЯ 91 Китайский ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПРОДУКЦИОННЫЙ ПРОЦЕСС, 2018-2033 (USD THOUSAND)

СТАТЬЯ 92 ЧИНА ГЛИОКСАЛ МАРКЕТ, ПАККАГИНГ, 2018-2033 (USD THOUSAND)

Таблица 93 Китайские драмы в ГЛЫОКСАЛЬНЫЙ МАРКЕТ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 94 КИТАЙСКИЙ КОМПОСИТЕТ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, СТАТЬЯ, 2018-2033 (USD THOUSAND)

Таблица 95 Китайские Джерриканы в Глиоксальном Маркете, Тип, 2018-2033 (USD THOUSAND)

СТАТЬЯ 96 КИТАЙСКИЕ БОТТЛЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

Таблица 97 Китайский Глиоксальский Маркет, ПРИМЕЧАНИЕ, 2018-2033 (USD THOUSAND)

TABLE 98 CHINA CROSS-LINKING IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

СТАТЬЯ 99 Китайские химические интермедии, в ГЛЫОКСАЛЬНОМ РЫНКЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

Таблица 100 КИТАЙСКИЕ БОЛЬНЫЕ ХИМИЧЕСКИЕ МАНИФАКТУРЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ТИП, 2018-2033 (USD THOUSAND)

СТАТЬЯ 101 ПОЛИМЕР КИТАЯ ПРОЦЕССИЯ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИП, 2018-2033 (USD THOUSAND)

СТАТЬЯ 102 ДРУГИЕ ЧИНЫ В ГЛИОКСАЛЬНОМ МАРЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

Таблица 103 Китайский ГЛЁКСАЛЬНЫЙ МАРКЕТ, КОНЕЧНЫЕ ИСПОЛЬЗОВАНИЯ, 2018-2033 (USD THOUSAND)

TABLE 104 CHINA GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

СТАТЬЯ 105 КОСМЕТИКА КИТАЯ И ПЕРСОНАЛЬНАЯ КАРТА В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 106 ИНДИЯ ГЛЫОКСАЛЬНЫЙ МАРКЕТ, К ГРАДЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 107 ИНДИЯ ГЛЫОКСАЛЬНЫЙ МАРКЕТ, К ГРАДУ, 2018-2033 (ТЫСЯЧ ТОНС)

СТАТЬЯ 108 ИНДИЯ ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПО БЕСПЛАТНОСТИ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 109 ИНДИЯ ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПРОДУКЦИОННЫЙ ПРОЦЕСС, 2018-2033 (USD THOUSAND)

Таблица 110 ИНДИЯ ГЛИОКСАЛЬНЫЙ МАРКЕТ, ПАККАГИНГ, 2018-2033 (USD THOUSAND)

Таблица 111 Индийские драмы в ГЛЁКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

Таблица 112 INDIA COMPOSITE IBC in GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

Таблица 113 Индия Джерриканс в Глиоксаль Маркет, Тип, 2018-2033 (USD THOUSAND)

Таблица 114 «Индия Боттлз» в ГЛЁКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 115 ИНДИЯ ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПРИМЕЧАНИЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 116 ИНДИЯ КРОСС-ЛИНКИНГ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 117 ИНДИЙСКИЕ ХИМИЧЕСКИЕ ИНТЕРМЕДИАЦИИ, В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 118 ИНДИЯ БОЛК ХИМИЧЕСКИЕ ПРОИЗВОДИТЕЛЬСТВА В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 119 ИНДИЙСКИЙ ПОЛИМЕР, ПРОЦЕССИРОВАННЫЙ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 120 ДРУГИХ ИНДИЙ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 121 ИНДИЯ ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПО КОНЕЧНОМУ ИСПОЛЬЗОВАНИЮ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 122 ИНДИЯ ГЛЁКСАЛЬНЫЙ МАРКЕТ, К концу использования, 2018-2033 (USD THOUSAND)

СТАТЬЯ 123 ИНДИЙСКИЕ КОСМЕТИКИ И ПЕРСОНАЛЬНЫЙ КАРТ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

Таблица 124 Японский ГЛЁКСАЛЬНЫЙ МАРКЕТ, К ГРАДЕ, 2018-2033 (USD THOUSAND)

Таблица 125 Японский ГЛЁКСАЛЬНЫЙ МАРКЕТ, КРАЙДЫ, 2018-2033 (Тысяча тонн)

Таблица 126 Японский ГЛЁКСАЛЬНЫЙ МАРКЕТ, Клянусь ЧЕСТЬЮ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 127 ЯПОНСКИЙ ГЛИОКСАЛЬНЫЙ МАРКЕТ, ПРОДУКЦИОННЫЙ ПРОЦЕСС, 2018-2033 (USD THOUSAND)

Таблица 128 Японский ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПАККАГИНГ, 2018-2033 (USD THOUSAND)

Таблица 129 японские драмы в глиоксальском рынке, по типу, 2018-2033 (USD THOUSAND)

Таблица 130 Японский Композитный КСГМГ в ГЛЮКСАЛЬНОМ МАРКЕ, КИП, 2018-2033 (USD THOUSAND)

СТАТЬЯ 131 ЯПОНСКИЕ ИЕРРИКАНСЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

Таблица 132 Японские Боттлы в Глиоксал Маркет, Тип, 2018-2033 (USD THOUSAND)

Таблица 133 Японский ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПРИМЕЧАНИЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 134 ЯПОНСКИЙ КРОСС-ЛИНКИНГ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 135 Японские химические интермедии, в ГЛЫОКСАЛЬНЫЙ МАРКЕТ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 136 ЯПОНСКИЕ БОЛЬКОВЫЕ ХИМИЧЕСКИЕ ПРОИЗВОДИТЕЛЬСТВА В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 137 ЯПОНСКИЙ ПОЛИМЕР, ПРОЦЕССИРОВАННЫЙ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 138 ДРУГИХ ЯПОНИЙ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

Таблица 139 Японский ГЛЁКСАЛЬНЫЙ МАРКЕТ, КОНЕЧНО-ИМЕНИЙСКИЙ, 2018-2033 (USD THOUSAND)

TABLE 140 JAPAN GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

СТАТЬЯ 141 Японская косметика и личная забота в ГЛИОКСАЛЬНОМ РЫНКЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

Таблица 142 Южная Корея ГЛЁКСАЛЬНЫЙ МАРКЕТ, КРАЙД, 2018-2033 (USD THOUSAND)

Таблица 143 Южная Корея ГЛЁКСАЛЬНЫЙ МАРКЕТ, КРАЙД, 2018-2033 (ТЫСЯЧ ТОНС)

Таблица 144 Южная Корея ГЛЁКСАЛЬНЫЙ МАРКЕТ, БЕСЧЕТНОСТЬ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 145 ЮЖНАЯ КОРЕЯ ГЛИОКСАЛЬНЫЙ МАРКЕТ, ПРОДУКЦИОННЫЙ ПРОЦЕСС, 2018-2033 (USD THOUSAND)

Таблица 146 Южная Корея ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПАККАГИНГ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 147 ПРАВЫ ЮЖНОЙ КОРЕИ В ГЛЫОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 148 ЮЖНАЯ КОРЕЙСКАЯ КОМПОЦИЯ МКБ В ГЛИОКСАЛЬНОМ МАРКЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 149 ЮЖНАЯ КОРЕЯ ЖЕРРИКАНС В ГЛЫОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

Таблица 150 южно-корейских бутылок в Глиоксальском Маркете, Тип, 2018-2033 (USD THOUSAND)

Таблица 151 Южная Корея ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПРИМЕЧАНИЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 152 ЮЖНАЯ КОРЕЙСКАЯ КРОССКАЯ КРОССКАЯ В ГЛЫОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 153 Южнокорейские химические интермедии, в ГЛЫОКСАЛЬНОМ РЫНКЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 154 ЮЖНАЯ КОРЕА БОЛК ЧЕМИКАЛЬНЫЕ МАНИФАКТУРЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 155 ПОЛИМЕР ЮЖНОЙ КОРЕИ, ПРОЦЕССИРОВАННЫЙ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 156 ЮЖНАЯ КОРЕА ДРУГИЕ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 157 ЮЖНАЯ КОРЕЯ ГЛЁКСАЛЬНЫЙ МАРКЕТ, КОНЦ-УСЛЕДОВАТЕЛЬСТВА, 2018-2033 (USD THOUSAND)

Таблица 158 Южная Корея ГЛЁКСАЛЬНАЯ МАРКЕТ, К концу использования, 2018-2033 (USD THOUSAND)

СТАТЬЯ 159 ЮЖНАЯ КОРЕА КОСМЕТИКА И ПЕРСОНАЛЬНАЯ КАРТА В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИП, 2018-2033 (USD THOUSAND)

Таблица 160 TAIWAN GLYOXAL MARKET, КРАЙДЫ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 161 ТАЙВАН ГЛЁКСАЛЬНЫЙ МАРКЕТ, КОЛУМБИЯ, 2018-2033 (Тысяча тонн)

СТАТЬЯ 162 ТАЙВАН ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПО БЕСПЛАТНОСТИ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 163 ТАЙВАН ГЛИОКСАЛ МАРКЕТ, ПРОДУКЦИОННЫЙ ПРОЦЕСС, 2018-2033 (USD THOUSAND)

СТАТЬЯ 164 ТАЙВАН ГЛИОКСАЛ МАРКЕТ, ПАККАГИНГ, 2018-2033 (USD THOUSAND)

Таблица 165 таиванских драмов в ГЛЫОКСАЛЬНОМ МАРКЕТЕ, ТИП, 2018-2033 (USD THOUSAND)

СТАТЬЯ 166 ТАЙВАНСКИЙ КОМПОСИТЕТ МКБ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 167 ТАЙВАН ДЖЕРРИКАНС В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 168 ТАЙВАНСКИХ БОТТЛЕЙ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 169 ТАЙВАН ГЛИОКСАЛ МАРКЕТ, ПРИМЕЧАНИЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 170 ТАЙВАНСКИЙ КРОСС-ЛИНКИНГ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 171 ТАЙВАНСКИЕ ХИМИЧЕСКИЕ ИНТЕРМЕДИАЦИИ, В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 172 ТАЙВАН БОЛК ЧЕМИКАЛЬНЫЕ МАНИФАКТУРЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ТИП, 2018-2033 (USD THOUSAND)

СТАТЬЯ 173 ТАЙВАНСКИЙ ПОЛИМЕР, ПРОЦЕССИРОВАННЫЙ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 174 ТАЙВАН ДРУГИЕ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 175 ТАЙВАН ГЛЁКСАЛЬНЫЙ МАРКЕТ, КОНЕЧНЫЕ ИСПОЛЬЗОВАНИЯ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 176 ТАЙВАН ГЛИОКСАЛ МАРКЕТ, К концу использования, 2018-2033 (USD THOUSAND)

СТАТЬЯ 177 ТАЙВАНСКИЕ КОСМЕТИКИ И ПЕРСОНАЛЬНАЯ ОХРАНА В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 178 Вьетнамский ГЛЁКСАЛЬНЫЙ МАРКЕТ, К ГРАДЕ, 2018-2033 (USD THOUSAND)

Таблица 179 Вьетнамский ГЛЁКСАЛЬНЫЙ МАРКЕТ, К ГРАДЕ, 2018-2033 (Тысяча тонн)

Таблица 180 Вьетнамский Глиоксальский Маркет, Чистота, 2018-2033 (USD THOUSAND)

СТАТЬЯ 181 ВЕТНАМ ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПРОДУКЦИОННЫЙ ПРОЦЕСС, 2018-2033 (USD THOUSAND)

Таблица 182 Вьетнамский Глиоксальский Маркет, ПАККАГИНГ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 183 ВЕТНАМНЫЕ ДРУМЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 184 ВЕТНАМОВЫЙ КОМПОЗИТЕЛЬ МКБ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, СТАТЬЯ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 185 ВЕТНАМОВЫХ ИЕРРИКАНСОВ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 186 ВЕТНАМНЫЕ БОТТЛЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

Таблица 187 Вьетнамский ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПРИМЕЧАНИЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 188 ВЕТНАМОВЫЙ КРОССКИЙ ЛИНКИНГ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 189 VIETNAM CHEMICAL INTERMEDIATES, IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

СТАТЬЯ 190 ВЕТНАМНЫЕ КОММУНИКАЛЬНЫЕ КОММУНИКАЛЬНЫЕ ПРОДУКТИВЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 191 ВЕТНАМНЫЙ ПОЛИМЕР, ПРОЦЕССИРОВАННЫЙ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, СТАТЬЯ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 192 ВЕТНАМОВЫЕ ДРУГИЕ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 193 ВЕТНАМНЫЙ ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПО КОНЕЧНОМУ ИСПОЛЬЗОВАНИЮ, 2018-2033 (USD THOUSAND)

Таблица 194 Вьетнамский ГЛЁКСАЛЬНЫЙ МАРКЕТ, К концу использования, 2018-2033 (USD THOUSAND)

СТАТЬЯ 195 ВЕТНАМОВЫЕ КОСМЕТИКИ И ПЕРСОНАЛЬНАЯ КАРТИВА В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 196 ИНДОНЕССИЯ ГЛЁКСАЛЬНЫЙ МАРКЕТ, К ГРАДЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 197 ИНДОНЕССИЙСКИЙ ГЛЁКСАЛЬНЫЙ МАРКЕТ, К ГРАДЕ, 2018-2033 (ТЫСЯЧ ТОНС)

СТАТЬЯ 198 ИНДОНЕССИЙСКИЙ ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПО БЕСПЛАТНОСТИ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 199 ИНДОНЕССИЙСКИЙ ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПРОДУКЦИОННЫЙ ПРОЦЕСС, 2018-2033 (USD THOUSAND)

Таблица 200 ИНДОНЕССИЯ ГЛИОКСАЛЬНЫЙ МАРКЕТ, ПАККАГИНГ, 2018-2033 (USD THOUSAND)

Таблица 201 ИНДОНЕССИЙСКИЕ ПРАВИЛА В ГЛЫОКСАЛЬНОМ МАРЕ, ТИП, 2018-2033 (USD THOUSAND)

Таблица 202 INDONESIA COMPOSITE IBC in GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

Таблица 203 ИНДОНЕССИЙСКИЕ ЖЕРРИКАНСЫ В ГЛИОКСАЛЬСКОМ МАРКЕТЕ, КИП, 2018-2033 (USD THOUSAND)

Таблица 204 ИНДОНЕССИЙСКИЕ БОТТЛЫ В ГЛЫОКСАЛЬНОМ МАРКЕТЕ, ТИП, 2018-2033 (USD THOUSAND)

СТАТЬЯ 205 ИНДОНЕССИЙСКИЙ ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПРИМЕЧАНИЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 206 ИНДОНЕССИЙСКИЙ КРОССИНГ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

Таблица 207 Индонезийские химические интермедии, в ГЛЫОКСАЛЬНОМ РЫНКЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 208 ИНСДОНЕССИЙСКИЕ БОЛЬНЫЕ ХИМИЧЕСКИЕ МАНИФАКТУРЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

Таблица 209 ИНДОНЕССИЙСКИЙ ПОЛИМЕР, ОБРАЩАЮЩИЙСЯ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ТИП, 2018-2033 (USD THOUSAND)

СТАТЬЯ 210 ИНДОНЕСИЯ ДРУГИХ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 211 ИНДОНЕСИЯ ГЛЁКСАЛЬНЫЙ МАРКЕТ, КОНЦЕМНЫЕ ХИМИКАЛЫ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 212 ИНДОНЕССИЙСКИЙ ГЛЁКСАЛЬНЫЙ МАРКЕТ, К концу использования, 2018-2033 (USD THOUSAND)

СТАТЬЯ 213 ИНДОНЕССИЙСКИЕ КОСМЕТИКИ И ПЕРСОНАЛЬНАЯ КАРТИВА В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 214 ТАЙЛАНД ГЛИОКСАЛЬНЫЙ МАРКЕТ, К ГРАДЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 215 ТАЙЛАНД ГЛИОКСАЛЬНЫЙ МАРКЕТ, К ГРАДЕ, 2018-2033 (ТЫСЯЧ ТОНС)

СТАТЬЯ 216 ТАЙЛАНД ГЛИОКСАЛЬНЫЙ МАРКЕТ, ПО БЕСПЛАТНОСТИ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 217 ТАЙЛАНД ГЛИОКСАЛ МАРКЕТ, ПРОДУКЦИОННЫЙ ПРОЦЕСС, 2018-2033 (USD THOUSAND)

СТАТЬЯ 218 ТАЙЛАНД ГЛИОКСАЛ МАРКЕТ, ПАККАГИНГ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 219 ТАЙЛАНДСКИХ ДРУМОВ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 220 ТАЙЛАНДСКИЙ КОМПОЗИТНЫЙ КСГМГ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 221 ТАЙЛАНД ДЖЕРРИКАНС В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 222 ТАЙЛАНДСКИЕ БОТТЛЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 223 ТАЙЛАНД ГЛИОКСАЛ МАРКЕТ, ПРИМЕЧАНИЕ, 2018-2033 (USD THOUSAND)

224 THAILAND CROSS-LINKING IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

СТАТЬЯ 225 ТАЙЛАНДСКИЕ ХИМИЧЕСКИЕ ИНТЕРМЕДИАЦИИ, В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 226 ТАЙЛАНДСКИЕ КОММУНИКАЛЬНЫЕ КОММУНИКАЛЬНЫЕ КОММУНИКАЛЬНЫЕ КОММУНИКАЛЬНЫЕ КОММУНИКАЛЬНЫЕ ПРОИЗВОДЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 227 ТАЙЛАНДСКИЙ ПОЛИМЕР, ПРОЦЕССИРОВАННЫЙ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 228 ТАЙЛАНД ДРУГИХ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 229 ТАЙЛАНДСКИЙ ГЛИОКСАЛЬНЫЙ МАРКЕТ, КОНЕЧНЫЕ ИСПОЛЬЗОВАНИЯ, 2018-2033 (USD THOUSAND)

TABLE 230 THAILAND GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

СТАТЬЯ 231 ТАЙЛАНДСКИЕ КОСМЕТИКИ И ПЕРСОНАЛЬНАЯ КАРТНА В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 232 АВСТРАЛИЙСКИЙ ГЛЁКСАЛЬНЫЙ МАРКЕТ, К ГРАДЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 233 АВСТРАЛИЙСКИЙ ГЛЁКСАЛЬНЫЙ МАРКЕТ, КРАЙД, 2018-2033 (ТЫСЯЧ ТОНС)

СТАТЬЯ 234 АВСТРАЛИЙСКИЙ ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПО БЕСПЛАТНОСТИ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 235 АВСТРАЛИЙСКИЙ ГЛИОКСАЛЬНЫЙ МАРКЕТ, ПО ПРОДУКЦИОННОМУ ПРОЦЕССУ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 236 АВСТРАЛИЙСКИЙ ГЛИОКСАЛЬНЫЙ МАРКЕТ, ПАККАГИНГ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 237 АВСТРАЛИЙСКИЕ ДРУМЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 238 АВСТРАЛИЙСКИЙ КОМПОЗИТНЫЙ МКБ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, СТАТЬЯ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 239 АВСТРАЛИЙСКИЕ ЙЕРРИКАНСЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 240 АВСТРАЛИЙСКИХ БОТТЛЕЙ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 241 АВСТРАЛИЙСКИЙ ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПРИМЕЧАНИЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 242 АВСТРАЛИЙСКИЙ КРОСС-ЛИНКИНГ В ГЛИОКСАЛЬСКОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 243 АВСТРАЛИЙСКИЕ ХИМИЧЕСКИЕ ИНТЕРМЕДИАТЕЛЬСТВА, В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 244 АВСТРАЛИЙСКИЕ БОЛЬКИЕ ХИМИЧЕСКИЕ ПРОИЗВОДСТВА В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 245 АВСТРАЛИЙСКИЙ ПОЛИМЕР, ПРОЦЕССИРОВАННЫЙ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 246 ДРУГИЕ АВСТРАЛИИ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 247 АВСТРАЛИЙСКИЙ ГЛЁКСАЛЬНЫЙ МАРКЕТ, ПО КОНЕЧНОМУ ИСПОЛЬЗОВАНИЮ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 248 АВСТРАЛИЙСКИЙ ГЛЁКСАЛЬНЫЙ МАРКЕТ, К концу использования, 2018-2033 (USD THOUSAND)

СТАТЬЯ 249 АВСТРАЛИЙСКИЕ КОСМЕТИКИ И ПЕРСОНАЛЬНАЯ ОХРАНА В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

250 MALAYSIA GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND)

Таблица 251 MALAYSIA GLYOXAL MARKET, BY GRADE, 2018-2033

СТАТЬЯ 252 MALAYSIA GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

СТАТЬЯ 253 MALAYSIA GLYOXAL MARKET, ПО ПРОДУКЦИОННОМУ ПРОЦЕССУ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 254 MALAYSIA GLYOXAL MARKET, ПАККАГИНГ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 255 МАЛАЙСИЙСКИХ РУКОВОДОВ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, СТАТЬЯ, 2018-2033 (USD THOUSAND)

Таблица 256 MALAYSIA COMPOSITE IBC in GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

Таблица 257 Малайзия Джерриканс в Глиоксал Маркет, Тип, 2018-2033 (USD THOUSAND)

СТАТЬЯ 258 МАЛАЙСИЙСКИХ БОТТЛЕЙ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

Таблица 259 MALAYSIA GLYOXAL MARKET, ПРИМЕЧАНИЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 260 МАЛАЙСИЯ КРОСС-ЛИНКИНГ В ГЛИОКСАЛЬСКОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 261 MALAYSIA CHEMICAL INTERMEDIATES, IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

СТАТЬЯ 262 MALAYSIA BULK CHEMICALS MANUFACTURING IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

СТАТЬЯ 263 ПОЛИМЕР МАЛАЙСИЙСКОЙ ПРОЦЕССИИ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ТИП, 2018-2033 (USD THOUSAND)

СТАТЬЯ 264 MALAYSIA OTHERS IN GLYOXAL MARKET, BYPE, 2018-2033 (USD THOUSAND)

СТАТЬЯ 265 MALAYSIA GLYOXAL MARKET, BY END-USE CHEMICALS, 2018-2033 (USD THOUSAND)

СТАТЬЯ 266 MALAYSIA GLYOXAL MARKET, К концу использования, 2018-2033 (USD THOUSAND)

СТАТЬЯ 267 МАЛАЙСИЙСКИЕ КОСМЕТИКИ И ПЕРСОНАЛЬНАЯ ОХРАНА В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

Таблица 268 SINGAPORE GLYOXAL MARKET, КРАЙДЫ, 2018-2033 (USD THOUSAND)

Таблица 269 СИНГАПУР ГЛИОКСАЛЬНЫЙ МАРКЕТ, К ГРАДЕ, 2018-2033 (Тысяча тонн)

Таблица 270 SINGAPORE GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

СТАТЬЯ 271 СИНГАПУР ГЛИОКСАЛЬНЫЙ МАРКЕТ, ПРОДУКЦИОННЫЙ ПРОЦЕСС, 2018-2033 (USD THOUSAND)

Таблица 272 СИНГАПУР ГЛИОКСАЛ МАРКЕТ, ПАККАГИНГ, 2018-2033 (USD THOUSAND)

Таблица 273 СИНГАПУРНЫЕ ДРУМЫ В ГЛЫОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 274 СИНГАПУРНЫЙ КОМПОЗИТНЫЙ МКБ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

Таблица 275 СИНГАПУР ДЖЕРРИКАНС В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

Таблица 276 СИНГАПУРНЫХ БОТТЛЕЙ В ГЛЫОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

Таблица 277 СИНГАПУР ГЛИОКСАЛЬНЫЙ МАРКЕТ, ПРИМЕЧАНИЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 278 СИНГАПУРНЫЙ КРОСС-ЛИНКИНГ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

СТАТЬЯ 279 СИНГАПУРНЫЕ ХИМИЧЕСКИЕ ИНТЕРМЕДИАТЕЛЬСТВА, В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 280 СИНГАПУРНЫЕ КОММЕНТАРИЙНЫЕ ХИМИЧЕСКИЕ ПРОДУКТИВЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 281 СИНГАПУРНЫЙ ПОЛИМЕР, ПРОЦЕССИРОВАННЫЙ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 282 СИНГАПУРЫ ДРУГИХ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 283 СИНГАПУР ГЛИОКСАЛЬНЫЙ МАРКЕТ, ПО КОНЕЧНОМУ ИСПОЛЬЗОВАНИЮ, 2018-2033 (USD THOUSAND)

TABLE 284 SINGAPORE GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

СТАТЬЯ 285 СИНГАПУРНЫЕ КОСМЕТИКИ И ПЕРСОНАЛЬНАЯ ЦЕЛЬ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

Таблица 286 Филлиппины Глиоксаль Маркет, БЛАГОДА, 2018-2033 (USD THOUSAND)

Таблица 287 Филлиппины Глиоксаль Маркет, БЛАГОДА, 2018-2033 (Тысяча тонн)

Таблица 288 Филлиппины Глиоксаль Маркет, Чистота, 2018-2033 (USD THOUSAND)

СТАТЬЯ 289 ФИЛЛИППИН ГЛИОКСАЛЬНЫЙ МАРКЕТ, ПРОДУКЦИОННЫЙ ПРОЦЕСС, 2018-2033 (USD THOUSAND)

Таблица 290 Филлиппины Глиоксаль Маркет, ПАККАГИНГ, 2018-2033 (USD THOUSAND)

Таблица 291 ФИЛЛИППИНОВЫЕ ДРУМЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 292 ФИЛЛИППИНОВЫЙ КОМПОЗИТЕЛЬ МКБ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 293 ФИЛЛИППИНЫ ЖЕРРИКАНСЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

Таблица 294 Филлиппинские Ботлеты в Глиоксал Маркет, Тип, 2018-2033 (USD THOUSAND)

Таблица 295 Филлиппины Глиоксаль Маркет, ПРИМЕЧАНИЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 296 ФИЛЛИППИНОВ КРОССКИЙ ЛИНКИНГ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 297 ХИМИЧЕСКИХ ИНТЕРМЕДИАТЕЛЬНЫХ ФИЛЛИППИНОВ, В ГЛИОКСАЛЬНОМ МАРКЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 298 ФИЛЛИППИННЫЕ КОМПЛЕКТИВНЫЕ КОМПЛЕКТИВНЫЕ ПРОИЗВОДСТВА В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 299 ПОЛИМЕР ФИЛЛИППИНОВ, ОБРАЩАЮЩИЙСЯ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 300 ФИЛЛИППИН ДРУГИХ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, ВЫБОР, 2018-2033 (USD THOUSAND)

Таблица 301 ФИЛЛИППИНЫ ГЛИОКСАЛЬНЫЙ МАРКЕТ, КОНЕЧНЫЕ ХИМИКАЛИ, 2018-2033 (USD THOUSAND)

Таблица 302 Филлиппины Глиоксаль Маркет, К концу использования, 2018-2033 (USD THOUSAND)

СТАТЬЯ 303 ФИЛЛИППИНСКИЕ КОСМЕТИКИ И ПЕРСОНАЛЬНАЯ КАРТИВА В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 304 ПРЕДОСТАВЛЕНИЕ АСИА-ПАЦИФИЧЕСКОГО ГЛИОКСАЛЬНОГО МАРКЕТА, К ГРАДЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 305 ПОСТАНОВЛЕНИЕ АСИА-ПАЦИФИЧЕСКОГО ГЛИОКСАЛЬНОГО МАРКЕТА, К ГРАДЕ, 2018-2033 (ТУСАНДЫЕ ТОНЫ)

СТАТЬЯ 306 ПРЕДОСТАВЛЕНИЕ АСИА-ПАЦИФИЧЕСКОГО ГЛИОКСАЛЬНОГО МАРКЕТА, ПО ПРАВИТЕЛЬНОСТИ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 307 ПОСТАНОВЛЕНИЕ АСИА-ПАЦИФИЧЕСКОГО ГЛИОКСАЛЬНОГО МАРКЕТА, ПО ПРОДУКЦИОННОМУ ПРОЦЕССУ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 308 ПОСТАНОВЛЕНИЕ АСИА-ПАЦИФИЧЕСКОГО ГЛИОКСАЛЬНОГО МАРКЕТА, ПАККАГИНГ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 309 ПРЕДОСТАВЛЕНИЕ АСИА-ПАЦИФИЧЕСКИХ ПРАВИЛ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 310 ПРЕДОСТАВЛЕНИЕ АСИА-ПАЦИФИЧЕСКОГО КОМПОЗИТА IBC в ГЛИОКСАЛЬНОМ МАРКЕТЕ, КИТАЙ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 311 ПЕРЕСТ АСИА-ПАЦИФИЧЕСКИХ ИЕРРИКАНСОВ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 312 ПЕРЕДАЧА АСИА-ПАЦИФИЧЕСКИХ БОТТЛЕЙ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 313 ПОСТАНОВЛЕНИЕ АСИА-ПАЦИФИЧЕСКОГО ГЛИОКСАЛЬНОГО МАРКЕТА, ПРИМЕЧАНИЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 314 ПРЕДОСТАВЛЕНИЕ АСИА-ПАЦИФИЧЕСКОГО КРОССА-ЛИНКИНГА В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 315 ПРЕДОСТАВЛЕНИЕ АСИА-ПАЦИФИЧЕСКИХ ХИМИЧЕСКИХ ИНТЕРМЕДИАТЕЛЕЙ, В ГЛИОКСАЛЬНОМ МАРКЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 316 ПРЕДОСТАВЛЕНИЕ АСИА-ПАЦИФИЧЕСКИХ БОЛЬНЫХ ХИМИЧЕСКИХ МАНИФАКТОРОВ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 317 ПРЕДОСТАВЛЕНИЕ АСИА-ПАЦИФИЧЕСКОГО ПОЛИМЕРА, ПРОЦЕССИРОВАННОГО В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 318 ПЕРЕДАЧА АСИА-ПАЦИФИЧЕСКИХ ДРУГИХ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 319 ПРОСТОКИ АСИА-ПАЦИФИЧЕСКОГО ГЛИОКСАЛЬНОГО МАРКЕТА, ПО КОНЕЧНОМУ ИСПОЛЬЗОВАНИЮ, 2018-2033 (USD THOUSAND)

СТАТЬЯ 320 ПЕРЕДАЧА АСИА-ПАЦИФИЧЕСКОГО ГЛИОКСАЛЬНОГО МАРКЕТА, К концу использования, 2018-2033 (USD THOUSAND)

СТАТЬЯ 321 ПРЕДОСТАВЛЕНИЕ АСИА-ПАЦИФИЧЕСКИХ КОСМЕТИКОВ И ПЕРСОНАЛЬНОЙ КАРТЫ В ГЛИОКСАЛЬНОМ МАРКЕТЕ, В ТИПЕ, 2018-2033 (USD THOUSAND)

Список рисунков

ФИГРАФИЯ 1 АСИА-ПАЦИФИЧЕСКИЙ ГЛИОКСАЛЬНЫЙ МАРКЕТ: СЕГМЕНТАЦИЯ

ФИГРАФИЯ 2 АСИА-ПАЦИФИЧЕСКИЙ ГЛИОКСАЛЬНЫЙ МАРКЕТ: ТРИАНГУЛЯЦИЯ ДАННЫХ

ФИГРА 3 АСИА-ПАЦИФИЧЕСКИЙ ГЛИОКСАЛЬНЫЙ МАРКЕТ: ДРОК АНАЛИЗИС

ФИГРА 4 АСИА-ПАЦИФИЧЕСКИЙ ГЛИОКСАЛЬНЫЙ МАРКЕТ: ФИЛИППИНЫ VS РЕГИОНАЛЬНЫЙ АНАЛИЗ

ФИГРА 5 АСИА-ПАЦИФИЧЕСКИЙ ГЛИОКСАЛЬНЫЙ МАРКЕТ: КОМПАНИЯ ИССЛЕДОВАНИЕ АНАЛИЗА

ФИГРА 6 АСИА-ПАЦИФИЧЕСКИЙ ГЛИОКСАЛЬНЫЙ МАРКЕТ: ИНТЕРВЬЮ-ДЕМОГРАФИКА

ФИГРА 7 АСИА-ПАЦИФИЧЕСКИЙ ГЛИОКСАЛЬНЫЙ МАРКЕТ: ДБМР МАРКЕТ ПОСИЦИОННЫЙ ГРИД

8 DBMR VENDOR SHARE ANALYSIS

ФИГРАФИЯ 9 АСИА-ПАЦИФИЧЕСКИЙ ГЛИОКСАЛЬНЫЙ МАРКЕТ: СЕГМЕНТАЦИЯ

Рисунок 10 ИСКЛЮЧИТЕЛЬНОЕ РЕЗЮМЕ

11 СТРАТЕГИЧЕСКИЕ РЕШЕНИЯ

ФИГРА 12 ШЕСТЬ СЕГМЕНТОВ КОМПРИЗАЦИЯ АСИА-ПАЦИФИЧЕСКОГО ГЛИОКСАЛЬНОГО МАРКЕТА, ПО ПРОДУКТУ (2025)