Asia Pacific Panel Mount Industrial Display Market

Размер рынка в млрд долларов США

CAGR :

%

USD

731.18 Million

USD

1,500.25 Million

2025

2033

USD

731.18 Million

USD

1,500.25 Million

2025

2033

| 2026 –2033 | |

| USD 731.18 Million | |

| USD 1,500.25 Million | |

| % | |

|

Asia-Pacific Panel Mount Industrial Display Market Segmentation, By Technology (LED, Liquid Crystal Display (LCD), and OLED), Panel Size (14" -21", Up To 14", 22"-40" and 41", and above), Resolution (HD, 4K, and Others), Touch Availability (Touch and Non Touch), Application (HMI, Industrial Open Frame Monitors, Remote Monitoring, and Imaging), End User (Manufacturing, Medical, Oil and Gas, Food Processing, Transportation, Energy and Power, and Others) - Industry Trends and Forecast to 2033

Каков размер и темпы роста рынка промышленных дисплеев Азиатско-Тихоокеанской панели

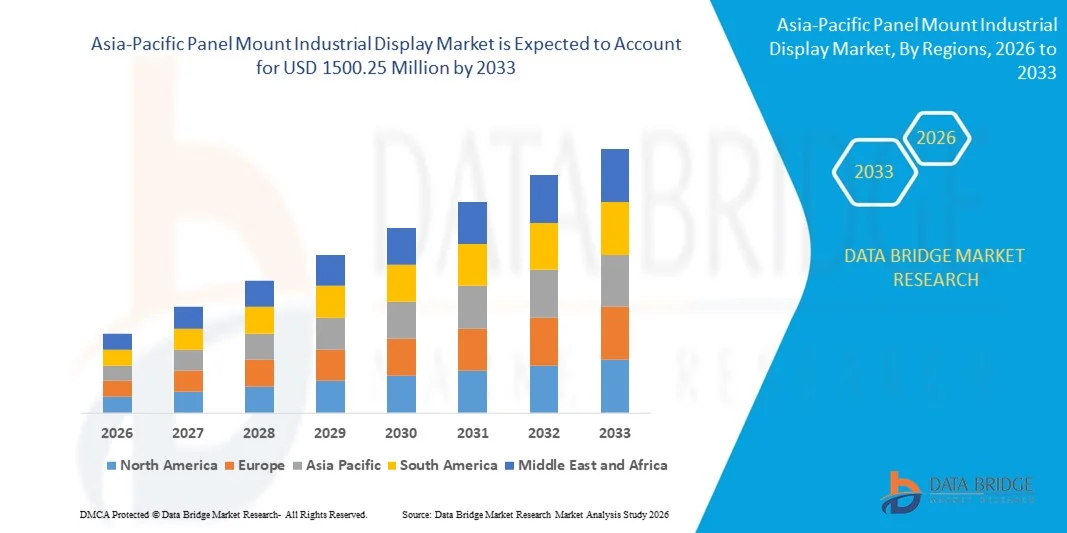

- Согласно анализу Data Bridge Market Research, размер рынка промышленных дисплеев в Азиатско-Тихоокеанском регионе был оценен как731,18 млн долларов США в 2025 годуОжидается, что он достигнет$1500,25 млн к 2033 году, вCAGR 9,40%в течение прогнозируемого периода

- Рост рынка в значительной степени обусловлен растущим внедрением промышленной автоматизации и интеграции интеллектуальных заводских решений, которые способствуют внедрению передовых технологий отображения для мониторинга и управления сложными промышленными процессами.

- Кроме того, растущий спрос на долговечные, высокопроизводительные и интерактивные решения для отображения, которые обеспечивают визуализацию и аналитику в реальном времени в производственном, энергетическом и транспортном секторах, укрепляет промышленные дисплеи для монтажа панелей в качестве основных компонентов современных промышленных операций. Эти факторы ускоряют внедрение во многих отраслях, тем самым значительно стимулируя рост рынка.

Размер рынка и прогноз

- Рыночная стоимость Азиатско-Тихоокеанского региона (2025):731,18 млн. долларов США

- Ожидаемая рыночная стоимость (2033):$1500,25 млн.

- Прогноз CAGR (2026–2033):9.40%

Азиатско-Тихоокеанская панель Mount Industrial Display Market Analysis

- Панельные промышленные дисплеи, обеспечивающие высококачественную визуализацию и возможности интерфейса оператора для машин, панелей управления иудаленный мониторингСистемы становятся все более важными в промышленных условиях из-за их способности повышать эффективность процесса, эксплуатационную безопасность и принятие решений в режиме реального времени.

- Растущее освоение рынка в первую очередь подпитывается растущей промышленной оцифровкой, растущим спросом на решения HMI на интеллектуальных заводах и потребностью в надежных и простых в интеграции дисплеях, которые поддерживают прогностическое обслуживание, подключение к IoT и передовые приложения мониторинга.

- Китай доминирует на рынке промышленных панелей В 2025 году благодаря своему обширному производственному сектору, растущему внедрению промышленной автоматизации и растущим инвестициям в интеллектуальные заводские решения.

- Ожидается, что Индия станет самой быстрорастущей страной на рынке промышленных дисплеев в течение прогнозируемого периода из-за растущей модернизации промышленности, растущего внедрения автоматизации заводов и роста производства электроники и автомобилей.

- Сегмент HD доминировал на рынке с долей рынка 48% в 2025 году, благодаря своей экономической эффективности и пригодности для большинства требований промышленного мониторинга. HD-дисплеи обеспечивают достаточную ясность для визуализации данных в режиме реального времени, управления оператором и мониторинга тревоги без чрезмерных затрат на оборудование или энергию.

Сегментация рынка промышленных дисплеев Report Scope and Panel Mount

|

Атрибуты |

Панель Mount Industrial Display Key Market Insights |

|

Сегменты покрыты |

|

|

Страны, охваченные |

Азиатско-Тихоокеанский регион

|

|

Ключевые игроки рынка |

|

|

Рыночные возможности |

|

|

Информационные наборы данных с добавленной стоимостью |

|

Какова ключевая тенденция на рынке промышленных дисплеев Азиатско-Тихоокеанского региона

Растущее внедрение Smart Factory Automation

- Значительной тенденцией на рынке промышленных дисплеев является растущее внедрение «умной» автоматизации производства, обусловленное необходимостью мониторинга в режиме реального времени, повышения операционной эффективности и бесшовного взаимодействия человека и машины в производственных средах. Эта тенденция побуждает производителей развертывать передовые дисплеи, которые обеспечивают интуитивную визуализацию и контроль сложных производственных процессов.

- Например, Siemens предлагает дисплеи SIMATIC HMI, которые интегрируются с его системами автоматизации, предоставляя операторам данные машины в реальном времени, панели управления производительностью и интерактивные элементы управления. Эти решения улучшают видимость процесса и позволяют прогнозировать техническое обслуживание, уменьшая время простоя в высокоавтоматизированных объектах.

- Интеграция промышленных дисплеев с оборудованием с поддержкой IoT ускоряется, позволяя компаниям собирать, анализировать и отображать критически важные данные на производственных площадках. Это позиционирование панелей в качестве основных инструментов для инициатив Индустрии 4.0, поддержки цифровых двойников, удаленного мониторинга и оптимизации процессов.

- Растет интерес к прочным дисплеям, способным работать в суровых промышленных условиях, таких как высокая температура, пыль и вибрация. Производители все чаще ищут решения, которые сочетают долговечность с сенсорными экранами высокого разрешения для поддержания эксплуатационной надежности и безопасности сотрудников.

- Отрасли здравоохранения и автоматизации лабораторий внедряют промышленные дисплеи для повышения точности управления оборудованием и мониторинга экспериментов в режиме реального времени. Эти приложения требуют высокочувствительных интерфейсов и гибкой интеграции дисплеев для поддержки сложных рабочих процессов и строгих нормативных стандартов.

- На рынке наблюдается повышенный спрос на модульные и масштабируемые системы отображения, которые могут быть адаптированы к конкретным производственным или промышленным рабочим процессам. Эта тенденция отражает всеобъемлющий сдвиг в сторону гибких, совместимых решений HMI, которые повышают производительность и обеспечивают бесшовную цифровую интеграцию в различных отраслях.

Азиатско-Тихоокеанская панель Mount Industrial Display Market Dynamics

водитель

Растущий спрос на высокопроизводительные HMI-дисплеи

- Растущая сложность промышленных процессов и стремление к автоматизации стимулируют спрос на высокопроизводительные HMI-дисплеи, которые предлагают сенсорную интерактивность, высокое разрешение и визуализацию данных в реальном времени. Эти дисплеи позволяют операторам эффективно управлять несколькими параметрами машины и снижать частоту ошибок.

- Например, Rockwell Automation предоставляет серию PanelView Plus, предлагая высокопроизводительные панели отображения, которые интегрируются с контроллерами Allen-Bradley. Эти панели улучшают управление процессом, поддерживают предиктивное обслуживание и повышают эксплуатационную безопасность на заводских этажах.

- Производители все чаще отдают приоритет дисплеям, поддерживающим мультисенсорную функциональность, графические интерфейсы и совместимость с современными промышленными протоколами. Эти возможности обеспечивают бесшовную интеграцию с системами SCADA, PLC и MES, что повышает общую эффективность производства.

- Промышленный автомобильный сектор использует высокопроизводительные панельные монтажные дисплеи для мониторинга производительности сборочных линий, операций роботов и показателей цепочки поставок. Эти решения улучшают принятие решений в режиме реального времени и упрощают процедуры технического обслуживания.

- Растущие инициативы по оцифровке промышленности стимулируют инвестиции в передовые дисплеи, которые поддерживают аналитику, приборные панели и удаленный доступ. Растущее ожидание более умных, быстрых и надежных решений для мониторинга продолжает стимулировать внедрение высокопроизводительных систем HMI.

Сдержанность/вызов

Высокие затраты и жесткие экологические ограничения

- Рынок промышленных дисплеев с панелями сталкивается с проблемами из-за высоких затрат на приобретение и обслуживание, особенно для прочных или специализированных дисплеев, предназначенных для экстремальных условий. Эти расходы могут ограничить принятие среди малых и средних предприятий с ограниченными бюджетами.

- Например, Advantech производит дисплеи для монтажа панелей промышленного класса, спроектированные для экстремальных температур, вибрации и воздействия пыли, но их передовой дизайн и материалы способствуют повышению цен. Компании должны сбалансировать затраты с требованиями к производительности и долговечности

- Работа в суровых промышленных условиях требует, чтобы дисплеи соответствовали строгим сертификатам, таким как IP65 / IP67 для водо- и пылестойкости, увеличивая сложность конструкции и производственные затраты. Соблюдение правил безопасности и охраны окружающей среды добавляет еще один уровень финансовой и операционной нагрузки.

- Ограниченная доступность высокопрочных компонентов, специализированных сенсорных экранов и систем подсветки может замедлить производство и ограничить масштабируемость. Производители сталкиваются с давлением для поддержания стабильной производительности при контроле затрат и проблем цепочки поставок.

- Рынок продолжает сталкиваться с ограничениями, связанными с развертыванием современных дисплеев в существующей инфраструктуре с различными электрическими и механическими стандартами. Решение этих экологических и стоимостных проблем остается критически важным для более широкого внедрения и долгосрочного роста.

Азиатско-Тихоокеанская панель Mount Industrial Display Market Scope

Рынок сегментирован на основе технологии, размера панели, разрешения, доступности касания, приложения и конечного пользователя.

- По технологии

На основе технологии рынок промышленных дисплеев сегментирован на светодиодный, жидкокристаллический дисплей (LCD) и OLED. Сегмент ЖК-дисплеев доминировал на рынке с самой большой долей выручки в 2025 году, чему способствовали его надежность, экономичность и широкое внедрение в различных промышленных приложениях. ЖК-дисплеи предпочитают отрасли для их четкой видимости при различных условиях освещения и совместимости с устаревшими системами. Они также поддерживают широкий диапазон размеров и разрешений, обеспечивая бесшовную интеграцию в панели управления и интерфейсы операторов. Спрос на технологию ЖК-дисплеев еще больше усиливается постоянными улучшениями яркости, контрастности и долговечности, которые делают ее пригодной как для внутренних, так и для умеренно суровых промышленных условий.

Ожидается, что в сегменте OLED будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, чему способствует растущее внедрение в передовых промышленных приложениях, требующих высокой контрастности, широких углов обзора и превосходной цветопередачи. Например, такие компании, как Advantech, внедряют дисплеи на основе OLED в премиальных системах HMI, где четкость и визуальная точность имеют решающее значение. Технология OLED также позволяет создавать более тонкие и легкие панели, которые экономят пространство в компактных диспетчерских. Его энергоэффективность и потенциал для гибких конструкций еще больше повышают интерес к медицинским и производственным приложениям. Растущее внимание к интеллектуальным заводам следующего поколения и решениям для автоматизации поддерживает эту траекторию быстрого роста.

- Размер панели

Исходя из размеров панелей, рынок сегментирован на 14"-21", До 14", 22"-40" и 41" и выше. Сегмент 14-21 доминировал на рынке с наибольшей долей выручки в 2025 году благодаря своей универсальности и совместимости со стандартными промышленными системами управления. Эти дисплеи среднего размера обеспечивают баланс между читаемостью и удобством установки, что делает их подходящими для панелей операторов, интерфейсов машин и станций мониторинга. Отрасли часто предпочитают этот диапазон размеров, потому что он обеспечивает четкую визуализацию оперативных данных, не занимая слишком много места. Спрос также обусловлен интеграцией с мультидисплеями и модульными панелями управления в производственных и технологических средах автоматизации.

Ожидается, что в сегменте 22-40 будет наблюдаться самый быстрый рост с 2026 по 2033 год, чему способствует увеличение развертывания в передовых приложениях мониторинга и удаленной визуализации. Например, Siemens интегрировала широкоформатные дисплеи в диспетчерские, чтобы обеспечить операторам повышенную ситуационную осведомленность. Большие панели позволяют выполнять многооконные операции и детально визуализировать сложные процессы. Их растущая популярность поддерживается растущим внедрением в управление энергией, мониторинг транспорта и интеллектуальные заводские установки, где комплексная визуализация повышает эффективность работы.

- Резолюцией

На основе разрешения рынок сегментирован на HD, 4K и другие. Сегмент HD доминировал на рынке с наибольшей долей выручки в 48% в 2025 году, что обусловлено его экономической эффективностью и пригодностью для большинства требований промышленного мониторинга. HD-дисплеи обеспечивают достаточную ясность для визуализации данных процесса в реальном времени, управления оператором и мониторинга тревоги без чрезмерных затрат на оборудование или энергию. Многие отрасли по-прежнему полагаются на разрешение HD из-за его совместимости с устаревшими системами и простоты интеграции в многопанельные настройки. HD-дисплеи также обеспечивают постоянную производительность при переменном освещении и условиях окружающей среды, что делает их выбором по умолчанию для производственных и перерабатывающих предприятий.

Ожидается, что сегмент 4K будет наблюдать самый быстрый рост с 2026 по 2033 год, чему способствует растущий спрос на визуализацию высокой четкости в таких приложениях, как визуализация, медицинский мониторинг и передовые системы HMI. Например, компания Beckhoff внедрила 4K-дисплеи в высокопроизводительные системы автоматизации для точной визуализации сложных производственных линий. Превосходное разрешение повышает четкость деталей и точность работы. По мере того, как промышленные процессы становятся более интенсивными, 4K-дисплеи обеспечивают лучшее понимание и облегчают прогностическое обслуживание и контроль качества, ускоряя их внедрение.

- Доступность Touch

На основе доступности сенсорных дисплеев рынок сегментирован на сенсорные и не сенсорные дисплеи. Сегмент non-touch доминировал на рынке с самой большой долей выручки в 2025 году, что обусловлено его надежностью, надежностью и снижением потребностей в обслуживании в суровых промышленных условиях. Дисплеи без касания широко используются в настройках, где операторы в основном используют внешние устройства ввода или панели управления для взаимодействия. Их простой дизайн и долговечность против пыли, вибрации и колебаний температуры делают их идеальными для производственных полов и технологических заводов. Кроме того, не сенсорные дисплеи часто предлагают более длительный срок службы и более низкую общую стоимость владения, что способствует широкому внедрению в устаревшие промышленные установки.

Ожидается, что сегмент сенсорных решений продемонстрирует самый быстрый рост с 2026 по 2033 год, чему будет способствовать расширение применения интерактивных систем HMI и интеллектуальных промышленных решений. Например, Schneider Electric развернула сенсорные панельные дисплеи для повышения эффективности оператора и оптимизации управления автоматизированными процессами. Сенсорные дисплеи обеспечивают интуитивное взаимодействие, уменьшают потребность в дополнительных периферийных устройствах ввода и поддерживают операции на основе жестов. Их растущее внедрение также обусловлено ростом интеллектуальных заводов и инициатив Industry 4.0, требующих доступа к данным в режиме реального времени и контроля на месте.

- С помощью приложения

На основе применения рынок сегментирован на HMI, промышленные мониторы с открытыми рамками, удаленный мониторинг и визуализацию. Сегмент HMI доминировал на рынке с наибольшей долей выручки в 2025 году, что обусловлено его критической ролью в мониторинге и контроле промышленных процессов. HMI позволяют операторам визуализировать производственные данные, регулировать параметры и получать оповещения в режиме реального времени, повышая эффективность и безопасность на производственных и перерабатывающих предприятиях. Дисплеи HMI часто выбираются из-за их долговечности, видимости при различных условиях освещения и интеграции с программируемыми логическими контроллерами (PLC). Их совместимость с устаревшими и современными системами автоматизации еще больше усиливает их доминирование на рынке.

Ожидается, что в сегменте удаленного мониторинга будет наблюдаться самый быстрый рост с 2026 по 2033 год, чему способствует рост промышленной оцифровки и принятие решений для мониторинга с поддержкой IoT. Например, Honeywell использует панельные дисплеи в настройках удаленного мониторинга для визуализации и управления в режиме реального времени на нескольких сайтах. Дистанционные мониторы позволяют централизованно управлять сложными операциями, прогнозировать техническое обслуживание и сокращать время простоя. Ожидается, что растущий акцент на промышленной автоматизации и интеллектуальном управлении объектами ускорит развертывание этих дисплеев в нескольких секторах.

- Конечный пользователь

На базе конечного потребителя рынок сегментирован в производство, медицину, нефть и газ, пищевую промышленность, транспорт, энергетику и энергетику и другие. Производственный сегмент доминировал на рынке с самой большой долей выручки в 2025 году, что обусловлено высоким спросом на решения для управления процессами, автоматизации и мониторинга на различных производственных линиях. Производственные мощности часто используют панельные монтажные дисплеи для повышения эффективности, визуализации производственных данных в режиме реального времени и поддержки инициатив по профилактическому обслуживанию. Доминирование сегмента поддерживается текущими проектами модернизации и автоматизации, направленными на повышение производительности и безопасности.

Ожидается, что в медицинском сегменте будет наблюдаться самый быстрый рост с 2026 по 2033 год, чему способствует растущее внедрение передовых решений для диагностической визуализации, мониторинга пациентов и автоматизации лабораторий. Например, GE Healthcare интегрирует панельные дисплеи в медицинские устройства визуализации, чтобы обеспечить визуализацию высокого разрешения для точной диагностики. Медицинские дисплеи требуют превосходной четкости, надежности и соответствия стандартам безопасности, что приводит к специализированному спросу. Рост также обусловлен растущим вниманием к телемедицине и автоматизированным системам здравоохранения, которые полагаются на интерактивные и высококачественные промышленные дисплеи.

Азиатско-Тихоокеанская панель Mount Industrial Display Market Региональный анализ

- Китай доминировал на рынке промышленных дисплеев с самой большой долей дохода в 2025 году, чему способствовал его обширный производственный сектор, увеличение внедрения промышленной автоматизации и рост инвестиций в интеллектуальные заводские решения.

- Устойчивые правительственные инициативы по продвижению Индустрии 4.0 в сочетании с быстрой урбанизацией и расширением производства электроники и автомобилей укрепляют лидерство Китая на региональном рынке.

- Присутствие ведущих отечественных производителей дисплеев, таких как Weintek Labs, сотрудничество с глобальными компаниями по автоматизации и внедрение доступных, но высокопроизводительных решений HMI, продолжают укреплять доминирующее положение Китая в течение прогнозируемого периода. Расширение внедрения промышленного IoT и повышение внимания к производительности и эффективности процессов еще больше укрепляют проникновение на рынок через промышленные центры.

Японская панель Mount Industrial Display Market Insight

Ожидается, что японский рынок будет неуклонно расти с 2026 по 2033 год, чему будет способствовать его передовой производственный сектор и сильный акцент на высококачественные решения для промышленной автоматизации. Японская промышленность все чаще внедряет компактные, многофункциональные и панели высокого разрешения для интеллектуальных заводов и операций по робототехнике, что отражает акцент страны на инновации и точность. Постоянные инвестиции в НИОКР и сотрудничество между японскими производителями и глобальными игроками в области автоматизации укрепляют перспективы устойчивого роста рынка. Приверженность Японии операционной эффективности, технологическому прогрессу и надежности лежит в основе ее сильного регионального позиционирования.

Индийская панель Mount Industrial Display Market Insight

Индия, по прогнозам, зарегистрирует самый быстрый CAGR на рынке промышленных дисплеев в Азиатско-Тихоокеанском регионе в течение 2026–2033 годов, чему будет способствовать растущая промышленная модернизация, растущее внедрение автоматизации заводов и рост производства электроники и автомобилей. Правительственные программы, продвигающие «Make in India» и промышленную цифровизацию, ускоряют освоение рынка. Спрос на экономически эффективные, долговечные и простые в интеграции дисплеи особенно высок среди развивающихся производственных МСП. Расширение промышленных IoT-инициатив, расширение партнерских отношений с глобальными поставщиками решений для автоматизации, такими как Siemens, и повышение осведомленности об оптимизации процессов обеспечивают становление Индии как самого быстрорастущего рынка в регионе.

Каковы ведущие компании на рынке промышленных дисплеев Азиатско-Тихоокеанского региона

Индустрия промышленных дисплеев в основном возглавляется хорошо зарекомендовавшими себя компаниями, в том числе:

- Advantech Co., Ltd. (Тайвань)

- Siemens AG (Германия)

- Schneider Electric (Франция)

- Panasonic Holdings Corporation (Япония)

- Rockwell Automation, Inc. (США)

- LG Display Co., Ltd. (Южная Корея)

- Samsung Electronics Co., Ltd. (Южная Корея)

- Mitsubishi Electric Corporation (Япония)

- BOE Technology Group Co., Ltd. (Китай)

- AU Optronics Corp. (Тайвань)

- Winmate Inc. (Тайвань)

- Planar Systems, Inc. (США)

- Eizo Corporation (Япония)

- Sparton Corporation (США)

- Pepperl+Fuchs (Германия)

- GE Automation (США)

- Beijer Electronics Group AB (Швеция)

- Kontron AG (Германия)

- Litemax Electronics Inc (Тайвань)

- Axiomtek Co., Ltd. (Тайвань)

Последние события на Азиатско-Тихоокеанском рынке промышленных дисплеев Panel Mount

- В апреле 2023 года компания Advantech Co., Ltd., мировой лидер в области промышленных вычислительных и дисплейных решений, представила новую линейку прочных панелей для промышленных дисплеев, специально разработанных для суровых производственных условий в Юго-Восточной Азии. Этот запуск подчеркивает нацеленность Advantech на предоставление надежных высокопроизводительных решений HMI, адаптированных к высоким требованиям секторов промышленной автоматизации. Включая передовые технологии сенсорного экрана и подключения к IoT, Advantech укрепляет свои позиции на быстро растущем рынке промышленных дисплеев для монтажа панелей.

- В марте 2023 года Siemens AG запустила свою последнюю серию промышленных дисплеев, основанных на искусственном интеллекте, с аналитикой для прогнозного обслуживания на интеллектуальных заводах. Новые дисплеи Siemens, предназначенные для автомобильной и энергетической промышленности, позволяют осуществлять мониторинг в режиме реального времени и повышать эффективность работы. Этот запуск подчеркивает стремление Siemens к инновациям в технологии промышленных дисплеев и его вклад в ускорение глобального внедрения Industry 4.0.

- В марте 2023 года Schneider Electric завершила развертывание своих передовых дисплеев для монтажа панелей в рамках проекта «Модернизация интеллектуальных сетей» в Германии. Эти дисплеи используются в удаленных центрах мониторинга и управления для повышения надежности сети и оперативной видимости. Проект демонстрирует стремление Schneider Electric интегрировать передовые решения визуализации в критическую инфраструктуру, поддерживая более интеллектуальные и устойчивые энергетические сети.

- В феврале 2023 года Rockwell Automation, Inc. объявила о стратегическом партнерстве с ведущими производителями для интеграции своих промышленных дисплеев для монтажа панелей с периферийными вычислительными платформами. Это сотрудничество направлено на улучшение обработки данных в режиме реального времени и повышение эффективности автоматизации на производственных площадках. Инициатива подчеркивает стремление Rockwell Automation предоставлять комплексные решения, которые оптимизируют производственные процессы и обеспечивают более интеллектуальные промышленные экосистемы.

- В январе 2023 года LG Display Co., Ltd. представила новую серию промышленных дисплеев с монтажом панелей сверхвысокой четкости с технологией OLED на CES 2023. Эти дисплеи обеспечивают исключительное качество изображения и энергоэффективность, обслуживая передовые промышленные приложения, такие как медицинское оборудование и транспортные системы. Внедрение LG Display подчеркивает нацеленность компании на расширение своего присутствия на рынке промышленных дисплеев с помощью визуальных решений следующего поколения.

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.