Europe Angioplasty Balloons Market

Размер рынка в млрд долларов США

CAGR :

%

USD

795.22 Million

USD

874.84 Million

2025

2033

USD

795.22 Million

USD

874.84 Million

2025

2033

| 2026 –2033 | |

| USD 795.22 Million | |

| USD 874.84 Million | |

| % | |

|

Europe Angioplasty Balloons Market Segmentation, By Type (Plain Old Balloon Angioplasty, Drug-Coated Balloon (DCB) Angioplasty, Cutting Balloons, Scoring Balloons, and Stent Graft Balloon Catheter), Material (Nylon, Polyurethane, Silicone Urethane Co-Polymers, and Other), Balloon Type (Semi-Compliant and Non-Compliant), Disease Indication (Coronary Angioplasty, Venous Angioplasty, Carotid Angioplasty, Renal Artery Angioplasty, and Peripheral Angioplasty), End User (Cath Labs, Hospitals, Specialty Clinics, Ambulatory Surgery Centers, and Diagnostic Centers)- Industry Trends and Forecast to 2033

Europe Angioplasty Balloons Market Size

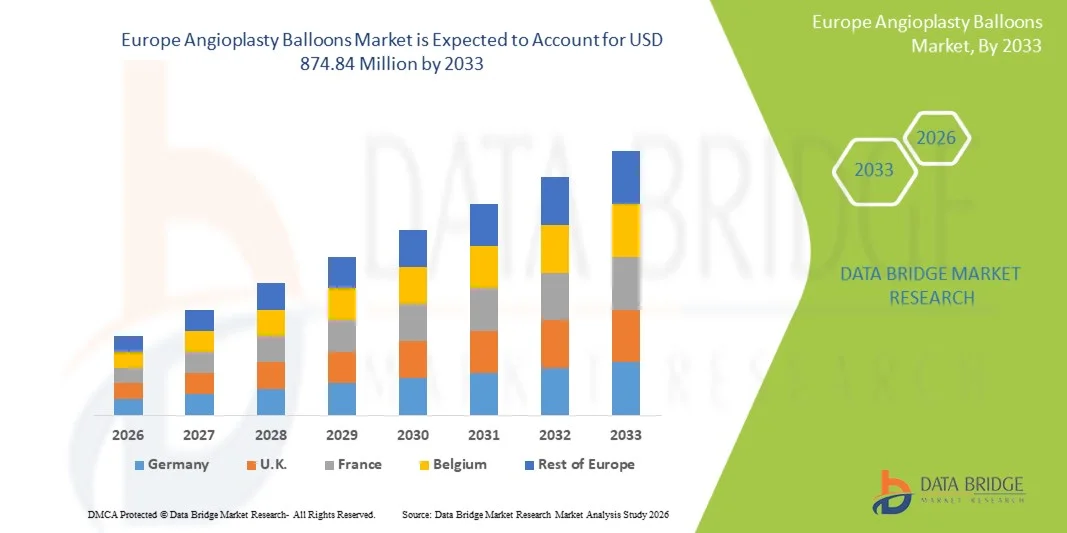

- The Europe angioplasty balloons market size was valued at USD 795.22 million in 2025 and is expected to reach USD 874.84 million by 2033, at a CAGR of 1.2% during the forecast period

- The market growth is largely fueled by the rising prevalence of cardiovascular diseases, increasing geriatric population, and continuous technological advancements in minimally invasive interventional procedures across Europe, which are enhancing treatment outcomes and procedural efficiency

- Furthermore, growing preference for minimally invasive surgeries, increasing adoption of drug-coated and scoring balloons, and strong healthcare infrastructure across countries such as Germany, France, and the UK are establishing angioplasty balloons as a critical component in modern cardiovascular treatment. These converging factors are accelerating the adoption of advanced angioplasty solutions, thereby significantly boosting the market growth

Europe Angioplasty Balloons Market Analysis

- Angioplasty balloons, used for dilating narrowed or blocked coronary and peripheral arteries, are increasingly critical components of modern interventional cardiology procedures in both hospitals and specialized cardiac centers due to their minimally invasive nature, precision, and integration with advanced catheter systems

- The escalating demand for angioplasty balloons is primarily fueled by the rising prevalence of cardiovascular diseases, growing geriatric population, and continuous technological advancements in drug-coated and specialty balloons, which improve procedural success rates and patient outcomes

- Germany dominated the Europe angioplasty balloons market with the largest revenue share of 28.4% in 2025, characterized by well-established healthcare infrastructure, high adoption of minimally invasive procedures, and the presence of leading medical device manufacturers

- France is expected to be the fastest growing country during the forecast period due to increasing healthcare investments, rising awareness about cardiovascular health, and expanding reimbursement coverage for interventional procedures

- Drug-Coated Balloon (DCB) Angioplasty segment dominated the Europe angioplasty balloons market with a market share of 47.8% in 2025, driven by its proven efficacy in reducing restenosis, growing clinical adoption, and compatibility with complex coronary and peripheral artery interventions

Report Scope and Europe Angioplasty Balloons Market Segmentation

|

Attributes |

Europe Angioplasty Balloons Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Angioplasty Balloons Market Trends

“Innovation in Drug-Coated and Specialty Balloons”

- A significant and accelerating trend in the Europe angioplasty balloons market is the growing adoption of drug-coated and specialty balloons, which improve procedural outcomes, reduce restenosis rates, and enhance patient recovery times

- For instance, the SeQuent® Please Neo DCB integrates antiproliferative coating with advanced catheter technology, enabling precise arterial dilation while minimizing the risk of vessel re-narrowing. Similarly, the Ranger™ Drug-Coated Balloon can be used for complex coronary lesions, offering reliable performance and improved long-term patency

- Specialty balloon innovations, such as scoring and cutting balloons, allow controlled plaque modification and better vessel expansion, reducing trauma to arterial walls. For instance, the AngioSculpt™ scoring balloon uses a helical nitinol scoring element to optimize lumen gain during angioplasty procedures

- Integration with imaging and delivery systems enables interventional cardiologists to achieve higher precision and improved procedural efficiency. Through advanced catheter designs, physicians can navigate tortuous vessels more effectively, increasing treatment success rates

- The trend towards more targeted, efficient, and clinically optimized balloons is reshaping expectations for interventional cardiology procedures. Consequently, companies such as B. Braun are developing next-generation drug-coated balloons with enhanced coating uniformity and trackability

- The demand for advanced balloons with superior safety and efficacy profiles is growing rapidly across both coronary and peripheral interventions, as hospitals increasingly prioritize better patient outcomes and cost-effective procedural solutions

- Growing adoption of remote procedural monitoring and data analytics in interventional cardiology is enhancing procedural planning and balloon selection, improving safety and long-term outcomes for patients across European hospitals

Europe Angioplasty Balloons Market Dynamics

Driver

“Rising Cardiovascular Disease Prevalence and Minimally Invasive Preference”

- The increasing prevalence of cardiovascular diseases across Europe, coupled with a growing preference for minimally invasive procedures, is a significant driver for the heightened demand for angioplasty balloons

- For instance, in March 2025, Medtronic reported advancements in drug-coated balloon delivery systems designed for complex coronary and peripheral interventions, targeting improved clinical outcomes. Such developments by key companies are expected to drive market growth during the forecast period

- As patient populations age and coronary artery disease becomes more common, angioplasty balloons provide effective, less invasive alternatives to open surgery, offering quicker recovery times and reduced hospital stays

- Furthermore, growing awareness among healthcare providers about the benefits of drug-coated and specialty balloons is making them a preferred choice for both routine and complex interventions, integrating seamlessly with modern cardiac care protocols

- The efficiency, safety, and procedural flexibility of contemporary angioplasty balloons, along with advancements in catheter technology and drug delivery, are key factors propelling their adoption in European hospitals and specialized cardiac centers

- Increased investment in hospital infrastructure and catheterization labs across Europe is supporting the adoption of advanced balloon technologies. For instance, new cardiac centers in France and Italy are equipping interventional suites with state-of-the-art balloon delivery systems

- Strategic partnerships between balloon manufacturers and cardiology societies are driving clinical education and training programs, improving procedural proficiency and encouraging wider adoption of specialized balloon technologies

Restraint/Challenge

“Cost and Regulatory Compliance Hurdles”

- The high device costs and stringent regulatory requirements pose significant challenges to broader adoption of angioplasty balloons across Europe, limiting penetration in price-sensitive healthcare systems

- For instance, high-profile reports on procedural reimbursement limitations and varying approval standards across countries have made some hospitals cautious about investing in premium drug-coated or specialty balloons

- Addressing these concerns through better cost-efficiency, clear clinical evidence, and alignment with European regulatory guidelines is crucial for wider acceptance. Companies such as Boston Scientific emphasize clinical trial data and regulatory compliance in their marketing to reassure hospitals and clinicians

- In addition, the complexity of training interventional cardiologists to use advanced balloon technologies can delay adoption, particularly in smaller or less specialized centers, creating a temporary barrier to market growth

- Overcoming these challenges through physician education programs, cost-optimized balloon designs, and streamlined regulatory approvals will be vital for sustained growth of the Europe angioplasty balloons market

- Variability in health insurance and reimbursement policies across European countries can slow adoption of high-cost balloons, particularly in Eastern Europe, where funding for advanced cardiac devices is limited

- Limited long-term clinical outcome data for newer specialty balloons can create hesitation among clinicians and hospital procurement teams. For instance, some centers prefer established balloon types until sufficient real-world evidence validates newer technologies’ efficacy and safety

Europe Angioplasty Balloons Market Scope

The market is segmented on the basis of type, material, balloon type, disease indication, and end user.

- By Type

On the basis of type, the Europe angioplasty balloons market is segmented into Plain Old Balloon Angioplasty (POBA), Drug-Coated Balloon (DCB) Angioplasty, Cutting Balloons, Scoring Balloons, and Stent Graft Balloon Catheter. The Drug-Coated Balloon (DCB) segment dominated the market with the largest revenue share of 47.8% in 2025, driven by its proven efficacy in reducing restenosis, growing clinical adoption, and suitability for complex coronary and peripheral interventions. Interventional cardiologists often prefer DCBs for high-risk patients, as they deliver localized drugs to the arterial walls without leaving permanent implants. The segment also benefits from innovations in coating technologies and delivery systems that enhance procedural precision. Hospitals and cath labs in Germany, France, and the U.K. routinely utilize DCBs, reinforcing their dominant market position. Increasing clinical evidence supporting long-term patient outcomes further accelerates adoption. In addition, partnerships between manufacturers and healthcare institutions promote awareness and training, sustaining segment leadership.

The Cutting Balloon segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by rising adoption in complex lesion treatments, including calcified and fibrotic plaques. Cutting balloons provide controlled scoring of the plaque, improving lumen gain and procedural outcomes while reducing trauma to arterial walls. They are increasingly adopted in specialty clinics and tertiary cardiac centers due to precision and safety. Clinical trials demonstrating enhanced outcomes in challenging lesions further support market expansion. Rising prevalence of cardiovascular diseases and aging populations are driving demand for cutting balloons across Europe. Manufacturers are focusing on next-generation cutting balloons with improved deliverability and safety profiles, ensuring continued growth.

- By Material

On the basis of material, the market is segmented into nylon, polyurethane, silicone urethane co-polymers, and others. The Nylon segment dominated the market in 2025, owing to its excellent flexibility, trackability, and compatibility with complex catheter navigation. Nylon balloons are highly favored by interventional cardiologists for tortuous and calcified vessels, offering reliable performance across coronary and peripheral procedures. Their cost-effectiveness and wide availability make them suitable for most hospitals. They also exhibit good expansion control, reducing procedural complications. Continuous R&D has enhanced material durability and safety, further reinforcing dominance. Adoption is particularly high in Germany and France, where advanced cardiac centers rely on Nylon-based balloons for routine and complex interventions.

The Silicone Urethane Co-Polymers segment is expected to witness the fastest growth from 2026 to 2033, driven by superior compliance, enhanced drug coating adherence, and improved safety profiles. This material allows precise arterial expansion while minimizing vessel trauma, making it ideal for DCBs and specialty balloons. The demand is rising in hospitals and specialty clinics seeking advanced solutions for high-risk patients. Innovation in polymer formulations is improving procedural outcomes and reducing complications. Growing awareness of safety and long-term efficacy is boosting adoption across Europe. Manufacturers are actively promoting the advantages of this material to expand its clinical usage.

- By Balloon Type

On the basis of balloon type, the market is segmented into semi-compliant and non-compliant balloons. The Semi-Compliant segment dominated the market in 2025, as these balloons provide an optimal balance between flexibility and vessel expansion control, suitable for a wide range of coronary and peripheral interventions. They conform to varying vessel diameters and navigate tortuous anatomies, reducing procedural complications. Compatibility with DCBs, scoring, and cutting balloons further enhances clinical adoption. Hospitals and cath labs prefer semi-compliant balloons for routine interventions. Continuous innovation in catheter and balloon design strengthens their clinical utility. Their wide availability and cost-effectiveness support ongoing dominance.

The Non-Compliant segment is expected to witness the fastest growth from 2026 to 2033, driven by its precision in high-pressure applications and use in post-dilation of stented arteries. Non-compliant balloons are critical in complex lesions where controlled dilation is necessary to avoid vessel rupture. Their adoption is increasing in tertiary cardiac centers performing advanced interventions. Improved material technology and safety features further boost market growth. Rising awareness of procedural precision among cardiologists accelerates demand. Manufacturers are investing in next-generation non-compliant balloons with enhanced deliverability and trackability.

- By Disease Indication

On the basis of disease indication, the market is segmented into coronary angioplasty, venous angioplasty, carotid angioplasty, renal artery angioplasty, and peripheral angioplasty. The Coronary Angioplasty segment dominated the market in 2025, accounting for the majority of procedures due to high prevalence of coronary artery disease in Europe. Coronary interventions are routinely performed in hospitals and specialized cath labs, with drug-coated and specialty balloons well established. Technological innovation, reimbursement support, and improved patient outcomes reinforce the segment’s leadership. Increasing numbers of elderly patients drive procedure volumes. Clinical guidelines continue to promote minimally invasive coronary interventions. Leading manufacturers focus on product portfolios tailored for coronary procedures, sustaining dominance.

The Peripheral Angioplasty segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing incidence of peripheral artery disease, especially in the elderly. Peripheral interventions require specialized balloons, including drug-coated and scoring types, for complex lesions in leg and arm arteries. Growing awareness among physicians and patients, combined with adoption of minimally invasive techniques, accelerates market growth. Manufacturers are introducing advanced peripheral balloons with better safety and trackability. Expanding infrastructure in specialty clinics and hospitals supports adoption. Rising focus on patient comfort and reduced hospital stays further drives demand.

- By End User

On the basis of end user, the market is segmented into cath labs, hospitals, specialty clinics, ambulatory surgery centers, and diagnostic centers. The Hospitals segment dominated the market in 2025, due to large procedure volumes, advanced infrastructure, and presence of experienced interventional cardiologists. Hospitals perform complex coronary and peripheral interventions and invest heavily in DCBs, scoring, and cutting balloons. High patient footfall, routine adoption of innovative procedures, and established cardiac programs contribute to the leading market share. Continuous training and clinical education strengthen procedural outcomes. Hospitals also leverage advanced imaging and delivery systems, reinforcing dominance.

The Specialty Clinics segment is expected to witness the fastest growth from 2026 to 2033, as smaller clinics increasingly adopt minimally invasive interventions for targeted populations. Specialty clinics expand infrastructure for peripheral and coronary interventions with high-precision, patient-specific balloon therapies. Rising cardiovascular awareness, procedural efficiency, and cost-effective care models are driving rapid adoption. Clinics are investing in DCBs and cutting/scoring balloons for niche patient needs. Training programs and partnerships with manufacturers support clinical expertise. Growing patient preference for outpatient and day-care interventions further fuels growth.

Europe Angioplasty Balloons Market Regional Analysis

- Germany dominated the Europe angioplasty balloons market with the largest revenue share of 28.4% in 2025, characterized by well-established healthcare infrastructure, high adoption of minimally invasive procedures, and the presence of leading medical device manufacturers

- Patients and hospitals in the country highly value advanced balloon technologies, such as drug-coated, cutting, and scoring balloons, for their proven efficacy in reducing restenosis, improving procedural outcomes, and supporting minimally invasive coronary and peripheral interventions

- This widespread adoption is further supported by high healthcare expenditure, advanced cardiac care centers, and strong clinical expertise among interventional cardiologists, establishing Germany as the primary market for angioplasty balloons across Europe

The Germany Angioplasty Balloons Market Insight

The Germany angioplasty balloons market captured the largest revenue share of 28.4% in 2025, driven by well-established healthcare infrastructure, high procedural volumes, and the presence of leading interventional cardiology device manufacturers. Hospitals and specialized cath labs prioritize the use of advanced balloon technologies, including drug-coated, cutting, and scoring balloons, for complex coronary and peripheral interventions. The country’s strong focus on minimally invasive procedures and ongoing clinical training programs supports widespread adoption. Moreover, reimbursement policies and public health initiatives promote the use of innovative balloons across hospitals and cardiac centers. Continuous investment in research and development, along with partnerships between manufacturers and healthcare providers, is further propelling market expansion. Germany’s emphasis on patient safety and procedural efficiency ensures sustained demand for angioplasty balloons across the region.

France Angioplasty Balloons Market Insight

The France angioplasty balloons market anticipated to grow at a noteworthy CAGR in 2025, fueled by growing cardiovascular disease prevalence and increasing awareness among healthcare providers. Hospitals and specialty cardiac centers are adopting advanced balloon technologies, including drug-coated and semi-compliant balloons, for both coronary and peripheral interventions. France’s investment in healthcare infrastructure and training programs enhances procedural efficiency and adoption rates. Increasing focus on minimally invasive therapies, patient safety, and long-term outcomes supports market growth. In addition, favorable reimbursement policies encourage the use of high-precision balloons in complex cases. Collaborations between manufacturers and medical institutions are also promoting clinical education and procedural adoption.

U.K. Angioplasty Balloons Market Insight

The U.K. angioplasty balloons market held a 15% revenue share in 2025, driven by well-developed cardiac care programs, high procedural volumes, and growing adoption of minimally invasive interventions. Hospitals and cath labs increasingly utilize drug-coated and cutting/scoring balloons to improve patient outcomes and reduce restenosis. Rising awareness of cardiovascular diseases among patients and clinicians contributes to the strong demand for advanced balloon technologies. The country’s robust healthcare infrastructure, along with ongoing clinical trials and physician training, supports procedural precision. In addition, adoption in both public and private hospitals ensures widespread usage. Manufacturers are actively promoting advanced balloon devices, which further enhances market growth in the U.K.

Italy Angioplasty Balloons Market Insight

The Italy angioplasty balloons market contributed 8% of Europe’s market in 2025, driven by expanding healthcare infrastructure and growing prevalence of coronary and peripheral artery diseases. Hospitals and cardiac centers are increasingly using drug-coated, semi-compliant, and specialty balloons for minimally invasive interventions. The focus on improving procedural success and reducing patient recovery time supports adoption. Clinical awareness programs and training initiatives for interventional cardiologists are enhancing usage across hospitals. Favorable reimbursement schemes for coronary and peripheral procedures are also encouraging hospitals to invest in advanced balloon technologies. Collaboration with manufacturers ensures ongoing supply of innovative devices, boosting market penetration.

Europe Angioplasty Balloons Market Share

The Europe Angioplasty Balloons industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Boston Scientific Corporation (U.S.)

- Abbott (U.S.)

- B. Braun SE (Germany)

- Terumo Corporation (Japan)

- BIOTRONIK SE & Co. KG (Germany)

- Cook (U.S.)

- Cordis (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- BD (U.S.)

- AngioDynamics, Inc. (U.S.)

- Merit Medical Systems, Inc. (U.S.)

- Teleflex Incorporated (U.S.)

- Integer Holdings Corporation (U.S.)

- NATEC Medical Ltd. (Ireland)

- ENDOCOR GmbH (Germany)

- Cardinal Health, Inc. (U.S.)

- Alvimedica Medical Technologies (Turkey)

- Hexacath (France)

- QT Vascular Ltd. (Singapore)

What are the Recent Developments in Europe Angioplasty Balloons Market?

- In May 2025, Medtronic received expanded CE‑Mark indications for its Prevail™ drug‑coated balloon (DCB) catheter in Europe, including use for complex bifurcation lesions and broader coronary artery disease treatments. This expansion builds on its original European launch and demonstrates growing adoption of advanced DCB technologies in complex vascular cases across Europe

- In May 2025, Boston Scientific announced the launch of the Sterling® SL PTA Balloon Dilatation Catheter in Europe, designed specifically for below‑the‑knee peripheral angioplasty with a low tip profile for improved deliverability and rapid deflation. This launch supports physicians treating peripheral artery disease with minimally invasive balloon options

- In October 2023, Boston Scientific presented clinical performance data on its Agent DCB at the TCT conference, showing the drug‑coated balloon significantly reduced target lesion failure and myocardial infarction compared to uncoated angioplasty in in‑stent restenosis, underscoring the clinical impact of advanced balloon therapies now available in Europe via CE Mark

- In July 2021, Medtronic began the European rollout of its newest Prevail DCB catheter following CE Mark approval, aimed at treating coronary artery disease, small vessel disease, and in‑stent restenosis with enhanced deliverability and safety, reflecting evolving device innovation in the Europe market

- In July 2021, Medtronic formally launched the Prevail™ drug‑coated balloon catheter in Europe after CE Mark approval, which delivers paclitaxel to arterial tissue and is used in percutaneous coronary intervention, marking a key product introduction in the interventional cardiology device category

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.