Europe Microgrid Market

Размер рынка в млрд долларов США

CAGR :

%

USD

4.08 Billion

USD

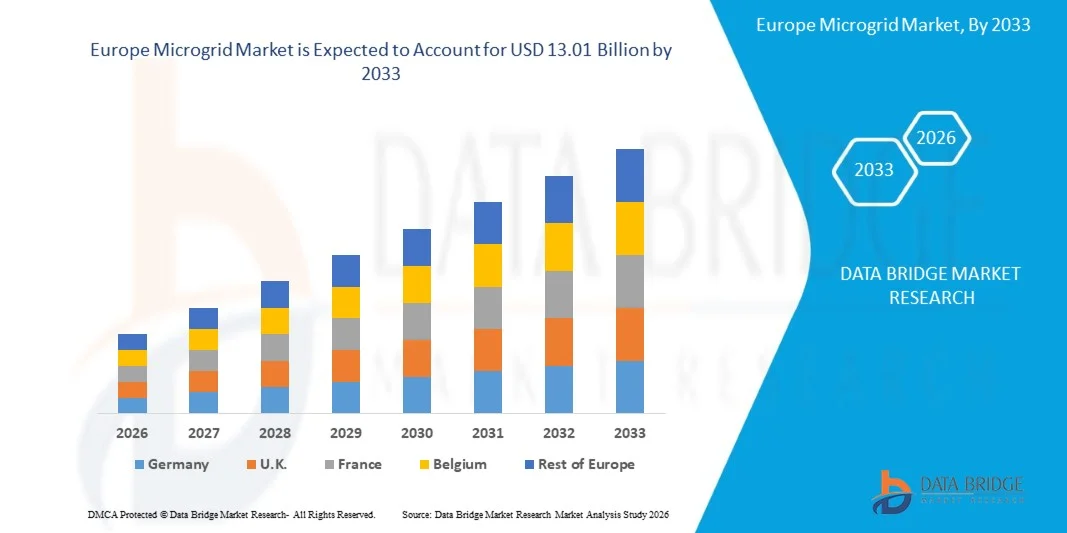

13.01 Billion

2025

2033

USD

4.08 Billion

USD

13.01 Billion

2025

2033

| 2026 –2033 | |

| USD 4.08 Billion | |

| USD 13.01 Billion | |

| % | |

|

Europe Microgrid Market Segmentation, By Grid Type (Alternate Current Microgrid, Direct Current Microgrid, and Hybrid), Connectivity (Grid Connected and Remote/Island), Offering (Hardware, Software and Services), Vertical (Healthcare, Educational Institutions, Industrial, Military and Electric Utility), Power Source (Natural Gas, Combined Heat and Power, Diesel, Solar, Fuel Cells, and Others)- Industry Trends and Forecast to 2033

Каков размер и обзор рынка микросетей в Европе

- Согласно анализу Data Bridge Market Research, размер рынка микросетей в Европе был оценен как4,08 млрд долларов США в 2025 годуОжидается, что он достигнет$13,01 млрд к 2033 году, вCAGR 15,60%в течение прогнозируемого периода

- Рост рынка в значительной степени обусловлен растущим спросом на децентрализованные энергетические системы, интеграцией возобновляемых источников энергии и потребностью в энергетической безопасности и надежности.

- Растущие инвестиции в интеллектуальные сети, технологии хранения энергии и правительственные инициативы по развитию устойчивой энергетической инфраструктуры также способствуют расширению рынка.

Размер рынка и прогноз:

- Размер рынка (2025):$4,08 млрд.

- Прогнозируемый размер рынка (2033):$13,01 млрд.

- CAGR (2026-2033):15.60%

Что такое анализ рынка микросетей в Европе

- Растущее внедрение возобновляемых источников энергии, таких как солнечная энергия, ветер и биомасса, стимулирует спрос на решения для микросетей.

- Увеличение частоты отключений электроэнергии и растущая потребность в устойчивой энергетической инфраструктуре в промышленных, коммерческих и отдаленных районах ускоряют рост рынка.

- Германия доминировала на европейском рынке микросетей с самой большой долей доходов в 2025 году, чему способствовали твердые обязательства правительства по декарбонизации, энергоэффективности и стабильности сетей, которые поощряют внедрение локализованных энергетических систем. Обширная промышленная база страны и передовые инициативы по интеграции возобновляемых источников энергии стимулируют спрос на устойчивые и гибкие энергетические решения.

- Ожидается, что в Великобритании будут наблюдаться самые высокие ежегодные темпы роста (CAGR) на европейском рынке микросетей из-за растущих инвестиций в низкоуглеродные энергетические решения, внедрения распределенной возобновляемой генерации и государственных стимулов для проектов в области чистой энергии. Увеличение спроса на энергию в городских центрах и коммерческих секторах, а также растущий интерес к энергетической устойчивости и интеграции интеллектуальных сетей стимулируют быстрый рост рынка в Великобритании.

- Сегмент микросетей переменного тока занимал самую большую долю рынка в 2025 году благодаря обширной существующей инфраструктуре, построенной вокруг распределения электроэнергии переменного тока и ее совместимости с обычными электрическими системами. Микросети переменного тока широко используются, поскольку они поддерживают широкий спектр приложений и облегчают интеграцию с коммунальными сетями. Они также предпочтительны для крупномасштабного развертывания на коммерческих и промышленных объектах из-за их способности эффективно справляться с более высокими нагрузками. Кроме того, микросети переменного тока обеспечивают гибкость в обслуживании и операционной масштабируемости.

Каков объем отчета и сегментация рынка микросетей в Европе

|

Атрибуты |

Европа Microgrid Key Market Insights |

|

Сегменты покрыты |

|

|

Страны, охваченные |

Европа

|

|

Ключевые игроки рынка |

|

|

Рыночные возможности |

|

|

Информационные наборы данных с добавленной стоимостью |

В дополнение к информации о рыночных сценариях, таких как рыночная стоимость, темпы роста, сегментация, географическое покрытие и основные игроки, рыночные отчеты, курируемые Data Bridge Market Research, также включают углубленный экспертный анализ, географически представленное производство и мощности компании, сетевые схемы дистрибьюторов и партнеров, подробный и обновленный анализ ценового тренда и анализ дефицита цепочки поставок и спроса. |

Каковы тенденции европейского рынка микросетей

«Растущее внедрение возобновляемых источников энергии и систем хранения энергии»

Растущее внимание к интеграции чистой энергии значительно формирует рынок микросетей, поскольку организации и коммунальные службы стремятся повысить надежность, эффективность и устойчивость энергетики. Микросети набирают обороты благодаря своей способности обеспечивать локальное производство энергии, резервное питание во время отключений и интеграцию с возобновляемыми источниками, что делает их идеальными для промышленных, коммерческих и общественных приложений. Эта тенденция побуждает разработчиков к инновациям с гибридными решениями для микросетей, которые сочетают в себе солнечные, ветровые и технологии хранения.

Растущая осведомленность об энергетической устойчивости, оптимизации затрат и экологической ответственности ускорила внедрение микросетей во многих секторах. Корпорации, учебные заведения, больницы и операторы критической инфраструктуры активно внедряют микросетевые решения для обеспечения бесперебойного электроснабжения и снижения углеродного следа. Это также привело к партнерским отношениям между поставщиками технологий, коммунальными компаниями и системными интеграторами для повышения возможностей управления энергопотреблением.

Тенденции децентрализации влияют на стратегии закупок энергии, при этом заинтересованные стороны подчеркивают локализованную генерацию, интеллектуальный контроль и независимость сети. Эти факторы помогают организациям оптимизировать эксплуатационные расходы, смягчить риски сбоев в работе сети и улучшить учетные данные устойчивости. Компании все чаще используют микросети для демонстрации приверженности целям ESG и повышения операционной надежности.

Например, в 2024 году Bloom Energy в США и Schneider Electric запустили передовые решения для микросетей для коммерческих и промышленных объектов, интегрируя возобновляемую генерацию, хранение энергии и интеллектуальные системы управления. Эти развертывания были разработаны для обеспечения высокой надежности, снижения затрат на электроэнергию и поддержки целей корпоративной устойчивости. Решения также продавались как готовые к будущему, масштабируемые и экологически ответственные энергетические системы.

В то время как спрос на микросети растет, долгосрочное расширение рынка зависит от продолжающихся технологических инноваций, оптимизации затрат и поддержки политики. Производители и разработчики сосредоточены на повышении эффективности системы, совместимости с существующей инфраструктурой и разработке стандартизированных модульных решений для более широкого внедрения.

Какова динамика рынка микросетей в Европе

водитель

Повышение потребности в энергетической устойчивости и интеграции возобновляемых источников энергии

Увеличение спроса на надежное и непрерывное электроснабжение является основным драйвером для рынка микросетей. Организации внедряют микросети для обеспечения бесперебойного электроснабжения, особенно в критически важных объектах и регионах, подверженных нестабильности сети. Тенденция также поощряет инвестиции в распределенные энергетические ресурсы (DER) и технологии интеллектуальных сетей для повышения энергетической безопасности.

Расширение приложений в промышленном, коммерческом, институциональном и удаленном секторах способствует росту рынка. Микросети помогают оптимизировать потребление энергии, снизить затраты и обеспечить интеграцию возобновляемой генерации, способствуя достижению целей устойчивого развития и операционной эффективности.

Поставщики технологий и разработчики энергетических решений продвигают внедрение микросетей с помощью инновационных предложений, таких как гибридные микросети, интеграция хранения энергии и платформы управления энергией на основе ИИ. Эти инициативы повышают надежность, предсказуемость и экономическую эффективность, поощряя сотрудничество между заинтересованными сторонами для повышения производительности системы.

Например, в 2023 году Tesla в США и Siemens развернули микросети для хранения энергии для промышленных и коммунальных применений, подчеркнув операционную эффективность и интеграцию с возобновляемыми источниками энергии. Эти развертывания продемонстрировали потенциал для экономии затрат, энергетической независимости и снижения углеродного следа.

Хотя растущий спрос поддерживает рост, более широкое внедрение зависит от финансирования, нормативной поддержки и технологической стандартизации. Инвестиции в масштабируемые, модульные решения, совместимость и расширенный мониторинг будут иметь решающее значение для удовлетворения спроса и поддержания конкурентных преимуществ.

Сдержанность/вызов

«Высокие капитальные затраты и сложность интеграции»

Относительно высокая первоначальная стоимость систем микросетей, включая инфраструктуру генерации, хранения и управления, остается ключевой проблемой, ограничивая внедрение среди организаций, чувствительных к затратам. Сложные проектные, монтажные и эксплуатационные требования дополнительно способствуют капитальным и эксплуатационным расходам.

Ограниченная осведомленность и технический опыт ограничивают принятие в определенных секторах, особенно для малых и средних предприятий и отдаленных общин. Пробелы в знаниях в области управления энергопотреблением, соблюдения нормативных требований и финансовых стимулов могут замедлить развертывание.

Интеграция с существующей энергетической инфраструктурой и соблюдение сетевых кодов добавляет сложности и стоимости. Расширенный мониторинг, интеллектуальный контроль и требования к взаимосвязи требуют квалифицированной рабочей силы, специализированного программного обеспечения и долгосрочных планов обслуживания.

Например, в 2024 году развертывание микросетей в образовательных кампусах и медицинских учреждениях ABB и Schneider Electric столкнулось с задержкой внедрения из-за высоких затрат на установку, одобрения регулирующих органов и проблем системной интеграции. Эти факторы повлияли на сроки осуществления проектов и потребовали дополнительных инвестиций в обучение и поддержку.

Преодоление этих проблем потребует экономически эффективного проектирования, стандартизированных решений и поддерживающей политики. Сотрудничество с коммунальными службами, поставщиками технологий и регулирующими органами может раскрыть весь потенциал микросетей, а разработка вариантов финансирования, решений «под ключ» и образовательных инициатив ускорит внедрение на рынок.

Что такое европейский рынок микросетей

Рынок сегментирован на основе типа сети, подключения, предложения, вертикального и источника питания.

• По типу сетки

По типу сетки европейский рынок микросетей сегментирован на альтернативные текущие микросети, прямые текущие микросети и гибридные. Сегмент микросетей переменного тока занимал самую большую долю рынка в 2025 году благодаря обширной существующей инфраструктуре, построенной вокруг распределения электроэнергии переменного тока и ее совместимости с обычными электрическими системами. Микросети переменного тока широко используются, поскольку они поддерживают широкий спектр приложений и облегчают интеграцию с коммунальными сетями. Они также предпочтительны для крупномасштабного развертывания на коммерческих и промышленных объектах из-за их способности эффективно справляться с более высокими нагрузками. Кроме того, микросети переменного тока обеспечивают гибкость в обслуживании и операционной масштабируемости.

Ожидается, что в сегменте микросетей постоянного тока будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, что обусловлено более высокой энергоэффективностью и снижением потерь конверсии, что делает его идеальным для возобновляемых источников энергии и современных нагрузок постоянного тока. Микросети постоянного тока становятся все более предпочтительными для их упрощенной архитектуры, более быстрого времени отклика и более легкой интеграции с солнечными фотоэлектрическими и аккумуляторными батареями. Они особенно подходят для жилых комплексов, кампусов и удаленных промышленных объектов. Растущее внедрение приборов и электроники постоянного тока еще больше усиливает расширение этого сегмента.

• Подключение

В Европе рынок микросетей сегментирован на Grid Connected и Remote/Island. Сегмент Grid Connected занимал самую большую долю рынка в 2025 году благодаря широкому внедрению взаимосвязанных систем, которые повышают надежность сети и поддерживают обмен энергией с традиционными коммунальными сетями. Сетевые микросети позволяют оптимизировать управление энергопотреблением и экономить средства за счет программ реагирования на спрос. Они также помогают коммунальным службам сбалансировать пиковые нагрузки и уменьшить потери энергии. Бесшовная интеграция с возобновляемыми источниками энергии, такими как солнечная энергия и ветер, еще больше увеличивает их развертывание в городских и полугородских районах.

Ожидается, что в сегменте удаленных/островных электростанций будут наблюдаться самые высокие темпы роста с 2026 по 2033 год, что обусловлено растущим спросом на внесетевые решения в районах с ограниченным доступом к централизованной энергии. Дистанционные/островные микросети обеспечивают надежную мощность для изолированных сообществ, военных баз и критической инфраструктуры. Они также помогают снизить зависимость от дизель-генераторов и ископаемого топлива, способствуя устойчивому использованию энергии. Технологические достижения в области хранения энергии и гибридных систем делают эти микросети более надежными и экономически эффективными.

• Предлагая

На основе предложения европейский рынок микросетей сегментирован на аппаратное обеспечение, программное обеспечение и услуги. Сегмент аппаратного обеспечения занимал самую большую долю рынка в 2025 году, чему способствовали значительные инвестиции в основные компоненты, такие как инверторы, контроллеры и системы хранения энергии, которые образуют основной физический слой установок микросетей. Надежность оборудования напрямую влияет на производительность, эффективность и долговечность микросетей. Рост крупномасштабных промышленных и институциональных микросетей еще больше повысил спрос на передовые аппаратные решения. Кроме того, интеграция с системами возобновляемых источников энергии сделала надежные аппаратные предложения критически важными для долгосрочной энергетической стабильности.

Ожидается, что в сегменте программного обеспечения будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, обусловленные растущим внедрением передовых платформ управления энергопотреблением и аналитических инструментов, повышающих операционную эффективность. Программные решения обеспечивают мониторинг в режиме реального времени, прогнозное обслуживание и интеллектуальную балансировку нагрузки. Они также облегчают бесшовную интеграцию с устройствами IoT, облачными платформами и интеллектуальными сетями. Растущий акцент на цифровизацию и удаленное управление микросетями еще больше ускоряет внедрение программного обеспечения.

• Вертикальный

На основе вертикали европейский рынок микросетей сегментирован на здравоохранение, образовательные учреждения, промышленные, военные и электрические предприятия. Промышленный сегмент занимал самую большую долю рынка в 2025 году, чему способствовал высокий спрос на устойчивое и экономически эффективное электроснабжение в производственных подразделениях и тяжелой промышленности. Промышленные микросети обеспечивают бесперебойную работу, снижают затраты на энергию и повышают производительность. Они также имеют решающее значение для объектов с критическими процессами, которые не могут переносить перебои в подаче электроэнергии. Интеграция возобновляемых источников энергии в промышленные микросети поддерживает инициативы в области устойчивого развития и соблюдения нормативных требований.

Ожидается, что в сегменте здравоохранения будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, обусловленные критической потребностью в бесперебойной электроэнергии в больницах и медицинских учреждениях. Микросети здравоохранения обеспечивают непрерывную работу жизненно важного оборудования и критически важных ИТ-систем. Повышение осведомленности об энергетической устойчивости и готовности к стихийным бедствиям заставляет больницы внедрять гибридные и резервные решения для микросетей. Кроме того, регуляторная поддержка и стимулы для интеграции возобновляемых источников энергии в медицинских учреждениях поддерживают рост сегмента. Дистанционный мониторинг и интеллектуальные системы управления энергопотреблением еще больше повышают надежность работы.

• Источник энергии

На основе источника энергии европейский рынок микросетей сегментирован на природный газ, комбинированное тепло и энергию, дизельное топливо, солнечную энергию, топливные элементы и другие. Сегмент природного газа занимал самую большую долю рынка в 2025 году благодаря своей надежности, установленному использованию в распределенной генерации и способности обеспечивать стабильную мощность. Микросети природного газа являются экономически эффективными, масштабируемыми и пригодными для промышленного и коммерческого применения. Они обеспечивают более низкие выбросы по сравнению с обычными дизельными системами. Сегмент выигрывает от зрелой инфраструктуры, широкой доступности и высокой операционной эффективности.

Ожидается, что в сегменте солнечной энергии будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, обусловленные падением затрат на солнечную фотоэлектрическую энергию, политикой поддержки возобновляемых источников энергии и усилением интеграции с системами хранения аккумуляторов. Солнечные микросети обеспечивают чистые, устойчивые энергетические решения, одновременно снижая зависимость от ископаемого топлива. Они особенно подходят для отдаленных районов, кампусов и жилых районов. Достижения в области технологий хранения и интеллектуальных контроллеров еще больше повышают эффективность и надежность солнечных микросетей. Растущая экологическая осведомленность и чистые нулевые энергетические цели ускоряют внедрение солнечной энергии в микросетях.

В каком регионе находится наибольшая доля европейского рынка микросетей

- Германия доминировала на европейском рынке микросетей с самой большой долей доходов в 2025 году, чему способствовали твердые обязательства правительства по декарбонизации, энергоэффективности и стабильности сетей, которые поощряют внедрение локализованных энергетических систем. Обширная промышленная база страны и передовые инициативы по интеграции возобновляемых источников энергии стимулируют спрос на устойчивые и гибкие энергетические решения.

- Развертывание микросетей в Германии часто сосредоточено на коммерческих кластерах, университетских кампусах и пилотных проектах, которые оптимизируют управление энергопотреблением и сокращают выбросы.

- Кроме того, поддерживающая нормативно-правовая база и политика в области интеллектуальных сетей еще больше укрепляют лидерство Германии на европейском рынке микросетей.

Британская Microgrid Market Insight

Рынок микросетей в Великобритании является самым быстрорастущим в Европе, чему способствует ускорение выполнения обязательств по достижению нулевых целевых показателей в области энергетики и интеграция распределенной возобновляемой генерации. Переход страны к низкоуглеродным энергетическим системам стимулирует инвестиции в коммерческие и городские проекты микросетей, которые повышают устойчивость и управляют пиковыми нагрузками. Государственные стимулы и мандаты в области устойчивого развития побуждают предприятия и учреждения внедрять интеллектуальные технологии управления энергопотреблением. Кроме того, растущие затраты на энергию и волатильность повышают интерес к локализованным системам генерации, хранения и сетевого взаимодействия, стимулируя быстрый рост рынка в секторе макросетей Великобритании.

Какова доля рынка микросетей в Европе

Индустрия микросетей в Европе в основном управляется хорошо зарекомендовавшими себя компаниями, в том числе:

•Siemens AG (Германия)

ABB Ltd (Швейцария)

•Schneider Electric SE (Франция)

Rolls-Royce plc (Великобритания)

Norvento Enerxía (Испания)

•InnoVentum (Швеция)

• E.ON SE (Германия)

SMA Solar Technology AG (Германия)

Independent Power Corporation PLC (Великобритания)

•Spirae LLC (Великобритания)

Victron Energy (Нидерланды)

Хранение фрактальной энергии (Италия)

Ampd Energy (Швейцария)

Korindo Energy Europe (Испания)

Green Eagle Solutions (Германия)

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.