Europe Ostomy Devices Market

Размер рынка в млрд долларов США

CAGR :

%

USD

2.11 Billion

USD

3.81 Billion

2025

2033

USD

2.11 Billion

USD

3.81 Billion

2025

2033

| 2026 –2033 | |

| USD 2.11 Billion | |

| USD 3.81 Billion | |

| % | |

|

Europe Ostomy Devices Market Segmentation, By Product (Bags and Accessories), Surgery Type (Ileostomy Drainage Bags, Colostomy Drainage Bags, and Urostomy Drainage Bags), Shape of Skin Barrier (Flat and Convex), System Type (One-piece System and Two-piece System), End User (Ambulatory Surgical Centers, Hospitals, Home Care, and Others) - Industry Trends and Forecast to 2033

Europe Ostomy Devices Market Size

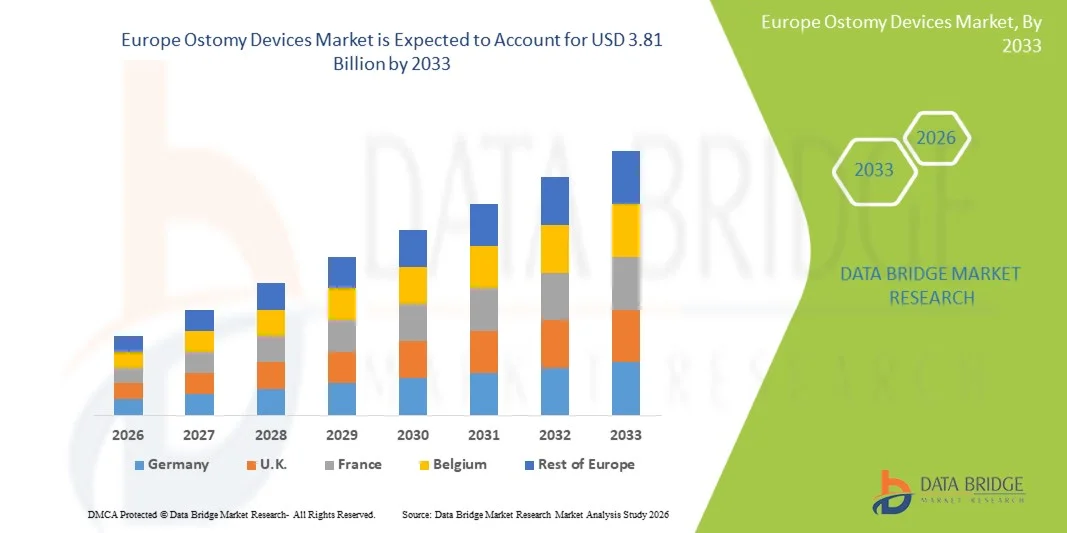

- The Europe Ostomy Devices Market size was valued at USD 2.11 billion in 2025 and is expected to reach USD 3.81 billion by 2033, at a CAGR of 7.70% during the forecast period

- The market growth is largely fueled by the increasing prevalence of gastrointestinal disorders, colorectal cancer, and other conditions requiring ostomy surgeries, leading to a rising demand for effective ostomy devices in both hospital and homecare settings

- Furthermore, growing awareness of post-surgical care, advancements in ostomy device design for enhanced comfort, and the rising preference for convenient, user-friendly, and skin-friendly solutions are establishing modern ostomy devices as essential tools in patient care. These converging factors are accelerating the uptake of ostomy devices solutions, thereby significantly boosting the market growth

Europe Ostomy Devices Market Analysis

- Ostomy devices, including colostomy, ileostomy, and urostomy appliances, are increasingly vital in modern healthcare due to their role in improving post-surgical quality of life, enhancing patient comfort, and enabling better management of gastrointestinal and urinary conditions

- The escalating demand for ostomy devices is primarily driven by the rising prevalence of colorectal cancer, inflammatory bowel disease, and other conditions requiring ostomy procedures, along with growing awareness of post-operative care and preference for user-friendly, skin-friendly, and discreet solutions

- The U.K. dominated the Europe Ostomy Devices Market with the largest revenue share of approximately 38.7% in 2025, supported by advanced healthcare infrastructure, high patient awareness, and the presence of leading manufacturers and distributors in the region

- Germany is expected to be the fastest-growing region in the Europe Ostomy Devices Market during the forecast period, with a projected growth rate of 8.3% CAGR, driven by increasing adoption of modern ostomy care solutions, government healthcare initiatives, and rising geriatric populations

- The Bags segment dominated the largest market revenue share of 56.8% in 2025, driven by high adoption among patients requiring long-term ostomy care

Report Scope and Europe Ostomy Devices Market Segmentation

|

Attributes |

Ostomy Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

• ConvaTec Group Plc (U.K.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Ostomy Devices Market Trends

“Rising Adoption of Advanced and User-Friendly Ostomy Solutions”

- A prominent trend in the global Europe Ostomy Devices Market is the increasing adoption of advanced, easy-to-use, and patient-centric products

- This includes innovations such as lightweight pouches, skin-friendly adhesives, odor-control technology, and customizable barrier options, which improve patient comfort and quality of life

- For instance, in 2024, Hollister Incorporated introduced a new line of closed ostomy pouches with advanced hydrocolloid skin barriers, providing better adhesion and reducing skin irritation for long-term users. Such innovations are helping patients manage their conditions more discreetly and confidently

- The trend is further supported by growing awareness among patients and healthcare providers about the importance of ostomy care and post-operative rehabilitation. Patient education programs and digital platforms offering guidance on ostomy management are contributing to informed product choices and increasing adoption

- In addition, the rise of home healthcare services and telemedicine has encouraged the use of portable and convenient ostomy solutions, enabling patients to maintain their daily activities with minimal disruption

Europe Ostomy Devices Market Dynamics

Driver

“Increasing Prevalence of Gastrointestinal Disorders and Post-Surgical Needs”

- The growing prevalence of colorectal cancer, inflammatory bowel disease (IBD), Crohn’s disease, and other gastrointestinal conditions is a key driver for the Europe Ostomy Devices Market

- A higher number of surgeries, including colostomy, ileostomy, and urostomy procedures, leads to rising demand for quality ostomy care products

- For instance, in 2025, the National Health Service (NHS) in the U.K. reported a significant rise in colorectal surgeries, driving the need for advanced ostomy pouches, skin barriers, and support accessories. Manufacturers are responding with a range of products tailored to different patient needs, including pediatric, adult, and elderly populations

- Furthermore, improved post-operative care protocols and enhanced awareness of ostomy maintenance practices are encouraging patients to adopt modern and specialized ostomy devices. This ensures better hygiene, reduced complications, and improved overall outcomes

- The increasing role of healthcare providers and patient support programs, including counseling and home delivery of ostomy supplies, is further fueling market growth by making these devices more accessible and convenient for patients

Restraint/Challenge

“High Costs and Limited Awareness in Emerging Markets”

- Despite market growth, the relatively high cost of premium ostomy devices can limit adoption, particularly in developing countries or among price-sensitive patients. Advanced features such as odor-control systems, extended wear adhesives, and specialized barriers often come at a higher price point compared to standard products

- For instance, a study conducted in 2024 across Southeast Asia indicated that many patients opted for basic ostomy solutions due to affordability concerns, despite the availability of more advanced devices

- Limited awareness about proper ostomy care and product options in emerging regions is another challenge. Patients may lack access to trained healthcare professionals, educational resources, or supportive post-surgical guidance, which can affect compliance and satisfaction

- Addressing these challenges requires the development of cost-effective ostomy devices, patient education campaigns, and partnerships between healthcare providers and manufacturers to increase accessibility. Initiatives such as low-cost pouch programs and community-based training sessions are helping overcome these barriers and supporting long-term market growth

- Regulatory challenges and variations in reimbursement policies across different countries can also restrict market penetration, requiring manufacturers to navigate complex compliance and pricing frameworks to expand globally

Europe Ostomy Devices Market Scope

The market is segmented on the basis of product, surgery type, shape of skin barrier, system type, and end-user.

• By Product

On the basis of product, the Europe Ostomy Devices Market is segmented into Bags and Accessories. The Bags segment dominated the largest market revenue share of 56.8% in 2025, driven by high adoption among patients requiring long-term ostomy care. Bags are essential for daily waste collection, and their quality and comfort directly affect patient compliance and satisfaction. The segment benefits from innovations such as odor control, leak-proof designs, and skin-friendly materials. Increasing prevalence of colorectal cancer, inflammatory bowel disease, and urinary diversion surgeries supports consistent demand. The availability of pre-cut and customizable bags enhances usability for patients. Rising awareness and patient education programs contribute to segment growth. Technological improvements in adhesion and durability further strengthen adoption. Hospitals and home care providers prefer reliable bag systems for patient safety. Continuous advancements in patient-centric designs maintain market dominance. Overall, the Bags segment remains the backbone of ostomy care products.

The Accessories segment is expected to witness the fastest CAGR of 18.9% from 2026 to 2033, fueled by growing demand for supplementary products such as barrier rings, adhesives, skin protectants, and cleansing wipes. Accessories improve patient comfort and reduce complications such as skin irritation and leakage. The segment benefits from increasing patient awareness and recommendations from healthcare professionals. Expansion of home care services and outpatient facilities further supports growth. Innovative accessory kits combining multiple products enhance convenience. Rising adoption of personalized care routines accelerates demand. Accessibility through online and retail channels also contributes to segment expansion. Growing use of accessories for post-operative care strengthens market potential. Continuous R&D in skin-friendly materials promotes adoption. Increasing chronic disease prevalence drives long-term accessory consumption. Overall, this segment is expected to grow rapidly over the forecast period.

• By Surgery Type

On the basis of surgery type, the Europe Ostomy Devices Market is segmented into Ileostomy Drainage Bags, Colostomy Drainage Bags, and Urostomy Drainage Bags. The Colostomy Drainage Bags segment held the largest market revenue share of 44.3% in 2025, driven by the high prevalence of colorectal cancer and diverticulitis requiring colostomy procedures. Colostomy bags are widely used due to their efficiency in managing fecal output and minimizing skin complications. The segment benefits from technological innovations in bag adhesion, odor control, and comfort. Hospital adoption and home care programs enhance market penetration. Standardized product designs and availability in multiple sizes further support growth. Rising patient education and support programs contribute to segment adoption. Healthcare professionals prioritize reliable and easy-to-use colostomy systems. Increasing surgical procedures globally strengthen the segment. Patients prefer discreet and comfortable designs, driving demand. Continuous innovation and product awareness maintain dominance.

The Ileostomy Drainage Bags segment is expected to witness the fastest CAGR of 19.4% from 2026 to 2033, fueled by increasing cases of Crohn’s disease, ulcerative colitis, and bowel obstruction surgeries. Ileostomy procedures are increasingly performed due to early diagnosis and surgical advancements. The segment benefits from improved bag systems that reduce leakage and enhance patient comfort. Rising awareness among patients and caregivers supports adoption. Hospitals and home care centers are expanding support for post-operative care. Technological improvements in lightweight and discreet designs enhance usability. The growing number of outpatient surgeries increases demand. Personalized care plans drive accessory and bag sales. Advancements in one-piece and two-piece systems further enhance adoption. Continuous R&D in patient-centric solutions accelerates growth.

• By Shape of Skin Barrier

On the basis of shape of skin barrier, the Europe Ostomy Devices Market is segmented into Flat and Convex. The Flat skin barrier segment accounted for the largest market revenue share of 52.6% in 2025, driven by its suitability for patients with normal peristomal contours and ease of application. Flat barriers are preferred due to their comfort, affordability, and compatibility with most bag systems. Hospitals and home care providers often recommend flat barriers for routine ostomy management. The segment benefits from widespread availability in multiple sizes and materials. Patient preference for lightweight and discreet designs enhances adoption. Growing number of post-operative care programs contributes to segment demand. Technological improvements in adhesive quality support skin health. Education on proper barrier selection ensures consistent usage. Healthcare providers recommend flat barriers for new ostomy patients. Overall, flat barriers maintain strong market dominance.

The Convex skin barrier segment is expected to witness the fastest CAGR of 20.2% from 2026 to 2033, fueled by the growing number of patients with retracted or uneven peristomal surfaces requiring additional support. Convex barriers improve adhesion and minimize leakage, ensuring better patient comfort. The segment benefits from technological advancements in flexible and skin-friendly convex designs. Increased awareness among surgeons and patients supports adoption. Hospitals and home care services are increasingly using convex barriers for complex cases. Product innovations such as adjustable convexity enhance usability. Rising chronic disease prevalence drives long-term demand. Patient education and support programs contribute to growth. Improved clinical outcomes strengthen market preference. Overall, convex barriers are projected to grow rapidly during the forecast period.

• By System Type

On the basis of system type, the Europe Ostomy Devices Market is segmented into One-piece System and Two-piece System. The One-piece system segment dominated the largest market revenue share of 49.1% in 2025, driven by ease of use and lightweight design suitable for new ostomy patients. One-piece systems integrate the bag and skin barrier, reducing application complexity and enhancing patient comfort. The segment benefits from technological innovations in adhesives and odor control. Hospitals and home care providers often recommend one-piece systems for routine management. Availability in multiple sizes supports adoption. Patient preference for discreet and convenient products strengthens demand. Continuous R&D in product comfort maintains market dominance. Training programs for patients and caregivers further encourage usage. Widespread adoption in outpatient care supports growth. Overall, one-piece systems remain the preferred choice for many patients.

The Two-piece system segment is expected to witness the fastest CAGR of 19.7% from 2026 to 2033, fueled by the flexibility of changing bags without removing the skin barrier, reducing skin irritation. Two-piece systems are preferred for patients requiring frequent bag changes or with complex stomas. Technological advancements in coupling mechanisms enhance usability. Growing awareness among healthcare providers supports adoption. Hospitals and home care programs increasingly recommend two-piece systems for long-term care. Customizable options increase patient satisfaction. Rising post-operative care procedures drive segment growth. Improved patient outcomes promote preference for two-piece systems. Expansion of specialty care centers accelerates adoption. Overall, this segment is expected to grow rapidly.

• By End-User

On the basis of end-user, the Europe Ostomy Devices Market is segmented into Ambulatory Surgical Centers, Hospitals, Home Care, and Others. The Hospitals segment dominated the largest market revenue share of 55.4% in 2025, driven by high patient inflow for ostomy surgeries and post-operative care. Hospitals provide comprehensive care, including patient education, product selection, and follow-up support, supporting strong product demand. The segment benefits from advanced procurement systems and bulk purchasing. Hospitals also drive adoption of new technologies such as one-piece and two-piece systems. Rising prevalence of colorectal and urinary tract conditions enhances utilization. Partnerships with manufacturers ensure consistent supply. Clinical guidelines recommending best-in-class devices support hospital adoption. Healthcare professional recommendations influence patient preference. Overall, hospitals remain the primary end-user segment.

The Home Care segment is expected to witness the fastest CAGR of 20.5% from 2026 to 2033, fueled by the increasing trend of post-operative care at home and patient preference for independent management. Home care adoption is supported by telemedicine consultations and caregiver training. Patients benefit from easy-to-use products and accessibility of supplies through retail and online channels. Rising awareness about ostomy care and comfort drives segment growth. Technological innovations such as lightweight and discreet products enhance home usability. Expansion of home healthcare services globally supports demand. Increasing chronic disease prevalence accelerates adoption. Home care monitoring systems complement product usage. The segment is expected to grow rapidly during the forecast period.

Europe Ostomy Devices Market Regional Analysis

- The Europe Ostomy Devices Market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by robust healthcare systems, increasing patient awareness, and government initiatives supporting post-operative care

- Urbanization and rising incidence of gastrointestinal diseases are also fueling demand for advanced ostomy solutions in both hospital and homecare settings. In 2025, Coloplast launched biodegradable ostomy pouches in Germany and France, providing improved comfort and sustainability, which was well-received by patients and healthcare providers

- The availability of training programs and patient education campaigns across Europe has further strengthened adoption

U.K. Europe Ostomy Devices Market Insight

The U.K. Europe Ostomy Devices Market dominated the European Europe Ostomy Devices Market with the largest revenue share of approximately 38.7% in 2025, supported by advanced healthcare infrastructure, high patient awareness, and a strong presence of leading manufacturers and distributors. For example, the National Health Service (NHS) partnered with major ostomy device manufacturers in 2025 to ensure timely access to modern ostomy pouches and accessories for post-operative patients. Government reimbursement policies and educational initiatives promoting proper ostomy care have significantly contributed to the adoption of modern devices, improving patient quality of life and post-operative outcomes.

Germany Europe Ostomy Devices Market Insight

The Germany Europe Ostomy Devices Market is expected to expand at 8.3% CAGR, during the forecast period, driven by increasing awareness of proper post-surgical care and the demand for technologically advanced and patient-friendly solutions. In 2025, B. Braun introduced specialized ostomy products for elderly patients, offering enhanced skin protection and comfort, which accelerated market uptake. Germany’s emphasis on healthcare innovation, robust hospital infrastructure, and the rising geriatric population are contributing to steady growth in the market.

Europe Ostomy Devices Market Share

The Ostomy Devices industry is primarily led by well-established companies, including:

• ConvaTec Group Plc (U.K.)

• Hollister Incorporated (U.S.)

• B. Braun S.E. (Germany)

• Hollister Limited (Canada)

• Marlen Manufacturing & Supply, Inc. (U.S.)

• Salts Healthcare Ltd. (U.K.)

• Nitto Denko Corporation (Japan)

• Medline Industries, Inc. (U.S.)

• Flexicare Medical Ltd. (U.K.)

• StomaSense Inc. (U.S.)

• Welland Medical Ltd. (U.K.)

• Omega Healthcare Ltd. (India)

Latest Developments in Europe Ostomy Devices Market

- In June 2021, Welland Medical Limited, a provider of ostomy care products, launched its Aurum Plus ostomy pouch range, offering closed, drainable, and urostomy options in various sizes focused on improved comfort and skin health for ostomates

- In February 2024, Coloplast A/S announced a distribution partnership with Medline Industries to expand the availability of its ostomy care product range across the United States, strengthening market reach and access for patient care

- In May 2024, Coloplast secured reimbursement approval in the UK for the Heylo digital leakage notification system — the world’s first sensor‑assisted solution designed to detect potential leakage early — and also expanded its SenSura Mio ostomy range with two new products, reinforcing its innovation pipeline under its Strive25 strategy

- In July 2024, Revel, an ostomy care brand, introduced its first product “It’s in the Bag”, a deodorizing lubricant developed with LiquiGlide technology to create self‑lubricating, slippery pouch surfaces that improve ease of use and odor control for ostomates

- In October 2024, Hollister Incorporated launched its Advanced Stomahesive Barrier line, featuring improved adhesion, longer wear time, and enhanced skin protection, addressing key user concerns around leakage and peristomal irritation

- In May 2025, Salts Healthcare Ltd secured a major contract with NHS England to supply a comprehensive range of ostomy care products — including pouches, barriers, and accessories — across the United Kingdom, expanding its commercial footprint in a major national healthcare system

- In August 2025, Coloplast reported continued strong organic growth in its SenSura Mio portfolio, with the convex and concave product variants driving revenue across Europe and the U.S., highlighting sustained market adoption of next‑generation ostomy care products

- In August 2025, global market analysis noted that manufacturers introduced over 1,300 new stoma care products between 2023 and 2025, including next‑generation pouches and accessories with hypoallergenic adhesives, odor‑control filters, and biodegradable materials to improve patient comfort and sustainability

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.