Global Adhesive Films Market

Размер рынка в млрд долларов США

CAGR :

%

USD

96.64 Billion

USD

149.78 Billion

2025

2033

USD

96.64 Billion

USD

149.78 Billion

2025

2033

| 2026 –2033 | |

| USD 96.64 Billion | |

| USD 149.78 Billion | |

| % | |

|

Global Adhesive Films Market Segmentation, By Film Material (Polypropylene (PP), Polyethylene (PE), Polyvinyl Chloride (PVC), and Others), Application (Tapes, Graphic Films, and Labels), End Use Industries (Packaging, Transportation, Electrical and Electronics, and Others) - Industry Trends and Forecast to 2033

What is the Global Adhesive Films Market Size and Growth Rate?

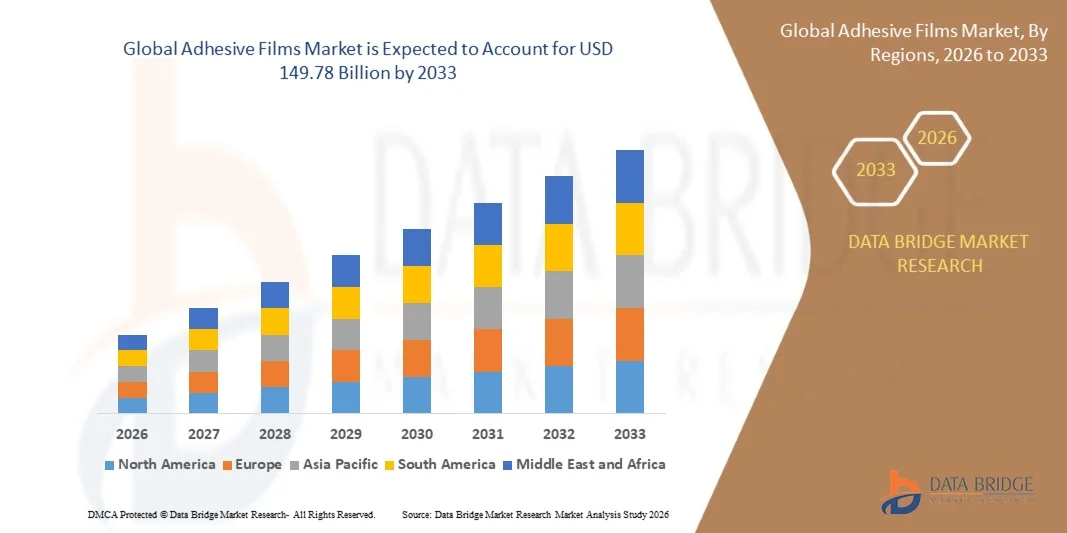

- The global adhesive films market size was valued at USD 96.64 billion in 2025 and is expected to reach USD 149.78 billion by 2033, at a CAGR of 5.63% during the forecast period

- The adhesive films market has witnessed significant growth driven by advancements in material science and increasing demand across various industries such as packaging, automotive, electronics, and healthcare. Adhesive films are widely used for applications including tapes, labels, and graphic films, offering superior bonding, durability, and flexibility compared to traditional adhesive methods

What are the Major Takeaways of Adhesive Films Market?

- The market is particularly bolstered by the increasing demand for lightweight, durable, and easy-to-apply adhesive solutions in sectors such as electronics, where adhesive films are essential in the production of smartphones, displays, and flexible circuits

- Key advancements in the market include the development of pressure-sensitive adhesive (PSA) films, which are gaining traction due to their ease of application and removal without damaging surfaces. Innovations in bio-based and eco-friendly adhesive films are also transforming the market, responding to growing sustainability concerns

- Asia-Pacific dominated the adhesive films market with a 48.36% revenue share in 2025, driven by strong growth in packaging, automotive, electrical and electronics, and industrial manufacturing activities across China, Japan, India, South Korea, and Southeast Asia

- North America is projected to register the fastest CAGR of 6.9% from 2026 to 2033, driven by increasing demand for sustainable packaging materials, rising EV production, and expanding adoption of specialty films in electronics and healthcare applications

- The Polypropylene (PP) segment dominated the market with a 38.7% share in 2025, as it remains the most widely used material owing to its excellent moisture resistance, durability, flexibility, and cost-effectiveness

Report Scope and Adhesive Films Market Segmentation

|

Attributes |

Adhesive Films Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Adhesive Films Market?

“Increasing Demand for Eco-Friendly Adhesive Films”

- A key trend in the adhesive films market is the increasing demand for eco-friendly adhesive films, driven by growing environmental concerns and the push for sustainability across industries

- Manufacturers are focusing on developing biodegradable and bio-based adhesive films that reduce the environmental impact of conventional plastic-based adhesives. For instance, H.B. Fuller, a leading company in the sector, launched the Swift Melt 1515-1, a bio-compatible adhesive for medical tape applications

- This shift is particularly evident in industries such as packaging, where eco-friendly adhesive films are used for food packaging and labels that meet sustainable regulations. In addition, in electronics, eco-friendly adhesive films are being utilized in the production of flexible circuits and displays, offering strong bonding while maintaining low environmental impact

- The push for more sustainable solutions, combined with innovations in material science, is helping shape the future of the adhesive films market, offering more environmentally responsible options without compromising on performance

What are the Key Drivers of Adhesive Films Market?

- As the global focus shifts toward sustainability, there is an increasing demand for eco-friendly products, including bio-based and biodegradable adhesive films. This growing concern over environmental impact is encouraging companies to innovate and adopt green solutions

- For instance, in the packaging industry, brands are turning to adhesive films made from renewable resources to reduce their carbon footprint. Companies such as H.B. Fuller have launched products such as Swift Melt 1515-1, a bio-compatible adhesive designed for medical applications in regions such as the Indian subcontinent

- This trend toward sustainable materials is driven by consumer demand and by regulatory pressures, with governments worldwide tightening restrictions on plastic usage and promoting eco-friendly alternatives

- The eco-conscious movement is therefore a significant market driver for adhesive films, as it pushes manufacturers to invest in materials that balance performance with environmental responsibility

Which Factor is Challenging the Growth of the Adhesive Films Market?

- The adhesive films market faces stiff competition from alternative bonding technologies such as liquid adhesives, heat sealing, and mechanical fasteners, each offering specific advantages in certain applications

- For instance, liquid adhesives can provide better coverage and flexibility in complex bonding scenarios, while heat sealing is often preferred in packaging applications for its speed and cost-effectiveness. Mechanical fasteners, such as screws or rivets, may be favored in industries such as automotive for their strength and reliability

- Despite these alternatives, adhesive films still present a market opportunity for growth, particularly in industries where precise, thin, and uniform bonding is critical

- As technology evolves, adhesive films can be developed to compete more effectively, offering enhanced features such as faster curing times, stronger adhesion, or improved environmental resistance

- For instance, the growing demand for automotive lightweighting and electronic devices with compact designs presents an opportunity for adhesive films to offer superior performance over bulkier mechanical fasteners or other bonding technologies

How is the Adhesive Films Market Segmented?

The market is segmented on the basis of film material, application, and end-use industries.

• By Film Material

On the basis of film material, the adhesive films market is segmented into Polypropylene (PP), Polyethylene (PE), Polyvinyl Chloride (PVC), and Others. The Polypropylene (PP) segment dominated the market with a 38.7% share in 2025, as it remains the most widely used material owing to its excellent moisture resistance, durability, flexibility, and cost-effectiveness. PP-based adhesive films are extensively used in packaging, labeling, lamination, and industrial bonding applications due to their strong adhesion properties and compatibility with multiple substrates. Their lightweight nature and recyclability further support strong demand across consumer goods and logistics applications.

The Polyethylene (PE) segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by rising adoption in flexible packaging, protective films, and electrical insulation applications. Increasing demand for lightweight, chemical-resistant, and high-performance films in packaging and electronics is further accelerating segment growth globally.

• By Application

On the basis of application, the market is segmented into Tapes, Graphic Films, and Labels. The Tapes segment dominated the market with a 42.1% share in 2025, supported by extensive usage across packaging, automotive assembly, construction, and industrial bonding applications. Adhesive film tapes are widely preferred for sealing, masking, surface protection, insulation, and structural bonding due to their superior adhesion strength and ease of application. Growing demand from e-commerce packaging and industrial manufacturing continues to strengthen segment leadership.

The Labels segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing use in food & beverage packaging, pharmaceuticals, retail products, and logistics tracking. Rising demand for smart labeling, barcode integration, tamper-evident packaging, and high-quality printing solutions is further boosting the adoption of adhesive film labels across global markets.

• By End Use Industries

On the basis of end-use industries, the adhesive films market is segmented into Packaging, Transportation, Electrical and Electronics, and Others. The Packaging segment dominated the market with a 45.6% share in 2025, driven by strong demand for flexible packaging solutions, product labeling, sealing applications, and protective wrapping across food, consumer goods, and healthcare products. Increasing growth in e-commerce and retail logistics has significantly supported the use of adhesive films in secure packaging applications.

The Electrical and Electronics segment is expected to grow at the fastest CAGR from 2026 to 2033, propelled by increasing demand for insulation films, protective laminates, display bonding, and circuit board applications. Rising production of consumer electronics, EV components, semiconductors, and smart devices is driving strong adoption of advanced adhesive films in the global electronics industry.

Which Region Holds the Largest Share of the Adhesive Films Market?

- Asia-Pacific dominated the adhesive films market with a 48.36% revenue share in 2025, driven by strong growth in packaging, automotive, electrical and electronics, and industrial manufacturing activities across China, Japan, India, South Korea, and Southeast Asia. The region continues to benefit from rapid industrialization, expanding flexible packaging demand, and increasing use of high-performance bonding solutions in consumer electronics and transportation applications

- Leading companies in Asia-Pacific are introducing advanced adhesive film solutions with enhanced thermal resistance, moisture protection, UV stability, and lightweight bonding capabilities, strengthening the region’s technological advantage. Continuous investment in packaging innovation, EV manufacturing, and electronics production drives long-term market expansion

- Strong manufacturing ecosystems, availability of raw materials, cost-efficient production facilities, and sustained industrial investment further reinforce regional market leadership

China Adhesive Films Market Insight

China is the largest contributor in Asia-Pacific, supported by its world-leading manufacturing capacity in packaging, electronics, automotive components, and industrial materials. Rising demand for protective films, labels, tapes, and specialty adhesive solutions across consumer goods and EV applications continues to drive market growth. Strong domestic production capabilities and government-backed industrial development initiatives further strengthen demand.

Japan Adhesive Films Market Insight

Japan contributes significantly to regional growth, driven by advanced electronics manufacturing, automotive innovation, and precision industrial applications. Increasing use of adhesive films in display panels, semiconductor packaging, automotive interiors, and high-performance insulation materials supports steady market expansion.

India Adhesive Films Market Insight

India is emerging as a major growth hub, driven by rapid expansion in food packaging, retail labeling, construction materials, and automotive manufacturing. Rising e-commerce activity and increasing demand for flexible packaging solutions are significantly boosting the adoption of adhesive films across the country.

South Korea Adhesive Films Market Insight

South Korea contributes significantly due to strong demand from semiconductors, display technologies, EV batteries, and consumer electronics. Rapid development in high-performance electronics and smart manufacturing continues to accelerate the need for advanced adhesive film solutions.

North America Adhesive Films Market

North America is projected to register the fastest CAGR of 6.9% from 2026 to 2033, driven by increasing demand for sustainable packaging materials, rising EV production, and expanding adoption of specialty films in electronics and healthcare applications. Strong innovation in adhesive technologies and growing investments in high-performance industrial materials are expected to accelerate regional growth.

U.S. Adhesive Films Market Insight

The U.S. is the largest contributor in North America, supported by strong demand from packaging, automotive, aerospace, and electronics industries. Increasing use of lightweight bonding materials in EVs, advanced electronics, and medical devices is intensifying demand for adhesive films. Presence of major manufacturers such as 3M, DOW, and H.B. Fuller further drives market growth.

Canada Adhesive Films Market Insight

Canada contributes significantly to regional growth, driven by rising demand for industrial packaging, construction materials, and automotive components. Increasing adoption of sustainable film solutions and expanding industrial manufacturing capabilities continue to support market penetration across the country.

Which are the Top Companies in Adhesive Films Market?

The adhesive films industry is primarily led by well-established companies, including:

- Master Bond (U.S.)

- NuSil (U.S.)

- Axiom Materials, Inc. (U.S.)

- Parker Hannifin Corp (U.S.)

- Bondline Electronics Ltd (U.K.)

- AI Technology, Inc. (U.S.)

- Gurit Services AG (Switzerland)

- Galp (Portugal)

- Marathon Petroleum Corporation (U.S.)

- Devson Catalyst (India)

- GLOBAL PRECISION BALL AND ROLLER (U.S.)

- Idemitsu Kosan Co., Ltd. (Japan)

- H.B. Fuller Company (U.S.)

- DOW (U.S.)

- 3M (U.S.)

- Solvay (Belgium)

- Henkel AG & Co. KGaA (Germany)

- Nitto Denko Corporation (Japan)

- L&L Products (U.S.)

What are the Recent Developments in Global Adhesive Films Market?

- In July 2024, Phytonics, a Germany-based startup, developed an innovative self-adhesive film featuring microstructured surfaces designed to reduce glare on photovoltaic (PV) modules. The product is available in both sheet and roll formats and is suitable for integration into new as well as existing solar PV systems. This development is expected to support the growing adoption of high-performance adhesive films in renewable energy applications and improve solar panel efficiency

- In April 2024, BASF signed a Letter of Intent (LoI) with Youyi Group to strengthen the strategic partnership between the two companies. The agreement focuses on the supply of butyl acrylate (BA) and 2-ethylhexyl acrylate (2-EHA) from BASF’s Zhanjiang Verbund site to address rising demand in China’s adhesive materials industry. This collaboration is such asly to reinforce BASF’s regional supply capabilities and support market growth in Asia-Pacific

- In May 2023, H.B. Fuller Company announced the completion of its acquisition of U.K.-based family-owned adhesive manufacturer Beardow Adams. The acquisition expanded H.B. Fuller’s sales presence across more than 70 countries and strengthened access to over 20,000 end-user applications. This strategic move is expected to enhance the company’s global market reach and strengthen its position in the adhesive films industry

- In April 2023, Resonac Corporation announced the expansion of its adhesive film production capacity for semiconductor packaging in Japan. The expansion aims to meet growing demand from advanced electronics and semiconductor manufacturing applications. This capacity enhancement is anticipated to support rising demand from the electronics sector and accelerate market growth in high-performance adhesive films

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.