Global Application Release Automation Ara Market

Размер рынка в млрд долларов США

CAGR :

%

USD

6.21 Billion

USD

26.19 Billion

2025

2033

USD

6.21 Billion

USD

26.19 Billion

2025

2033

| 2026 –2033 | |

| USD 6.21 Billion | |

| USD 26.19 Billion | |

| % | |

|

Global Application Release Automation (ARA) Market Segmentation, By Component (Solutions and Services), Organization Size (Large Enterprise and SMEs), Deployment Type (Cloud and On-Premises), Vertical (Healthcare, Media and Entertainment, Manufacturing, Retail & Consumer Goods and Consumer Goods, ITES and Telecommunications, Banking, Financial Services, and Insurance, and Others), Model (Software Prototyping, Incremental Model, Agile Model, Waterfall Model, and Spiral Model) - Industry Trends and Forecast to 2033

What is the Global Application Release Automation (ARA) Market Size and Growth Rate?

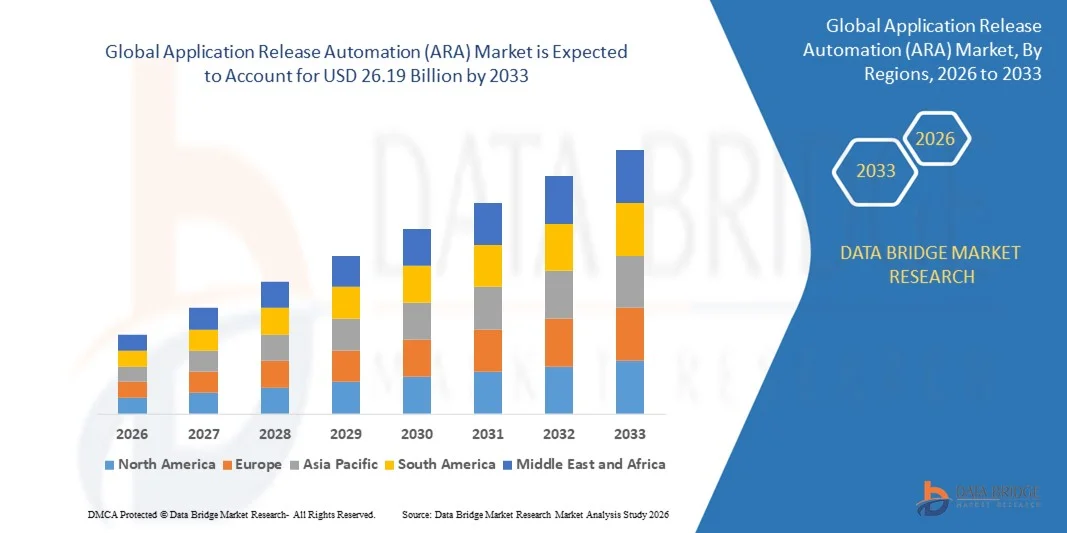

- The global application release automation (ARA) market size was valued at USD 6.21 billion in 2025 and is expected to reach USD 26.19 billion by 2033, at a CAGR of 19.70% during the forecast period

- Rise in the numerous applications running in dynamic It environment is a crucial factor accelerating the market growth, also rise in the optimized resource utilization, increase in the demand for application release automation market, increase in the user engagement over digital platforms, growing focus on competitive intelligence, together and rise in the need to improve the audience experience are the major factors among others boosting the application release automation (ARA) market

What are the Major Takeaways of Application Release Automation (ARA) Market?

- Rise in the advancements in AI and its use in application development and cloud-based platforms creating a favourable environment for application development will further create new opportunities for application release automation (ARA) market

- However, heavy dependence on legacy processes acts as the major factors among others restraining the market growth, and will further challenge the application release automation (ARA) market

- North America dominated the application release automation (ARA) market with a 41.6% revenue share in 2025, driven by rapid adoption of DevOps practices, cloud-native development, and large-scale digital transformation initiatives across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 9.62% from 2026 to 2033, fueled by expanding IT services industries, rapid cloud adoption, and strong growth in digital banking, e-commerce, and telecom infrastructure across China, Japan, India, South Korea, and Southeast Asia

- The Solutions segment dominated the market with a 68.5% share in 2025, as enterprises increasingly adopt integrated ARA platforms to automate deployment pipelines, manage release workflows, and ensure compliance across hybrid IT environments

Report Scope and Application Release Automation (ARA) Market Segmentation

|

Attributes |

Application Release Automation (ARA) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Application Release Automation (ARA) Market?

Accelerating Adoption of Cloud-Native, DevOps-Integrated, and AI-Driven Release Automation Platforms

- The application release automation (ARA) market is witnessing strong adoption of cloud-native, containerized, and microservices-based deployment platforms designed to support DevOps pipelines, Kubernetes environments, and hybrid IT infrastructures

- Vendors are introducing AI-powered orchestration, policy-driven automation, and low-code workflow capabilities that enhance deployment speed, reduce manual intervention, and improve release consistency across multi-cloud ecosystems

- Growing demand for faster time-to-market, continuous integration/continuous deployment (CI/CD), and zero-downtime releases is accelerating enterprise transition from manual release management to automated solutions

- For instance, companies such as IBM, Microsoft, Red Hat, Inc., and CloudBees, Inc. are enhancing their ARA platforms with Kubernetes integration, GitOps workflows, and advanced analytics

- Increasing complexity of distributed applications, API-driven architectures, and multi-environment deployments is driving demand for scalable and centralized automation frameworks

- As enterprises prioritize digital transformation, ARA platforms will remain essential for streamlined software delivery, compliance enforcement, and operational agility

What are the Key Drivers of Application Release Automation (ARA) Market?

- Rising adoption of DevOps practices, agile development methodologies, and CI/CD pipelines is significantly boosting demand for automated release management solutions

- For instance, in 2025, leading companies such as VMware, Inc., Digital.ai, and Progress Software Corporation expanded their automation capabilities with enhanced security controls, multi-cloud deployment support, and real-time monitoring tools

- Growing deployment of hybrid cloud, SaaS platforms, and enterprise applications across banking, telecom, healthcare, and retail sectors is accelerating ARA adoption globally

- Advancements in AI-driven testing, automated rollback mechanisms, configuration management, and compliance tracking have strengthened release reliability and reduced operational risks

- Increasing focus on application modernization, container orchestration, and infrastructure-as-code (IaC) is creating strong demand for integrated automation tools

- Supported by steady enterprise IT spending, digital innovation initiatives, and cybersecurity compliance requirements, the ARA market is expected to witness sustained long-term growth

Which Factor is Challenging the Growth of the Application Release Automation (ARA) Market?

- High implementation and integration costs associated with enterprise-grade ARA platforms limit adoption among small and mid-sized organizations

- For instance, during 2024–2025, enterprises reported increased spending on cloud infrastructure, cybersecurity compliance, and DevOps tooling, impacting overall IT budget allocation for automation solutions

- Complexity in integrating ARA platforms with legacy systems, multi-cloud environments, and diverse toolchains increases deployment challenges

- Shortage of skilled DevOps engineers and automation specialists slows effective implementation and optimization

- Competition from open-source CI/CD tools and native cloud deployment services creates pricing pressure and reduces differentiation among vendors

- To address these challenges, companies are focusing on subscription-based pricing models, simplified user interfaces, AI-assisted deployment workflows, and enhanced interoperability, thereby improving accessibility and global adoption of Application Release Automation (ARA) solutions

How is the Application Release Automation (ARA) Market Segmented?

The market is segmented on the basis of component, organization size, deployment type, vertical, and model.

- By Component

On the basis of component, the application release automation (ARA) market is segmented into Solutions and Services. The Solutions segment dominated the market with a 68.5% share in 2025, as enterprises increasingly adopt integrated ARA platforms to automate deployment pipelines, manage release workflows, and ensure compliance across hybrid IT environments. These solutions provide centralized dashboards, automated rollback capabilities, environment provisioning, and DevOps toolchain integration, making them essential for large-scale digital transformation initiatives. Strong demand for CI/CD orchestration, Kubernetes deployment automation, and multi-cloud release management further strengthens segment leadership.

The Services segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising demand for consulting, implementation, managed services, and training support. As organizations modernize legacy systems and migrate to cloud-native architectures, service providers play a critical role in customization, integration, and ongoing optimization of ARA platforms.

- By Organization Size

On the basis of organization size, the market is segmented into Large Enterprises and SMEs. The Large Enterprises segment dominated the market with a 61.2% share in 2025, supported by complex IT infrastructures, multi-region deployment environments, and high software release frequency. Large organizations require advanced automation tools to manage microservices, ensure governance compliance, and reduce downtime risks. Strong investments in DevOps transformation and cybersecurity compliance further drive ARA adoption among global enterprises.

The SMEs segment is expected to grow at the fastest CAGR from 2026 to 2033, fueled by increasing availability of subscription-based, cloud-hosted ARA platforms. Growing awareness of automation benefits, cost-efficient SaaS deployment models, and rising digital adoption among mid-sized firms are accelerating market penetration within this segment.

- By Deployment Mode

On the basis of deployment mode, the application release automation (ARA) market is segmented into Cloud and On-Premises. The Cloud segment dominated the market with a 57.8% share in 2025, driven by rapid adoption of SaaS-based DevOps tools, scalability advantages, lower upfront costs, and seamless integration with public and hybrid cloud infrastructures. Cloud deployment enables faster implementation, automated updates, and remote accessibility, making it the preferred option for modern enterprises.

The On-Premises segment is projected to grow at a steady pace, particularly among regulated industries requiring strict data control and security compliance. However, cloud-based ARA platforms are expected to register the fastest growth from 2026 to 2033 due to accelerating enterprise cloud migration strategies.

- By Vertical

On the basis of vertical, the market is segmented into Healthcare; Media and Entertainment; Manufacturing; Retail & Consumer Goods; ITES and Telecommunications; Banking, Financial Services, and Insurance (BFSI); and Others. The ITES and Telecommunications segment dominated the market with a 29.6% share in 2025, supported by continuous software updates, network virtualization, and rapid service deployment requirements. Telecom operators and IT service providers rely heavily on automated release pipelines to maintain uptime and manage large-scale distributed applications.

The Banking, Financial Services, and Insurance (BFSI) segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by digital banking transformation, regulatory compliance mandates, cybersecurity requirements, and high transaction-based application updates.

- By Model

On the basis of model, the application release automation (ARA) market is segmented into Software Prototyping, Incremental Model, Agile Model, Waterfall Model, and Spiral Model. The Agile Model segment dominated the market with a 46.4% share in 2025, as organizations increasingly adopt agile and DevOps practices to enable continuous integration and rapid release cycles. Agile methodologies require automated testing, deployment, and rollback mechanisms, making ARA tools indispensable for iterative development.

The Incremental Model segment is projected to grow at the fastest CAGR from 2026 to 2033, supported by enterprises transitioning from traditional waterfall structures to phased, modular software delivery approaches. Increasing emphasis on flexibility, reduced risk, and faster feature rollouts continues to accelerate adoption across development teams globally.

Which Region Holds the Largest Share of the Application Release Automation (ARA) Market?

- North America dominated the application release automation (ARA) market with a 41.6% revenue share in 2025, driven by rapid adoption of DevOps practices, cloud-native development, and large-scale digital transformation initiatives across the U.S. and Canada. High concentration of enterprise IT firms, SaaS providers, fintech companies, and telecom operators continues to fuel demand for automated release orchestration and CI/CD pipeline optimization

- Leading companies such as IBM, Microsoft, and Red Hat, Inc. are expanding AI-driven deployment automation, Kubernetes-native release tools, and multi-cloud integration capabilities, strengthening the region’s technological leadership

- Strong venture capital funding, high enterprise IT spending, mature cloud infrastructure, and advanced cybersecurity frameworks further reinforce North America’s market dominance

U.S. Application Release Automation (ARA) Market Insight

The U.S. represents the largest contributor within North America, supported by widespread implementation of DevOps pipelines, hybrid cloud environments, and microservices architectures across BFSI, healthcare, retail, and telecom sectors. Increasing adoption of AI-enabled monitoring, automated rollback systems, and infrastructure-as-code practices intensifies demand for advanced ARA platforms. Presence of major cloud service providers, enterprise software innovators, and strong startup ecosystems accelerates continuous innovation and large-scale deployment automation adoption.

Canada Application Release Automation (ARA) Market Insight

Canada contributes significantly to regional growth, driven by rising investment in digital government services, fintech platforms, and telecom modernization. Growing focus on secure software deployment, compliance management, and automated testing strengthens demand for ARA solutions. Supportive regulatory frameworks, skilled DevOps professionals, and expanding cloud adoption further enhance market penetration across enterprises and public-sector organizations.

Asia-Pacific Application Release Automation (ARA) Market

Asia-Pacific is projected to register the fastest CAGR of 9.62% from 2026 to 2033, fueled by expanding IT services industries, rapid cloud adoption, and strong growth in digital banking, e-commerce, and telecom infrastructure across China, Japan, India, South Korea, and Southeast Asia. Rising demand for faster application delivery cycles and scalable multi-cloud deployment environments accelerates ARA adoption across the region.

China Application Release Automation (ARA) Market Insight

China leads the Asia-Pacific market due to rapid expansion of domestic cloud platforms, fintech ecosystems, and large-scale enterprise software modernization. Government-backed digital transformation initiatives and strong investment in AI-driven development platforms drive demand for advanced release automation solutions. Growing SaaS adoption and high-volume enterprise deployments further strengthen market growth.

Japan Application Release Automation (ARA) Market Insight

Japan demonstrates steady growth supported by enterprise modernization, cloud migration strategies, and increasing adoption of agile methodologies. Strong focus on operational efficiency, regulatory compliance, and cybersecurity encourages integration of automated release management platforms across financial services, manufacturing, and telecom sectors.

India Application Release Automation (ARA) Market Insight

India is emerging as a high-growth market driven by expanding ITES industry, startup ecosystems, and rapid digitalization of banking and retail sectors. Increasing adoption of DevOps frameworks, SaaS platforms, and cloud-native development environments accelerates ARA implementation across enterprises.

South Korea Application Release Automation (ARA) Market Insight

South Korea contributes significantly due to strong telecom infrastructure, advanced IT services capabilities, and rapid deployment of enterprise cloud solutions. Growing focus on digital innovation, AI-based software development, and automation-driven efficiency continues to support sustained market expansion.

Which are the Top Companies in Application Release Automation (ARA) Market?

The application release automation (ARA) industry is primarily led by well-established companies, including:

- IBM (U.S.)

- Microsoft (U.S.)

- FUJITSU (Japan)

- Red Hat, Inc. (U.S.)

- VMware, Inc. (U.S.)

- BMC Software, Inc. (U.S.)

- CA Technologies (U.S.)

- Micro Focus (U.K.)

- Coforge (India)

- Attunity (U.S.)

- ARCAD Software (France)

- Progress Software Corporation (U.S.)

- Clarive (Spain)

- CloudBees, Inc. (U.S.)

- CollabNet (U.S.)

- Datical (U.S.)

- Flexagon LLC (U.S.)

- Inedo (U.S.)

- MidVision Ltd (U.K.)

- Octopus Deploy (Australia)

- Plutora (U.S.)

- Puppet (U.S.)

- Rocket Software, Inc. (U.S.)

- Digital.ai (U.S.)

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.