Global Atomic Layer Deposition Market

Размер рынка в млрд долларов США

CAGR :

%

USD

2.94 Billion

USD

8.81 Billion

2025

2033

USD

2.94 Billion

USD

8.81 Billion

2025

2033

| 2026 –2033 | |

| USD 2.94 Billion | |

| USD 8.81 Billion | |

| % | |

|

Global Atomic Layer Deposition Market Segmentation, By Product Type (Metal ALD, Aluminium Oxide ALD, Plasma Enhanced ALD, Catalytic ALD, and Others), Application (Semiconductors, Solar Devices, Electronics, Medical Equipment, Research & Development Facilities, Fuel Cells, Optical Devices, Thermoelectric Materials, Magnetic Heads, Sensors, Barrier Layers, Primer Layers, Non—IC Application, and Others) - Industry Trends and Forecast to 2033

What is the Global Atomic Layer Deposition Market Size and Growth Rate?

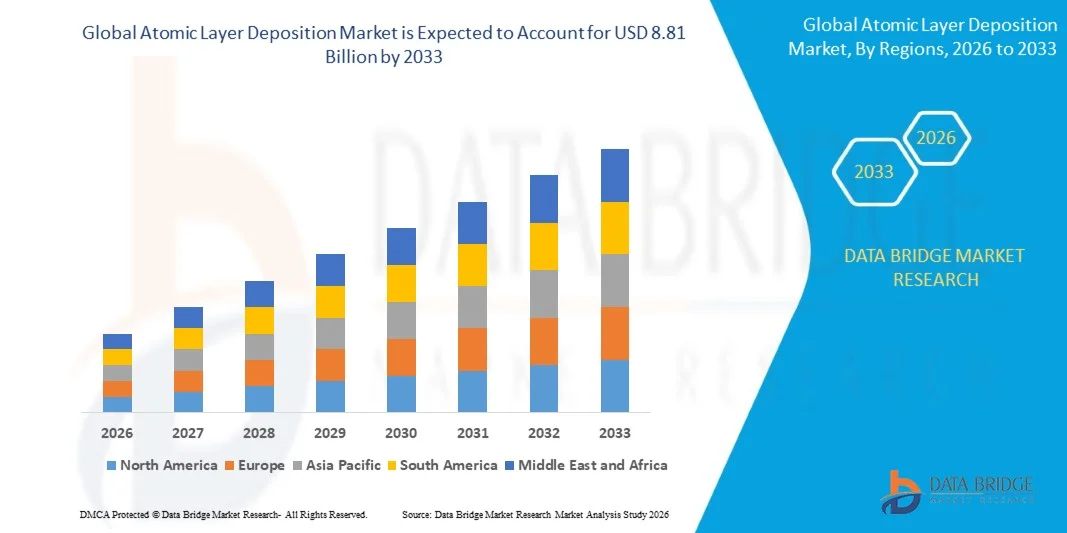

- The global atomic layer deposition market size was valued at USD 2.94 billion in 2025 and is expected to reach USD 8.81 billion by 2033, at a CAGR of 14.7% during the forecast period

- Microelectronics is a process of manufacturing electronic components at the microscopic level. The microelectronics market is rapidly growing due to the demand for inexpensive and lightweight equipment

- Microelectronics components include transistors, capacitors, diodes, resistors, inductors, and others. All these electronic components are used to manufacture mobile phones, laptops, electronic toys, and others

What are the Major Takeaways of Atomic Layer Deposition Market?

- Photovoltaic (PV) is commonly called an energy harvesting technology, and the technology is used to convert solar energy into electric energy, which is electricity

- The demand for photovoltaic cells has been increasing due to the relatively low price and wide range of applications such as solar traffic lights, solar power pumps, solar lamps, solar power calculators, and others

- Asia-Pacific dominated the atomic layer deposition market with a 43.2% revenue share in 2025, driven by strong growth in semiconductor fabrication, advanced electronics manufacturing, display panel production, and rapid expansion of chip foundries across China, Japan, South Korea, and Taiwan

- North America is projected to register the fastest CAGR of 10.84% from 2026 to 2033, driven by rapid growth in semiconductor R&D, AI hardware development, quantum computing, and advanced materials research across the U.S. and Canada

- The Plasma Enhanced ALD segment dominated the market with a 38.6% share in 2025, as it remains the preferred technology for advanced semiconductor fabrication, high-performance coatings, and next-generation electronic components

Report Scope and Atomic Layer Deposition Market Segmentation

|

Attributes |

Atomic Layer Deposition Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Atomic Layer Deposition Market?

“Increasing Shift Toward High-Precision, Compact, and Semiconductor-Focused Atomic Layer Deposition Systems”

- The atomic layer deposition market is witnessing strong adoption of high-precision thin-film coating systems designed to support advanced semiconductors, MEMS, sensors, display panels, and energy storage devices

- Manufacturers are introducing high-throughput, plasma-enhanced, and spatial ALD systems that offer atomic-scale film thickness control, excellent conformality, and compatibility with complex 3D structures and next-generation chip architectures

- Growing demand for cost-efficient, compact, and high-performance deposition tools is driving usage across semiconductor fabs, nanotechnology research centres, solar cell manufacturing, and electronics laboratories

- For instance, companies such as Applied Materials, Lam Research, Tokyo Electron, ASM International, and Beneq are expanding their ALD portfolios with advanced wafer-level processing and enhanced precursor delivery technologies

- Increasing need for smaller transistor nodes, advanced packaging, and high-k dielectric coatings is accelerating the shift toward precision ALD platforms

- As electronics become more compact and technologically advanced, atomic layer deposition will remain vital for semiconductor scaling, high-performance coatings, and advanced material engineering

What are the Key Drivers of Atomic Layer Deposition Market?

- Rising demand for ultra-thin, uniform, and highly accurate film deposition technologies to support advanced semiconductor manufacturing is a major growth driver

- For instance, in 2025, leading companies such as AIXTRON, ASM International, and Oxford Instruments upgraded their ALD systems to support finer process control, higher throughput, and advanced material compatibility

- Growing adoption across AI chips, memory devices, consumer electronics, EV batteries, solar panels, and medical electronics is boosting demand across the U.S., Europe, and Asia-Pacific

- Advancements in plasma-enhanced ALD, spatial ALD, precursor chemistry, and wafer-scale automation have strengthened efficiency, scalability, and process precision

- Rising use of AI processors, 3D NAND memory, advanced displays, and next-generation sensors is creating demand for highly controlled atomic-scale deposition technologies

- Supported by steady investments in semiconductor R&D, nanotechnology innovation, and advanced manufacturing infrastructure, the Atomic Layer Deposition market is expected to witness strong long-term growth

Which Factor is Challenging the Growth of the Atomic Layer Deposition Market?

- High costs associated with premium deposition chambers, advanced precursor materials, and precision process control systems restrict adoption among small fabs and research institutions

- For instance, during 2024–2025, fluctuations in semiconductor equipment costs, specialty gas prices, and material supply chains increased system manufacturing expenses for several global vendors

- Complexity in handling atomic-scale thickness control, multi-layer deposition sequences, and material compatibility increases the need for highly skilled engineers and process specialists

- Limited awareness in emerging markets regarding ALD applications, process integration, and material engineering benefits slows adoption

- Competition from chemical vapor deposition (CVD), physical vapor deposition (PVD), and other thin-film technologies creates pricing pressure and reduces product differentiation

- To address these issues, companies are focusing on cost-optimized system designs, improved automation, and higher process integration to increase global adoption of atomic layer deposition systems

How is the Atomic Layer Deposition Market Segmented?

The market is segmented on the basis of product type and application.

• By Product Type

On the basis of product type, the Atomic Layer Deposition market is segmented into Metal ALD, Aluminium Oxide ALD, Plasma Enhanced ALD, Catalytic ALD, and Others. The Plasma Enhanced ALD segment dominated the market with a 38.6% share in 2025, as it remains the preferred technology for advanced semiconductor fabrication, high-performance coatings, and next-generation electronic components. This segment is widely adopted due to its ability to deliver superior film uniformity, enhanced deposition rates, low-temperature processing, and precise thickness control at the atomic scale. It is extensively used across semiconductor fabs, memory device manufacturing, and advanced display production facilities.

The Metal ALD segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by rising demand for conductive thin films in advanced chips, AI processors, 3D NAND memory, and high-density interconnects. Increasing innovation in metal precursors and process integration is further accelerating adoption globally.

• By Application

On the basis of application, the market is segmented into Semiconductors, Solar Devices, Electronics, Medical Equipment, Research & Development Facilities, Fuel Cells, Optical Devices, Thermoelectric Materials, Magnetic Heads, Sensors, Barrier Layers, Primer Layers, Non-IC Application, and Others. The Semiconductors segment dominated the market with a 42.9% share in 2025, supported by rapid growth in chip miniaturization, advanced node fabrication, and increasing demand for high-performance computing systems. Atomic Layer Deposition is extensively used in depositing high-k dielectric layers, gate oxides, barrier films, spacer layers, and conformal coatings for complex 3D structures such as FinFETs and memory devices. Its ability to provide highly uniform ultra-thin films makes it essential for modern semiconductor manufacturing.

The Sensors segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing deployment of IoT devices, automotive ADAS systems, industrial automation, and smart healthcare equipment. Rising demand for precision-coated micro sensors and MEMS devices continues to strengthen long-term market expansion.

Which Region Holds the Largest Share of the Atomic Layer Deposition Market?

- Asia-Pacific dominated the atomic layer deposition market with a 43.2% revenue share in 2025, driven by strong growth in semiconductor fabrication, advanced electronics manufacturing, display panel production, and rapid expansion of chip foundries across China, Japan, South Korea, and Taiwan. High adoption of ALD systems for 3D NAND memory, advanced logic nodes, sensors, and semiconductor packaging continues to fuel demand across wafer fabs, R&D centres, and precision electronics manufacturing facilities

- Leading companies in Asia-Pacific are introducing high-throughput plasma-enhanced ALD systems, advanced precursor technologies, and wafer-scale deposition tools, strengthening the region’s technological advantage. Continuous investment in AI chips, EV electronics, high-density memory, and semiconductor infrastructure drives long-term market expansion

- Strong semiconductor ecosystems, high-volume electronics production, and sustained investment in advanced materials manufacturing further reinforce regional market leadership

China Atomic Layer Deposition Market Insight

China is the largest contributor in Asia-Pacific, supported by massive semiconductor investments, rapid foundry expansion, and strong government support for domestic chip manufacturing. Increasing development of AI processors, memory chips, sensors, and display technologies intensifies demand for ALD systems capable of precise atomic-scale coating. Presence of large-scale manufacturing clusters and local equipment suppliers further drives market growth.

Japan Atomic Layer Deposition Market Insight

Japan contributes significantly to regional growth, driven by advanced semiconductor materials research, precision electronics manufacturing, and strong adoption of deposition technologies across industrial and medical electronics sectors. Continuous modernization of semiconductor and display manufacturing facilities strengthens market demand.

India Atomic Layer Deposition Market Insight

India is emerging as a major growth hub, driven by expanding semiconductor design centres, electronics manufacturing initiatives, and government-backed chip fabrication investments. Growing demand for sensors, consumer electronics, and industrial devices fuels ALD adoption in research and prototyping environments.

South Korea Atomic Layer Deposition Market Insight

South Korea contributes significantly due to strong demand for memory devices, AI processors, OLED displays, and high-performance consumer electronics. Rapid development of semiconductor fabs and display technologies drives adoption of advanced ALD systems with higher deposition precision and throughput.

North America Atomic Layer Deposition Market

North America is projected to register the fastest CAGR of 10.84% from 2026 to 2033, driven by rapid growth in semiconductor R&D, AI hardware development, quantum computing, and advanced materials research across the U.S. and Canada. Rising demand for ultra-thin film deposition in advanced chip architectures, medical devices, and aerospace electronics continues to accelerate market expansion.

U.S. Atomic Layer Deposition Market Insight

The U.S. is the largest contributor in North America, supported by strong semiconductor innovation, rapid adoption of advanced node technologies, and extensive utilization of ALD systems across foundries, research labs, and defence electronics sectors. Increasing development of AI accelerators, high-speed processors, and advanced sensors intensifies demand for precision deposition solutions.

Canada Atomic Layer Deposition Market Insight

Canada contributes significantly to regional growth, driven by expanding nanotechnology research clusters, rising semiconductor design activities, and growing investment in healthcare electronics and advanced materials R&D. Universities and innovation centres increasingly utilize ALD systems for precision coating and materials engineering applications.

Which are the Top Companies in Atomic Layer Deposition Market?

The atomic layer deposition industry is primarily led by well-established companies, including:

- ADEKA CORPORATION (Japan)

- AIXTRON SE (Germany)

- Applied Materials Inc. (U.S.)

- ASM International N.V. (Netherlands)

- LAM RESEARCH CORPORATION (U.S.)

- Tokyo Electron Limited (Japan)

- Kurt J. Lesker Company (U.S.)

- Beneq Oy (Finland)

- Veeco Instruments Inc. (U.S.)

- ANRIC TECH. (South Korea)

- Encapsulix (France)

- SENTECH Instruments GmbH (Germany)

- Oxford Instruments plc (U.K.)

- Forge Nano Inc. (U.S.)

- Merck KGaA (Germany)

- HZO, Inc. (U.S.)

- Picosun Oy (Finland)

What are the Recent Developments in Global Atomic Layer Deposition Market?

- In November 2025, Beneq Oy launched the Transmute ALD platform, an advanced next-generation deposition system developed for high-volume manufacturing of wide-bandgap power electronics, RF components, and micro-LED applications. The platform integrates plasma pretreatment, PEALD, and thermal ALD capabilities to ensure high-throughput production with precise atomic-level interface control. In conclusion, this launch strengthens Beneq’s position in advanced semiconductor deposition technologies and supports next-generation electronics manufacturing

- In September 2025, Forge Nano Inc. introduced its TEPHRA One 200 mm single-wafer ALD tool at SEMICON Taiwan, designed to support automated deposition of oxides, nitrides, and nanolaminate coatings for compound semiconductor fabrication. The system enables faster coating speeds and scalable wafer-level production for advanced electronics applications. In conclusion, this innovation enhances production efficiency and expands Forge Nano’s capabilities in semiconductor ALD solutions

- In February 2025, Lam Research Corporation unveiled the ALTUS Halo atomic layer deposition system, recognized as the industry’s first molybdenum ALD solution for high-volume semiconductor manufacturing. The platform delivers low-resistivity and void-free metallization essential for advanced memory and logic chips, supporting continued scaling for AI and next-generation devices. In conclusion, this development reinforces Lam Research’s leadership in precision semiconductor deposition technologies

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.