Global Bio Implants Market

Размер рынка в млрд долларов США

CAGR :

%

USD

146.10 Billion

USD

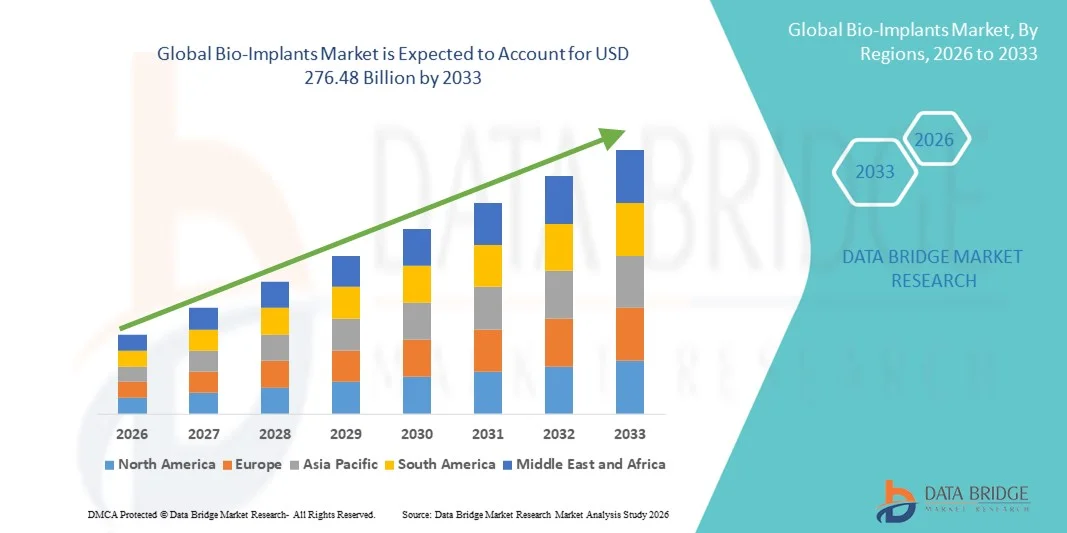

276.48 Billion

2025

2033

USD

146.10 Billion

USD

276.48 Billion

2025

2033

| 2026 –2033 | |

| USD 146.10 Billion | |

| USD 276.48 Billion | |

| % | |

|

Global Bio-Implants Market Segmentation, By Product Type (Orthopaedics and Trauma, Pacing Devices, Stents and Related Implants, Spinal Implants, Ophthalmic Implants, Structural Cardiac Implants, Dental Implants, Neurostimulators Implants and Prosthetic Implants), Type (Allograft, Autograft, Xenograft and Synthetic), Material (Biomaterial Metal, Alloy, Polymer, Ceramics and Acrylic Hydrogel), Mode of Administration (Surgical and Non-Surgical), End-User (Clinics, Hospitals and Ambulatory Surgical Centres) - Industry Trends and Forecast to 2033

Bio-Implants Market Size

- The global bio-implants market size was valued at USD 146.10 billion in 2025 and is expected to reach USD 276.48 billion by 2033, at a CAGR of 8.30% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic diseases, rising number of surgical procedures, and continuous advancements in biomaterials and implant technologies, leading to greater adoption of bio-implants across orthopedic, dental, cardiovascular, and cosmetic applications. Rapid progress in 3D printing, bioresorbable materials, and tissue engineering is further accelerating innovation and expanding the clinical use of bio-implant solutions in both developed and emerging healthcare markets

- Furthermore, the growing demand for minimally invasive procedures, improved patient outcomes, and long-lasting biocompatible materials is establishing bio-implants as a critical component of modern medical treatment. Increasing geriatric population, expanding healthcare infrastructure, and rising investments in research and development are accelerating the uptake of bio-implant solutions, thereby significantly boosting overall industry growth

Bio-Implants Market Analysis

- Bio-implants, designed to replace, support, or enhance biological structures within the human body, are increasingly vital components of modern healthcare across orthopedic, dental, cardiovascular, spinal, and cosmetic procedures due to their high biocompatibility, durability, and ability to restore physiological function. Continuous advancements in biomaterials such as titanium alloys, ceramics, polymers, and bioresorbable materials are further enhancing implant safety and long-term performance

- The escalating demand for bio-implants is primarily fueled by the rising prevalence of degenerative diseases, increasing incidence of trauma and orthopedic injuries, expanding geriatric population, and growing preference for minimally invasive surgical procedures. Technological innovations including 3D-printed implants, patient-specific customization, and improved surface coatings are accelerating product adoption and improving clinical outcomes

- North America dominated the bio-implants market with the largest revenue share of approximately 39.4% in 2025, characterized by advanced healthcare infrastructure, strong reimbursement frameworks, high surgical procedure volumes, and the presence of leading medical device manufacturers. The U.S. continues to witness substantial growth in orthopedic, dental, and spinal implant procedures, driven by technological innovation and rising demand for joint replacement surgeries

- Asia-Pacific is expected to be the fastest-growing region in the bio-implants market during the forecast period, projected to register a CAGR of approximately 10.6%–11.4%, driven by increasing healthcare expenditure, expanding medical tourism, improving access to advanced surgical treatments, and rising awareness regarding implant-based therapies across emerging economies such as China and India

- The Surgical segment dominated with a revenue share of 81.5% in 2025, driven by the necessity of operative procedures for implant placement. Majority of orthopedic, cardiac, spinal, and dental implants require surgical intervention

Report Scope and Bio-Implants Market Segmentation

|

Attributes |

Bio-Implants Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Bio-Implants Market Trends

Innovation in Biocompatible, Bioactive, and Customized Implant Solutions

- A prominent global trend in the bio-implants market is the continuous advancement of highly biocompatible and bioactive materials that enhance long-term implant performance and patient safety

- Manufacturers are increasingly focusing on implants that promote faster healing, improved tissue integration, and reduced inflammatory response

- The use of advanced titanium alloys, ceramic composites, polymer-based biomaterials, and bioresorbable implants is significantly transforming orthopedic, dental, spinal, and cardiovascular procedures

- For instance, Zimmer Biomet has developed advanced joint reconstruction systems designed to improve implant longevity and support natural bone in-growth, reducing the likelihood of revision surgeries. Such technological developments are strengthening surgeon confidence and expanding clinical adoption globally

- In addition, the rise of 3D printing and patient-specific implant customization is reshaping surgical planning. Customized implants designed using digital imaging and computer-assisted modeling allow better anatomical fit, improved functionality, and shorter recovery periods

- The growing demand for minimally invasive surgeries and faster rehabilitation timelines is further accelerating the transition toward next-generation bio-implant technologies across both developed and emerging market

Bio-Implants Market Dynamics

Driver

Increasing Burden of Degenerative Diseases and Expanding Surgical Volumes

- The rising global prevalence of degenerative disorders, trauma injuries, and chronic conditions is a major driver fueling the growth of the bio-implants market. Age-related diseases such as osteoarthritis, osteoporosis, cardiovascular blockages, and dental deterioration are increasing significantly due to longer life expectancy and sedentary lifestyles

- This trend is leading to a higher number of joint replacements, spinal fixation procedures, dental implant surgeries, and cardiac implant placements worldwide

- For instance, data from the World Health Organization highlights the rapid growth of the elderly population globally, which directly correlates with increased demand for orthopedic and cardiovascular implant procedures

- As healthcare systems expand their surgical capabilities, the volume of implant-based interventions continues to rise steadily

- Moreover, improving healthcare infrastructure in Asia-Pacific and Latin America, expanding medical insurance coverage, and growing awareness about early surgical intervention are contributing to higher treatment rate

- Technological advancements that improve implant durability and surgical precision are further encouraging both physicians and patients to opt for implant-based therapeutic solutions

Restraint/Challenge

High Treatment Costs, Regulatory Complexities, and Risk Factors

- Despite strong growth potential, the global bio-implants market faces challenges related to high procedural costs and stringent regulatory requirements

- Implant surgeries often require specialized equipment, skilled surgeons, and extended rehabilitation, resulting in substantial treatment expenses. These financial barriers can limit accessibility, particularly in low- and middle-income countries where reimbursement systems may be underdeveloped

- For instance, complex procedures such as total hip or knee replacement surgeries can involve significant hospital and implant costs, restricting affordability for certain patient populations. Such economic constraints may delay elective implant procedures in cost-sensitive markets

- In addition, potential complications such as infection, implant loosening, allergic reactions, or device failure pose clinical risks. Regulatory authorities impose strict approval pathways and post-market surveillance requirements to ensure patient safety, which can extend product development timelines and increase compliance costs for manufacturers

- Addressing these challenges through cost-efficient manufacturing, enhanced biomaterial safety, surgeon training, and improved regulatory harmonization will be critical for sustaining long-term global market expansion

Bio-Implants Market Scope

The market is segmented on the basis of product type, type, material, mode of administration, and end-user.

- By Product Type

On the basis of product type, the Global Bio-Implants market is segmented into Orthopaedics and Trauma, Pacing Devices, Stents and Related Implants, Spinal Implants, Ophthalmic Implants, Structural Cardiac Implants, Dental Implants, Neurostimulators Implants, and Prosthetic Implants. The Orthopaedics and Trauma segment dominated the largest market revenue share of 28.6% in 2025, driven by the rising prevalence of osteoporosis, fractures, and sports injuries globally. Increasing geriatric population and growing demand for joint replacement procedures significantly contribute to segment growth. Technological advancements in minimally invasive orthopedic surgeries enhance procedural success rates and recovery. Rising awareness regarding early treatment of musculoskeletal disorders supports adoption. Favorable reimbursement policies in developed economies strengthen market penetration. Expanding healthcare infrastructure in emerging economies further accelerates growth. Increasing adoption of robotic-assisted surgeries improves precision. Growing medical tourism for orthopedic procedures boosts revenue. Continuous innovation in implant durability and biomaterials enhances patient outcomes. Rising incidence of road accidents worldwide drives implant demand. Increasing clinical trials and procedural guidelines further strengthen market share.

The Dental Implants segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, driven by rising awareness regarding oral health and increasing demand for cosmetic dentistry procedures. Growth is supported by the aging population and edentulous patients requiring restorative treatments. Technological advancements, including 3D imaging and computer-guided implant placement, enhance precision and outcomes. Increasing disposable income in emerging economies supports affordability. Expansion of private dental clinics globally accelerates adoption. Rising medical tourism for cost-effective dental procedures contributes to rapid growth. Continuous innovation in biomaterials and implant designs improves durability and success rates. Greater access to dental insurance in select countries supports market expansion. Minimally invasive implant techniques reduce recovery time and improve patient comfort. Awareness campaigns on oral care further drive adoption. Increasing collaborations between manufacturers and dental associations enhance market penetration. Expansion of research in regenerative dentistry fuels long-term growth.

- By Type

On the basis of type, the Global Bio-Implants market is segmented into Allograft, Autograft, Xenograft, and Synthetic. The Autograft segment dominated the market with a revenue share of 34.2% in 2025, attributed to its high biocompatibility and minimal risk of immune rejection. Autografts are widely used in orthopedic, spinal, and dental procedures due to higher clinical success rates. Faster healing and integration with host tissue support procedural preference. Rising trauma and spinal surgeries globally drive adoption. Increasing awareness among surgeons regarding long-term benefits enhances utilization. Lower infection risk compared to other graft types strengthens clinical acceptance. Technological improvements in graft harvesting further boost procedural efficiency. Growing number of bone reconstruction procedures contributes to revenue. Expanding surgical capabilities in developing regions support segment dominance. Continuous research in graft viability improves outcomes. Government funding in advanced surgical centers strengthens adoption. High-quality donor material availability supports global market share.

The Synthetic segment is expected to witness the fastest CAGR of 10.4% from 2026 to 2033, fueled by growing demand for off-the-shelf, customizable graft substitutes. Synthetic grafts eliminate donor site complications and reduce surgery time. Advancements in biomaterials, bioactive, and bioresorbable substitutes drive innovation. Increasing regulatory approvals and clinical validations accelerate commercialization. Rising preference for predictable and consistent quality enhances market acceptance. Expanding orthopedic, dental, and spinal procedures support adoption. Continuous R&D in composite polymers and nanomaterials improves mechanical properties. Growing demand in minimally invasive procedures strengthens growth. Rising awareness of synthetic alternatives among surgeons further drives uptake. Availability of cost-effective synthetic grafts in emerging markets supports expansion. Collaboration between manufacturers and hospitals enhances adoption. Improved patient outcomes with synthetic grafts further encourage growth.

- By Material

On the basis of material, the Global Bio-Implants market is segmented into Biomaterial Metal, Alloy, Polymer, Ceramics, and Acrylic Hydrogel. The Biomaterial Metal segment dominated with a revenue share of 39.7% in 2025, due to high strength, durability, and biocompatibility. Metals such as titanium and stainless steel are extensively used in orthopedic, dental, and spinal implants. Superior load-bearing capacity makes metals suitable for joint replacements and trauma fixation. Rising volumes of hip and knee replacement surgeries globally drive demand. Continuous advancements in corrosion resistance enhance implant longevity. Strong clinical track record and surgeon familiarity support adoption. Expanding hospital infrastructure globally further accelerates utilization. Growing prevalence of degenerative bone disorders contributes to revenue. Improved surface coatings and alloy innovations enhance performance. Rising emergency trauma and accident-related procedures strengthen segment share. High reimbursement coverage in developed countries supports market dominance. Continuous product innovation in metals ensures long-term growth.

The Polymer segment is projected to witness the fastest CAGR of 10.9% from 2026 to 2033, driven by rising adoption of lightweight and flexible implant materials. Polymers reduce imaging interference, making them suitable for spinal and cardiovascular implants. Increasing demand for bioresorbable and biodegradable implants fuels segment growth. Advancements in polymer chemistry improve mechanical strength, durability, and biocompatibility. Minimally invasive surgeries support higher polymer implant adoption. Expanding neurostimulator and cardiac procedures further drive market growth. Continuous R&D investments in polymer-based composites enhance performance. Patient comfort and reduced complication rates encourage surgeon preference. Availability of cost-effective polymer implants in emerging markets boosts adoption. Collaboration with academic institutions accelerates material innovations. Growing awareness of polymer advantages strengthens long-term growth. Market penetration in Asia-Pacific and Latin America further supports rapid CAGR.

- By Mode of Administration

On the basis of mode of administration, the Global Bio-Implants market is segmented into Surgical and Non-Surgical. The Surgical segment dominated with a revenue share of 81.5% in 2025, driven by the necessity of operative procedures for implant placement. Majority of orthopedic, cardiac, spinal, and dental implants require surgical intervention. Rising hospital admissions for trauma and chronic diseases support growth. Technological advancements in robotic-assisted and minimally invasive surgeries improve procedural outcomes. Increasing number of skilled surgeons globally enhances accessibility. Expanding healthcare investments in emerging markets contribute to procedural growth. Continuous development of advanced surgical instruments strengthens adoption. Increasing awareness about implant-based treatments drives hospital demand. Rising geriatric population and chronic disease prevalence support segment dominance. Government funding in surgical infrastructure further boosts usage. Hospitals remain primary adoption centers due to expertise availability. Rising preference for high-precision procedures enhances surgical implant adoption.

The Non-Surgical segment is expected to witness the fastest CAGR of 8.7% from 2026 to 2033, driven by innovations in minimally invasive implant placement and image-guided procedures. Growing patient preference for outpatient procedures with shorter recovery time enhances adoption. Increasing awareness of non-surgical solutions in orthopedic, dental, and spinal treatments accelerates demand. Technological advancements in catheter-based and guided delivery systems support market growth. Expanding ambulatory care facilities globally improve accessibility. Reduced hospitalization and lower procedural costs drive adoption. Rising regulatory approvals for innovative non-surgical implants accelerate commercialization. Collaboration with private healthcare networks supports rapid uptake. Patient comfort and lower complication risks further strengthen growth. Expansion in emerging economies fuels high demand. Adoption of non-surgical implants in cosmetic and dental applications contributes to CAGR. Continuous R&D in minimally invasive solutions ensures sustained segment growth.

- By End-User

On the basis of end-user, the Global Bio-Implants market is segmented into Clinics, Hospitals, and Ambulatory Surgical Centres. The Hospitals segment dominated with a revenue share of 56.4% in 2025, due to high patient volume and advanced surgical infrastructure. Complex procedures for orthopedic, cardiac, spinal, and dental implants are primarily conducted in hospitals. Availability of multidisciplinary expertise strengthens dominance. Rising emergency trauma and surgical admissions further contribute to growth. Government healthcare funding and reimbursement support procedural expansion. Advanced imaging, ICU, and post-operative care facilities enhance treatment capability. Hospitals remain preferred due to access to highly skilled surgeons. Rising adoption of robotic and minimally invasive surgeries supports segment leadership. Continuous innovation in implantable devices drives hospital utilization. Expanding healthcare infrastructure globally accelerates adoption. High patient trust and safety perception further support growth. Hospitals dominate in both developed and emerging economies for implant procedures.

The Ambulatory Surgical Centres segment is expected to witness the fastest CAGR of 9.5% from 2026 to 2033, driven by the increasing shift toward outpatient surgical procedures. Lower costs compared to hospital-based surgeries improve affordability and patient preference. Rising adoption of minimally invasive implant techniques enhances growth. Shorter hospital stays and faster recovery times further support segment expansion. Expansion of private healthcare facilities globally increases accessibility. Favorable reimbursement frameworks in developed markets drive adoption. Technological innovation in ASC-based implant procedures accelerates uptake. Patient convenience and reduced infection risk enhance appeal. Collaboration with specialty clinics supports rapid segment growth. Rising awareness about outpatient options fuels demand. Increasing orthopedic, dental, and cardiac outpatient procedures contribute to CAGR. Expanding ASC infrastructure in emerging economies strengthens long-term growth.

Bio-Implants Market Regional Analysis

- North America dominated the bio-implants market with the largest revenue share of approximately 39.4% in 2025, characterized by advanced healthcare infrastructure, strong reimbursement frameworks, high surgical procedure volumes, and the presence of leading medical device manufacturers

- The region benefits from early adoption of innovative implant technologies, including orthopedic, dental, and spinal implants. Hospitals and specialized clinics continue to witness substantial growth in surgical procedures due to technological advancements and rising demand for joint replacement surgeries

- High awareness about minimally invasive procedures supports adoption. Continuous R&D in biomaterials and implant customization strengthens the market. Patients’ preference for predictable surgical outcomes and faster recovery enhances penetration. Strong clinical training and government policies further reinforce growth. Advanced surgical planning and digital integration promote efficiency. Rising geriatric population and lifestyle-related injuries drive demand

U.S. Bio-Implants Market Insight

The U.S. bio-implants market captured the largest revenue share in 2025 within North America, fueled by increasing adoption of orthopedic, dental, and spinal implants, alongside rapid technological innovation. Hospitals and ambulatory surgical centers are key end-users, leveraging robotic-assisted and minimally invasive procedures. The growing geriatric population, rising trauma cases, and demand for joint replacement surgeries propel the market. Advanced materials, including bioresorbable polymers and customized implants, improve surgical outcomes. Favorable reimbursement policies support patient access. Private clinics and outpatient centers are expanding, enhancing availability. Ongoing R&D programs strengthen product portfolios. Awareness among surgeons and patients about innovative procedures drives adoption. Government initiatives for healthcare modernization further stimulate growth. Clinical evidence of improved recovery and reduced complications encourages use. Strategic partnerships between hospitals and manufacturers ensure reliable supply.

Europe Bio-Implants Market Insight

The Europe bio-implants market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by established healthcare systems, stringent regulatory frameworks, and rising surgical volumes. Hospitals, private clinics, and multi-specialty centers remain the key end-users. European consumers value advanced surgical procedures, minimally invasive techniques, and predictable clinical outcomes. Urbanization and investment in healthcare infrastructure accelerate market penetration. Technological innovation, including robotic-assisted surgeries and 3D-printed implants, enhances procedural efficiency. The increase in musculoskeletal disorders and geriatric population drives demand. Private hospital expansions and multi-family healthcare systems improve accessibility. Rising awareness of polymer and synthetic implants fosters adoption. Government funding and healthcare initiatives promote innovation. Cross-border healthcare and medical tourism further contribute to growth. Continuous product development strengthens competitiveness.

U.K. Bio-Implants Market Insight

The U.K. bio-implants market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing demand for minimally invasive orthopedic and dental procedures. Hospitals and outpatient centers remain the major end-users. The growing geriatric population and rising awareness about advanced surgical treatments accelerate adoption. Private clinics and medical tourism enhance access to implant-based therapies. Advanced materials, bioresorbable implants, and polymer-based solutions strengthen procedural outcomes. Government reimbursement frameworks support commercialization. Expansion of e-commerce and retail infrastructure enables better product availability. Surgeons’ preference for precision implants and predictable outcomes further fuels growth. Integration of robotic-assisted surgeries improves efficiency. Rising orthopedic, spinal, and dental procedures drive adoption. Continuous clinical training supports procedural success. Patients’ demand for faster recovery promotes uptake.

Germany Bio-Implants Market Insight

The Germany bio-implants market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, emphasis on innovation, and increasing awareness of advanced implant technologies. Hospitals, multi-specialty centers, and outpatient clinics are key end-users. High surgical volumes in orthopedic, spinal, and dental procedures drive revenue. Technological integration, including robotic-assisted procedures and 3D-printed implants, enhances precision and outcomes. Rising geriatric population and lifestyle-related injuries support market growth. Strong government initiatives for healthcare modernization and sustainability promote adoption. Patients increasingly prefer bioresorbable and synthetic implants. Private hospitals and clinics expand access to advanced surgical solutions. Clinical evidence of improved recovery encourages adoption. Continuous R&D strengthens product portfolios. Availability of cost-effective domestic manufacturing ensures supply reliability.

Asia-Pacific Bio-Implants Market Insight

The Asia-Pacific bio-implants market is poised to grow at the fastest CAGR of approximately 10.6%–11.4% from 2026 to 2033, driven by increasing healthcare expenditure, expanding medical tourism, improving access to advanced surgical treatments, and rising awareness regarding implant-based therapies across emerging economies such as China and India. Rising surgical volumes in orthopedic, dental, and spinal procedures support growth. Expansion of private hospitals and specialty clinics accelerates adoption. Urbanization, disposable income growth, and awareness of minimally invasive procedures enhance market penetration. Government investment in hospital modernization fuels demand. Hospitals and outpatient centers remain the primary end-users. Technological innovation, including robotic-assisted and 3D-printed implants, improves outcomes. Patient preference for customized implants increases uptake. Rising geriatric population and lifestyle-related injuries drive adoption. Awareness of bioresorbable and polymer-based implants fosters acceptance. Domestic manufacturing in China and India ensures product availability. Medical tourism further boosts regional revenue.

Japan Bio-Implants Market Insight

The Japan bio-implants market is gaining momentum due to the country’s high-tech surgical infrastructure, aging population, and strong adoption of minimally invasive procedures. Hospitals and clinics are the major end-users. Rising demand for orthopedic, dental, and spinal implants supports market expansion. Robotic-assisted surgeries and advanced imaging enhance surgical precision. Awareness of polymer, synthetic, and bioresorbable implants drives adoption. Government reimbursement frameworks improve patient access. Outpatient and private surgical centers increase availability. Surgeons’ preference for reliable implants strengthens uptake. Rising geriatric population fuels demand for predictable outcomes. Clinical evidence supports increased adoption. Expansion of domestic manufacturing improves accessibility. Continuous R&D and training programs promote innovation. Technological integration and patient awareness sustain growth.

China Bio-Implants Market Insight

The China bio-implants market accounted for the largest revenue share in Asia-Pacific of approximately 22.8% in 2025, attributed to high surgical volumes, rapid urbanization, expanding healthcare infrastructure, and strong domestic manufacturing capabilities. Hospitals, multi-specialty centers, and outpatient facilities are key end-users. Increasing awareness of orthopedic, spinal, and dental implant procedures drives adoption. Demand for minimally invasive procedures and advanced materials accelerates uptake. Government investment in hospital modernization promotes market growth. Medical tourism contributes to increasing surgical volumes. Technological adoption, including robotic-assisted surgeries and 3D printing, enhances outcomes. Patients prefer bioresorbable and synthetic polymer implants. Private hospital expansions improve accessibility. Rising disposable incomes enable affordability. Continuous clinical training and R&D strengthen product portfolios. Integration of digital surgical planning sustains growth and reinforces revenue share.

Bio-Implants Market Share

The Bio-Implants industry is primarily led by well-established companies, including:

- Stryker Corporation (U.S.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Medtronic (Ireland)

- B. Braun S.E.(Germany)

- Smith & Nephew plc (U.K.)

- Boston Scientific Corporation (U.S.)

- Abbott Laboratories (U.S.)

- NuVasive, Inc. (U.S.)

- Globus Medical, Inc. (U.S.)

- Arthrex, Inc. (U.S.)

- Medicover AB (Sweden)

- LivaNova PLC (U.K.)

- Biosensors International Group (Singapore)

- LimaCorporate S.p.A. (Italy)

- Nuvo Group, Inc. (U.S.)

- Orthofix Medical Inc. (U.S.)

- Integra LifeSciences Holdings Corporation (U.S.)

- Arjo AB (Sweden)

- Bauerfeind AG (Germany)

Latest Developments in Global Bio-Implants Market

- In December 2021, Envista Holdings Corporation received FDA approval for its Nobel Biocare N1 implant system, a next-generation dental implant designed to enhance stability and long-term osseointegration by incorporating biologically driven implant components, representing a significant advance in dental bio-implant solutions

- In October 2023, Smith+Nephew launched its REGENETEN bioinductive implant in the Japanese market, designed to promote rotator cuff healing by stimulating tendon tissue regeneration, expanding access to advanced soft tissue bio-implant technology in Asia-Pacific

- In March 2024, Zimmer Biomet entered into an acquisition agreement for OSSIS, a company specializing in custom 3D-printed orthopedic implants for complex reconstructive procedures, strengthening Zimmer Biomet’s personalized bio-implant portfolio and capabilities in tailored joint reconstruction solutions

- In July 2024, Himed and Lithoz formed a Material Research Partnership Agreement to develop novel bioceramic feedstocks by integrating Himed’s calcium phosphate (CaP) with Lithoz’s ceramic binder for use in advanced 3D printing. This collaboration aims to enhance the performance and application range of bioceramic implants through improved manufacturing materials

- In November 2024, Zimmer Biomet Holdings, Inc. received FDA approval for its Oxford cementless partial knee implant, a new orthopedic bio-implant designed for long-term performance and improved patient outcomes, signaling continued innovation in orthopedic bio-implant technologies

- In January 2025, BioPoly LLC announced the first-ever use of its BioPoly radial head implant in elbow surgery, marking a milestone in the clinical adoption of advanced polymer-based orthopedic bio-implants and expanding treatment options for complex joint injuries

- In March 2025, RevBio, Inc. received regulatory approvals in several European countries to commence clinical trials for its dental implant stabilization product, driving forward the next phase of evidence-based bio-implant innovation in dental applications

- In June 2025, CollPlant Biotechnologies announced the successful 3D bioprinting of commercial-size breast implants using proprietary recombinant human collagen (rhCollagen) bioinks, representing a major breakthrough in sustainable, animal-free implant technology and large-scale clinical-grade production

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.