Global Colposcopy Market

Размер рынка в млрд долларов США

CAGR :

%

USD

621.70 Million

USD

1,139.68 Million

2025

2033

USD

621.70 Million

USD

1,139.68 Million

2025

2033

| 2026 –2033 | |

| USD 621.70 Million | |

| USD 1,139.68 Million | |

| % | |

|

Global Colposcopy Market Segmentation, By Instrument Type (Optical Colposcopes and Video/Digital Colposcopes), Instrument Portability (Portable, Fixed and Handheld), Magnification Type (Fixed and Variable), Application (Cervical Cancer Screening, Physical Examinations, Oral and Others), End User (Hospitals, Clinics, Diagnostic Centers and Others) - Industry Trends and Forecast to 2033

Colposcopy Market Size

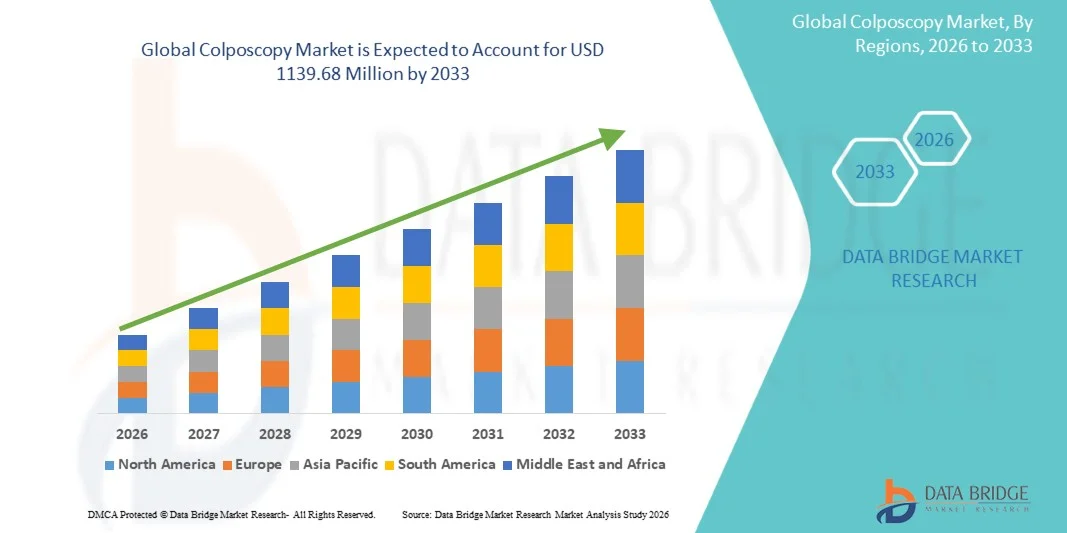

- The global colposcopy market size was valued at USD 621.70 Million in 2025 and is expected to reach USD 1139.68 Million by 2033, at a CAGR of 7.87% during the forecast period

- The market growth is largely fueled by the increasing prevalence of cervical cancer and other gynecological disorders, along with growing awareness regarding early diagnosis and routine cervical screening programs, leading to higher adoption of colposcopy procedures in hospitals and specialty clinics

- Furthermore, rising government initiatives promoting women’s health, expanding access to screening services in developing regions, and continuous technological advancements in digital and video colposcopes are establishing colposcopy systems as essential diagnostic tools in gynecological care. These converging factors are accelerating the uptake of colposcopy solutions, thereby significantly boosting the industry’s growth

Colposcopy Market Analysis

- Colposcopy systems, used for the detailed examination of the cervix, vagina, and vulva to detect precancerous and cancerous lesions, are increasingly vital components of modern gynecological diagnostics in hospitals and specialty clinics due to their enhanced visualization capabilities, improved diagnostic accuracy, and integration with digital imaging and biopsy systems

- The escalating demand for colposcopy devices is primarily fueled by the rising prevalence of cervical cancer, expanding cervical screening programs, increasing awareness regarding early disease detection, and a growing emphasis on preventive women’s healthcare services globally

- North America dominated the Colposcopy market with the largest revenue share of 38.6% in 2025, characterized by well-established cervical cancer screening programs, advanced healthcare infrastructure, high healthcare expenditure, and strong presence of leading medical device manufacturers, with the U.S. witnessing substantial growth in digital colposcopy adoption across hospitals and ambulatory surgical centers

- Asia-Pacific is expected to be the fastest-growing region in the Colposcopy market during the forecast period, projected to register a CAGR of 8.9%, driven by increasing government initiatives for women’s health screening, rising healthcare investments, improving access to diagnostic services, and growing awareness in countries such as China and India

- The cervical cancer screening segment held the largest market revenue share of 69.5% in 2025, driven by increasing global incidence of cervical cancer

Report Scope and Colposcopy Market Segmentation

|

Attributes |

Colposcopy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Olympus Corporation (Japan) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Colposcopy Market Trends

“Integration of Digital Imaging and AI-Assisted Diagnostic Systems”

- A significant and accelerating trend in the global Colposcopy market is the transition from conventional optical colposcopes to digital and video colposcopy systems integrated with advanced imaging software. These technologies enhance visualization, documentation, and diagnostic accuracy in cervical cancer screening and gynecological examinations

- For instance, companies such as Olympus Corporation and Carl Zeiss Meditec are offering high-resolution digital colposcopes equipped with enhanced magnification and image capture capabilities, allowing clinicians to detect abnormal cervical lesions more precisely. The incorporation of artificial intelligence–based image analysis tools is further improving early detection of cervical

- The incorporation of artificial intelligence–based image analysis tools is further improving early detection of cervical intraepithelial neoplasia (CIN). AI-assisted systems can support clinicians by highlighting suspicious areas, reducing diagnostic variability, and improving workflow efficiency in busy screening centers

- In addition, portable and handheld colposcopy devices are gaining traction, particularly in low- and middle-income countries, where access to traditional bulky systems is limited. Compact digital devices enable point-of-care screening and support outreach programs aimed at increasing cervical cancer screening coverage

- The growing emphasis on early diagnosis and preventive women’s healthcare is encouraging healthcare providers to adopt technologically advanced colposcopy systems that offer improved accuracy, digital recordkeeping, and integration with hospital information systems

- This shift toward digitalization and intelligent imaging solutions is reshaping clinical practices and strengthening the role of colposcopy in comprehensive cervical cancer prevention strategies

Colposcopy Market Dynamics

Driver

“Rising Prevalence of Cervical Cancer and Expanding Screening Programs”

- The increasing global burden of cervical cancer is a primary driver for the growth of the Colposcopy market. Rising awareness regarding women’s health and the importance of early detection is significantly boosting demand for diagnostic procedures following abnormal Pap smear or HPV test results

- According to data and initiatives supported by World Health Organization, global efforts to eliminate cervical cancer through widespread screening and vaccination programs are accelerating the adoption of colposcopy procedures worldwide

- Governments and healthcare organizations are expanding national screening programs, particularly in developing economies, to improve early diagnosis rates. This expansion directly increases the demand for colposcopy equipment in hospitals, specialty clinics, and ambulatory surgical centers

- Furthermore, the growing prevalence of human papillomavirus (HPV) infections—a leading cause of cervical cancer—is contributing to a higher number of diagnostic follow-up procedures requiring colposcopic examination

- Increasing healthcare expenditure, improved access to gynecological services, and the establishment of specialized women’s health clinics are additional factors propelling market growth

- Technological advancements that reduce procedure time and improve patient comfort are also encouraging clinicians to adopt modern colposcopy systems, thereby strengthening overall market expansion

Restraint/Challenge

“High Equipment Costs and Limited Access in Low-Resource Settings”

- The high cost of advanced digital colposcopy systems remains a significant challenge, particularly for small healthcare facilities and providers in low- and middle-income regions. Acquisition costs, maintenance expenses, and required training for skilled professionals can limit widespread adoption

- For instance, premium imaging systems offered by manufacturers such as CooperSurgical may require substantial capital investment, which may not be feasible for resource-constrained facilities

- In addition, limited availability of trained gynecologists and colposcopy specialists in rural or underserved areas can restrict procedural accessibility. Proper interpretation of findings requires clinical expertise, and inadequate training may affect diagnostic accuracy

- Social stigma and lack of awareness regarding cervical cancer screening in certain regions can also hinder patient participation, indirectly affecting demand for colposcopy procedures

- Regulatory approval processes and compliance with medical device standards may further increase time-to-market and operational costs for manufacturers

- Addressing these challenges through cost-effective device development, training programs for healthcare professionals, and expanded public health awareness campaigns will be essential to ensure sustained growth in the global Colposcopy market

Colposcopy Market Scope

The market is segmented on the basis of instrument type, instrument portability, magnification type, application, and end user.

• By Instrument Type

On the basis of instrument type, the Colposcopy market is segmented into optical colposcopes and video/digital colposcopes. The video/digital colposcopes segment dominated the largest market revenue share of 57.4% in 2025, driven by the increasing preference for advanced imaging systems in gynecological diagnostics. These devices provide high-definition visualization, image capture, and real-time display, improving diagnostic accuracy. Hospitals favor digital systems for enhanced documentation and integration with electronic medical records. Rising cervical cancer screening initiatives globally contribute significantly to demand. Growing adoption of AI-assisted image enhancement further strengthens market penetration. Developed regions such as North America and Europe account for major installations due to better healthcare infrastructure. Digital systems also allow easy patient counseling using recorded visuals. Continuous product innovation and improved lighting technologies enhance performance. Increasing healthcare investments and reimbursement support further drive adoption. Training programs for gynecologists are increasingly centered around digital colposcopy systems. Expanding private hospital networks also contribute to revenue growth.

The optical colposcopes segment is expected to witness the fastest CAGR of 9.1% from 2026 to 2033, driven by cost-effectiveness and strong demand from emerging markets. Optical systems remain a preferred choice for smaller clinics due to lower initial investment requirements. Government-funded screening programs in developing nations are boosting installations. These systems are easier to maintain and require minimal technical expertise. Rising awareness about early cervical cancer detection is supporting uptake. Improvements in optical lens clarity and LED illumination enhance usability. Expansion of rural healthcare facilities increases demand. International healthcare organizations are supporting low-cost screening solutions, driving adoption. Growing patient footfall in tier-2 and tier-3 cities further accelerates growth. Public-private partnerships in women’s healthcare contribute to expansion.

• By Instrument Portability

On the basis of instrument portability, the market is segmented into portable, fixed, and handheld colposcopes. The portable colposcopes segment accounted for the largest market revenue share of 42.3% in 2025, owing to their flexibility and ease of movement within hospital departments. Portable systems are widely used in outreach screening programs and mobile health units. Rising cervical cancer awareness campaigns have increased the need for mobile diagnostic equipment. Hospitals prefer portable systems for multi-room usage efficiency. Improved battery life and compact designs enhance practicality. Increasing investments in community health initiatives further support demand. Non-governmental organizations conducting rural screening drives significantly contribute to adoption. Technological advancements in lightweight imaging systems improve diagnostic precision. Growing demand for cost-efficient and scalable solutions sustains segment dominance.

The handheld colposcopes segment is projected to witness the fastest CAGR of 10.2% from 2026 to 2033, driven by rising demand for point-of-care diagnostics. Handheld devices are compact, affordable, and suitable for primary care settings. Expanding telemedicine services encourage adoption of handheld imaging tools. Smartphone-compatible colposcopes are gaining popularity due to digital connectivity. Government screening initiatives in low-resource areas support growth. Increased training of healthcare workers in rural regions accelerates adoption. Growing preference for portable screening kits enhances segment expansion.

• By Magnification Type

On the basis of magnification type, the market is segmented into fixed and variable magnification colposcopes. The variable magnification segment dominated the largest market revenue share of 61.8% in 2025, driven by the need for precise visualization during cervical examinations. Adjustable zoom capabilities allow clinicians to detect minor lesions more effectively. Hospitals prefer variable systems for advanced gynecological procedures. Integration with digital imaging enhances diagnostic confidence. Increasing demand for early-stage cancer detection supports growth. Technological innovations in optical engineering improve clarity and depth perception. Rising clinical trials evaluating advanced visualization methods further strengthen demand. Developed healthcare systems show higher adoption rates. Continuous R&D investment by manufacturers sustains technological leadership.

The fixed magnification segment is expected to witness the fastest CAGR of 8.7% from 2026 to 2033, supported by affordability and simplified operation. Fixed systems are widely adopted in smaller diagnostic clinics. Lower maintenance requirements make them cost-effective solutions. Expansion of healthcare services in developing economies drives growth. Rising awareness programs and subsidized screening initiatives contribute to adoption. Increasing patient load in primary healthcare centers accelerates installations. Technological refinement in optical clarity further improves competitiveness.

• By Application

On the basis of application, the market is segmented into cervical cancer screening, physical examinations, oral examinations, and others. The cervical cancer screening segment held the largest market revenue share of 69.5% in 2025, driven by increasing global incidence of cervical cancer. Government-led HPV vaccination and screening campaigns significantly boost demand. Hospitals and diagnostic centers prioritize early detection programs. Rising female health awareness contributes to consistent testing rates. Technological improvements in visualization tools enhance diagnostic accuracy. Supportive reimbursement policies in developed nations strengthen adoption. Increasing collaborations between public health agencies and hospitals drive growth. Expanding screening coverage in Asia-Pacific further contributes to revenue generation.

The oral examination segment is expected to witness the fastest CAGR of 9.6% from 2026 to 2033, fueled by expanding applications beyond gynecology. Growing awareness about oral cancer detection increases adoption. Dental and oncology clinics are incorporating advanced imaging tools. Technological upgrades enabling multi-specialty use strengthen growth. Rising tobacco consumption in certain regions increases oral cancer risk, boosting demand. Research initiatives exploring early oral lesion detection support expansion.

• By End User

On the basis of end user, the market is segmented into hospitals, clinics, diagnostic centers, and others. The hospitals segment accounted for the largest market revenue share of 46.7% in 2025, driven by higher patient inflow and availability of advanced infrastructure. Hospitals conduct large-scale cervical screening and diagnostic procedures. Skilled gynecologists and trained staff support efficient utilization. Integration of digital systems into hospital IT networks enhances workflow. Rising investments in women’s healthcare departments strengthen growth. Favorable reimbursement policies further boost installations.

The diagnostic centers segment is projected to witness the fastest CAGR of 10.4% from 2026 to 2033, driven by increasing demand for specialized outpatient screening services. Expansion of private diagnostic chains in emerging economies accelerates growth. Patients prefer standalone centers for faster appointments and cost-effective services. Growing preventive healthcare awareness contributes to adoption. Technological upgrades in independent labs enhance service offerings. Rising partnerships with hospitals further expand operational capacity.

Colposcopy Market Regional Analysis

- North America dominated the colposcopy market with the largest revenue share of 38.6% in 2025, characterized by well-established cervical cancer screening programs, advanced healthcare infrastructure, and high healthcare expenditure

- Healthcare providers in the region highly value the diagnostic accuracy, enhanced visualization, and early lesion detection capabilities offered by modern digital colposcopy systems

- This widespread adoption is further supported by strong reimbursement frameworks, increasing awareness of HPV-related cancers, and the presence of leading medical device manufacturers, establishing colposcopy as a critical tool in preventive gynecological care across hospitals and ambulatory surgical centers

U.S. Colposcopy Market Insight

The U.S. colposcopy market captured the largest revenue share of 81% within North America in 2025, driven by substantial growth in cervical cancer screening and HPV detection programs. The country has a well-structured preventive healthcare system that emphasizes early diagnosis of precancerous cervical lesions. Hospitals and ambulatory surgical centers are increasingly adopting digital colposcopy systems to improve imaging accuracy and patient outcomes. Rising awareness regarding women’s health and routine gynecological examinations further fuels demand. Favorable reimbursement policies and high healthcare spending strengthen market penetration. Additionally, continuous technological advancements, including portable and video colposcopes, are enhancing procedural efficiency. The strong presence of established medical device manufacturers further supports innovation and distribution across the U.S.

Europe Colposcopy Market Insight

The Europe colposcopy market is projected to expand at a substantial CAGR throughout the forecast period, supported by organized cervical cancer screening initiatives across countries such as Germany, the U.K., and France. Rising awareness of HPV vaccination and early cancer detection programs is driving procedural volumes. Healthcare providers are increasingly investing in advanced digital colposcopy equipment to enhance diagnostic precision. Government-backed public health policies and national screening guidelines strengthen adoption. Expanding gynecological care services and improved healthcare access further contribute to growth. Technological advancements in imaging systems and patient record integration are also supporting market development across the region.

U.K. Colposcopy Market Insight

The U.K. colposcopy market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by strong national cervical screening programs and increased awareness of women’s preventive healthcare. The National Health Service (NHS) plays a central role in promoting early detection of cervical abnormalities. Hospitals and specialized clinics are upgrading to digital colposcopy systems to improve workflow efficiency and documentation accuracy. Rising HPV testing rates and improved referral pathways are contributing to procedural growth. Continuous investments in healthcare modernization and training programs further enhance adoption. The U.K. remains a significant contributor to the European colposcopy landscape.

Germany Colposcopy Market Insight

The Germany colposcopy market is expected to expand at a considerable CAGR during the forecast period, supported by advanced healthcare infrastructure and increasing participation in cervical cancer screening programs. The country emphasizes early diagnosis and preventive gynecological examinations. Healthcare facilities are integrating technologically advanced colposcopes to improve image clarity and diagnostic reliability. Rising healthcare expenditure and strong insurance coverage facilitate patient access to screening services. Growing awareness campaigns regarding HPV and cervical cancer risk factors are further driving demand. Germany continues to demonstrate steady growth in women’s diagnostic healthcare services.

Asia-Pacific Colposcopy Market Insight

The Asia-Pacific colposcopy market is expected to be the fastest-growing region, projected to register a CAGR of 8.9% during the forecast period. Growth is driven by increasing government initiatives focused on women’s health screening and cervical cancer prevention. Rising healthcare investments and improving access to diagnostic services are expanding market opportunities. Countries such as China and India are witnessing higher screening participation due to growing public health awareness. Expanding hospital infrastructure and rising adoption of modern diagnostic technologies further support market growth. International collaborations and funding programs are strengthening screening capabilities in emerging economies. Asia-Pacific presents significant long-term potential for colposcopy device manufacturers.

Japan Colposcopy Market Insight

The Japan colposcopy market is gaining momentum due to growing emphasis on preventive healthcare and early cancer detection. The country’s advanced medical infrastructure supports the adoption of high-resolution digital colposcopy systems. Rising awareness of HPV infections and cervical cancer risks is encouraging routine screening among women. Government-supported health programs and improved gynecological care services further promote market growth. Technological advancements aimed at improving imaging accuracy and patient comfort are enhancing procedural outcomes. Japan continues to play a stable role within the Asia-Pacific diagnostic landscape.

China Colposcopy Market Insight

The China colposcopy market accounted for the largest revenue share in Asia-Pacific in 2025, driven by expanding healthcare infrastructure and increasing government focus on women’s health initiatives. Rising cervical cancer incidence and growing awareness campaigns are boosting screening volumes. Hospitals and diagnostic centers are adopting modern colposcopy systems to improve early detection rates. Increasing healthcare funding and expansion of public screening programs further strengthen market demand. Domestic and international manufacturers are actively expanding their presence in the country. China remains a high-growth and strategically important market within the Asia-Pacific region.

Colposcopy Market Share

The Colposcopy industry is primarily led by well-established companies, including:

• Olympus Corporation (Japan)

• Leisegang GmbH (Germany)

• CooperSurgical, Inc. (U.S.)

• ZEISS Group (Germany)

• MedGyn Products, Inc. (U.S.)

• ATMOS MedizinTechnik GmbH & Co. KG (Germany)

• DYSIS Medical (U.K.)

• Seiler Instrument Inc. (U.S.)

• Kaps GmbH & Co. KG (Germany)

• Kernel Medical Equipment Co., Ltd. (China)

• Ecleris (Argentina)

• Wallach Surgical Devices (U.S.)

• Alltion (China)

• Philips Healthcare (Netherlands)

• Edan Instruments, Inc. (China)

Latest Developments in Global Colposcopy Market

- In August 2021, DYSIS Medical announced the launch of its DYSIS View digital colposcope, an advanced cervical imaging system incorporating Dynamic Spectral Imaging (DSI) technology designed to improve the detection and mapping of cervical lesions. The system enhances visualization of abnormal tissue patterns and supports clinicians in making more accurate biopsy decisions, thereby strengthening early cervical cancer diagnosis and screening programs globally

- In May 2023, MobileODT announced the transition from its EVA 3.0 platform to the upgraded EVA System App and cloud-based Portal, enhancing its digital colposcopy ecosystem. The updated platform introduced improved image capture capabilities, secure cloud storage, remote access functionality, and better integration with electronic medical record systems, reinforcing the shift toward connected and telemedicine-enabled cervical screening solutions

- In December 2023, Olympus Corporation introduced the OCS-900 video colposcope, a next-generation digital colposcopy system designed to deliver high-resolution imaging, ergonomic usability, and electronic health record (EHR) compatibility. The device supports real-time image sharing, documentation, and training applications, making it suitable for hospitals, gynecology clinics, and academic institutions focused on cervical cancer diagnostics and education

- In June 2024, DYSIS Medical launched the DYSIS Ultra colposcopy system in Europe, integrating artificial intelligence-based decision support tools to assist clinicians in identifying and assessing cervical abnormalities. The AI-enabled system provides objective lesion mapping and color-coded analysis, aiming to reduce diagnostic variability and improve clinical outcomes in cervical cancer screening programs

- In June 2024, Bharat Serums and Vaccines (BSV) partnered with the Public Awareness Committee of the Federation of Obstetric and Gynaecological Societies of India (FOGSI) to initiate structured colposcopy training programs across multiple regions in India. The initiative focused on strengthening physician expertise in colposcopy procedures, enhancing early detection of cervical precancerous lesions, and supporting nationwide cervical cancer prevention efforts

- In July 2025, CooperSurgical expanded its women’s health portfolio through the acquisition of a telehealth solutions provider, enabling integration of remote screening capabilities with its colposcopy product offerings. This strategic move supports broader patient access to cervical diagnostic services and aligns with the growing adoption of hybrid and digital healthcare delivery model

- In September 2025, MedGyn Products entered into a strategic distribution partnership with a leading healthcare provider in Latin America to expand the availability of its colposcopy devices in emerging markets. The collaboration aims to strengthen cervical screening infrastructure in the region by improving access to both optical and digital colposcopy systems in hospitals and specialty clinics

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.