Global Continuous Glucose Monitoring Market

Размер рынка в млрд долларов США

CAGR :

%

USD

12.69 Billion

USD

41.60 Billion

2025

2033

USD

12.69 Billion

USD

41.60 Billion

2025

2033

| 2026 –2033 | |

| USD 12.69 Billion | |

| USD 41.60 Billion | |

| % | |

|

Global Continuous Glucose Monitoring Market Segmentation, By Component (Integrated Insulin Pumps, Transmitters and Receivers and Sensors), Demographics (Child Population (14 Years)), End User (Clinics and Diagnostic Centers, Home Care, Private Clinics, Hospitals and Others)- Industry Trends and Forecast to 2033

Continuous Glucose Monitoring Market Size

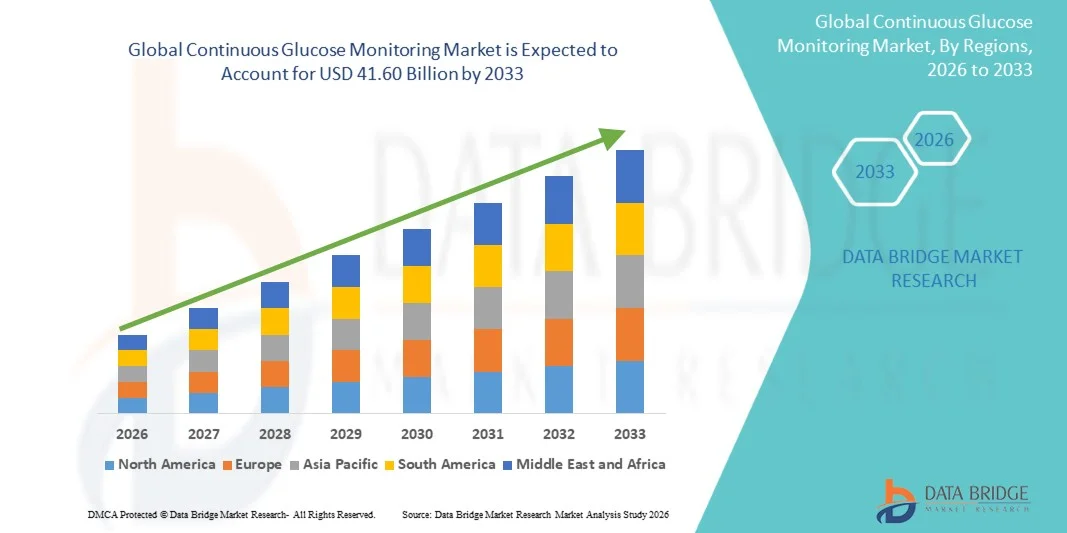

- The global continuous glucose monitoring market size was valued at USD 12.69 billion in 2025 and is expected to reach USD 41.60 billion by 2033, at a CAGR of 16.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of diabetes worldwide and continuous technological advancements in wearable healthcare devices, leading to greater adoption of real-time glucose monitoring solutions across both homecare and clinical settings. The growing shift toward digital health management and remote patient monitoring is further accelerating the integration of continuous glucose monitoring systems into routine diabetes care

- Furthermore, rising patient demand for convenient, minimally invasive, and accurate glucose tracking solutions is establishing Continuous Glucose Monitoring systems as a preferred alternative to traditional fingerstick testing methods. These converging factors are accelerating the uptake of Continuous Glucose Monitoring solutions, thereby significantly boosting the industry's growth

Continuous Glucose Monitoring Market Analysis

- Continuous Glucose Monitoring systems, offering real-time tracking of blood glucose levels through wearable sensor-based technology, have become essential tools in modern diabetes management across both homecare and clinical settings due to their accuracy, convenience, and ability to provide continuous data insights

- The escalating demand for Continuous Glucose Monitoring systems is primarily fueled by the rising global prevalence of diabetes, increasing adoption of wearable medical technologies, and a growing preference for minimally invasive glucose monitoring solutions that reduce the need for frequent fingerstick testing

- North America dominated the continuous glucose monitoring market with the largest revenue share of 44.8% in 2025, characterized by advanced healthcare infrastructure, strong reimbursement frameworks, high diabetes awareness, and the presence of leading CGM manufacturers. The U.S. experienced substantial growth in CGM adoption, particularly among Type 1 and insulin-dependent Type 2 diabetic populations, supported by technological advancements such as real-time data sharing and smartphone integration

- Asia-Pacific is expected to be the fastest-growing region in the continuous glucose monitoring market during the forecast period, projected to expand at a CAGR of 14.2%, driven by the rapidly increasing diabetic population, rising healthcare expenditure, improving access to advanced medical devices, and growing awareness regarding proactive glucose monitoring in countries such as China, India, and Japan

- The Adult Population (>14 Years) segment accounted for the largest market revenue share of 68.2% in 2025, attributed to the high prevalence of type 2 diabetes among adults globally

Report Scope and Continuous Glucose Monitoring Market Segmentation

|

Attributes |

Continuous Glucose Monitoring Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Abbott (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Continuous Glucose Monitoring Market Trends

“Advancing Real-Time Surgical Intelligence and System Interoperability”

- A prominent and rapidly evolving trend in the global AI-assisted intraoperative decision support devices market is the advancement of real-time surgical intelligence systems that integrate high-resolution imaging, predictive analytics, and machine learning algorithms directly into operating room workflows. These technologies are transforming traditional surgical environments into data-driven ecosystems capable of supporting precise and informed decision-making during complex procedures

- For instance, platforms such as Medtronic’s StealthStation navigation system enable surgeons to visualize detailed anatomical structures intraoperatively, improving procedural accuracy and reducing the risk of complications. Such systems combine imaging data with advanced analytics to guide surgical actions with enhanced confidence

- Hospitals and surgical centers are increasingly prioritizing solutions that seamlessly integrate with imaging platforms, electronic health records, and robotic-assisted surgical technologies. This interoperability ensures uninterrupted data flow, enabling clinicians to access critical patient insights without disrupting procedural efficiency

- The growing preference for minimally invasive and precision-guided surgeries is further strengthening the demand for intelligent intraoperative support systems that enhance visualization, optimize surgical pathways, and support evidence-based clinical decisions

- Manufacturers are continuously innovating to develop comprehensive platforms that merge imaging capabilities, AI-driven analytics, and predictive modeling, thereby meeting the rising complexity of surgical interventions and improving overall patient safety and outcomes

Continuous Glucose Monitoring Market Dynamics

Driver

“Rising Burden of Complex Surgical Procedures and Chronic Diseases”

- The increasing global prevalence of chronic diseases and the growing number of complex surgical procedures are key drivers accelerating the adoption of AI-assisted intraoperative decision support devices. As patient cases become more intricate, surgeons require advanced technological assistance to ensure accuracy, efficiency, and improved clinical outcomes

- For instance, Stryker’s NAV3 robotic-assisted system has been widely adopted in major hospitals across the United States to enhance orthopedic surgical precision, streamline operating room workflows, and reduce the likelihood of postoperative complications

- Healthcare institutions are investing significantly in advanced surgical technologies to minimize errors, shorten recovery times, and optimize procedural success rates. These investments are aligned with the broader shift toward value-based healthcare and outcome-driven treatment strategies

- Technological advancements, including improved imaging resolution, real-time analytics, and AI-enabled predictive insights, are strengthening intraoperative decision-making capabilities, enabling surgeons to make informed adjustments during procedures

- Furthermore, increasing healthcare expenditure, supportive government initiatives promoting advanced medical technologies, and the growing emphasis on evidence-based surgical practices are collectively contributing to the expansion of this market

Restraint/Challenge

“High Capital Investment and Regulatory Complexities”

- The substantial initial capital investment required for AI-assisted intraoperative decision support systems remains a significant barrier, particularly for smaller hospitals and surgical centers in developing regions. The cost of hardware, software integration, maintenance, and upgrades can limit accessibility despite clear clinical advantages

- Early implementations of Brainlab’s Curve Navigation system, for instance, required considerable financial commitment, making adoption challenging for budget-constrained healthcare facilities

- For instance, In addition to financial considerations, the need for specialized clinician training and workflow adaptation can slow market penetration. Integrating advanced decision support technologies into existing surgical protocols requires time, resources, and institutional commitment.

- Stringent regulatory approval processes and compliance with evolving safety and quality standards further present challenges for manufacturers seeking timely product commercialization

- Moreover, skepticism or limited awareness regarding the reliability and long-term efficacy of AI-based intraoperative systems among certain healthcare providers may restrain adoption

- Addressing these concerns through cost optimization strategies, comprehensive training programs, robust cybersecurity frameworks, and validated clinical outcome data will be critical to ensuring sustained market growth and broader acceptance

Continuous Glucose Monitoring Market Scope

The market is segmented on the basis of component, demographics, and end user.

• By Component

On the basis of component, the Continuous Glucose Monitoring market is segmented into Integrated Insulin Pumps, Transmitters & Receivers, and Sensors. The Sensors segment dominated the largest market revenue share of 49.5% in 2025, driven by their recurring usage and essential role in continuous glucose tracking. Sensors require periodic replacement, creating consistent revenue generation for manufacturers. Increasing adoption of real-time CGM systems among diabetic patients further strengthens demand. Technological advancements have improved sensor accuracy, wear duration, and patient comfort. Hospitals and homecare users prefer minimally invasive sensors with extended calibration intervals. Rising prevalence of diabetes globally significantly supports segment growth. Integration with smartphone apps and cloud platforms enhances usability. Regulatory approvals for advanced sensors also boost confidence among healthcare providers. The segment benefits from strong reimbursement support in developed markets. Continuous innovation in next-generation biosensors ensures sustained dominance.

The Integrated Insulin Pumps segment is expected to witness the fastest CAGR of 17.8% from 2026 to 2033, driven by the growing adoption of automated insulin delivery systems. Integration of CGM with insulin pumps enables closed-loop systems, improving glycemic control and reducing hypoglycemia risks. Increasing demand for artificial pancreas systems accelerates growth. Patients prefer integrated devices for convenience and reduced manual intervention. Technological advancements in smart algorithms and AI-driven glucose prediction further fuel adoption. Rising awareness of advanced diabetes management solutions supports expansion. Favorable reimbursement policies in North America and Europe strengthen market penetration. Expansion into emerging markets with growing diabetic populations contributes to rapid growth. Continuous product innovation and strategic collaborations among device manufacturers enhance segment momentum.

• By Demographics

On the basis of demographics, the Continuous Glucose Monitoring market is segmented into Child Population (≤14 Years) and Adult Population (>14 Years). The Adult Population (>14 Years) segment accounted for the largest market revenue share of 68.2% in 2025, attributed to the high prevalence of type 2 diabetes among adults globally. Sedentary lifestyles, obesity, and aging populations significantly contribute to increased adoption of CGM devices. Adults increasingly prefer continuous monitoring for better glycemic management and prevention of long-term complications. Workplace health awareness programs and physician recommendations also drive demand. Growing health consciousness and adoption of wearable technologies support segment growth. Insurance coverage for adult diabetes care enhances accessibility. Technological integration with smartphones and wearable devices improves convenience. Higher diagnosis rates in adults further strengthen dominance.

The Child Population (≤14 Years) segment is expected to witness the fastest CAGR of 16.4% from 2026 to 2033, driven by increasing incidence of type 1 diabetes among children. Parents prefer real-time CGM systems for remote monitoring and safety assurance. Integration with smartphone alerts and caregiver notifications supports adoption. Government initiatives promoting pediatric diabetes care contribute to growth. Technological advancements have improved sensor comfort and reduced invasiveness, making them suitable for children. Awareness campaigns by healthcare organizations further boost adoption. Pediatric-focused device approvals and expanding reimbursement coverage accelerate market penetration. Increasing school-based health monitoring programs also contribute to segment expansion.

• By End User

On the basis of end user, the market is segmented into Clinics and Diagnostic Centers, Home Care, Private Clinics, Hospitals, and Others. The Hospitals segment dominated with 38.9% market share in 2025, supported by advanced diabetes management programs and access to trained healthcare professionals. Hospitals use CGM devices for inpatient glucose monitoring, especially in critical care and surgical units. Availability of advanced diagnostic infrastructure encourages device adoption. Increasing hospital admissions related to diabetes complications further drive demand. Reimbursement policies and structured care protocols strengthen hospital-based usage. Physicians rely on CGM data for treatment adjustments and insulin therapy optimization. Strategic partnerships between hospitals and device manufacturers enhance availability. Growing clinical research on CGM systems also supports dominance.

The Home Care segment is anticipated to witness the fastest CAGR of 18.6% from 2026 to 2033, driven by the rising preference for self-monitoring and remote diabetes management. Patients increasingly adopt CGM devices for daily glucose tracking without frequent hospital visits. Integration with smartphones, wearable devices, and telehealth platforms supports convenience. Growing awareness about proactive diabetes control fuels demand. Favorable reimbursement and subscription-based sensor supply models accelerate adoption. Increasing internet penetration and digital literacy enhance accessibility. Technological improvements in wearable CGM systems further support growth. Expansion of home-based chronic disease management programs significantly contributes to rapid segment expansion

Continuous Glucose Monitoring Market Regional Analysis

- North America dominated the continuous glucose monitoring market with the largest revenue share of 44.8% in 2025, characterized by advanced healthcare infrastructure, strong reimbursement frameworks, high diabetes awareness, and the presence of leading CGM manufacturers such as Dexcom and Abbott

- The region’s well-established clinical guidelines and insurance coverage policies have significantly supported device adoption among diabetic patients

- Continuous technological advancements, including real-time glucose tracking, improved sensor accuracy, and seamless smartphone connectivity, have further strengthened market growth across both hospital and homecare settings

U.S. Continuous Glucose Monitoring Market Insight

The U.S. continuous glucose monitoring market captured the largest revenue share in 2025 within North America, driven by the high prevalence of diabetes and rapid adoption of advanced glucose monitoring technologies. Strong reimbursement support from public and private payers, coupled with increasing awareness among patients regarding proactive diabetes management, has accelerated CGM utilization. Adoption is particularly high among Type 1 and insulin-dependent Type 2 diabetic populations. Moreover, features such as real-time data sharing with caregivers and healthcare professionals, smartphone integration, and compatibility with insulin pumps are contributing to sustained market expansion in the country.

Europe Continuous Glucose Monitoring Market Insight

The Europe continuous glucose monitoring market is projected to expand at a substantial CAGR throughout the forecast period, supported by favorable government healthcare policies, rising diabetes prevalence, and growing emphasis on preventive care. Countries across the region are strengthening reimbursement pathways for CGM devices, encouraging broader patient access. Increasing awareness regarding continuous glucose tracking and improved patient outcomes is promoting adoption across hospitals and homecare environments. Furthermore, technological innovation and collaboration between healthcare providers and device manufacturers are reinforcing market growth.

U.K. Continuous Glucose Monitoring Market Insight

The U.K. continuous glucose monitoring market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by expanding National Health Service (NHS) support for CGM adoption and rising diabetes management initiatives. Increased focus on reducing diabetes-related complications and hospital admissions is encouraging healthcare providers to recommend real-time glucose monitoring solutions. Additionally, patient preference for minimally invasive, wearable monitoring systems and improved access through reimbursement programs are expected to sustain market growth in the country.

Germany Continuous Glucose Monitoring Market Insight

The Germany continuous glucose monitoring market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, supportive statutory health insurance coverage, and increasing digital health adoption. Germany’s focus on advanced medical technologies and structured diabetes management programs is accelerating CGM penetration. The growing acceptance of wearable health devices and emphasis on data-driven treatment decisions are further contributing to market development across both clinical and personal healthcare settings.

Asia-Pacific Continuous Glucose Monitoring Market Insight

The Asia-Pacific continuous glucose monitoring market is poised to grow at the fastest CAGR of 14.2% during the forecast period, driven by the rapidly increasing diabetic population, rising healthcare expenditure, and improving access to advanced medical technologies in countries such as China, India, and Japan. Expanding urbanization, sedentary lifestyles, and dietary changes have significantly increased diabetes incidence, creating strong demand for effective glucose monitoring solutions. Government initiatives promoting early diagnosis and disease management, along with increasing awareness regarding proactive glucose control, are further supporting regional growth.

Japan Continuous Glucose Monitoring Market Insight

The Japan continuous glucose monitoring market is gaining steady momentum due to the country’s advanced healthcare system, aging population, and strong focus on chronic disease management. Increasing prevalence of diabetes among elderly individuals is encouraging the adoption of continuous monitoring systems that offer convenience and real-time tracking. Technological sophistication, coupled with patient preference for compact and accurate wearable devices, is fostering broader integration of CGM systems into routine diabetes care.

China Continuous Glucose Monitoring Market Insight

The China continuous glucose monitoring market accounted for the largest revenue share in Asia Pacific in 2025, attributed to the country’s expanding diabetic population, growing middle class, and rapid modernization of healthcare infrastructure. Increasing awareness about continuous glucose monitoring, along with improved affordability and domestic manufacturing capabilities, is strengthening market penetration. Government efforts to enhance chronic disease management and digital health adoption are also contributing to sustained growth of the CGM market in China.

Continuous Glucose Monitoring Market Share

The Continuous Glucose Monitoring industry is primarily led by well-established companies, including:

• Abbott (U.S.)

• Dexcom, Inc. (U.S.)

• Medtronic plc (Ireland)

• Senseonics Holdings, Inc. (U.S.)

• Roche Holding AG (Switzerland)

• Ascensia Diabetes Care Holdings AG (Switzerland)

• Insulet Corporation (U.S.)

• Tandem Diabetes Care, Inc. (U.S.)

• Ypsomed AG (Switzerland)

• Novo Nordisk A/S (Denmark)

• Sanofi S.A. (France)

• B. Braun Melsungen AG (Germany)

• GlySens Incorporated (U.S.)

• Nemaura Medical Inc. (U.K.)

• AgaMatrix, Inc. (U.S.)

• LifeScan IP Holdings, LLC (U.S.)

• Terumo Corporation (Japan)

• Arkray, Inc. (Japan)

• MicroTech Medical (China)

• POCTech Co., Ltd. (China)

Latest Developments in Global Continuous Glucose Monitoring Market

- In June 2021, Abbott Laboratories announced U.S. FDA clearance for its FreeStyle Libre 2 iOS app, allowing users to receive real-time glucose alarms directly on their iPhone without requiring a separate reader device. This development enhanced user convenience and marked a significant step toward smartphone-integrated diabetes management solutions

- In December 2021, Dexcom received CE Mark approval for its Dexcom G7 Continuous Glucose Monitoring System in Europe. The G7 introduced a smaller all-in-one sensor and transmitter design with faster warm-up time, improving patient comfort and ease of use compared to previous generations

- In August 2022, Abbott Laboratories launched the FreeStyle Libre 3 system in the United States following FDA clearance. The system, recognized as one of the world’s smallest and thinnest CGM sensors, provided real-time glucose readings sent directly to a smartphone every minute, strengthening Abbott’s competitive position in the global CGM market

- In April 2023, Medtronic received U.S. FDA approval for its MiniMed 780G system with Guardian 4 sensor, an advanced hybrid closed-loop insulin delivery system that integrates CGM data with automated insulin adjustments. This approval reinforced the integration of CGM technology with automated diabetes management platforms

- In March 2024, Abbott Laboratories announced U.S. FDA clearance for Lingo and Libre Rio, two over-the-counter continuous glucose monitoring systems built on the FreeStyle Libre platform. These products expanded CGM access beyond insulin-dependent patients to broader consumer and wellness markets

- In August 2024, Dexcom launched Stelo by Dexcom, its first over-the-counter CGM designed for adults with Type 2 diabetes who do not use insulin. This strategic move significantly broadened Dexcom’s addressable market and marked an important milestone in non-prescription CGM adoption

- In October 2024, Senseonics Holdings received U.S. FDA approval for the Eversense 365 Continuous Glucose Monitoring System, the first implantable CGM designed to last up to one year. This long-duration implantable technology represented a breakthrough in reducing sensor replacement frequency and improving long-term glucose monitoring compliance

- In April 2025, Dexcom received FDA approval for the Dexcom G7 15-Day Continuous Glucose Monitoring System, extending sensor wear time while maintaining high accuracy standards. The longer wear duration aims to improve patient convenience and reduce overall device costs per day of use

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.