Global Craniomaxillofacial Implants Market

Размер рынка в млрд долларов США

CAGR :

%

USD

1.89 Billion

USD

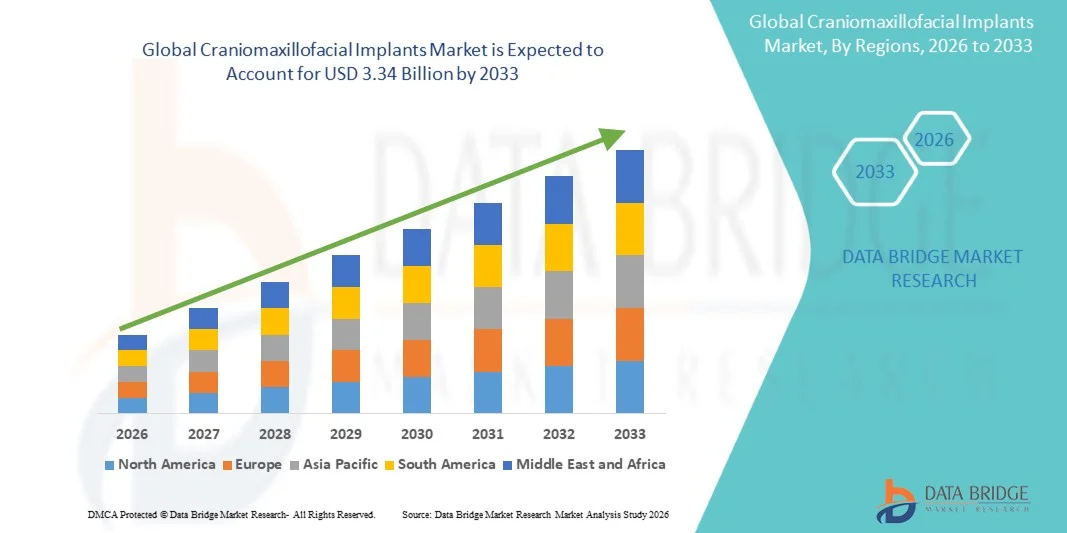

3.34 Billion

2025

2033

USD

1.89 Billion

USD

3.34 Billion

2025

2033

| 2026 –2033 | |

| USD 1.89 Billion | |

| USD 3.34 Billion | |

| % | |

|

Global Craniomaxillofacial Implants Market Segmentation, By Type (Mid Face, Plates, Screws, Mandibular Orthognathic Implants, Neuro, Mesh, Bone Graft, and Dural Repair)), Material of Construction (Calcium Phosphate Ceramics, Titanium, Alloys And Other Metals, Polymers Or Biomaterials), Material of Application Site (Internal Fixators and External Fixators), Property (Resorbable Fixators and Non-Resorbable Fixators) - Industry Trends and Forecast to 2033

Craniomaxillofacial Implants Market Size

- The global craniomaxillofacial implants market size was valued at USD 1.89 billion in 2025 and is expected to reach USD 3.34 billion by 2033, at a CAGR of 7.40% during the forecast period

- The market growth is largely fueled by the rising incidence of facial trauma, congenital craniofacial deformities, and increasing cases of road accidents and sports-related injuries, leading to a growing demand for reconstructive and corrective surgical procedures across hospitals and specialty surgical centers

- Furthermore, increasing adoption of advanced biomaterials such as titanium and bioresorbable implants, along with technological advancements in 3D printing and patient-specific implant design, is establishing craniomaxillofacial implants as essential solutions in modern reconstructive surgery. These converging factors are accelerating the uptake of craniomaxillofacial implant solutions, thereby significantly boosting the industry's growth

Craniomaxillofacial Implants Market Analysis

- Craniomaxillofacial implants, used for the fixation, reconstruction, and regeneration of facial bones and soft tissues, are increasingly vital components of modern reconstructive and trauma surgery in both hospital and specialty surgical settings due to their precision, biocompatibility, and ability to restore both function and aesthetics

- The escalating demand for craniomaxillofacial implants is primarily fueled by the rising incidence of facial trauma, increasing number of orthognathic and reconstructive surgeries, growing awareness regarding aesthetic outcomes, and technological advancements such as 3D-printed patient-specific implants

- North America dominated the craniomaxillofacial implants market with the largest revenue share of 38.6% in 2025, characterized by advanced healthcare infrastructure, high healthcare expenditure, and strong presence of leading medical device manufacturers, with the U.S. witnessing substantial procedural volumes driven by trauma cases and elective corrective surgeries

- Asia-Pacific is expected to be the fastest-growing region in the craniomaxillofacial implants market during the forecast period, projected to register a CAGR of 9.4%, due to increasing healthcare investments, rising medical tourism, growing incidence of road accidents, and improving access to advanced surgical care

- The internal fixators segment dominated with a market share of 72.4% in 2025, driven by widespread use in permanent fracture stabilization and reconstructive surgeries

Report Scope and Craniomaxillofacial Implants Market Segmentation

|

Attributes |

Craniomaxillofacial Implants Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Stryker Corporation (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Craniomaxillofacial Implants Market Trends

“Rising Adoption of 3D Printing and Patient-Specific Implants”

- A significant and accelerating trend in the global Craniomaxillofacial (CMF) Implants market is the increasing adoption of 3D printing and patient-specific implant solutions. Advances in additive manufacturing technologies are enabling the production of customized implants tailored precisely to a patient’s anatomical structure, improving surgical outcomes and aesthetic results

- For instance, companies such as Stryker Corporation and Zimmer Biomet are expanding their portfolios of patient-specific cranial and facial reconstruction implants manufactured using advanced 3D modeling and titanium printing technologies

- The integration of computer-aided design (CAD) and computer-aided manufacturing (CAM) with preoperative imaging techniques such as CT scans allows surgeons to plan procedures more accurately. Customized plates, meshes, and screws reduce intraoperative adjustments and shorten surgical time

- In addition, bioresorbable materials are gaining traction in pediatric and trauma applications, as they eliminate the need for secondary removal surgeries. Companies like Johnson & Johnson (through its DePuy Synthes division) offer advanced fixation systems designed to improve stability while supporting natural healing

- The growing demand for minimally invasive reconstructive procedures and improved cosmetic outcomes is further accelerating the development of lightweight, anatomically contoured implant systems

- This technological evolution toward precision-driven, patient-centric solutions is reshaping cranial and maxillofacial surgical practices across hospitals and specialty surgical centers

Craniomaxillofacial Implants Market Dynamics

Driver

“Increasing Incidence of Facial Trauma and Growing Demand for Reconstructive Surgeries”

- The rising prevalence of facial trauma resulting from road accidents, sports injuries, and physical assaults is a major driver for the Craniomaxillofacial Implants market. The need for effective reconstruction of facial bones and cranial defects significantly increases demand for fixation plates, screws, meshes, and distraction systems

- According to global health data referenced by organizations such as World Health Organization, road traffic injuries remain a leading cause of trauma-related hospitalizations worldwide, contributing to increased reconstructive surgical procedures

- For instance, WHO estimates indicate that millions of individuals suffer severe facial and head injuries annually due to road accidents, particularly in developing nations, thereby increasing the demand for cranial plating systems and orbital reconstruction implants

- Furthermore, the growing number of orthognathic surgeries and cosmetic facial enhancement procedures is positively influencing market expansion. Rising awareness regarding aesthetic appearance and improved access to specialized surgical care are supporting demand in both developed and emerging economies

- The increasing geriatric population is another contributing factor, as older individuals are more susceptible to fractures and degenerative bone conditions requiring surgical intervention

- Expanding healthcare infrastructure, particularly in Asia-Pacific and Latin America, along with favorable reimbursement policies in developed regions, is encouraging hospitals to adopt advanced CMF implant systems

- Continuous product innovation and surgeon training programs are further strengthening clinical adoption and supporting sustained market growth

Restraint/Challenge

“High Surgical Costs and Risk of Postoperative Complications”

- The high cost associated with craniomaxillofacial surgical procedures and implant systems remains a key restraint for market growth. Advanced titanium and customized implants can be expensive, limiting accessibility for patients in low- and middle-income regions

- In addition to implant costs, the requirement for specialized surgical expertise, operating room infrastructure, and post-operative care further increases the overall treatment expense

- For instance, patient-specific titanium cranial implants and advanced fixation systems from manufacturers such as Medtronic may involve significant procurement costs, along with expenses related to digital surgical planning and imaging, making procedures less affordable in cost-sensitive healthcare systems

- Postoperative risks such as infection, implant rejection, nerve damage, and implant failure may also pose challenges. Although technological advancements have reduced complication rates, such risks can impact patient confidence and clinical decision-making

- Stringent regulatory approval processes for implantable medical devices may delay product launches and increase compliance costs for manufacturers

- Moreover, limited availability of skilled maxillofacial surgeons in certain regions can restrict procedural volume and access to advanced reconstructive treatments

- Addressing these challenges through cost optimization, improved biomaterial development, enhanced surgical training, and streamlined regulatory pathways will be essential to ensure long-term growth in the global Craniomaxillofacial Implants market

Craniomaxillofacial Implants Market Scope

The market is segmented on the basis of type, material of construction, material of application site, and property.

• By Type

On the basis of type, the Craniomaxillofacial Implants market is segmented into mid face, plates, screws, mandibular orthognathic implants, neuro, mesh, bone graft, and dural repair. The plates segment dominated the largest market revenue share of 34.8% in 2025, driven by its extensive use in trauma fixation, fracture stabilization, and reconstructive surgeries. Plates are widely preferred due to their strength, adaptability to different anatomical contours, and compatibility with titanium and bioresorbable materials. Increasing incidences of road accidents and sports-related facial injuries have significantly contributed to demand. Surgeons rely on plates for rigid fixation and improved healing outcomes. Technological advancements such as 3D-printed patient-specific plates further enhance surgical precision. Growing healthcare expenditure in emerging economies supports segment expansion. Hospitals prefer plate systems for complex reconstructive cases due to proven clinical efficacy. The integration of advanced biomaterials improves durability and biocompatibility. Demand is also rising due to increased awareness regarding facial aesthetics and corrective surgeries. Furthermore, regulatory approvals for innovative fixation systems have accelerated product launches.

The mid face segment is anticipated to witness the fastest growth rate with a CAGR of 9.6% from 2026 to 2033, fueled by rising cases of midfacial fractures and congenital deformities. The growing demand for cosmetic reconstruction and orthognathic procedures contributes significantly to segment expansion. Increasing awareness regarding advanced surgical treatments is encouraging adoption. Technological innovations in minimally invasive surgical tools enhance patient recovery rates. Expanding access to specialized maxillofacial surgeons in developing regions further drives growth. Rising geriatric population prone to facial fractures also supports demand. Advancements in imaging and surgical planning software improve treatment precision. Surge in trauma-related hospital admissions globally contributes to segment growth. In addition, insurance coverage improvements for reconstructive procedures boost market penetration. The segment benefits from ongoing research in bioresorbable and lightweight implant materials. Hospitals increasingly adopt customized midface implants for better aesthetic outcomes. Overall, expanding reconstructive and trauma care services are key growth catalysts.

• By Material of Construction

On the basis of material of construction, the market is segmented into calcium phosphate ceramics, titanium, alloys and other metals, and polymers or biomaterials. The titanium segment accounted for the largest revenue share of 46.5% in 2025, driven by its superior strength, corrosion resistance, and excellent biocompatibility. Titanium implants are widely used due to their long-term stability and minimal risk of rejection. Surgeons prefer titanium for complex cranial and mandibular reconstructions. Its compatibility with advanced imaging techniques enhances surgical outcomes. Rising trauma cases and reconstructive surgeries boost demand for durable materials. Continuous R&D investments in titanium alloy innovations further expand applications. Healthcare providers favor titanium implants for their proven clinical success rates. Growth in medical tourism also contributes to segment dominance. The increasing number of neurosurgical and orthognathic procedures worldwide supports steady adoption. Regulatory approvals for next-generation titanium systems accelerate market penetration.

The polymers or biomaterials segment is projected to grow at the fastest CAGR of 10.8% from 2026 to 2033, owing to rising demand for lightweight and bioresorbable solutions. These materials reduce the need for secondary surgeries for implant removal. Increasing focus on patient comfort and reduced post-operative complications drives growth. Advancements in bioengineered materials improve strength and healing compatibility. Growing preference for minimally invasive procedures supports adoption. Research initiatives in biodegradable polymers enhance innovation pipelines. Surgeons are increasingly opting for biomaterials in pediatric cases. Expansion of 3D printing technology facilitates customized polymer implants. Rising awareness regarding resorbable solutions contributes to demand. Furthermore, favorable regulatory support for advanced biomaterials accelerates commercialization.

• By Material of Application Site

On the basis of material of application site, the market is segmented into internal fixators and external fixators. The internal fixators segment dominated with a market share of 72.4% in 2025, driven by widespread use in permanent fracture stabilization and reconstructive surgeries. Internal fixators provide superior stability and promote faster bone healing. Surgeons prefer internal systems due to reduced infection risk compared to external devices. Growing trauma incidence and elective cosmetic surgeries boost segment demand. Advancements in resorbable internal fixation systems further enhance growth. Hospitals increasingly adopt internal plates and screws for complex procedures. Rising availability of skilled surgeons supports expansion. Increased healthcare spending globally drives procedure volumes. The segment benefits from improved surgical instrumentation and navigation systems. Long-term success rates of internal fixation solutions ensure sustained demand.

The external fixators segment is expected to register the fastest CAGR of 8.9% from 2026 to 2033, fueled by increasing emergency trauma cases. External systems are particularly useful in severe fractures requiring temporary stabilization. Their minimally invasive placement reduces surgical complexity. Growing adoption in developing countries supports growth. Advancements in lightweight and adjustable fixator designs improve patient comfort. Increasing demand in battlefield and accident trauma care contributes to expansion. Surgeons utilize external fixators as interim solutions before definitive surgery. Rising awareness about advanced trauma management enhances uptake. Furthermore, government investments in emergency healthcare infrastructure drive segment growth.

• By Property

On the basis of property, the market is segmented into resorbable fixators and non-resorbable fixators. The non-resorbable fixators segment held the largest market share of 58.3% in 2025, driven by their durability and high mechanical strength. These implants provide long-term structural stability in major reconstructive procedures. Titanium-based non-resorbable devices are widely used across hospitals. Surgeons prefer them for complex mandibular and cranial reconstructions. Proven clinical outcomes and lower failure rates support dominance. Rising trauma surgeries globally contribute to demand. Increasing adoption in geriatric patients further strengthens growth. Technological improvements in alloy compositions enhance longevity. The segment benefits from established reimbursement frameworks.

The resorbable fixators segment is anticipated to grow at the fastest CAGR of 11.2% from 2026 to 2033, due to growing preference for implants that naturally degrade over time. These devices eliminate the need for secondary removal surgeries. Rising adoption in pediatric and cosmetic procedures drives expansion. Continuous innovation in biodegradable materials enhances product performance. Surgeons increasingly favor resorbable systems for reduced long-term complications. Expanding R&D investments accelerate commercialization of advanced solutions. Growing patient awareness regarding minimally invasive treatments supports demand. In addition, supportive regulatory pathways for bioresorbable implants further stimulate market growth.

Craniomaxillofacial Implants Market Regional Analysis

- North America dominated the craniomaxillofacial implants market with the largest revenue share of 38.6% in 2025, characterized by advanced healthcare infrastructure, high healthcare expenditure, and a strong presence of leading medical device manufacturers

- Surgeons and healthcare providers in the region highly value the precision, durability, and biocompatibility offered by modern craniomaxillofacial implant systems for trauma reconstruction and corrective procedures

- This widespread adoption is further supported by rising trauma cases, increasing demand for elective corrective and cosmetic facial surgeries, favorable reimbursement policies, and continuous technological advancements, establishing craniomaxillofacial implants as essential components in reconstructive and maxillofacial surgical care

U.S. Craniomaxillofacial Implants Market Insight

The U.S. craniomaxillofacial implants market captured the largest revenue share within North America in 2025, driven by high procedural volumes associated with facial trauma, congenital deformities, and elective corrective surgeries. Increasing incidence of road accidents and sports-related injuries significantly contributes to demand for reconstructive implants. Hospitals and ambulatory surgical centers are increasingly adopting advanced titanium and bioresorbable implant systems to improve surgical outcomes. Strong reimbursement frameworks and high healthcare spending further support market expansion. Technological innovations such as 3D-printed patient-specific implants and computer-assisted surgical planning enhance precision and efficiency. The presence of established medical device manufacturers and skilled maxillofacial surgeons reinforces the country’s leadership position.

Europe Craniomaxillofacial Implants Market Insight

The Europe craniomaxillofacial implants market is projected to expand at a substantial CAGR during the forecast period, supported by advanced surgical infrastructure and increasing reconstructive procedures. Rising prevalence of facial trauma and congenital craniofacial abnormalities drives demand for implant systems. Countries such as Germany, the U.K., and France are investing in technologically advanced surgical tools and materials. Growing adoption of minimally invasive surgical techniques further supports market growth. Favorable public healthcare systems and reimbursement structures enhance patient access to reconstructive care. Continuous innovation in biomaterials and fixation systems strengthens the regional market outlook.

U.K. Craniomaxillofacial Implants Market Insight

The U.K. craniomaxillofacial implants market is anticipated to grow at a noteworthy CAGR, driven by increasing reconstructive surgeries and trauma management procedures. The country’s healthcare system emphasizes early intervention and corrective treatments for craniofacial abnormalities. Rising demand for cosmetic and orthognathic surgeries is contributing to implant adoption. Technological advancements in fixation devices and customized implant solutions improve patient outcomes. Investments in hospital modernization and surgical training further enhance procedural efficiency. The U.K. remains an important contributor to Europe’s reconstructive surgery market.

Germany Craniomaxillofacial Implants Market Insight

The Germany craniomaxillofacial implants market is expected to expand at a considerable CAGR during the forecast period, supported by strong healthcare infrastructure and advanced surgical expertise. The country reports high volumes of maxillofacial trauma and reconstructive procedures. Increasing adoption of patient-specific implants and 3D-printed solutions enhances surgical precision. Strong collaboration between research institutions and medical device manufacturers drives innovation. Favorable insurance coverage and rising healthcare investments further support market growth. Germany continues to be a major hub for advanced reconstructive surgical technologies in Europe.

Asia-Pacific Craniomaxillofacial Implants Market Insight

The Asia-Pacific craniomaxillofacial implants market is expected to be the fastest-growing region, projected to register a CAGR of 9.4% during the forecast period. Growth is driven by increasing healthcare investments, rising incidence of road accidents, and expanding access to advanced surgical care. Countries such as China, India, and Japan are witnessing higher demand for reconstructive and cosmetic facial procedures. Growing medical tourism in emerging economies further strengthens procedural volumes. Government initiatives aimed at improving trauma care infrastructure are accelerating adoption. Expanding hospital networks and rising awareness of corrective treatments contribute to long-term growth potential.

Japan Craniomaxillofacial Implants Market Insight

The Japan craniomaxillofacial implants market is gaining momentum due to increasing demand for reconstructive and orthognathic surgeries. The country’s aging population and rising incidence of trauma cases contribute to procedural growth. Advanced healthcare infrastructure supports the adoption of high-quality titanium and bioresorbable implants. Technological innovation in surgical navigation and customized implant design enhances treatment precision. Government healthcare support and skilled surgical professionals further promote adoption. Japan continues to play a steady role within the Asia-Pacific reconstructive surgery market.

China Craniomaxillofacial Implants Market Insight

The China craniomaxillofacial implants market accounted for the largest revenue share in Asia-Pacific in 2025, driven by expanding healthcare infrastructure and rising trauma cases. Increasing road accidents and sports injuries are contributing to demand for reconstructive surgeries. Growth in cosmetic and corrective facial procedures further strengthens implant adoption. Domestic and international manufacturers are expanding their presence to meet rising demand. Improving access to tertiary care hospitals and advanced surgical technologies enhances treatment availability. China remains a high-growth and strategically significant market within the Asia-Pacific region.

Craniomaxillofacial Implants Market Share

The Craniomaxillofacial Implants industry is primarily led by well-established companies, including:

• Stryker Corporation (U.S.)

• Johnson & Johnson (U.S.)

• Zimmer Biomet Holdings, Inc. (U.S.)

• Medtronic plc (Ireland)

• Smith & Nephew plc (U.K.)

• B. Braun Melsungen AG (Germany)

• OsteoMed (U.S.)

• KLS Martin Group (Germany)

• Matrix Surgical USA (U.S.)

• Medartis AG (Switzerland)

• Biomet Microfixation (U.S.)

• Acumed LLC (U.S.)

• Jeil Medical Corporation (South Korea)

• Integra LifeSciences (U.S.)

• Anika Therapeutics (U.S.)

Latest Developments in Global Craniomaxillofacial Implants Market

- In February 2021, Stryker Corporation announced the expansion of its Virtual Surgical Planning (VSP) Orthognathics platform for craniomaxillofacial procedures, enhancing its portfolio of patient-specific implants and cutting guides. The platform integrates advanced 3D imaging, surgical simulation, and customized implant manufacturing to improve anatomical accuracy, reduce intraoperative adjustments, and enhance post-surgical outcomes in complex craniofacial reconstructions

- In April 2022, Zimmer Biomet Holdings, Inc. completed the acquisition of Embody, Inc., a regenerative medicine company specializing in collagen-based healing solutions. Although focused broadly on soft tissue healing, this acquisition strengthened Zimmer Biomet’s biologics and reconstruction portfolio, supporting craniomaxillofacial procedures that require advanced healing and fixation support

- In March 2023, KLS Martin Group expanded its IPS (Individual Patient Solutions) portfolio with new 3D-printed patient-specific titanium cranial and facial implants. Manufactured using additive manufacturing technology, these implants are tailored from patient CT data, enabling precise defect reconstruction, improved contour matching, and reduced surgical time in trauma and oncologic reconstruction cases

- In September 2023, Johnson & Johnson MedTech (through DePuy Synthes) highlighted advancements in its TRUMATCH CMF Solutions, integrating digital surgical planning with customized implant fabrication. The system enhances workflow efficiency by combining preoperative planning software, 3D-printed guides, and patient-specific implants to improve precision in mandibular and midface reconstruction procedures

- In May 2024, Zimmer Biomet received U.S. FDA 510(k) clearance for an expanded craniomaxillofacial plating system designed to improve fixation strength and intraoperative flexibility. The updated system offers enhanced screw geometry and low-profile plate design to reduce soft tissue irritation while maintaining structural stability in facial trauma repair

- In July 2024, OsteoMed announced the commercial availability of its bioresorbable craniofacial fixation system in the United States. The system is specifically designed for pediatric craniofacial reconstruction, gradually resorbing over time to eliminate the need for secondary implant removal surgery, which is particularly beneficial in growing patients

- In January 2025, Stryker Corporation expanded its CMF portfolio with enhancements to its custom cranial implant solutions, incorporating improved 3D-printing materials and faster production timelines. The upgrades were aimed at accelerating delivery of patient-matched implants for trauma and neurosurgical applications, addressing growing demand for personalized reconstructive solutions

- In March 2025, Medtronic plc advanced its cranial reconstruction offerings by integrating improved surgical navigation compatibility with its cranial implant systems. The integration allows surgeons to combine implant placement with real-time navigation technology, enhancing surgical precision in complex craniomaxillofacial and neurosurgical procedures

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.