Global Cryocooler Market

Размер рынка в млрд долларов США

CAGR :

%

USD

3.26 Billion

USD

5.13 Billion

2025

2033

USD

3.26 Billion

USD

5.13 Billion

2025

2033

| 2026 –2033 | |

| USD 3.26 Billion | |

| USD 5.13 Billion | |

| % | |

|

Global Cryocooler Market Segmentation, By Offering (Hardware and Services), Type (Gifford-Mcmahon Cryocoolers, Pulse-Tube Cryocoolers, Stirling Cryocoolers, Stirling Cryocoolers, and Brayton Cryocoolers), Heat Exchanger Type (Recuperative Heat Exchangers and Regenerative Heat Exchangers), Operating Cycle (Open-Loop-Cycle Cryocoolers and Closed-Loop-Cycle Cryocoolers), Temperature Range (1K-5K, 5.1K-10K, 10.1K-50K, 50.1K-100K, and 100.1K-300K), End User (Military, Medical, Commercial, Environmental, Energy, Transport, Research and Development, Space, Agriculture and Biology, Mining and Metal, and Others) - Industry Trends and Forecast to 2033

Cryocooler Market Size

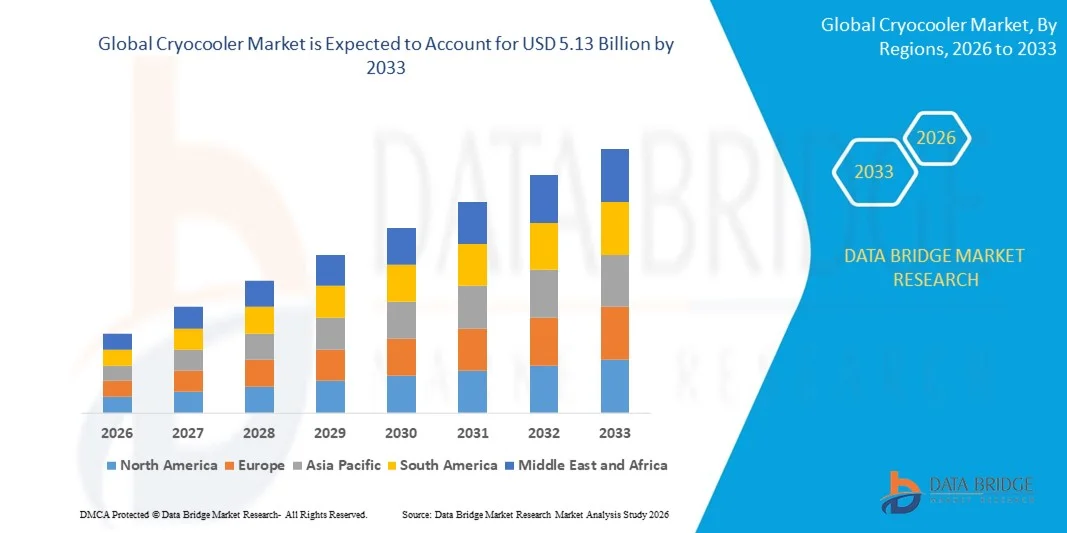

- The global cryocooler market size was valued at USD 3.26 billion in 2025 and is expected to reach USD 5.13 billion by 2033, at a CAGR of 5.80% during the forecast period

- The market growth is largely driven by increasing demand for ultra-low temperature cooling solutions across advanced applications such as quantum computing, space exploration, defense, and medical imaging. Technological advancements in cryogenic systems are enabling higher efficiency, lower vibration, and more compact designs, which are expanding adoption across research, industrial, and commercial sectors

- Furthermore, rising investments in satellite programs, quantum research, superconducting devices, and high-performance infrared sensors are creating strong demand for reliable and high-precision cryocoolers. These converging factors are accelerating the uptake of cryogenic cooling solutions, thereby significantly boosting the market’s growth potential

Cryocooler Market Analysis

- Cryocoolers, providing highly efficient cooling at cryogenic temperatures, are increasingly critical for applications in medical imaging (MRI), space and defense systems, quantum computing, and laboratory research due to their ability to maintain stable low-temperature environments for sensitive instruments and detectors

- The escalating demand for cryocoolers is primarily fueled by advancements in compact and low-vibration designs, increasing global space and defense initiatives, expanding research in quantum and superconducting technologies, and the need for highly reliable cooling in mission-critical applications

- North America dominated the cryocooler market with a share of 35.01% in 2025, due to strong demand from defense, space exploration, and advanced medical imaging sectors

- Asia-Pacific is expected to be the fastest growing region in the cryocooler market during the forecast period due to rising satellite launches, expanding defense budgets, and increasing healthcare infrastructure investments

- Closed-loop-cycle cryocoolers segment dominated the market with a market share of 68.59% in 2025, due to its efficiency and ability to recirculate working gases without continuous replenishment. Closed-loop systems are widely used in space missions, medical imaging, and defense equipment due to their reliability and controlled operating environment. Their reduced operational costs and suitability for long-duration applications contribute to their dominant position

Report Scope and Cryocooler Market Segmentation

|

Attributes |

Cryocooler Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Cryocooler Market Trends

Adoption of Cryocoolers in Quantum Computing and Space

- A key trend in the cryocooler market is the expanding adoption of cryogenic cooling systems in quantum computing and space applications, driven by the increasing need for ultra-low temperature environments to enable precise experimental and operational outcomes. Cryocoolers are becoming indispensable for maintaining superconducting qubits and sensitive space instrumentation at temperatures close to absolute zero

- For instance, companies such as Bluefors supply cryogenic systems that are widely used in quantum computing research facilities, ensuring stable low-temperature environments for superconducting qubit operations. These systems enhance coherence times and improve experimental reliability in complex quantum architectures

- The space industry is integrating advanced cryocoolers into satellite payloads and infrared detection systems, where extremely low temperatures are required to minimize thermal noise and enhance sensor performance. This is positioning cryocoolers as critical components for satellite imaging, astronomical observation, and space exploration missions

- In medical and scientific research, cryocoolers are increasingly deployed in MRI systems, superconducting magnet applications, and particle physics laboratories. Applications such as cryogenic MRI scanners and particle detectors rely on reliable, low-vibration cooling solutions to maintain performance and measurement accuracy

- Industrial sectors focusing on precision manufacturing and superconducting technologies are adopting cryocoolers to support processes that require highly stable temperature control. This trend is driving demand for compact, energy-efficient, and low-maintenance cryogenic solutions capable of operating under continuous load

- The market is witnessing growth in high-reliability cooling applications where cryocoolers contribute to maintaining extreme environmental conditions essential for advanced research and space missions. The increasing deployment of these systems is reinforcing the critical role of cryocoolers in enabling next-generation scientific and technological advancements

Cryocooler Market Dynamics

Driver

Rising Demand for Ultra-Low Temperature Cooling

- The growing demand for ultra-low temperature cooling in quantum computing, space exploration, and advanced scientific research is driving the need for high-performance cryocoolers. These systems are essential for applications that require precise temperature control below 10 K, where conventional refrigeration methods are ineffective

- For instance, companies such as Sumitomo Heavy Industries provide pulse tube cryocoolers that support space telescopes and quantum computing laboratories, enabling extended operation of sensitive instruments. These cryocoolers improve system stability and reduce thermal noise in critical applications

- The rising investments in quantum computing initiatives worldwide are increasing the deployment of cryogenic systems for maintaining superconducting qubit coherence. Stable low-temperature environments directly enhance computational performance and experimental reliability

- Expansion in space missions, including satellite-based infrared sensors and deep-space probes, is boosting demand for cryocoolers capable of long-term, vibration-free operation. These systems ensure the accuracy of thermal imaging and observation equipment in extreme conditions

- Sustained focus on research and development in cryogenics continues to support the growth of cryocooler adoption. The increasing expectation for stable ultra-low temperature environments reinforces cryocoolers as indispensable components for advanced technology and scientific exploration

Restraint/Challenge

High Costs and Maintenance Complexity

- The cryocooler market faces challenges due to high costs and complex maintenance requirements associated with precision cryogenic systems. Advanced cryocoolers demand specialized materials, precise engineering, and skilled operation, which increases capital expenditure and operational overheads

- For instance, Northrop Grumman produces space-qualified cryocoolers for satellite and defense applications that involve rigorous testing and maintenance protocols. The specialized nature of these systems contributes to elevated production and service costs, limiting adoption in cost-sensitive projects

- Maintaining cryocoolers requires careful monitoring of performance, periodic servicing, and strict adherence to operational protocols to avoid system failure. This complexity can extend downtime and increase total cost of ownership for end-users

- The reliance on advanced components such as low-vibration compressors, superconducting materials, and pulse-tube assemblies further complicates manufacturing and maintenance processes. Supply chain limitations and high component costs affect the economic feasibility for some applications

- Scaling cryocooler deployment while ensuring reliability and long-term operational efficiency remains a significant challenge. These constraints collectively require manufacturers and end-users to balance performance, cost, and maintainability to support sustainable market growth

Cryocooler Market Scope

The market is segmented on the basis of offering, type, heat exchanger type, operating cycle, temperature range, and end user.

- By Offering

On the basis of offering, the cryocooler market is segmented into hardware and services. The hardware segment dominated the market with the largest revenue share in 2025, driven by high demand for compressors, cold heads, and control electronics across medical imaging, space instruments, and defense surveillance systems. Cryocooler hardware forms the core functional component of cooling systems, requiring precision engineering and advanced materials to achieve ultra-low temperatures. Continuous procurement of integrated cryocooler units for MRI systems, infrared sensors, and satellite payloads further strengthens hardware demand across developed and emerging economies.

The services segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing need for maintenance, performance optimization, and lifecycle extension of installed cryocooler systems. As cryocoolers operate in critical and remote environments, regular servicing and system upgrades are essential to ensure reliability and minimize downtime. Growing deployment in space missions, research laboratories, and defense applications is accelerating demand for long-term service contracts and technical support solutions.

- By Type

On the basis of type, the cryocooler market is segmented into Gifford-McMahon cryocoolers, pulse-tube cryocoolers, Stirling cryocoolers, and Brayton cryocoolers. The Gifford-McMahon cryocoolers segment dominated the market in 2025 due to its widespread use in MRI systems, laboratory research, and semiconductor manufacturing. These systems are valued for their ability to achieve low temperatures with stable and continuous cooling performance. Their proven reliability and established integration in medical and industrial systems contribute significantly to their large installed base.

The pulse-tube cryocoolers segment is expected to witness the fastest growth from 2026 to 2033, driven by advantages such as lower vibration, higher reliability, and reduced maintenance requirements. Pulse-tube technology is increasingly preferred in space and military applications where minimal mechanical disturbance and long operational life are critical. Expanding adoption in infrared imaging systems and satellite-based sensors is further accelerating segment growth.

- By Heat Exchanger Type

On the basis of heat exchanger type, the cryocooler market is segmented into recuperative heat exchangers and regenerative heat exchangers. The regenerative heat exchangers segment dominated the market in 2025, as most cryocooler designs such as Stirling and Gifford-McMahon systems rely on regenerative processes to achieve efficient heat transfer. These exchangers enhance thermal efficiency by cyclically storing and releasing heat, enabling effective low-temperature performance. Their compatibility with compact and high-performance cryocooler systems supports their broad adoption across medical and defense sectors.

The recuperative heat exchangers segment is projected to register the fastest growth from 2026 to 2033, supported by increasing demand for continuous-flow cryogenic systems. Recuperative designs are gaining attention in advanced aerospace and energy applications where steady-state cooling and improved thermal control are required. Technological advancements in materials and microchannel designs are further strengthening their growth potential.

- By Operating Cycle

On the basis of operating cycle, the cryocooler market is segmented into open-loop-cycle cryocoolers and closed-loop-cycle cryocoolers. The closed-loop-cycle cryocoolers segment dominated the market with the largest share of 68.59% in 2025, driven by its efficiency and ability to recirculate working gases without continuous replenishment. Closed-loop systems are widely used in space missions, medical imaging, and defense equipment due to their reliability and controlled operating environment. Their reduced operational costs and suitability for long-duration applications contribute to their dominant position.

The open-loop-cycle cryocoolers segment is expected to witness the fastest growth from 2026 to 2033, supported by niche scientific and experimental applications requiring expendable cryogenic fluids. These systems are preferred in certain laboratory and aerospace testing scenarios where ultra-low temperatures are needed for short durations. Increasing research activities in quantum computing and particle physics are encouraging selective adoption of open-loop configurations.

- By Temperature Range

On the basis of temperature range, the cryocooler market is segmented into 1K–5K, 5.1K–10K, 10.1K–50K, 50.1K–100K, and 100.1K–300K. The 50.1K–100K segment dominated the market in 2025 due to its extensive use in infrared detectors, space imaging systems, and superconducting devices. This temperature range supports a wide range of commercial and military cooling requirements while maintaining system efficiency. Strong demand from aerospace and surveillance applications reinforces its leading revenue share.

The 1K–5K segment is anticipated to witness the fastest growth from 2026 to 2033, driven by expanding research in quantum technologies and superconducting electronics. Achieving ultra-low temperatures within this range is critical for advanced scientific experiments and next-generation computing systems. Increasing government funding and private investments in quantum research are accelerating adoption of cryocoolers operating in this range.

- By End User

On the basis of end user, the cryocooler market is segmented into military, medical, commercial, environmental, energy, transport, research and development, space, agriculture and biology, mining and metal, and others. The medical segment dominated the market in 2025, primarily due to high adoption of cryocoolers in MRI systems and advanced diagnostic imaging equipment. Growing healthcare infrastructure investments and increasing demand for non-invasive imaging solutions continue to drive installations globally. The consistent need for reliable and efficient cooling in medical devices ensures sustained revenue generation from this segment.

The space segment is projected to witness the fastest growth from 2026 to 2033, fueled by rising satellite launches and deep-space exploration programs. Cryocoolers are essential for cooling infrared sensors, space telescopes, and onboard scientific instruments operating in extreme environments. Expanding public and private space initiatives are significantly contributing to the rapid growth of this segment.

Cryocooler Market Regional Analysis

- North America dominated the cryocooler market with the largest revenue share of 35.01% in 2025, driven by strong demand from defense, space exploration, and advanced medical imaging sectors

- The presence of established aerospace agencies, defense contractors, and leading medical device manufacturers supports continuous procurement of cryogenic cooling systems

- Significant investments in infrared surveillance, satellite programs, and superconducting research further strengthen regional market growth

U.S. Cryocooler Market Insight

The U.S. cryocooler market captured the largest revenue share within North America in 2025, fueled by high defense expenditure and expanding space exploration initiatives. Increasing deployment of cryocoolers in missile guidance systems, space telescopes, and MRI equipment is accelerating adoption. Strong presence of aerospace research organizations and government-backed innovation programs continues to support technological advancements and commercial demand.

Europe Cryocooler Market Insight

The Europe cryocooler market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by growing investments in space missions, scientific research, and advanced healthcare infrastructure. Rising focus on environmental monitoring and energy-efficient cooling technologies is encouraging adoption across research institutions and industrial applications. Integration of cryocoolers into satellite payloads and laboratory-grade analytical instruments is further supporting regional growth.

U.K. Cryocooler Market Insight

The U.K. cryocooler market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by increasing investments in space research, quantum technology development, and defense modernization programs. The country’s expanding focus on advanced sensor technologies and satellite manufacturing is creating steady demand for compact and reliable cryogenic cooling systems. Collaboration between research universities and aerospace companies is also strengthening domestic adoption.

Germany Cryocooler Market Insight

The Germany cryocooler market is expected to expand at a considerable CAGR during the forecast period, driven by strong industrial research capabilities and advanced medical technology manufacturing. Germany’s emphasis on precision engineering and scientific instrumentation supports integration of cryocoolers into laboratory equipment and semiconductor applications. Growing focus on space research and high-performance imaging systems further contributes to market expansion.

Asia-Pacific Cryocooler Market Insight

The Asia-Pacific cryocooler market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rising satellite launches, expanding defense budgets, and increasing healthcare infrastructure investments. Rapid industrialization and technological advancements in countries such as China, Japan, and India are accelerating adoption of cryogenic systems. Expanding domestic manufacturing capabilities and government support for space and research initiatives are further propelling regional growth.

Japan Cryocooler Market Insight

The Japan cryocooler market is gaining momentum due to the country’s strong presence in space exploration, electronics manufacturing, and advanced research activities. Increasing development of infrared sensors, superconducting devices, and scientific instruments is driving demand for efficient cryogenic cooling technologies. Continuous innovation in compact and low-vibration cryocooler systems supports adoption across aerospace and laboratory applications.

China Cryocooler Market Insight

The China cryocooler market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid expansion of the space sector, growing defense modernization, and strong government-backed research programs. China’s increasing satellite deployments and investments in quantum communication technologies are generating high demand for advanced cryogenic systems. Presence of domestic manufacturers and expanding industrial base further strengthen the country’s market position.

Cryocooler Market Share

The cryocooler industry is primarily led by well-established companies, including:

- Sumitomo Heavy Industries, Ltd. (Japan)

- Chart Industries (U.S.)

- AMETEK, Inc. (U.S.)

- Cryomech Inc. (U.S.)

- Northrop Grumman (U.S.)

- Advanced Research Systems, Inc. (U.S.)

- RICOR (Israel)

- Air Liquide (France)

- Oxford Cryosystems (U.K.)

- Creare (U.S.)

- Lihan Cryogenic Technology Co., Ltd. (China)

- Tristan Technologies, Inc. (U.S.)

- Vacree Technologies Co., Ltd. (China)

- Honeywell International LLC (U.S.)

- Fabrum Solutions (U.S.)

- Acme Cryogenics (U.S.)

- Brooks Automation Inc. (U.S.)

- Thales Cryogenics (France)

- L3HARRIS, INC (U.S.)

Latest Developments in Global Cryocooler Market

- In July 2025, Bluefors introduced a millikelvin Cryo-CMOS system integrating readout electronics at 4 kelvin, enabling quantum processors to scale beyond 1,000 qubits per device. This advancement significantly enhances the efficiency and scalability of quantum computing infrastructure by reducing thermal noise and improving signal integrity at ultra-low temperatures. The development strengthens demand for high-performance dilution refrigerators and advanced cryogenic platforms, reinforcing the cryocooler market’s role in supporting next-generation quantum technologies and large-scale research facilities

- In July 2025, Honeywell Aerospace secured production contracts from the U.S. Department of Defense under the CRUISE and QUEST programs for quantum-sensor navigation systems. These contracts accelerate the deployment of precision navigation technologies that rely on stable cryogenic cooling for enhanced sensitivity and operational reliability. The initiative expands opportunities for compact, rugged cryocoolers in defense applications, contributing to sustained procurement and long-term growth in the aerospace and military segments

- In March 2025, Bluefors and Qblox signed a memorandum of understanding to co-develop low-dissipation control architectures for high-density quantum processors. This collaboration focuses on minimizing thermal load within cryogenic environments, enabling more qubits to operate efficiently within a single cooling system. The agreement promotes innovation in integrated cryogenic and control solutions, strengthening the ecosystem for scalable quantum computing and expanding commercial prospects for advanced cryocooler technologies

- In March 2025, DRDO and the Indian Army agreed to indigenize 0.5 watt Stirling cryocoolers with 70% local content by value. This move enhances domestic production capabilities and supports strategic self-reliance in critical defense technologies. The initiative is expected to stimulate local supply chains, reduce dependence on imports, and create new growth avenues for cryocooler manufacturers serving military surveillance and thermal imaging applications

- In January 2025, Lockheed Martin expanded its investment in next-generation infrared sensor payloads for satellite-based surveillance programs. These advanced payloads require highly reliable and vibration-controlled cryocoolers to maintain optimal detector performance in space environments. The expansion underscores rising demand for space-qualified cryogenic cooling systems, reinforcing long-term market growth driven by increasing satellite launches and global defense modernization efforts

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.