Global Dairy Free Yogurt Market

Размер рынка в млрд долларов США

CAGR :

%

USD

11.66 Billion

USD

45.98 Billion

2025

2033

USD

11.66 Billion

USD

45.98 Billion

2025

2033

| 2026 –2033 | |

| USD 11.66 Billion | |

| USD 45.98 Billion | |

| % | |

|

Global Dairy-Free Yogurt Market Segmentation, By, Type (Almond, Coconut, Cashew, Soy, Oat, Hemp, Rice, and Others), Flavour (Original/Plain, Vanilla, Strawberry, Blueberry, Mango, Raspberry, and Peach), Category (Conventional and Organic), Packaging Type (Tubs, Pouches, and Others), End-User (Household and Food Service Industry), Distribution Channel (Store Based and Non-Store Based)- Industry Trends and Forecast to 2033

Dairy-Free Yogurt Market Size

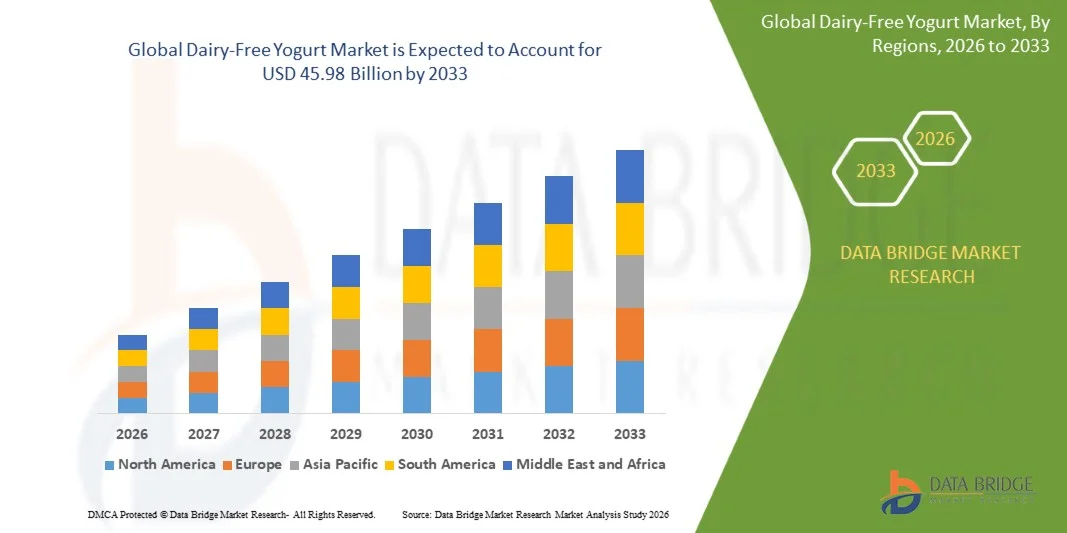

- The global dairy-free yogurt market size was valued at USD 11.66 billion in 2025 and is expected to reach USD 45.98 billion by 2033, at a CAGR of 18.70% during the forecast period

- The market growth is largely fuelled by the rising consumer preference for plant-based and lactose-free alternatives, coupled with increasing awareness of health and wellness benefits

- Growing adoption of vegan and clean-label diets, along with expansion in retail and e-commerce channels, is further driving market demand

Dairy-Free Yogurt Market Analysis

- Increasing health consciousness and dietary restrictions are boosting the popularity of dairy-free yogurt across all age groups

- The surge in plant-based milk alternatives, such as almond, soy, coconut, and oat milk, is fueling product development and market expansion

- North America dominated the dairy-free yogurt market with the largest revenue share of 38.5% in 2025, driven by growing health awareness, increasing lactose intolerance, and the rising adoption of plant-based diets

- The Asia-Pacific region is expected to witness the highest growth rate in the global dairy-free yogurt market, driven by rising disposable incomes, increasing urbanization, and growing health consciousness. The region’s expanding middle class, government initiatives promoting healthy diets, and demand for plant-based alternatives are accelerating market adoption

- The Almond segment held the largest market revenue share in 2025, driven by its high nutritional content, creamy texture, and widespread consumer preference as a versatile dairy alternative. Almond-based yogurts are rich in vitamin E, calcium, and protein, which support bone health and immunity. They are often fortified with probiotics, enhancing digestive health. Moreover, their neutral taste makes them ideal for both sweet and savory preparations, appealing to a wide demographic

Report Scope and Dairy-Free Yogurt Market Segmentation

|

Attributes |

Dairy-Free Yogurt Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Danone SA (France) |

|

Market Opportunities |

• Expansion Of Vegan And Plant-Based Product Lines |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Dairy-Free Yogurt Market Trends

“Rising Demand For Plant-Based And Functional Yogurts”

• The growing focus on plant-based diets and health-conscious eating habits is significantly shaping the dairy-free yogurt market, as consumers increasingly prefer alternatives that are free from lactose, dairy, and synthetic additives. Dairy-free yogurts are gaining traction due to their ability to provide nutritional value, enhanced texture, and digestive benefits, encouraging manufacturers to innovate with new formulations that cater to evolving consumer preferences

• Increasing awareness around gut health, immunity, and sustainable consumption has accelerated the demand for dairy-free yogurts in functional beverages, desserts, and breakfast products. Health-oriented consumers and environmentally aware populations are actively seeking products formulated with plant-based or fortified ingredients, prompting brands to prioritize clean-label sourcing and eco-friendly production processes

• Sustainability and clean-label trends are influencing purchasing decisions, with manufacturers emphasizing transparent labeling, eco-conscious production, and certification. These factors help brands differentiate products in a competitive market, build consumer trust, and drive adoption of organic, non-GMO, and allergen-free labeling. Marketing campaigns often highlight these benefits to reinforce brand positioning and appeal to health- and eco-conscious consumers

• For instance, in 2024, Danone in France and Alpro in Belgium expanded their dairy-free yogurt portfolios by incorporating oat, almond, and soy-based formulations. These launches responded to rising consumer preference for plant-based alternatives, with distribution across retail, specialty, and online channels. Products were also marketed as environmentally responsible and nutrient-rich, enhancing brand loyalty and repeat purchases among target audiences

• While demand for dairy-free yogurts is growing, sustained market expansion depends on continuous R&D, cost-effective production, and maintaining sensory and nutritional performance comparable to dairy counterparts. Manufacturers are focusing on improving scalability, shelf-life stability, and developing innovative flavors and fortifications to balance cost, quality, and consumer expectations for broader adoption

Dairy-Free Yogurt Market Dynamics

Driver

“Rising Consumer Preference For Plant-Based And Functional Products”

• Growing consumer interest in lactose-free, plant-based, and functional food products is a major driver for the dairy-free yogurt market. Manufacturers are increasingly offering dairy-free alternatives to meet clean-label, allergen-free, and nutrition-focused requirements, supporting product diversification and market growth

• Expanding applications in breakfast, snacks, desserts, and fortified beverages are influencing market growth. Dairy-free yogurts help provide protein, fiber, probiotics, and functional benefits while maintaining the natural positioning of products, enabling manufacturers to meet consumer expectations for high-quality, health-oriented offerings

• Food and beverage manufacturers are actively promoting dairy-free yogurt-based formulations through product innovation, marketing campaigns, and industry certifications. These efforts are supported by growing consumer preference for healthy, sustainable, and convenient products, and encourage partnerships between ingredient suppliers and brands to improve taste, texture, and nutritional performance

• For instance, in 2023, Danone in France and Oatly in Sweden reported increased incorporation of plant-based dairy-free yogurts in breakfast and dessert segments. This expansion followed higher consumer demand for lactose-free, non-GMO, and fortified products, driving repeat purchases and product differentiation. Both companies also highlighted sustainability and traceability in marketing campaigns to strengthen consumer trust and brand loyalty

• Although rising plant-based and functional trends support growth, wider adoption depends on cost optimization, ingredient availability, and scalable production processes. Investment in supply chain efficiency, sustainable sourcing, and advanced formulation technology will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

“Higher Cost And Limited Awareness Compared To Conventional Yogurts”

• The relatively higher cost of dairy-free yogurts compared to conventional dairy yogurts remains a key challenge, limiting adoption among price-sensitive consumers. Higher raw material costs and complex processing methods contribute to elevated pricing. In addition, fluctuating supply of certified plant-based ingredients can further affect cost stability and market penetration

• Consumer and manufacturer awareness remains uneven, particularly in developing markets where plant-based demand is still emerging. Limited understanding of functional benefits restricts adoption across certain product categories. This also leads to slower innovation uptake in emerging economies where educational initiatives on dairy-free alternatives are minimal

• Supply chain and distribution challenges also impact market growth, as dairy-free yogurts require sourcing from certified suppliers and adherence to stringent quality standards. Logistical complexities, storage requirements, and shorter shelf life of some plant-based yogurts increase operational costs. Companies must invest in cold storage, proper handling, and efficient transport networks to maintain product integrity

• For instance, in 2024, distributors in Singapore and Thailand supplying dairy-free brands such as Alpro and Oatly reported slower uptake due to higher prices and limited awareness of functional advantages compared to conventional dairy yogurts. Cold storage requirements and certification compliance were additional barriers, which prompted some retailers to limit shelf space for premium dairy-free yogurt products, affecting visibility and sales

• Overcoming these challenges will require cost-efficient production, expanded distribution networks, and focused educational initiatives for manufacturers and consumers. Collaboration with retailers, foodservice operators, and certification bodies can help unlock the long-term growth potential of the global dairy-free yogurt market. Furthermore, developing cost-competitive formulations and strengthening marketing strategies around functional and sustainability benefits will be essential for widespread adoption

Dairy-Free Yogurt Market Scope

The market is segmented on the basis of type, flavour, category, packaging type, end-user, and distribution channel.

• By Type

On the basis of type, the dairy-free yogurt market is segmented into Almond, Coconut, Cashew, Soy, Oat, Hemp, Rice, and Others. The Almond segment held the largest market revenue share in 2025, driven by its high nutritional content, creamy texture, and widespread consumer preference as a versatile dairy alternative. Almond-based yogurts are rich in vitamin E, calcium, and protein, which support bone health and immunity. They are often fortified with probiotics, enhancing digestive health. Moreover, their neutral taste makes them ideal for both sweet and savory preparations, appealing to a wide demographic.

The Oat segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its sustainable sourcing, rich fiber content, and ability to offer a naturally creamy texture. Oat-based yogurts are increasingly adopted in plant-based diets, appealing to environmentally conscious consumers. They provide heart-healthy benefits and promote gut health due to soluble fibers. In addition, oat yogurts are often flavored to match consumer preferences, enhancing their market attractiveness.

• By Flavour

On the basis of flavour, the market is segmented into Original/Plain, Vanilla, Strawberry, Blueberry, Mango, Raspberry, and Peach. The Original/Plain segment held the largest market share in 2025, driven by its versatility for consumption and use in cooking or smoothies. It serves as a base for adding natural sweeteners, fruits, or nuts. Consumers prefer plain dairy-free yogurt for controlling sugar intake while retaining the health benefits of probiotics. It is also widely used in recipes and meal preparations, increasing its demand across households.

The Strawberry segment is expected to register the fastest growth from 2026 to 2033, driven by its natural sweetness, appealing color, and popularity among children and young adults. Strawberry-flavored yogurts are often fortified with antioxidants and vitamins. Their ready-to-eat convenience makes them a preferred choice for breakfast or snacks. In addition, attractive packaging and promotional campaigns further drive consumer adoption.

• By Category

On the basis of category, the market is segmented into Conventional and Organic. The Conventional segment held the largest market revenue share in 2025 due to its widespread availability and cost-effectiveness. Conventional dairy-free yogurts are manufactured with optimized production techniques, ensuring consistency in taste and texture. They offer a wide variety of flavors and packaging options, catering to diverse consumer preferences. Moreover, they are often fortified with essential nutrients, enhancing their nutritional appeal.

The Organic segment is expected to witness the fastest growth from 2026 to 2033, driven by rising consumer preference for chemical-free, sustainably sourced ingredients. Organic dairy-free yogurts are often labeled with certifications, enhancing consumer trust. They appeal to health-conscious and environmentally aware consumers seeking natural and premium products. Their production involves minimal processing and no synthetic additives, aligning with clean-label trends. Organic yogurts also attract premium pricing, contributing to market growth.

• By Packaging Type

On the basis of packaging type, the market is segmented into Tubs, Pouches, and Others. The Tubs segment held the largest market share in 2025, driven by its convenience for household consumption and compatibility with various storage and serving needs. Tub packaging allows consumers to easily portion servings, store in refrigerators, and incorporate yogurt into recipes. Large tub sizes are preferred by families, contributing to steady sales. The packaging is also reusable in some cases, aligning with sustainable consumption trends.

The Pouches segment is expected to witness the fastest growth from 2026 to 2033, driven by their portability, single-serve convenience, and appeal to on-the-go consumers. Pouch packaging is increasingly used for children's snacks, travel-friendly portions, and ready-to-eat options. Innovative designs, squeezable features, and attractive graphics further boost consumer engagement. These pouches are also easier to ship and distribute, enhancing online and retail sales channels.

• By End-User

On the basis of end-user, the market is segmented into Household and Food Service Industry. The Household segment held the largest revenue share in 2025, driven by the growing adoption of plant-based diets and rising health awareness. Households increasingly prefer dairy-free yogurts as daily snacks, breakfast options, or ingredients in smoothies. The convenience of ready-to-eat products and variety of flavors support consistent consumption. Social media and health trend influence also play a role in driving household adoption.

The Food Service Industry segment is expected to witness the fastest growth from 2026 to 2033, driven by the growing inclusion of plant-based options in restaurants, cafes, and hotels. Businesses are responding to increasing vegan and lactose-intolerant customer demand. Dairy-free yogurts are incorporated into breakfast menus, desserts, and specialty dishes. Their use in catering and meal kits is expanding, further supporting adoption in commercial settings.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Store Based and Non-Store Based. The Store Based segment held the largest market revenue share in 2025, driven by the availability of dairy-free yogurts in supermarkets, hypermarkets, and specialty stores. Consumers rely on physical stores for product variety, promotions, and instant access. Retailers also offer loyalty programs and in-store sampling to boost sales. Store-based channels remain critical for brand visibility and consumer trust.

The Non-Store Based segment is expected to witness the fastest growth from 2026 to 2033, driven by the rise of e-commerce platforms, online grocery delivery, and direct-to-consumer subscription models. Online channels allow consumers to conveniently access niche and premium brands. Digital marketing campaigns, personalized offers, and home delivery enhance consumer engagement. This channel also supports subscription models for recurring purchases, promoting customer loyalty and steady revenue growth.

Dairy-Free Yogurt Market Regional Analysis

- North America dominated the dairy-free yogurt market with the largest revenue share of 38.5% in 2025, driven by growing health awareness, increasing lactose intolerance, and the rising adoption of plant-based diets

- Consumers in the region highly value the nutritional benefits, variety of flavors, and convenience offered by dairy-free yogurt products. The widespread availability of almond, coconut, and oat-based yogurts in supermarkets and specialty stores further supports market growth

- High disposable incomes, a preference for organic and fortified products, and strong e-commerce penetration have established dairy-free yogurts as a favored choice for both households and food service providers

U.S. Dairy-Free Yogurt Market Insight

The U.S. dairy-free yogurt market captured the largest revenue share in 2025 within North America, fueled by a shift toward plant-based alternatives and growing consumer focus on gut health. Consumers increasingly prefer yogurts made from almond, oat, and coconut due to their high protein content and probiotic enrichment. The growing trend of ready-to-eat and convenient snack options, along with rising vegan and lactose-free demand, further propels the market. In addition, the strong presence of established brands, combined with innovation in flavors and packaging, is supporting market expansion.

Europe Dairy-Free Yogurt Market Insight

The Europe dairy-free yogurt market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by the rising vegan population, increasing health consciousness, and supportive regulatory frameworks for plant-based products. The demand for clean-label, organic, and fortified dairy alternatives is increasing across countries such as Germany, France, and Italy. European consumers are also drawn to sustainable and ethically sourced ingredients. Growth is seen across both household consumption and foodservice applications, with manufacturers launching innovative flavors and eco-friendly packaging to meet evolving preferences.

U.K. Dairy-Free Yogurt Market Insight

The U.K. dairy-free yogurt market is expected to witness the fastest growth rate from 2026 to 2033, driven by growing awareness of plant-based diets and increasing lactose intolerance. Consumers in the U.K. are prioritizing products that offer nutritional benefits, convenience, and diverse flavor options. The rising demand for organic and fortified yogurts, along with strong e-commerce and retail penetration, is expected to support market expansion. Retailers and food service providers are actively promoting dairy-free alternatives, further stimulating adoption.

Germany Dairy-Free Yogurt Market Insight

The Germany dairy-free yogurt market is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing health awareness and the rising popularity of vegan diets. German consumers are increasingly seeking dairy-free options enriched with probiotics and nutrients for digestive and immune health. Strong demand exists across both retail and foodservice segments, with innovation in oat, almond, and coconut-based yogurts driving adoption. Sustainable sourcing and eco-friendly packaging also resonate strongly with German consumers, supporting market growth.

Asia-Pacific Dairy-Free Yogurt Market Insight

The Asia-Pacific dairy-free yogurt market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing urbanization, rising disposable incomes, and growing awareness of plant-based nutrition in countries such as China, Japan, and India. The region’s expanding middle class and rising health-conscious population are fueling demand for dairy-free yogurt varieties such as soy, almond, and oat. Government initiatives promoting healthy diets and sustainable food systems are further supporting market expansion. Manufacturers are focusing on localized flavors and convenient packaging to cater to diverse consumer preferences across APAC.

Japan Dairy-Free Yogurt Market Insight

The Japan dairy-free yogurt market is expected to witness the fastest growth rate from 2026 to 2033 due to increasing health awareness, the country’s high disposable income, and strong demand for convenient and fortified dairy alternatives. Japanese consumers favor probiotic-rich, plant-based yogurt products for digestive and immune health. The integration of convenient single-serve packaging and innovative flavors is boosting adoption. Moreover, the growing popularity of vegan diets and functional foods is expected to further accelerate market growth in both household and foodservice sectors.

China Dairy-Free Yogurt Market Insight

The China dairy-free yogurt market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rising health consciousness, rapid urbanization, and increasing adoption of plant-based diets. China represents a major market for almond, soy, and coconut-based yogurts, supported by strong domestic manufacturers and competitive pricing. The growing trend of ready-to-eat and fortified yogurt products is driving consumption across households and commercial establishments. Additionally, e-commerce platforms and modern retail chains are enhancing product availability, further propelling market growth.

Dairy-Free Yogurt Market Share

The Dairy-Free Yogurt industry is primarily led by well-established companies, including:

• Danone SA (France)

• COYO Pty. Ltd. (Australia)

• Forager Project (U.S.)

• The Coconut Collaborative (U.K.)

• Lavva (U.S.)

• Amy's Kitchen (U.S.)

• Barry Callebaut (Switzerland)

• Cargill (U.S.)

• Chr. Hansen (Denmark)

• Crowley Foods (U.S.)

• Daiya Foods (Canada)

• Doves Farm Food (U.K.)

• Edlong Dairy Technologies (U.S.)

• Emmi (Switzerland)

• Fonterra (New Zealand)

• Galaxy Nutritional Foods (U.K.)

• Good Karma Foods Inc. (U.S.)

• NANCY’s (U.S.)

• Hain Celestial (U.S.)

• Daiya Foods Inc. (Canada)

• Oatly AB (Sweden)

• YOSO (Germany)

• Amande Cultured Almond Milk (France)

• Vitasoy (Hong Kong)

• WhiteWave Services (U.S.)

• Yoplait (France)

Latest Developments in Global Dairy-Free Yogurt Market

- In September 2025, Silk (U.S.) announced a strategic partnership with a leading health food retailer to expand its distribution network across North America. This collaboration aims to increase brand visibility and accessibility, enabling Silk to reach a wider consumer base. The partnership is expected to drive sales growth, strengthen market presence, and enhance competitiveness in the dairy-free yogurt sector

- In July 2025, So Delicious (U.S.) launched a sustainability initiative targeting a 50% reduction in packaging waste over the next five years. This effort reflects the company’s commitment to environmental responsibility and meets growing consumer demand for eco-friendly products. The initiative is likely to boost brand loyalty, attract environmentally conscious consumers, and reinforce So Delicious’s market position

- In March 2024, Oatly AB (Sweden) introduced a new line of fortified plant-based yogurts enriched with probiotics and vitamins. The launch aims to address the rising consumer focus on digestive health and immunity support. By offering nutritionally enhanced options, Oatly is expected to capture health-conscious segments and increase its share in the competitive dairy-free yogurt market

- In November 2024, The Coconut Collaborative (U.K.) expanded its product portfolio by launching ready-to-drink yogurt smoothies. This development targets on-the-go consumers seeking convenient, healthy options. The expansion is projected to drive sales in retail and foodservice channels while enhancing the brand’s appeal among busy, health-focused customers

- In May 2023, COYO Pty. Ltd. (Australia) upgraded its production facilities to incorporate eco-friendly processes and reduce energy consumption. This initiative supports sustainability goals while maintaining product quality. The move is anticipated to strengthen the brand’s reputation, improve operational efficiency, and align with the increasing consumer preference for environmentally responsible products

- In August 2022, Forager Project (U.S.) launched a nationwide marketing campaign highlighting its organic and plant-based yogurt offerings. The campaign aimed to increase brand awareness and educate consumers on the health benefits of dairy-free products. This initiative helped Forager Project expand its consumer base, reinforce brand recognition, and support growth in the competitive North American market

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.